As a look-back on their first full year as Co-Directors of the SEC’s Division of Enforcement, Stephanie Avakian gave this speech – and Steve Peikin gave this speech – to recap their accomplishments. Stephanie’s speech expands on Enforcement’s “Guiding Principles” for investor protection – and emphasizes that statistics showing a decline in the number of enforcement actions don’t adequately reflect the quality of their efforts. Instead, the goal is to use limited resources to bring “meaningful cases that send clear & important messages.” Here’s the intro:

Last year Steve and I articulated five principles that would guide our decision-making. They are: (1) focus on the Main Street investor; (2) focus on individual accountability; (3) keep pace with technological change; (4) impose sanctions that most effectively further enforcement goals; and (5) constantly assess the allocation of our resources.

I’m going to talk about the Division’s approach to dealing with initial coin offerings (ICO) and digital assets, and second, I will address the Division’s Share Class Selection Disclosure Initiative. These two examples illustrate our approach of identifying challenges and risks facing investors and markets, and developing a response that addresses those challenges in a thoughtful and effective way, and that maximizes our use of resources.

In the context of ICOs, she goes on to discuss non-fraud enforcement actions for ICO registration cases – and says Enforcement isn’t going to shy away from recommending substantial remedies for Section 5 violations. And as I’ve previously blogged, it’s not just issuers who can be the target of an ICO enforcement action. Recent settlements included a hedge fund that violated investment company registration requirements and an unregistered broker dealer.

SEC Enforcement: “Money Isn’t Everything”

John’s blogged that the magnitude of monetary penalties might not be the right way to measure enforcement activity – and Steve Peikin seems to agree. In his recent speech, he elaborated on the full range of relief that the Division of Enforcement recommends to the SEC – and says Theranos is a good example of how customized non-monetary remedies are deployed:

Aspects of the Theranos matter have been covered extensively in other forums. But for today’s purposes, one of the most important elements of the Commission’s settlement with Holmes were undertakings that (1) required her to relinquish her voting control over Theranos by converting her supermajority shares to common shares, and (2) guaranteed that in a liquidation event, Holmes would not profit from her ownership stake in the company until $750 million had been returned to other Theranos investors.

In Theranos, the Commission confronted a situation where, because of the capital structure of the company, Holmes had nearly complete control of the company. And given what we alleged had occurred, it was appropriate to seek relief that protected investors from potential misuse of that controlling position going forward. The undertakings were designed to do exactly that.

Tomorrow’s Webcast: “This Is It! M&A Nuggets”

Tune in tomorrow for the DealLawyers.com webcast – “This Is It! M&A Nuggets” – to hear Weil Gotshal’s Rick Climan, Arnold & Porter’s Joel Greenberg, McDermott Will’s Wilson Chu and Sullivan & Cromwell’s Rita O’Neill impart a whole lot of practical guidance!

Our last “list” blog featured Nina Flax’s morning routine. Now we get to see how Karla Bos starts her day:

OK, here’s the “Bos” edition of the pre-8:30 am accomplishment list. Very different from Nina’s, aside from the requisite coffee and email consumption, but that’s no surprise—she’s a Commuting Supermom and I’m a Work-from-Home Empty Nester. My list looked more like hers when I had a commute and kids at home.

Even so, reflecting on my current list, I realized that 10 years ago I would have read it and totally rolled my eyes, wondering what working person could find the time for all this in the morning and get up so many hours before they really had to. All I can say is that I started to get up earlier and earlier over the years as it dawned on me that doing so allowed me to take control of my day and take care of myself in a meaningful way. So for me, where I am now, this program works:

1. Decide Whether Sleep Will Come Again After 4 a.m. I’ve learned that, as soon as one of my three dogs whimpers or my monkey mind starts jumping, going vertical bears more fruit than chasing a few extra and unlikely minutes of sleep. But if the dogs are quiet, I hold off so the husband can sleep.

2. Get Up by 4:45 a.m. I don’t say “wake up” because I am almost always awake by then. Sometime during the last 10 years I turned into a morning person.

3. Take Dogs Outside. Scan the yard and stand guard for predators (hence, no doggie door) while my little dogs sniff everything as if for the first time. “Oh tree, how I’ve missed you!” I take a moment to enjoy the early morning desert quiet—until the senior dog barks to announce we can go in NOW …

4. Feed the Dogs. For age and health reasons, everyone gets their own custom menu with varying levels of meds and supplements. Start my coffee. Encourage the puppy to eat instead of play.

5. Take Dogs Outside Again. And generally repeat a slightly faster version of step #3. If it’s light enough by now I putter in the yard and make a mental list of what needs attention.

6. Set Out Coffee for My Husband. He’s in the shower about now. He is much less of a morning person (and less of a talker) than I and has a healthy commute. We used to carpool when we worked at the same company, which I thought was great because I could talk and talk and check my email while he drove—but I think he enjoys the quiet time now.

7. Coffee/Digital Content Intake. This means distracting the dogs with dental chews while I drink coffee, check email, and read to get a little smarter about corporate governance and the world. Being in Arizona, I share Nina’s challenge of waking up to east coast days that are already in full swing. Fortunately, our geographically distributed and highly responsive team helps make the time zone balancing act manageable.

8. Throw on Workout Clothes. This is one of the times I listen to a favorite podcast. Once I’d worked from home for a while, I realized I’d stopped doing this, so now I catch up here and there in the morning and whenever I step out of my office for a break.

9. Exercise and Stretch. Some days this means a full-on workout (Empty Nester = spare room for a home gym), some days mostly stretching (which I don’t love because I am not flexible, so podcasts are a great distraction), but it’s a must. It’s key to managing stress, aging, and too much time sitting. Drink water.

10. Check Email.

11. Walk the Dogs. The desert gear required is a separate list but includes big floppy hat, tweezers to remove cactus spines, and a whistle and pepper spray to fend off any aggressive wildlife (which usually keep their distance, but we had a dicey encounter with a group of javelinas and we see coyotes most mornings). Also a headlamp when it’s still dark. Enjoy the stillness and quiet but watch for predators. (You get used to it, rather like walking the streets of NY.)

12. Check Email.

13. Brush Dogs’ Teeth. Owners of small dogs know they require dental vigilance or things get ugly and pricey. Another chance to listen to podcasts.

14. Shower—and Sing! Singing in the shower is another must. Really gets me energized, and I cannot think (worry) about anything when I am belting out a showtune.

15. Meditate for 10-15 Minutes. Mindfulness meditation, which I’m new at, but feels really valuable. One time in the day I don’t make mental lists (well, try not to; like I said, I am new at this).

16. Get Dressed. While I love that this takes far less time and effort now that I work from home, it’s still important to set and adhere to standards, e.g., anything you slept or worked out in is not suitable work attire, and you’re not trying hard enough if your husband comes home and looks startled when he sees you.

17. Eat a Healthy Breakfast. Admittedly this happens at my desk if the preceding 16 activities expanded.

18. Commute to Work. There are things I miss about working onsite with a team, but I adore that my commute simply means walking down the hallway to my home office, where the dogs settle in for a snooze. Power up and get to work!

Nasdaq Proposes Changes to Initial Listing Liquidity Requirements

On Friday, Nasdaq announced that it’s seeking public comment on potential changes to its liquidity requirements for new listings. While all input is welcome, the proposal identifies four topics of particular interest:

– Restricted Shares

– Minimum Investment Value for Holders

– Trading Volume

– Reg A+ Listings & SPACs

Any changes to the rules will apply only to initial listings – not continued listings. Comments are due by November 16th.

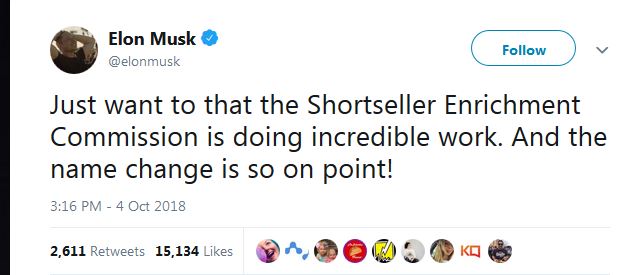

Less than a week into his settlement with the SEC over alleged securities law violations relating to his tweets, Tesla CEO Elon Musk took to Twitter to voice his displeasure with the SEC with this tweet:

Interestingly, in a speech that Liz will blog about next week, Steve Peikin – Co-Director of the SEC’s Enforcement – noted a few days ago that one of the remedies that the SEC obtained is a requirement that Tesla add an experienced securities lawyer to its legal department (see the 4th undertaking associated with fn 8; note that requirement wasn’t noted in the SEC’s press release). I can tell you that Tesla has had one of those already for years. And it doesn’t strike me that Musk is the kind of guy that will listen to his lawyers…

According to news reports, Mark Cuban urged Musk to settle. You may recall that Cuban battled the SEC for years over alleged insider trading – and then Cuban even showed up at the annual “SEC Speaks” conference afterwards. And I even had my own touch of fame after I blogged about Cuban’s settlement and he tweeted at me…

New “Disclosure Simplification” Rules: Effective November 5th

Yesterday, the SEC’s “Disclosure Simplification” rules were published in the Federal Register. They’ll be effective November 5th. I blogged last week about transition issues. We continue to post memos in our “Fast Act” Practice Area…

Group of Investors Files “ESG Disclosure” Rulemaking Petition

Recently, as noted in this press release, a group of investors, state treasurers, public pension funds & unions – representing more than $5 trillion in assets under management – and securities law experts and foundations filed this rulemaking petition with the SEC seeking a standard set of rules requiring companies to disclose environmental, social and governance (ESG) risks.

There were many signatories to this petition. Does that matter? Personally, I don’t think so. Unless they happen to align with the SEC Chair’s rulemaking agenda anyway, rulemaking petitions rarely are acted upon. Remember the rulemaking petition about political contribution disclosures that received over 1 million signatures in support that has gone nowhere…

Certain ISS policies, procedures, and products rely on GICS classifications, including executive compensation peer group formation, equity compensation plan evaluation, and Environmental & Social QualityScore. ISS has issued FAQs designed to answer the most frequently asked questions regarding how the adjustment to GICS structure will impact ISS analyses, and when those changes will be effective.

The FAQs address the following questions:

– How will the new GICS code affect the evaluation of equity compensation plans under ISS’ U.S. Equity Plan Scorecard?

– How will the new GICS code affect the evaluation of equity plans under ISS’ burn rate policy for France?

– How will the new GICS code affect the evaluation of executive compensation?

– How will the new GICS code affect the evaluation of director compensation?

– How will the new GICS code affect Environmental & Social QualityScore?

– How will the new GICS code affect ISS policies, such as the director performance evaluation policy, that examine a company’s TSR performance relative to its industry?

– When will Question 130 in Governance QualityScore, which examines each covered company’s burn rate relative to its industry, be updated to reflect the new GICS structure?

I previously blogged about how Hester Peirce’s dissent from the SEC’s refusal to permit the listing of a bitcoin ETF earned her the moniker “Crypto Mom” from crypto enthusiasts. Judging by a recent speech, Commissioner Peirce digs her new nickname – & wants to be regarded as a “free range” mom who “encourages her child to explore with limited supervision, which requires the acceptance of a certain level of risk.” This excerpt elaborates on what “free range parenting” means when it comes to the crypto:

Steering a speeding machine down the highway is an enormously complex and cognitively-challenging task, one that is dangerous for drivers, passengers, and innocent bystanders. Permitting people to drive means people will be injured and, in too many cases, die. Outlawing driving would save lives, but the costs in terms of lost quality of life of doing so would be enormous, albeit difficult to quantify.

Instead of banning it entirely, therefore, we place reasonable restrictions on driving. Some of us may decide to avoid risks the law allows us to take. A speed limit, after all, is not a mandate. Some of us may choose not to drive at night, in bad weather, or at all. But, barring bad behavior on our part, the choice is ours, not the government’s.

It puzzles me that it is so difficult for those of us who regulate the securities markets to understand this concept; after all, capital markets are all about taking risk, and queasiness around risk-taking is particularly inapt. A key purpose of financial markets is to permit investors to take risks, commensurate with their own risk appetites and circumstances, to earn returns on their investments. They commit their capital to projects with uncertain outcomes in the hope that there will be a return on their capital investment. The SEC, as regulator of the capital markets, therefore should appreciate the connection between risk and return and resist the urge to coddle the American investor.

I get the argument for a lighter regulatory touch, but the analogy between cars and crypto falls flat. I mean, even the most gruesome multi-car pileup never helped trigger a global depression – the same can’t be said for innovative financial instruments.

Ironically, Commissioner Peirce’s remarks came during the month marking the 10th anniversary of the financial crisis. Axios’ Felix Salmon commemorated that milestone by tweeting a copy of what may be the most chilling email ever sent – a message in which one NY Fed official told another that Morgan Stanley had informed Tim Geithner late on Friday, Sept. 20, 2008 that it would be unable to open on the following Monday, and indicating that if Morgan Stanley didn’t open, Goldman Sachs was “toast.”

“Crypto Mom” or “Stakeholder Slayer?”

Commissioner Peirce may like her “Crypto Mom” nickname, but I’d venture a guess she might actually prefer “Stakeholder Slayer.” That’s because in another recent speech, she made it clear that she’s not a fan of the idea of corporate “stakeholders.” Here’s an excerpt:

We have a deep and well-developed body of corporate law. It rests on the assumption that the board owes its principal duty to the shareholders collectively, not to an amorphous group of stakeholders. There is no compelling reason to overturn centuries of settled law, and there are many reasons not to.

Although she objects generally to efforts designed to compel directors to consider ESG issues as part of their fiduciary duties, Commissioner Peirce is particularly critical of California’s new law mandating inclusion of women directors on public company boards. She contends that California’s legislation “effectively forces corporations, including non-California corporations, to consider all women as stakeholders,” and argues that it opens a door to get other “favored groups” included in the stakeholder definition.

Cyber Insurance: GDPR Penalties? They May Not Cover It

One of the most intimidating aspects of the EU’s General Data Protection Regulation – GDPR – is the enormous potential penalties the companies can face for violating its provisions. Companies that run afoul of the GDPR could face fines of up to the greater of €20 million or 4% of their gross annual revenue.

For many companies, this regime means that the most significant potential cyber-related exposure they face is GDPR non-compliance. But this Womble Bond Dickinson memo says that if you expect your cyber insurance policy to protect you, you may be out of luck:

Companies with international exposure should check their cyber insurance policies to determine coverage of EU fines. According to an analysis conducted this summer by Aon, GDPR fines were found to be insurable in only two countries – Norway and Finland – out of the 30 European countries surveyed. In fact, in 20 of the 30 jurisdictions, including the UK, France, Spain and Italy, GDPR fines would specifically NOT be insurable. The other eight jurisdictions were less clear, and may depend on whether a GDPR fine is classified as civil or criminal.

The memo says the answer may be different for U.S. domiciled companies – but even here, the availability and scope of GDPR coverage varies from carrier to carrier.

Recently, Liz blogged about the California Assembly’s passage of Senate Bill 826, which requires exchange-listed companies headquartered in the Golden State to have women on their boards. On Sunday, California Gov. Jerry Brown signed that statute into law.

This excerpt from an article in Sunday’s LA Times summarizes the new law’s mandate:

The new law requires publicly traded corporations headquartered in California to include at least one woman on their boards of directors by the end of 2019 as part of an effort to close the gender gap in business. By the end of July 2021, a minimum of two women must sit on boards with five members, and there must be at least three women on boards with six or more members. Companies that fail to comply face fines of $100,000 for a first violation and $300,000 for a second or subsequent violation.

So how many companies are going to need to add women to their boards? Annalisa Barrett has crunched some of the numbers:

I examined Equilar data for the companies headquartered in California which were in the Russell 3000 Index as of June 2017 and found that, based on current board composition, 377 companies will have to add female director(s) their boards in order to be in compliance with SB 826 by December 31, 2021.

– 66 companies would have to add three women to their boards

– 175 companies would have to add two women to their boards

– 136 companies would have to add one woman to their boards

Annalisa notes that there are likely to be many more companies that will need to take action to comply the statute. Many public companies headquartered in California are too small to be in the Russell 3000 – and the majority of microcap companies (i.e., smaller than $300M in market capitalization) don’t have women on their boards. We’re posting memos in our “Board Diversity” Practice Area.

But Is It Legal? “California Über Alles”

In Gov. Brown’s signing statement, he acknowledged that “serious legal concerns” have been raised about the statute, and that its flaws “may prove fatal to its ultimate implementation.” This recent blog from Cooley’s Cydney Posner reviews some of the statute’s potential constitutional flaws. Here’s an excerpt addressing one of the most frequently cited concerns – the law’s “California Über Alles” provision, which purports to apply its mandate to companies that aren’t incorporated under California law:

You may recall that, generally, the “internal affairs doctrine” provides that the law of the state of incorporation governs those matters that pertain to the relationships among or between the corporation and its officers, directors and shareholders. In case you were wondering how California could profess to control the internal corporate affairs of a foreign corporation, you may not be familiar with the long arm of California’s Section 2115, which purports to apply to foreign corporations that satisfy certain tests related to presence in California (minimum contacts), referred to as “pseudo-foreign corporations.”

Cydney points out that the pseudo-foreign corporations statute used to cause severe problems for law firm opinion committees until the provision was amended to exclude from its application companies listed on the NYSE or Nasdaq. However, the new law expressly applies to these “pseudo-foreign” listed companies.

Cydney says that it is unclear whether courts will view the location of a company’s principal executive office as sufficient to overcome the internal affairs doctrine. Keith Bishop is skeptical that courts will sign-off on the statute – and this recent blog lays out his reasoning.

Transfer Agents: Market Share Leaders

This “Audit Analytics” blog discusses its annual review of 2018 market share leaders among transfer agents. Here’s an excerpt about the leaders for IPO market share:

AST has moved to the top transfer agent of IPO market share, putting Computershare/BNY Mellon into second. Two transfer agents that were in the top last year, Wells Fargo and Citibank, are not top competitors in the IPO market this year. Instead, Vstock Transfer, who was last in the top in 2016, has reappeared. Another notable change is from Deutsche Bank Trust Co Americas/TA, which has made an appearance in the top five for the very first time.

That was fast. Elon Musk apparently thought better of fighting the enforcement action that the SEC announced on Thursday over his tweets – because on Saturday evening, the SEC announced that it had reached a settlement with Musk & Tesla.

What, I’ve got to work weekends now? Broc never said anything about this. . . Anyway, this excerpt from the SEC’s press release lays out the deal’s basic terms:

Musk and Tesla have agreed to settle the charges against them without admitting or denying the SEC’s allegations. Among other relief, the settlements require that:

– Musk will step down as Tesla’s Chair and be replaced by an independent Chair. Musk will be ineligible to be re-elected Chair for three years;

– Tesla will appoint a total of two new independent directors to its board;

– Tesla will establish a new committee of independent directors and put in place additional controls & procedures to oversee Musk’s communications;

– Musk and Tesla will each pay a separate $20 million penalty. The $40 million in penalties will be distributed to harmed investors under a court-approved process.

According to this NYT article, Musk rejected a comparable deal before the the SEC filed its lawsuit. The sticking point was Musk’s unwillingness to accept the SEC’s standard “neither admit or deny” language (no, I’m not kidding).

Steve Quinlivan blogged his take on the settlement. This excerpt lays out the message to public companies with tweeters at the helm – and suggests that another prominent organization could learn a lesson here as well (also see our own new “Social Media Handbook” – and this blog by John Stark):

So the message to public companies is clear: If you have executives out there communicating material information on social media, you need to have disclosure controls and procedures in place to review the information before and after publication. Or at least one or the other. It would seem the White House would benefit from a similar rule.

Poll: Did the SEC Let Musk Off Too Easily?

On Friday, we ran a poll asking whether folks thought Musk should be subject to a D&O bar – 43% said ‘yes’ and 36% said ‘no’ (the rest punted). Now please take a moment to participate in a new anonymous poll:

find bike trails

Our October Eminders is Posted!

We’ve posted the October issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

That was fast. Yesterday, the SEC announced the filing of an enforcement action against Tesla CEO Elon Musk arising out of his ill-considered tweetstorm & subsequent comments about a potential “going private” transaction during the first two weeks of August. The SEC’s complaint makes it clear that Enforcement isn’t messing around – this is a Rule 10b-5 securities fraud case, unaccompanied by any non-scienter based allegations. Here’s an excerpt from the SEC’s press release:

On August 7, 2018, Musk tweeted to his 22 million Twitter followers that he could take Tesla private at $420 per share (a substantial premium to its trading price at the time), that funding for the transaction had been secured, and that the only remaining uncertainty was a shareholder vote.

The SEC’s complaint alleges that, in truth, Musk had not discussed specific deal terms with any potential financing partners, and he allegedly knew that the potential transaction was uncertain and subject to numerous contingencies. According to the SEC’s complaint, Musk’s tweets caused Tesla’s stock price to jump by over six percent on August 7, and led to significant market disruption.

Co-Director of Enforcement Stephanie Avakian added that taking care to provide truthful & accurate information is one of a CEO’s “most critical obligations” – and one that applies equally when communications are made via social media instead of through traditional media. Speaking of issues surrounding the use of social media – be sure to check out our new “Social Media Handbook.”

Musk’s predicament calls to mind another automotive industry visionary with whom he’s been compared – Preston Tucker. Check out this article for an overview of Tucker’s innovative “Tucker Torpedo” & the fallout from the SEC’s 1948 investigation into his company. Of course, let’s not get carried away – Tucker’s story had elements of tragedy to it, but Musk’s is pure farce.

Upping the Ante: SEC Seeks a D&O Bar Against Musk!

Elon Musk is one of the world’s wealthiest people, so financial penalties that might prove ruinous to anyone else may not provide that much of a sting. However, the potential raised by this portion of the SEC’s prayer for relief would definitely leave a mark:

Ordering that Defendant be prohibited from acting as an officer or director of any issuer that has a class of securities registered pursuant to Section 12 of the Exchange Act or that is required to file reports pursuant to Section 15(d) of the Exchange Act.

That’s a D&O bar, and it’s not unusual for the SEC to seek one – in fact, this ’Compliance & Enforcement’ blog says that they are sought in more than 70% of cases involving individual defendants.

But let’s face it, Elon Musk isn’t Joe Bagadonuts – we’re talking about a guy who figured out how to land a rocket standing up. There are few CEOs more closely identified with their companies than Elon Musk, and some question whether Tesla could survive without him. That means the SEC’s decision to pursue a bar raises the stakes for Musk, Tesla, and Tesla’s investors.

Poll: Should the SEC Seek a D&O Bar?

Please take a moment to participate in our anonymous poll:

This WSJ article speculates that the work that companies have done in order to comply with new accounting standards & address the financial statement impact of tax reform may have opened Pandora’s box when it comes to restatements. Here’s an excerpt:

During the first six months of 2018, 65 companies detected accounting mistakes significant enough to require them to restate and refile entire financial filings to regulators, compared with 60 companies for the same period last year, according to Audit Analytics. The Massachusetts-based research firm analyzed disclosures from more than 9,000 U.S.-listed going back to 2005, identifying companies that had to reissue their financials because prior documents were deemed no longer reliable.

The uptick came during a period when finance teams were overhauling corporate accounting paperwork to comply with the new U.S. tax law and new revenue accounting rules. In many instances CFOs and their staffs had to go over past financial reports to recalculate the value of tax credits or liabilities, or to assess how past results would look under new rules.

The article highlights two companies – Seneca Foods & Camping World Holdings – that restated financials based upon issues discovered during efforts to address the new revenue recognition standard (Seneca) and tax reform (Camping World).

We’ve previously blogged about Audit Analytics’ warning that the new revenue recognition standard might result in more restatements – so if this turns out to be a trend, they’ll have every right to say “we told you so.”

SEC Enforcement: A Very Expensive “Fish Story”

The SEC recently announced an enforcement action against SeaWorld & its CEO for alleged disclosure shortcomings associated with the impact of the documentary “Blackfish” on the company’s business. This Ning Chiu blog summarizes the proceeding. Here’s an excerpt:

News articles begin to speculate as early as August 2013 that there may be a link between the film and the company’s declining attendance. That fall, the company’s annual reputation study conducted by its communications department found that its score had fallen by more than 12% from the prior year. This finding was presented to the strategy committee that included the CEO, but was excluded from materials for a later meeting that the chairman of the board attended.

Musical acts and promotional partners started to cancel performances or withdraw from their marketing arrangements, which the SEC believes “should have provided confirmation” that the company’s reputation had been materially damaged by the film. Instead, in articles around the same time, the CEO expressly stated that he could not “connect anything” between the film and any effect on the company’s business. The company also stated in other media that there was “no truth” to the suggestion that the company’s reputation had suffered.

SeaWorld and its CEO agreed to settle the SEC’s charges without admitting or denying the allegations. The company paid a $4 million penalty and the CEO paid $850,000 in disgorgement and prejudgment interest and a $150,000 civil penalty.

Bad News: Give It to ‘Em Straight!

I guess you could say that the theme of today’s blogs is “bad news” – so this recent blog from Adam Epstein about how to deliver that kind of news to investors is probably a good way to close things out. The short answer is “give it to ’em straight.” Adam reviews all the ways he’s seen companies try to spin bad news, and says they just don’t work. Here’s an excerpt:

It doesn’t work. Smart investors have seen this movie before, and it ends badly. Every public company has bad quarters. Great companies face bad news directly, and succinctly, because nothing they say is going to undo the bad results. Every other path destroys trust and erodes value.

The blog acknowledges that sometimes a company’s bad quarter may distract from many other positive developments in the business. If that’s the case, the blog advises that instead of using those developments to spin bad news, management is better off to let those future results speak for themselves when announced.

Today is the “Say-on-Pay Workshop: 15th Annual Executive Compensation Conference”; yesterday was the “Proxy Disclosure Conference” (for which the video archive is already posted). Note you can still register to watch online by using your credit card and getting an ID/pw kicked out automatically to you without having to interface with our staff. Both Conferences are paired together; two Conferences for the price of one.

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take about a day to post the video archives after it’s shown live). A prominent link called “Enter the Conference Here” – on the home pages of those sites – will take you directly to today’s Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: HTML5, Windows Media or Flash Player). Here are the “Course Materials.”

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here is today’s conference agenda; times are Pacific.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if that is possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see this “List: CLE Credit By State.”

Corp Fin Issues CDI on “Disclosure Simplification” Effectiveness

Last week, I blogged that it was unclear when the SEC’s new disclosure simplification rules become effective. Yesterday, Corp Fin resolved that issue with this new CDI:

Question 105.09: On August 17, 2018, the SEC adopted amendments to certain disclosure requirements in Securities Act Release No. 33-10532, Disclosure Update and Simplification. The amendments will become effective 30 days after publication in the Federal Register. Among the amendments is the requirement to presentthe changes in shareholders’ equity in the interim financial statements (either in a separate statement or footnote) in quarterly reports on Form 10-Q. Refer to Rules 8-03(a)(5) and 10-01(a)(7) of Regulation S-X. When are filers expected to comply with this new requirement?

Answer: The amendments are effective for all filings made 30 days after publication in the Federal Register. In light of the anticipated timing of effectiveness of the amendments and expected proximity of effectiveness to the filing date for most filers’ quarterly reports, the staff would not object if the filer’s first presentation of the changes in shareholders’ equity is included in its Form 10-Q for the quarter that begins after the effective date of the amendments. For example, assuming an effective date of October 25, a December 31 fiscal year-end filer could omit this disclosure from its September 30, 2018 Form 10-Q. Likewise, a June 30 fiscal year-end filer could omit this disclosure from its September 30, 2018 and December 31, 2018 Forms 10-Q; however, the staff would object if it did not provide the disclosures in its March 31, 2019 Form 10-Q. (Sept. 25, 2018)

So the Staff says that although the new rules apply to any filings after the effective date, companies can hold off one quarter on the “Statement on Stockholders Equity.” That’s good news, as this Gibson Dunn blog notes, companies with 12/31 fiscal year ends will be able to wait to make the new disclosure until after their 3rd quarter 10-Q. And no, the rules haven’t been published in the Federal Register yet…

SEC Charges 5 Companies With Foregoing 10-Q Auditor Review

Last week, the SEC charged five companies with failing to have their independent auditors review their 10-Q interim financials. This is the first time the SEC has brought enforcement actions for violations of the Regulation S-X interim review requirement – and resulted from a review of filings, Corp Fin comment letters and other metrics that indicated potential violations. Each company agreed to settle the SEC’s charges, with the agency collecting a total of $250k in penalties.

Corp Fin’s New Edgar Guidance for ABS

Recently, Corp Fin issued this set of 12 FAQs for Edgar filings by asset-backed issuers…