This 91-page report from EY – and the related 7-page summary – say that Corp Fin issued 34% fewer comment letters last year. While that was partially due to the long-lasting government shutdown, it follows a 25% drop in the prior year – so there appears to be a trend. Not surprisingly, revenue recognition & non-GAAP were the most frequent comment topics. Here’s the full top 10 (see the report for example comments in each category):

1. Revenue recognition

2. Non-GAAP financial measures

3. MD&A (in order of frequency: (1) results of operations (20%), (2) critical accounting policies and estimates (10%), (3) liquidity matters (8%), (4) business overview (6%) and (5) contractual obligations (2%) – many companies received MD&A comments in more than one category)

4. Fair value measurements (including comments on fair value measurements under Accounting Standards Codification 820 – as well as fair value estimates, such as those related to revenue recognition, stock compensation and goodwill impairment analyses)

5. Intangible assets and goodwill

6. Income taxes

7. State sponsors of terrorism

8. Segment reporting

9. Acquisitions and business combinations

10. Signatures/exhibits/agreements (new to this year’s “Top 10”)

Foreign Nations Might Be Delaware’s New Competition

While you may think of Nevada – or even federal law – as Delaware’s primary competitor in the “corporate law” space, a forthcoming law review article says that non-US jurisdictions are the real threat. Here’s an excerpt:

While Delaware continues to dominate the market with 48.1% of US-listed companies, foreign nations now account for 13.4% of incorporations – more than double the 5.5% of US-listed companies incorporated in Nevada, which has been identified as the only other state besides Delaware actively vying to draw corporations that physically operate outside of its borders.

As this Article will show, offshore incorporation havens in recent decades have built sophisticated legal infrastructures that enable them to compete with Delaware. For one, they have attracted a network of elite foreign lawyers who help lawmakers in these jurisdictions draft “cutting edge” corporate law statutes. These lawmakers also rely heavily on incorporation fees for government revenues, allowing them to credibly commit to retaining laws that are attractive to the private sector.

Because the population of offshore incorporation havens tends to be a fraction of even sparsely populated states in the United States (for instance, as of 2019, the population of the Cayman Islands is 59,613 compared to 961,939 in Delaware and 2,998,039 in Nevada), these jurisdictions can enact legislation swiftly in response to private sector demand. They also do not confront the type of democratic accountability facing large nation states (or large states like New York or California), in part because they specialize in producing laws for corporations that do not physically operate within their territories.

Delaware’s judicial system is often pointed to as a competitive advantage over other states. These jurisdictions compete not by carbon copying Delaware’s judiciary, but rather by offering dispute resolution for a functionally similar to modern commercial arbitration. Like arbitration, courts in offshore incorporation havens swiftly resolve disputes without juries. Judges serving in these courts, like arbitrators, are credentialed business law jurists including partners at major international law firms who fly in from overseas to preside over cases ad hoc. Many legal proceedings take place in secret, and full-length opinions are frequently unpublished or available only to insiders.

I’m admittedly biased due to interning in Wilmington for a Delaware Justice back in the day, but isn’t transparency & predictability still a pretty big advantage? I guess if you can opt out of derivative suits & fiduciary duties, which is the case with many of these incorporation havens, that may matter less.

Last night, the SEC posted this Sunshine Act notice to announce it will hold an open meeting next Tuesday, November 5th to propose rule changes for proxy advisors & shareholder proposal thresholds – here’s the agenda. My blog yesterday included an excerpt from an FT article about what may be in the proposals. Check that out for a possible preview.

We’ll be covering this, along with the SEC’s recent Rule 14a-8 proposal during our upcoming webcast – “Shareholder Proposals: What Now” – on Thursday, November 21st. In that program, Davis Polk’s Ning Chiu, Morrison & Foerster’s Marty Dunn and Gibson Dunn’s Beth Ising will also be discussing Corp Fin’s new approach for processing shareholder proposal no-action requests and the expected impact of Staff Legal Bulletin No. 14K.

SEC Starts Posting “Edgar Is Down” Notices

Just last week, Broc blogged his frustration about how the SEC wasn’t posting “Edgar is down” notices as we thought they would be doing. Yesterday afternoon, the SEC posted their first one:

EDGAR System Technical Difficulties

The EDGAR system is experiencing technical issues, which may impact filers’ ability to make submissions to EDGAR. Our technical staff is working to resolve the issues. We apologize for any inconvenience caused. Please note that updates regarding the resolution of this issue will be posted on this site. Once the outage has been resolved, we will work with filers who are impacted to resolve any impact from the inability to file.

Update – For those Issuers who are unable to furnish or file an Item 2.02 Report on Form 8-K to meet the requirements of paragraph (b)(1) of Item 2.02, but are unable to do so because of these difficulties, the staff will adjust the receipt date of such report so that it will be deemed furnished or filed at the time the Issuer first attempted to submit such report.

Update – The technical issue has been resolved. EDGAR is operating normally. Filers who attempted to file but were unable to do so as a result of the outage should submit their filing as soon as possible, and contact Filer Support at 202 551-8900, or email EDGARFilingCorrections@sec.gov. Please provide the CIK, accession number of the impacted filing.

TCFD: Real-World Disclosures

A few months ago, I blogged about the “TCFD Implementation Guide” – it has annotated mock disclosures that show how companies could present climate-related financial info. Now, SASB and the Climate Disclosure Standards Board (CDSB) are back with this 50-page “Good Practice Handbook.”

The Handbook teases out specific examples of effective reporting from companies around the world. It focuses on the 4 core TCFD elements of governance, strategy, risk management, and metrics & targets.

Although we haven’t yet seen a Sunshine Act notice from the SEC, the Financial Times is reporting that the SEC could propose new rules for proxy advisors & shareholder proposal thresholds as soon as next Tuesday. For now, here’s what’s being reported as part of the proposal:

– Proxy advisors would be required to give companies two chances to review proxy voting materials before they are sent to shareholders

– Shareholder proposal resubmission threshold would increase to 6% approval in year one, 15% in year two and 30% in year three – if a shareholder proposal doesn’t hit those thresholds, companies would be able to exclude proposals on the same subject matter for the next three years

These things are always very speculative – both the substance & timing could change, and nothing’s certain till we see the proposal. The FT article emphasizes that too:

The Commission is expected to vote to put the changes out for comment on November 5, according to the people, who cautioned that the plans and the timing were still in flux and could change before the vote next month.

If the proposal is issued, you can bet we’ll be covering it in our upcoming webcast – “Shareholder Proposals: What Now” – on Thursday, November 21st. In that program, Davis Polk’s Ning Chiu, Morrison & Foerster’s Marty Dunn and Gibson Dunn’s Beth Ising will also be discussing Corp Fin’s new approach for processing shareholder proposal no-action requests and the expected impact of Staff Legal Bulletin 14K.

“Harmonization” of Private Offerings: NASAA Comments on SEC’s Concept Release

Right now, a “requirement” for relying on the Reg D private placement exemption is to file a Form D within 15 days of the date that securities are first sold under the exemption. “Requirement” is in quotes because filing a Form D isn’t a condition to the availability of the federal exemption – but it could disqualify the company from using the exemption in the future, and some state enforcement agencies say that a delinquent Form D kills the preemption the company would otherwise enjoy from state law registration requirements.

So it’s interesting that in its recent comment letter to the SEC’s “Concept Release on Harmonization of Securities Offering Exemptions,” the North American Securities Administrators Association – otherwise known as NASAA, the organization that represents state securities regulators – is recommending an amendment to Regulation D that would require pre-issuance as well as post-closing Form D filings. This Allen Matkins blog gives more details (and here are all the comments the SEC has received so far):

NASAA argues that a pre-issuance filing requirement will “alert regulators that the offering is forthcoming and to provide an opportunity for regulators to investigate the offering if any information in the Form D raises concern”. Form D was originally presented as a tool to “collect empirical data which will provide a basis for further action by the Commission either in terms of amending existing rules and regulations or proposing new ones”. It has evolved, however, into an enforcement tool for securities regulators. See “Is Form D Afflicted With Mission Creep?“

NASAA is also recommending amendments to the definition of “accredited investor” that would raise individual net worth & income requirements, and preserving Rule 504 in its current form. Our “Reg D Handbook” covers all the ins & outs of the current exemption – including the current Form D filing requirements and related “Blue Sky” impact.

“Climate-Change Accounting”: Not Adding Up?

Last week, as this WSJ article reports, Exxon began defending itself in New York state court about whether it improperly accounted for the cost of climate change regulations (they were also sued in Massachusetts). The NY suit was brought under New York’s sweeping Martin Act and arises out of a 4-year investigation – so of course there’s some controversy. According to the article, Exxon has denied wrongdoing – and said a reasonable investor wouldn’t expect to know these details. But then there’s this unrelated Reuters article about how investors want more transparent “climate-change accounting” so they can better understand & price risks. Here’s an excerpt:

Using a broad measure, global sustainable investment reached $30.1 trillion across the world’s five major markets at the end of 2018, according to the Global Sustainable Investment Review. This equates to between a quarter and half of all assets under management, due to varying estimates of that figure.

Condon said most investors were still more focused on returns than wider sustainability criteria but were becoming concerned that companies may expose them to possible future climate-related financial losses.

To try to price risk, the world’s biggest financial service providers are investing in companies which provide ESG-related data. This year alone, Moody’s bought Vigeo Eiris and Four Twenty Seven, MSCI bought Carbon Delta and the London Stock Exchange bought Beyond Ratings. S&P acquired Trucost in 2016. Independent climate risk advisors Engaged Tracking say they attracted two-thirds of their clients in the past year. All six companies provide data, assessments and consulting on the climate exposure of companies or bonds.

To reiterate, these investors weren’t reacting to Exxon’s disclosure specifically, or its court case. And we obviously don’t know what’ll happen there. But if there’s a scale weighing the pros & cons of a more standard disclosure framework for environmental costs & risks, the specter of this type of litigation – and investor appetite – seem to drop in on the “pro” side…

When I first saw this announcement from the SEC’s Enforcement Division about an emergency action to halt an unregistered ICO, I brushed it off as a takedown of yet another fraudulent “crypto” company. But this column from Bloomberg’s Matt Levine points out that this one is different.

In Matt’s words, the company here was doing the “best-practices-y thing” that had been blessed by several law firms. Its offering was structured as a “Simple Agreement for Future Tokens” – as John blogged last year, that’s an approach – based on the popular “SAFE” template for startup financing – that was starting to take off for Reg D token deals. Matt’s explanation of how it works:

1. Sell something—call it a “pre-token”—to accredited investors (institutions, venture capitalists, etc.) to raise money to build your platform. Concede that the pre-token is a security.

2. When the platform is built, it will run on a token, a cryptocurrency that can be used for transactions on the platform and that is not a security.

3. At some point — at or after the launch of the platform — the pre-token (the security) flips into the token (the non-security), and all the people who bought pre-tokens to finance the platform now have tokens to use on it. (Or to sell to people who will use them.)

This seems to honor the intention of securities law—you’re not selling speculative investments to retail investors to fund the development of a new business—while also honoring the intention of the ICO: Your platform is financed (indirectly, eventually) by the people who use it; the people putting up the money do so not in exchange for a share of the profits but for the ability to participate in the platform itself. In this model the pre-token will be called something like a “Token Purchase Agreement” or “Simple Agreement for Future Tokens”: It’s a security wrapper for the eventual utility token.

Unfortunately, the SEC’s complaint took issue with the fact that when the “pre-tokens” here were scheduled to flip into tokens, there would be no established ecosystem for them to trade as currency. Which would seem to be an obvious side-effect of financing a new form of cryptocurrency?

We’re not really sure what to make of this yet – there were some reports that early investors in this offering were flipping their tokens right away, which would be a problem in the SEC’s view. Matt also suggests that maybe the SEC would be more amenable if the pre-tokens didn’t flip until the ecosystem is running robustly. But probably not. John blogged recently on “The Mentor Blog” about how to do a Reg A token offering. So perhaps anyone considering an ICO should take a look at that…

“Reg D” ICOs: What’s the Harm in Trying?

This MarketWatch article notes there’s been a steep drop-off in the number of Reg D token offerings this year. If the Enforcement Division taking issue with a SAFT isn’t enough to put companies off that approach, keep in mind that the remedies in these actions go beyond just halting the current offering:

Until September 30, 2019, SEC enforcement actions in the crypto industry conveyed a consistent message: most crypto is a security, and if a token issuer does not follow the registration requirements of the 1933 Act, the issuer would face significant consequences in the form of substantial penalties, a mandated rescission offer to US investors, a requirement to register the tokens under Section 12(g) of the 1934 Act, and bad actor disqualifications preventing the issuer from future Regulation A and Regulation D offerings.

That’s the intro from this Wilson Sonsini memo – but it does note a recent “aberration” on the remedies front:

On September 30, the SEC announced a settlement with Block.one that did none of these things. Despite finding that Block.one issued tokens that were securities in the United States without complying with registration requirements of the 1933 Act, the SEC: imposed a financial penalty on Block.one that was minor in the context of the total size of Block.one’s capital raise; did not require Block.one to make a rescission offer to investors; did not require Block.one to register its tokens under the 1934 Act; and did not impose bad actor disqualifications under Regulation A and Regulation D.

And, as discussed below, the Block.one Settlement Order omitted any mention of key factual information necessary to support the SEC’s conclusion that the tokens were in fact securities. Equally surprising, the SEC did not address, in any respect, whether new tokens issued being used on a blockchain supported by Block.one are securities, and the SEC took no action (and offered no discussion) with respect to the issuance of those tokens.

What are we all to make from these mixed messages? This Eversheds Sutherland memo says that the most we can take away is that the SEC is evaluating facts in settlement proceedings on a case-by-case basis. If you’re doing an unregistered token offering right now, go document some good facts!

We just wrapped up “Lynn, Borges & Romanek’s 2020 Executive Compensation Disclosure Treatise” — and it’s been sent to the printers. This Edition includes updates to disclosure examples, info about the evolving link between ESG topics & executive pay, and a brand new chapter on hedging policy disclosure. All of the chapters have been posted in our “Treatise Portal” on CompensationStandards.com.

How to Order a Hard-Copy: Remember that a hard copy of the 2020 Treatise is not part of a CompensationStandards.com membership so it must be purchased separately. Act now to ensure delivery of this 1710-page comprehensive Treatise as soon as it’s done being printed. Here’s the “Detailed Table of Contents” listing the topics so you can get a sense of the Treatise’s practical nature. Order Now.

Yesterday, the SEC issued this 168-page proposing release to modernize filing fee disclosure that companies provide – and proposed changes to the agency’s payment method process. Among other changes, the SEC proposes:

– Amend most fee-bearing forms, schedules, statements & rules to require each fee table and accompanying disclosure to include all required information for fee calculation in a structured format (this Cooley blog explains the proposed revised format)

– Add the option for fee payment via Automated Clearing House (“ACH”)

– Eliminate the option for fee payment via paper checks & money orders

I doubt many folks pay via paper check or money orders these days. But I do remember how most paid that way thirty years ago before Edgar was mandatory and registration statements were hand-delivered to the SEC’s filing desk. By the way, calculating filing fees can be hard sometimes – it took me quite a while to put together our “SEC Filing Fees Handbook” to address those complex situations…

Yes, Edgar is Still Down. What If You Need to File Your Earnings Release?

For the life of me, I can’t understand why the SEC can’t get its act together to be transparent about when Edgar is down. A year ago, I blogged about how the SEC would post notices on this page when Edgar goes down “significantly” (and when the problem is resolved). Well, a year has gone by since the SEC indicated they would do this – but there hasn’t been a single notice posted. And as a member posted in our “Q&A Forum” (#10043) yesterday, Edgar was down most of the day – preventing this company from being able to file it’s Form 8-K with an earnings release. Boo, hiss…

September-October Issue of “The Corporate Counsel”

We recently mailed the September-October issue of “The Corporate Counsel” print newsletter (try a no-risk trial). The topics include:

– Beyond the Big 3: The Skinny on Other Standing Board Committees

– Standing Committees v. Special Committees

– Do Boards Establish Additional Standing Committees?

– How Much Authority May the Board Delegate to a Standing Committee?

– Some Things to Think About When Forming a Standing Committee

– Proxy Disclosure

– the Big 3: Other Common Standing Committees

– Key Takeaways About Standing Committees

John has been doing a great job blogging about the interesting varieties of insider trading cases that the SEC has brought in recent years (see this one as an example). It’s amazing to me that folks engaging in insider trading don’t realize how easy it is for the SEC Staff to follow an electronic breadcrumb trail.

Even more amazing is when a former member of the SEC Enforcement Staff is oblivious about how easy it is to follow an electronic trail. Here’s an excerpt from this “FT” story about a former SEC Staffer obstructing justice and ignoring his own electronic footprint (also see this blog for the DOJ complaint):

A former employee of the Securities and Exchange Commission was charged on Wednesday for allegedly leaking information about an investigation into a private equity group that he subsequently joined.Michael Cohn, who was a securities compliance examiner in the SEC’s enforcement division, was accused by federal prosecutors in Manhattan of giving investigative information to senior management at GPB Capital Holdings.

Mr Cohn left the SEC in October 2018 to take a job as chief compliance officer at the company, where he earned $400,000 a year, prosecutors said.“[T]he defendant abused the trust placed in him as an SEC employee, obstructing an active investigation,” said Richard Donoghue, the US attorney for the eastern district of New York. Mr Cohn is charged with obstruction of justice, unauthorised computer access and unauthorised disclosure of confidential information. He was arraigned on Wednesday morning and released on a $250,000 bond.“Mr Cohn is innocent of these charges and looks forward to vindicating himself at trial,” said Scott Resnik, his attorney.

The case is the second in the past two years involving allegations of staffers at the SEC and related institutions leaking information to companies as they sought jobs in the private sector. Last year, former employees of the Public Company Accounting Oversight Board, which is overseen by the SEC, were indicted for leaking information about inspections of audits at KPMG, where they had sought or taken jobs. KPMG agreed to pay $50m to settle the matter with the SEC earlier this year.

Mr Cohn had worked in the asset management unit of the SEC’s enforcement division, which he joined in 2014 from the private sector, according to a January announcement of his hiring by GPB. David Gentile, GPB’s founder, said at the time that Mr Cohn’s “deep knowledge and experience will be valuable to us”. GPB and an outside representative for the group did not immediately respond to requests for comment. A receptionist reached by phone said they would pass on the FT’s request for comment to others in the group.

In March, Investment News reported that the company had acknowledged an unscheduled FBI visit to its offices the prior month. Prosecutors accused Mr Cohn of accessing “numerous SEC databases” in September 2018 to steal information about the commission’s investigation into GPB. At the time, he was interviewing with the company for a position and had told individuals at GBP he had “inside information”, prosecutors alleged. He left the SEC on October 12 last year and accepted a job with CPB four days later, according to the government.

“When Cohn left the SEC to join GPB, he left with more than his own career ambitions,” said William Sweeney, assistant director-in-charge of the FBI’s New York field office, in a statement on Wednesday. “The proprietary information he allegedly retrieved — from databases he wasn’t authorised to access — included compromising information about a GPB investigation and sensitive details related to the same,” Mr Sweeney added.

All of this reminds me of my “Cap’n Cashbags video” that parodies a real-life SEC enforcement action involving napkins & insider trading tips…

Deal Cubes: “Lunch Atop a Skyscraper”!

Every once in a while, I still add deal cubes to my extensive “Deal Cube Museum” (found under the “Photos” tab on our home page). I just love this new one from Jessica Pearlman and Naomi Ogan of Fortive. The deal cube is a three-dimension depiction of the famous “Lunch Atop a Skyscraper.” Corbis Images owns the negative to this famous photo and it sold assets to Unity Glory International – hence, the deal cube in this image…keep sending in those deal cubes!

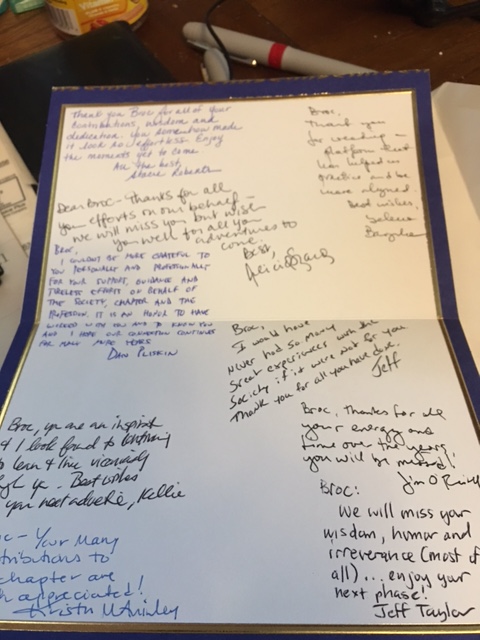

The Beauty of This Job

When I left the board of the MidAtlantic Chapter of the Society of Corporate Secretaries a few years ago (after 15 years of service), I received this wonderful handwritten card (as well as a gift certificate). For a guy that works from home, I haven’t seen a handwritten note for years! I was touched.

A long, long while back, I blogged about the creation of the SEC’s new “Division of Risk, Strategy and Financial Innovation” and noted that the nickname may be an acronym (which wound up as “RiskFin”). Some members back then took the ball and ran with it – one member voted for a nickname of “RSFE” pronounced “ris-fee” or “riskfee.” Another wanted a name change to “Division of Risk, Innovation (Financial) and Strategy,” aka Division of RIFs. One said it sounds eerily close to Riski.org, cool new open-source platform. As I blogged six years ago, that Division has now changed its name to the “Division of Economic & Risk Analysis,” with a nickname of “DERA.”

In that blog, I answered a bonus question of when was the Division of Corporation Finance formed. In response to that, some members noted that there were several divisions before the 1942 birth of Corp Fin, in which Staffers reviewed registration statements – including the “Division of Registration” which was formed in 1935. Old-timers out there, keep ’em coming…

A member reported this a while back: “Thought you’d be amused that when I imported your old podcast regarding the impact of FASB codification on SEC filings into iTunes, Apple classified it as “Blues” music! Such is the life of a corporate lawyer.”

Online Legal Training for New Lawyers: Compare the Pricing…

This blog about a new site offering legal training cracked me up in a few ways. First of all, this type of training is exactly what we’ve been doing both on TheCorporateCounsel.net – and DealLawyers.com – now for some time. And I haven’t sampled the stuff from the new site, but I’m willing to wager without seeing it that our stuff is much more practical.

And secondly, check out the new site’s pricing! Here’s an excerpt from the blog about that:

For a 1000-lawyer law firm, the first topic is $14,000 with the price dropping to $9,000 per topic if the firm subscribes to all six ($45,000). For a 500-lawyer firm, the all-in price is $27,000. For a 100-lawyer firm, the price is $9,000. On a per lawyer basis, this provides larger firms with a slight pricing discount ($45/lwyr for 1000-lawyer firm, $90/lwyr for 100-lawyer firm, $500 for solo practitioners or a 1-person legal department).

Wow! Compare that to the pricing for our popular “In-House Accelerator” Training on this site. That’s free for members of TheCorporateCounsel.net (and it’s popular not just with folks that are in-house, but also with those in firms that want to learn how to think like they’re in-house). And our “Deal U. Workshop” over on DealLawyers.com isn’t free for members of that site – but ours is much cheaper (and includes copies of the “Deal Tales” Paperbacks – a three volume set)…

California Dreaming…

Saw this picture that Jim McRitchie posted of a California license plate:

The SEC has cancelled tomorrow’s open Commission meeting about proposing changes to its whistleblower office. I think this is the third cancelled open meeting in as many months. Does it matter? Not really. Is it worth blogging about? Probably not. Did I blog about it anyway? Yes.

Here’s a few thoughts:

1. Are You Sure It Doesn’t Matter?– For starters, when the SEC has cancelled other open meetings in recent months, it still took action through the seriatim process. So in terms of taking action, the net result was the same. But even if the SEC hadn’t taken action, I don’t think cancelling open meetings by itself is a big deal. Over the decades since the SEC was born, I doubt a Commissioner has ever been persuaded by arguments made at an open meeting to change the way they intended to vote.

In rare cases, a SEC Chair will calendar an open meeting to force an issue to a vote. Then, as the meeting date gets closer, there may be some accommodation that allows the Commission to act by seriatim to get something done.

In the old days, some would travel to DC to attend open meetings – so cancellation would have disappointed those with flights scheduled. But that no longer is an issue because the meetings are webcast and very few people attend in person these days. Plus, I think some people have realized that there simply isn’t much value in “reading the tea leaves” by watching an open meeting in the first place. I haven’t watched one since Bill Donaldson was SEC Chair – that’s 15 years ago.

2. How Many SEC Staffers Attend Open Meetings? – Not many more than those required to go. I do remember attending my first open meeting when I was a Staffer in the late ’80s – the proposal of Regulation S. It was crowded. I got a glimpse of how the SEC operated at the highest level. But my mere attendance as a lowly Staffer was a bit of a novelty – in fact, if my boss knew I snuck down to the open meeting room, I might have been in trouble.

I would wager that well over 90% of the people who work at the SEC have never attended an open meeting (back then and now). There’s no reason for them to see one unless they happen to be curious about what it’s like…

3. Is the SEC Required to Hold Open Meetings? – I blogged about this topic a while back. The upshot is that it’s conceivable that the SEC could take various actions for years without an holding an open Commission meeting. But it doesn’t do so because of the interest in holding the meetings, both within the SEC and outside.

4. Why Does the SEC Keep Calendaring & Then Cancelling Open Meetings?– I have no idea. But it seems a little strange. I’ve never seen so many meetings cancelled in such a short period of time.

Typically, a meeting is cancelled because at least one Commissioner suddenly is unavailable. Particularly if the agenda items are not the “hottest” around, action is then just taken in seriatim. Note that the SEC can take action in seriatim without first announcing (and cancelling) an open meeting.

5. Why Was This Particular Meeting Cancelled?– I doubt that Commissioner unavailability is the reason why this whistleblower meeting was cancelled – the SEC’s cancellation notice indicates that the meeting may be rescheduled for November. So it’s unlikely we shall see action taken in seriatim for this one. My guess is that the SEC needs more time to formulate its proposal.

Audit Committees Must Enforce Auditor Independence Rules? What Gives?

Here’s a note from Lynn Turner: Have you looked at this guidance from the PCAOB Staff? It essentially “guts” the auditor independence rules. It states that if an auditor has violated the independence rules:

1. It must communicate that to the audit committee. No communication of that is required to be made to investors who believe the auditor has complied with such rules.

2. The auditor must have fixed the violation, or alternatively, even thought the violation still exists, must put a plan in place to fix it.

3. The PCAOB Staff still permits an auditor to say in their report they were – and are – independent during the audit engagement time period, even though in fact they are not. This is, at best, misleading to investors. Some might say it’s lying.

This is particularly troublesome because the process relies on an audit committee. Nearly all the audit committees that I have known have scant expertise when it comes to the auditor independence rules. In fact, I can say I have never known an audit committee member who was truly knowledgeable in this area. Even most auditors are not well-versed on the independence rules, although they should be. That is why the SEC required audit firms – back in 2000 – to establish internal quality controls.

However, recent enforcement cases illustrate how these controls are not effectively working inside the big audit firms, as the firms continue to do whatever is necessary to hang onto their audit clients. It is my understanding that auditors do not have to rotate off – or inform any of the investors in – the companies for which their audit independence has been compromised as noted in these enforcement actions.

Today, an auditor can operate under the policy of “It is better to beg forgiveness than to ask for permission.” Investors should be asking if there really are any independence rules.

Meanwhile, two Senators have sent this letter to SEC Chair Clayton asking what is going on with the PCAOB, including why Commissioner Peirce received such a new prominent role overseeing the PCAOB and why the PCAOB’s General Counsel and Enforcement Director positions have been vacant for so long…

SEC Seeking Ideas So Small-Caps Not So Thinly Traded…

Last week, the SEC issued this statement asking for ideas how to boost the liquidity of stocks that currently are thinly traded. See this Mayer Brown memo – and this background paper from the SEC…

There’s nothing I like more than an annual meeting web page that is “usable.” I think that Southern Company’s annual meeting page is one of the best in the US (European companies have been ahead of the game in this area for years). Among the cool features:

– One-stop-shop for proxy & other materials (annual/sustainability reports, etc.)

– Simple presentation of voting items and a link to the voting page have reduced broker non-votes – so the page provides tangible ROI

– HTML is SEO-friendly & easy to read

– Static PDF spreads can be brought to life like this one, making it easy to see who serves on which board committee, etc.

– Graphics & other features can be “reactive”

DOJ’s New “Inability to Pay” Guidance

As noted in these memos posted in our “White Collar Crime” Practice Area, the DOJ recently issued new guidance on how prosecutors should evaluate requests by corporate defendants for a reduction in fines and penalties based on an inability to pay – and announced a restructuring of its “Securities & Financial Fraud Unit” as the “Market Integrity & Major Frauds Unit”…

Tomorrow’s Webcast: “M&A in Aerospace, Defense & Government Services”

Tune in tomorrow for the DealLawyers.com webcast – “M&A in Aerospace, Defense & Government Services” – to hear Hogan Lovells’ Carine Stoick, Michael Vernick, & Brian Curran address some of the unique issues faced by companies doing deals that implicate the government in some way.

Section 404 of the Sarbanes-Oxley Act requires companies to review their internal control over financial reporting and report whether or not it is effective. Non-accelerated filers are required to provide management’s assessment of the effectiveness of their ICFR, while larger companies are required to accompany that assessment with an attestation from their outside auditors.

As it does every year, Audit Analytics took a look at the most recent round of negative auditor attestations & management-only assessments of ICFR. This recent blog reviews the results of the past 15 years of experience under SOX 404, and makes several interesting observations:

– Negative auditor attestations bottomed out in 2010 at 3.5% of filings. They rose fairly steadily and peaked at 6.7% in 2016. After declining to 5.2% in 2017, they rose again last year to 6.0% of filings.

– Negative management-only assessments peaked at a whopping 40.9% of filings in 2014, and have remained at or slightly below the 40% level since that time. In 2018, they declined slightly to 39.6% of filings.

The top reasons for negative audit attestations in 2018 were material or numerous year-end adjustments, shortcomings in accounting personnel, IT & security issues, inadequate segregation of duties and inadequate disclosure controls. Many of these same issues resulted in negative management-only assessments, although accounting personnel issues topped the list here. One item that made the top five reasons for negative management-only assessments that didn’t make the audit attestation list was an ineffective, understaffed, or non-existent audit committee.

Canada Heading for Mandatory “Say-on-Pay-Eh”?

Okay, that title is a very lame Canadian joke, but if you were made to look like a fool on a hockey rink by your Canadian pals as frequently as I am, you’d be looking for a little payback too. Anyway, according to this Blakes memo, recent amendments to the Canada Business Corporation Act may result in a mandatory “say-on-pay” regime for federally chartered Canadian public companies.

Details are in the memo, but what’s more interesting to me is that the memo points out that say-on-pay has already become pretty widespread in Canada among larger cap companies on a purely voluntary basis:

Shareholder Say-on-Pay advisory votes on the compensation practices of public companies in Canada started in 2010 when the major Canadian banks gave their shareholders an advisory Say-on-Pay vote. By 2011, 71 reporting issuers in Canada had adopted Say-on-Pay advisory votes, representing approximately 7% of Canadian listed issuers by number, excluding structured-product issuers and non-listed issuers.

That number has steadily grown each year, such that a total of 220 companies in Canada have now adopted an annual Say-on-Pay advisory vote, including more than 71% of companies in the TSX Composite Index and 52 of the TSX60 Index companies. The adoption of this practice has been completely voluntary thus far, in many cases in response to pressure from institutional investor groups, such as the Canadian Coalition for Good Governance (CCGG), or non-binding votes on shareholder proposals.

Board Elections Less Cozy? Yeah, But Let’s Not Get Carried Away . . .

A recent WSJ headline breathlessly announced that 478 directors failed to get a majority vote this year – and that’s up 39% since 2015. Okay, fair enough – but this Hunton Andrews Kurth memo analyzing the study upon which the WSJ article was based notes that it’s still exceedingly rare for a director to get less than a majority of the votes cast:

How often do directors fail to receive majority support when they stand for reelection? The answer is not often. According to a recent report, however, director “against/withhold” votes are on the rise even though they remain rare. In 2019, 478 directors failed to receive majority support—a small number, but up 38% from 2015. Likewise, the number of directors failing to receive at least 70% support for reelection increased 45% from 2015 to 2019. Overall average shareholder support for directors last year was 95% (votes cast).

The memo breaks down some of the study’s data, and notes that it’s rare for directors to receive less than 70% support – but that data indicates that institutional investors have become more willing to withhold votes from directors in uncontested elections.