Last week, Moody’s Investors Service published a scoring framework for assessing the governance characteristics of public companies not in the financial service area. Moody’s has scored governance for quite some time, but that was for their credit ratings business – this is a new “governance ratings” framework that stands alone. In other words, Moody’s has long incorporated governance issues into their credit ratings, but this is a new “Governance Assessment” which is separate from their credit ratings. But of course, the analysis for the two types of ratings will be somewhat related – you can think of it as a more comprehensive evaluation of the relevant governance factors that already contribute to a rating.

The new “GAs” provide stand-alone assessments of certain aspects of governance risk relative to defined benchmarks considered from the perspective of the potential impact on creditors. Five key components underpin Moody’s GA scores – ownership and control, compensation design and disclosure, board of director oversight and effectiveness, financial oversight and capital allocation, and compliance, controls and reporting. Each of the five components are scored by assessing several subcomponents.

GAs are expressed using a four-point scale between GA-1 and GA-4. Companies assessed at GA-1 have overall governance practices that generally score at the highest level based on our framework. Companies assessed at GA-4 have overall governance practices that generally score at a lower level.

Data used to conduct GA are sourced only from public disclosures like regulatory filings and investor presentations. Where disclosure is lacking, Moody’s GA will penalize the company and result in a less favorable score relative to the benchmark.

5 Takeways From the Proxy Season

In our “Proxy Season Developments” Practice Area,” we are posting the many reports recapping the recent proxy season as usual – including this note from EY’s Center for Board Matters that lists the top five takeaways…

Also see this blog by BlackRock’s Barbara Novick that has a host of stats for the proxy season…

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– What’s the “Long Term Stock Exchange”?

– Director Overboarding: The Latest Stats

– Board Recruitment: More Companies Looking for IR Expertise

– Attorney-Client: Preserving Privilege in a Crisis

– Expert Witnesses Aren’t Always Experts at Being Expert Witnesses

These Principles have also been updated to address SRD II with ‘avoidance’ added to ‘management’ of conflicts-of-interest with regard to the policy which should be disclosed. It also responds to feedback from the 2019 BPP Stakeholder Advisory Panel, acknowledging that conflicts of interest will always exist; therefore it is incumbent upon the BPP Signatories to have proper policies in place to try to avoid such conflicts wherever possible and when they do arise, to be transparent and manage them properly. The 2019 BPP Review Stakeholder Advisory Panel also reiterated the importance of the more stringent updated “Apply and Explain” approach for BPP Signatories to follow in light of SRD II Article 3j in relation to the Principles.

Another further area the updated Principles focused on was delineating the scope of proxy advisors’ responsibilities versus those of investors, in light of continued market misperceptions regarding the alleged overinfluence of proxy advisors and/or alleged “robo-voting” on the part of investors.

CEO Removals: Reputation Beats Financial Performance? Does Your Clawback Match?

During our upcoming “Proxy Disclosure Conference,” we have a panel devoted to the #MeToo era and how it might impact how your clawbacks (should) work. This PwC study shows how more CEOs were dismissed in the last calendar year for ethical lapses than for financial performance or conflicts with the board. So updating your clawback policies might be appropriate…

Reduced Rates Expire at End of This Friday: Our “Proxy Disclosure Conference”

– The SEC All-Stars: A Frank Conversation

– Hedging Disclosures & More

– Section 162(m) Deductibility (Is There Really Any Grandfathering?)

– Comp Issues: How to Handle PR & Employee Fallout

– The Top Compensation Consultants Speak

– Navigating ISS & Glass Lewis

– Clawbacks: #MeToo & More

– Director Pay Disclosures

– Proxy Disclosures: 20 Things You’ve Overlooked

– How to Handle Negative Proxy Advisor Recommendations

– Dealing with the Complexities of Perks

– The SEC All-Stars: The Bleeding Edge

– The Big Kahuna: Your Burning Questions Answered

– Hot Topics: 50 Practical Nuggets in 60 Minutes

Reduced Rates – Act by August 2nd: Proxy disclosures are in the cross-hairs like never before. With Congress, the SEC Staff, investors and the media scrutinizing disclosures, it is critical to have the best possible guidance. This pair of full-day Conferences will provide the latest essential—and practical—implementation guidance that you need. So register by August 2nd to take advantage of the discount.

Don’t forget that Inline XBRL (known as “iXBRL”) tagging will be required for Form 10-Q filings by large accelerated filers this quarter, following the June 15th phase-in period set by the SEC. This means that for many large calendar year-end companies, second quarter 10-Qs should be tagged with iXBRL, as well as the cover page of any “subsequently filed” Form 8-K. Skadden’s Ryan Adams reminds us of a few items that may have gone under the radar as companies begin to implement these changes, including a few potentially surprising new requirements in the exhibit index:

The Instructions to 601(b)(101) of Regulation S-K were recently amended to require that for Interactive Data Files, the exhibit index must include the word “Inline” within the title description for any XBRL-related exhibits. This comes along with an amendment to require a new Exhibit 104 containing cover page iXBRL data. As a result, all 10-Qs filed by companies that are required to comply with iXBRL should include both an Exhibit 101 and an Exhibit 104 – although the EDGAR Filer Manual provides that Exhibit 104 can be included in the Interactive Data File covered by Exhibit 101.

In addition, all 8-Ks that are required to comply with iXBRL should include an Exhibit 104. Not only are these changes somewhat unheralded, but eCFR currently has an incorrect version of the Item 601(a) table – showing that Exhibit 104 isn’t required for 10-Qs or 10-Ks. This is causing a lot of confusion as second quarter 10-Qs get filed.

“Gaming” Tokens Not Securities: Corp Fin’s No-Action Response

Any no-action letter signing off on a token is probably worth noting. Corp Fin issued this no-action response to “Pocketful of Quarters” last week indicating that – based on the facts presented – it wouldn’t recommend enforcement action if the company didn’t register its “gaming” tokens as securities. So this is a “definition of securities” no-action letter. See this blog by Stinson’s Steve Quinlivan…

Brexit Disclosure: New Developments to Consider

Here’s the intro from this blog by Cooley’s Cydney Posner:

With Boris Johnson as the UK’s new PM—and given his enthusiasm for Brexit and threat to leave the EU by October 31 even with a “hard” Brexit—it might make sense for companies to revisit the observations of SEC officials regarding the critical need for thoughtful and specific disclosures about Brexit. Note that the designated new head of the EU commission has said that “another extension [beyond the deadline of October 31] could be granted ‘if good reasons are provided’—such as holding a general election or second referendum.”

Reports from yesterday, however, indicated that Johnson’s election “has been greeted in Brussels with a rejection of the incoming British prime minister’s Brexit demands and an ominous warning by the newly appointed European commission president about the ‘challenging times ahead.’” To be sure, in terms of potential disruption, some practitioners have likened the havoc that Brexit could create to the chaos anticipated from the Y2K bug! But even if that analogy turns out to be a bit too apocalyptic, there’s no question that Brexit, especially a hard Brexit, could have a significant impact on many companies—and not just those based in the UK and EU. With that in mind, companies may want to reexamine and update their disclosures about the potential impact of Brexit on their businesses.

It’s not news to anyone reading this that the legal profession has big problems with depression, substance abuse, and other mental health issues. If you haven’t personally experienced any of these, you know friends or colleagues who have. But the question is, why are these problems so prevalent among lawyers?

This Law.com article is stirring up some controversy over its claims that when it comes to outside counsel, the problem is the client. Specifically, the article singles out law department attorneys as playing a big role in mental health issues among outside counsel. Here’s the gist of the argument:

Client demands for fast turnaround times, even on non-urgent matters, can leave outside counsel in constant crisis mode. That stress can lead to frayed relationships and mental health issues such as depression, addiction and anxiety, which firm lawyers are more likely to experience than corporate in-house counsel.

“We’re on this crisis level all the time because of the expectations coming from the clients,” said Dan Lukasik, the founder of Lawyers With Depression. He said “a change in the relationship” between firms and in-house clients is needed to improve law’s mental health culture.

Client demands are part of the stress equation, but so is the law firm environment, and I don’t think it’s at all fair to point the finger at in-house lawyers. If in-house attorneys set unreasonable expectations, it’s usually because their business people have set unreasonable expectations for them. In my experience, many in-house lawyers go out of their way to let you know if something they’re asking for isn’t urgent, and it’s exceedingly rare to find one who puts you through the ringer just for giggles.

I agree that most corporate lawyers operate “on a crisis level” all the time, but I think that has more to do with how we’re wired than it does with client demands or whether we’re in a law firm or a corporate setting. For instance, even if I know something’s not a crisis, I’ll often just assume the client needs me to attend to it immediately. That’s nuts, but I don’t think I’m alone. A lot of us are introverted, competitive, perfectionist, obsessive about our reputations & terrified of failure. Add in our professional bias toward catastrophic thinking, and you’ve got a bunch of gasoline-soaked rags just waiting for somebody to light a match when it comes to mental health problems.

Quick Poll: Why Do Lawyers Experience Mental Health Issues?

I just gave you my 2 cents about why I think so many of us struggle with mental health issues – check out this ABA Journal article for what other lawyers have to say about this topic. Here’s an anonymous poll so you can provide your thoughts:

survey tool

Transcript: “Joint Ventures – Practice Pointers”

We have posted the transcript for the recent DealLawyers.com webcast: “Joint Ventures – Practice Pointers.” We’ll have our second installment for this topic in an August 6th webcast: “Joint Ventures – Practice Pointers (Part II).”

There’s a great quote from the 5th Circuit’s 1981 decision in Huddleston v. Herman & MacLean that says that “to warn that the untoward may occur when the event is contingent is prudent; to caution that it is only possible for the unfavorable events to happen when they have already occurred is deceit.” That quote pretty much sums up the basis for the SEC’s enforcement proceeding against Facebook that was announced yesterday. Here’s an excerpt from the SEC’s press release:

The Securities and Exchange Commission today announced charges against Facebook Inc. for making misleading disclosures regarding the risk of misuse of Facebook user data. For more than two years, Facebook’s public disclosures presented the risk of misuse of user data as merely hypothetical when Facebook knew that a third-party developer had actually misused Facebook user data. Public companies must identify and consider the material risks to their business and have procedures designed to make disclosures that are accurate in all material respects, including not continuing to describe a risk as hypothetical when it has in fact happened.

The misleading disclosures arose out of Cambridge Analytica’s unauthorized use of Facebook user data. Facebook allegedly found out about Cambridge Analytica’s antics in 2015, but didn’t revise its disclosure until two years later. Facebook consented to a “neither admit nor deny” settlement that, among other things, enjoins it from future violations of Section 17(a)(2) and (3) of the Securities Act and Section 13(a) of the Exchange Act & various rules thereunder.

The company also agreed to pay $100 million to settle the charges, which sounds like a lot, but is chump change to Facebook. After all, the company also agreed yesterday to pay a $5 billion fine to settle FTC charges arising out of customer data privacy lapses. Still, it seems to me that the real elephant in the room may not be the size of the settlement, but the fact that no individuals were named.

The SEC almost always names individuals in corporate disclosure cases, although it didn’t do so in last year’s high-profile data privacy case against Altaba (Yahoo!). In any event, there’s nothing in the press release to suggest that actions against any individuals are contemplated – despite language in the complaint to the effect that “more than 30 Facebook employees in different corporate groups including senior managers in Facebook’s communications, legal, operations, policy, and privacy groups” were aware that Cambridge Analytica had improperly been provided with user data.

The FTC Gives Facebook a New Board Committee!

Speaking of that FTC settlement, Bloomberg’s Matt Levine points out in his column that it has imposed some interesting governance obligations on Facebook that may curb some of Mark Zuckerberg’s power. One of the conditions imposed under the terms of the settlement is a new board privacy committee that is intended to be difficult for Zuckerberg to mess with. Here’s an excerpt from the FTC’s statement on the settlement:

The order creates greater accountability at the board of directors level. It establishes an independent privacy committee of Facebook’s board of directors, removing unfettered control by Facebook’s CEO Mark Zuckerberg over decisions affecting user privacy. Members of the privacy committee must be independent and will be appointed by an independent nominating committee. Members can only be fired by a supermajority of the Facebook board of directors.

Here’s Matt’s take on the independent privacy committee requirement:

The upshot is … look, it is not entirely clear to me what the upshot is; we’ll see what happens. But my rough analysis is that if Zuckerberg wanted to do a bad privacy thing, and the independent privacy directors told him not to, he’d have a tough time of doing it. He couldn’t remove the independent privacy directors from their posts.

Perhaps he could remove them from the board, but he’d have a hard time replacing them, because the independent nominating committee has “the sole authority” to pick new directors. I suppose he could replace the nominating committee too. These provisions aren’t ironclad. But surely their purpose really is to take the final authority over one aspect of Facebook out of the hands of Zuckerberg.

BlackRock: “Move Along – Nothing to See Here. . .”

According to this recent Harvard Governance Blog from its Vice Chair, BlackRock would like you to know that it & the rest of the Big 3 are really small players in the grand scheme of things:

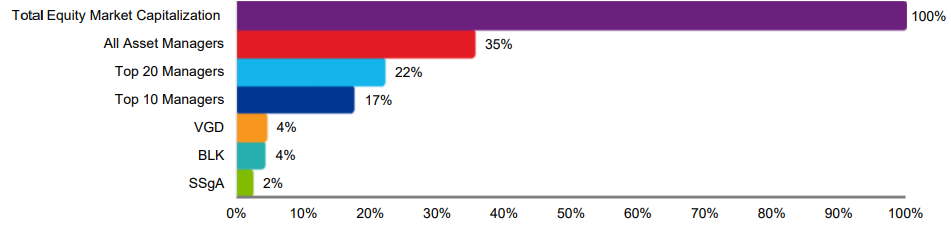

As index funds are currently growing more quickly than actively managed funds, some critics have expressed concern about increasing concentration of public company ownership in the hands of index fund managers. While it is true that assets under management (or “AUM”) in index portfolios have grown, index funds and ETFs represent less than 10% of global equity assets. Further, equity investors, and hence public company shareholders, are dispersed across a diverse range of asset owners and asset managers.

As of year-end 2017, Vanguard, BlackRock, and State Street manage $3.5 trillion, $3.3 trillion, and $1.8 trillion in global equity assets, respectively. These investors represent a minority position in the $83 trillion global equity market. As shown in Exhibit 1, the combined AUM of these three managers represents just over 10% of global equity assets.

Umm, gee – isn’t 10% of all the equity assets in the world kind of a lot? I don’t know why we’re supposed to take a lot of comfort from that number – particularly since the Big 3 reportedly control 25% of the stock in the S&P 500 and are on course to increase that stake to more than 40% over the next two decades. These numbers aren’t small.

The blog also says that those AUM numbers are misleading, because they represent “a variety of investment strategies, each with different investment objectives, constraints, and time horizons. For example, BlackRock has more than 50 equity portfolio management teams managing nearly 2,000 equity portfolios.” That’s great – but when Larry Fink comes out with annual letters telling boards of portfolio companies “how things are gonna be,” those 2,000 equity portfolios look pretty monolithic.

By the way, if this “50 portfolio managers/2,000 portfolios” pitch sounds familiar to you, it may be because at some point you heard the same pitch from one of the Big 3 when it was lobbying your client to allow it to go over a poison pill threshold. At least that’s where I first heard it.

It looks like a token issuer finally crossed the public offering goal line – at least when it comes to clearing Corp Fin’s review process. This Morrison & Foerster memo has the details. Here’s an excerpt:

On July 10, 2019, Blockstack Token LLC (“Blockstack”), a wholly-owned subsidiary of Blockstack PBC, a Delaware public benefit corporation, became the first company to have an offering of digital assets qualified by the U.S. Securities and Exchange Commission (“SEC”) under Regulation A.

Blockstack is a technology company that offers an open-source blockchain-enabled network for developers to build and publish their own decentralized applications. According to Blockstack’s website, over 165 applications have been built on the Blockstack platform. Purchasers of Blockstack’s tokens (“Stacks Tokens”) will be able to use the tokens on its platform.

Token offerings have been under increasing scrutiny, especially with respect to whether or not tokens are securities. In its offering circular disclosure, Blockstack acknowledges that the Stacks Tokens are characterized as investment contracts under the Howey test, while noting that the Stacks Tokens “will not have the rights traditionally associated with holders of debt instruments, nor…equity.” The disclosure, in its discussion about the nature of Blockstack’s decentralized network, also references the SEC’s recent guidance on evaluating whether digital assets constitute securities for purposes of the Securities Act of 1933.

Although there have been a boatload of Reg D token offerings, this is the first one that’s cleared SEC review. Here’s a copy of the company’s preliminary offering circular. As to how long the process took, the answer is about 3 months.

It appears that the initial Form 1-A filing was made on April 11, 2019. At least one substantive amendment to the filing was made in May, but the filing history is a little convoluted, because the deal originally involved a subsidiary entity & was converted to an offering by the parent company shortly before the SEC issued its qualification order. The subsidiary ultimately withdrew its filing, but the back & forth between two filers makes it difficult to determine how much of the time between filing and qualification was attributable to the Staff’s review process.

Registered ICOs: And Then There Were Two!

Blockstack may have been the first ICO to clear SEC review, but this Proskauer blog says that it had company just a day later:

The SEC also qualified the Regulation A offering circular of YouNow, Inc. (“YouNow”), for up to $50 million worth of Props Tokens (“Props”). Rather than solicit cash (or cryptocurrency) consideration for the sale of Props, YouNow and its affiliate, The Props Foundation Public Benefit Corporation, will use YouNow’s Regulation A program solely to distribute Props as rewards and grants to users, developers and other contributors within YouNow’s network of consumer-facing digital media applications.

Meanwhile, back in unregistered token deal land. . .

Blue Sky: New Jersey Sues Issuer of Unregistered Tokens

The SEC’s high-profile enforcement actions involving digital assets get most of the limelight, but as we’ve previously blogged, state securities regulators have been extremely active on the enforcement front when it comes to token deals. Last week, it was New Jersey’s turn to bring the hammer down. Here’s an excerpt from this “Modern Consensus” article describing the Garden State’s recent action:

New Jersey got in on the cryptocurrency offering enforcement action on July 18, suing blockchain-based online rental marketplace Pocketinns for an unregistered sale of securities last year. The state’s attorney general, Gurbir Grewal, was joined by the New Jersey Bureau of Securities today in announcing a three-count enforcement action against Princeton-based Pocketinns and its president, Sarvajnya Mada, over the January 15-31, 2018, sale of $410,000 in PINNS Tokens in an initial token offering.

The U.S. Securities and Exchange Commission (SEC) has brought several similar suits, initiating a high-profile action against blockchain instant messaging service Kik in June for its $100 million ICO in 2017. The agency released a long-awaited “plain English” guide defining when an ICO is a security in April.

Aside from violating the Garden State’s Uniform Securities Law by failing to register the offering, Grewal alleged that Mada acted as an unregistered agent and Pocketinns employed an unregistered agent during the sale.

The article says that the Pocketinns deal wasn’t very successful – it raised less than 1% of the $46 million it sought. But on the other hand, the company appears to have been extremely successful in buying itself all sorts of trouble.

Last week, Liz blogged about a recent rulemaking petition filed by a coalition of labor & progressive groups requesting the SEC to repeal & replace the Rule 10b-18 “safe harbor” under which most buybacks have been conducted.

The request to “repeal” 10b-18 is pretty straightforward, but what’s the “replace” part of the equation supposed to look like? The petitioners suggest that the SEC look at some 1970s-era proposals to limit buybacks, and point out that those proposals included:

– Limiting repurchases to 15 percent of the average daily trading volume for that security.

– Creating a narrower safe harbor and allowing repurchases that fall outside this safe harbor to be reviewed and approved on an individualized, case-by-case basis.

– Providing that repurchases inconsistent with the safe harbor are expressly “unlawful as fraudulent, deceptive, or manipulative.”

– Requiring various disclosures, including whether any officer or director is purchasing or disposing of the issuer’s securities, the source of funds to be used to effect the repurchases, the impact of the repurchases on the value of the remaining outstanding securities, and specific disclosures for large repurchases.

Companies continue to repurchase “massive amounts” of their own stock, and the market seems to be addicted to buybacks as well. So far, the SEC hasn’t seemed inclined to do much to further regulate buybacks, and tinkering with 10b-18 seems unlikely. But a presidential election’s looming, buybacks are getting clobbered in the media, & Democratic presidential hopefuls have them in the cross-hairs. When you throw into the mix the recent introduction of legislation that would ban open market buybacks, the SEC may at some point be faced with a situation where if it doesn’t act, Congress might.

ISS Policy Survey: Board Gender Diversity, Over-Boarding & More

Yesterday, ISS opened its “Annual Policy Survey.” In recent years, ISS used a 2-part survey, with a relatively high-level “governance principles survey” accompanied by a more granular “policy application survey.” This year, ISS is using a single survey with a more limited number of questions. ISS may have streamlined the process, but this excerpt addressing the topics covered in the survey shows that they’ve still covered quite a bit of ground:

Topics this year cover a broad range of issues, including: board gender diversity, director over-boarding, and director accountability relating to climate change risk, globally; combined chairman and CEO posts and the sun-setting of multi-class capital structures in the U.S.; the discharge of directors and board responsiveness to low support for remuneration proposals in Europe; and the use of Economic Value Added (EVA) in ISS’ quantitative pay-for-performance, financial-performance-analysis secondary screen for companies in the U.S. and Canada.

As always, this is the first step for ISS as it formulates its 2020 voting policies. In addition to the survey, ISS will gather input via regionally-based, topic-specific roundtables & calls. Interested market participants will also have an opportunity to comment on the final proposed changes to the policies.

SEC “Short- v. Long-Term” Roundtable: So What Happened?

Last week, the SEC hosted its roundtable on short-term v. long-term management of public companies. As Broc blogged when the roundtable was announced, the roundtable follows the SEC’s December 2018 request for comment on earnings releases & quarterly reporting. If you’re looking for a fairly detailed review of the discussion at the roundtable, check out this recent blog by Cooley’s Cydney Posner.

Following the lead of other federal law enforcement agencies, the SEC is looking to increase its capabilities when it comes to monitoring social media platforms. Here’s an excerpt from this GCN article:

The Securities and Exchange Commission also issued a sources sought notice for a commercial, off-the-shelf social media monitoring subscription to help it track emerging risk areas and activities of market participants to identify potential securities law violations.

Less interested in Twitter than the FBI, the SEC wants the ability to monitor Facebook, Instagram, YouTube, LinkedIn, and Reddit as well as public forums, blogs and message boards. It also requests sentiment analysis capabilities and the ability to identify bot accounts and fake user accounts. Data should be available through an application programming interface as well as through a browser.

I don’t know if anybody in SEC procurement is reading this, but I’ve got an idea that will save the taxpayers a lot of money. If you’re interested in “sentiment analysis capabilities,” don’t bother buying some crappy software license – just click on any random “Me on Facebook v. Me on Twitter” meme. It will tell you everything you need to know. You can Venmo me my reward money along with the thanks of a grateful nation.

Tomorrow’s Webcast: “Company Buybacks – Best Practices”

Tune in tomorrow for the webcast – “Company Buybacks: Best Practices” – to hear Skadden’s Josh LaGrange, Hunton Andrews Kurth’s Scott Kimpel, Simpson Thacher’s Lee Meyerson and Foley & Lardner’s Pat Quick provide practical guidance about how to conduct a stock repurchase program, including analysis of whether it’s the best use of funds.

Every proxy season, Corp Fin responds to somewhere between 200-400 no-action requests about shareholder proposals. Earlier this year, we blogged several times about how the government shutdown upended the process. And even though the Staff got back to “business as usual” when the shutdown ended, they had to be even more efficient given the time constraints – and that experience might have contributed to Corp Fin considering whether to rethink their approach to Rule 14a-8 no-action requests.

As you can hear at the 29-minute mark of this taping of a Chamber event a few days ago, SEC Chair Clayton & Corp Fin Director Hinman commented that they’re considering changing some aspects of their “referee” role (my word, not theirs) – so that, like other types of no-action requests, Corp Fin wouldn’t respond to every Rule 14a-8 submission. Rather, they’d focus on requests that involve “novel” issues and encourage companies & proponents to work things out themselves. Bill says they’re seeking input from the community on how they might change their approach.

As I blogged during the shutdown, companies continue to be very cautious about excluding proposals without first obtaining Staff no-action relief. Some speculate that we’ll see more litigation if Corp Fin does change their role and isn’t as involved – especially on matters that involve tough judgment calls. Any changes in Corp Fin’s role is bound to have a variety of views as this area is always contentious when change is considered, particularly if the SEC’s role might change.

How Asset Managers Feel About “Activists”

John’s blogged on DealLawyers.com that activist hedge funds don’t actually do much to improve company performance. But according to this SquareWell Partners survey (download required), the perception – at least among “active” asset managers – is that these funds are a useful market force, even if they have a short-term, selfish interest.

For that reason, it’s becoming more common for asset managers to align with activists on proxy fights and proposals if they agree with the substance of the activist’s argument – especially on governance & strategic matters. Here’s some interesting takeaways that can help you form alliances when you need them (this was also a topic covered earlier this week in our DealLawyers.com webcast – “How to Handle Hostile Attacks” – stay tuned for the transcript):

– 81% of investors expect companies to engage after they’ve analyzed the analyst’s arguments & formed a strategic response – i.e. don’t rush into a “PR War” – but also know that investors will engage with an activist even before the campaign is public

– 64% of active managers expect to engage with independent directors

– Investors consider a number of factors when assessing a targeted company – the top ones are company performance versus peers, management & board quality, and engagement history – they also look to broker reports, proxy advisors, media outlets & social media

– Investors are mixed on whether poor TSR is a dealbreaker – they’ll also consider ratios that show profitability, efficiency, debt & liquidity

– In addition to capital allocation decisions, active managers are most attuned to governance issues such as collective board expertise, board independence, chair quality and executive pay

Convertible Debt: Still a Good Way to Raise a Buck (or a Million)

This Fenwick survey looks at the terms of 100 convertible debt deals last year – for first-money and early- and late-stage bridge deals. Here’s some key findings:

– Year over year, deal sizes have continued to increase. The median overall deal size this year is up 14%, from $1.4 million to $1.6 million

– Conversion discounts are increasingly common, even in later-stage debt issuances, as is the practice of pairing the discount with a valuation cap

– In change-of-control situations, such as the sale of a company, most deals provide for a premium payout that is a multiple on top of the repayment of the principal balance. The number of deals giving a premium, as well as the median premium amount has remained steady year over year; however, this year the low end of the premium spectrum dropped from 25% to 10%

– Only 11% of deals used a valuation cap as a standalone provision in the absence of a conversion discount

At the recent Society conference, shareholder proposals – in particular, exclusions based on “micromanagement” – were a hot topic. I’ve blogged that last year’s Staff Legal Bulletin No. 14J revived that prong of Rule 14a-8(i)(7)’s “ordinary business” test.

Corp Fin Staffers have explained that proposals may be excludable due to “micromanagement” if they unduly limit management’s discretion – e.g. by advocating for specific methods or policies rather than deferring to the company to determine how to address a topic. They’ve also said that the complexity of the underlying subject matter doesn’t impact the analysis. And this 46-page Sullivan & Cromwell memo about trends in shareholder proposals looks at how “micromanagement” has been applied in some recent no-action letters.

Not everyone agrees with how things are playing out. For example, the Council of Institutional Investors recently submitted a comment letter to Corp Fin that frames the Staff’s approach as an arbitrary “too complex for shareholders” test – and requests that the Staff again revisit its approach to the rule. Specifically, CII takes issue with the Staff’s no-action relief for proposals relating to the use of non-GAAP adjustments in incentive plans (the topic of a rulemaking petition that CII filed with the SEC in April) – as well as requests for companies to report on greenhouse gas emissions. Here’s an excerpt:

With regard to the each of the Devon and Exxon proposals, the Staff said that, “by imposing this requirement, the Proposal would micromanage the Company by seeking to impose specific methods for implementing complex policies in place of the ongoing judgments of management as overseen by its board of directors.” [6] The Staff used the word “impose” twice in this sentence, but that doubling-down does not obviate the fact that the precatory recommendation would not impose anything on the company, other than for management to place the item on its proxy card and include the proposal and supporting statement in the proxy statement. These are requests to the boards on a major public policy issue, not directives.

Nor, for that matter, do the proposals require “specific methods.” The proposals thread the needle between vagueness and recommending overly specific policies. They do not suggest specific goals or a timetable, but rather frame a general structure, well understood by investors, for disclosure of goals.

Mandatory ESG Disclosure: Coming to an SEC Filing Near You?

Last week, the House Financial Services Committee debated five draft bills that would require companies to disclose information about climate change risk, political contributions and other ESG topics (you can also watch this week’s committee markup). This Davis Polk blog summarizes the hearing:

The committee memorandum prepared by the majority staff prior to the hearing stated that “investors have increasingly been demanding more and better disclosure of ESG information from public companies.” The target for improving this disclosure has been the SEC, which received an October 2018 petition from a coalition of investment managers, public pension funds and non-profit organizations requesting that the agency develop a robust ESG disclosure framework. Representative Juan Vargas (D-CA) noted in his remarks that this petition was the impetus for his draft legislation, ESG Disclosure Simplification Act of 2019, one of the bills considered at the hearing.

Several committee members on both sides of the aisle noted that, as interest in ESG disclosure rises, some public companies have responded by voluntarily adding these types of issues to their reporting efforts. However, debate ensued when considering that the draft bills would mandate this type of disclosure for all public companies. Issues raised during the question and answer period included:

– Whether mandated disclosure is necessary given current voluntary disclosure practices;

– The potential increased regulatory burden of these disclosures, which could negatively impact U.S. IPO markets; and

– Whether ESG issues qualify as material information for investors.

This column from Bloomberg’s Matt Levine points out that advice to quantify & disclose climate change risks might be something that companies hear from management gurus – and certainly some of their investors. But that has a different ring than an SEC mandate – especially if the underlying goal is to “solve climate change through the mechanism of corporate disclosure.” If regulating through securities laws ends up being our best hope to solve big problems, yikes – but at least we have a lot of thoughtful people in the field. And some even think a uniform ESG disclosure framework would help companies.

More on “California Reports on Mandatory Women Directors”

Last week, Broc blogged about discrepancies in the first “board diversity” report that the California Secretary of State published under new Section 301.3(c) of the California Corporations Code. A Secretary staffer later spoke with Cooley’s Cydney Posner to explain why the report looks the way it does – here’s an excerpt from her blog:

First, in the methodology, the Secretary acknowledges that there are gaps in available data because of the various filing deadlines: Forms 10-K are due, generally depending on the size of the company’s public float, 60, 75 or 90 days after the end of the company’s fiscal year, and the deadline for filing the California Statement is 150 days after the end of the company’s fiscal year. Accordingly, in some cases, the representative indicated, companies that may have their principal executive offices in California may not have filed their 10-Ks or California Statements during the designated review period and, as a result, their data was not included. (But there still appeared to be some unexplained omissions from the lists.)

Second, according to the representative, because of the language in the statute defining “female” as “an individual who self-identifies her gender as a woman, without regard to the individual’s designated sex at birth,” the Secretary is not reviewing 10-Ks or proxy statements to determine whether a company is compliant with the new board composition requirement. Rather, the Secretary is determining compliance based only on the California Statement, which, since March, has included a specific inquiry regarding the number of “female” directors.

Third, the California Statement is required to be filed by both foreign and domestic corporations and, if a company replied to the question regarding the number of female directors, even if it indicated that its principal executive offices were not located in California, the Secretary included that company on the compliant list; i.e., foreign corporations were not screened out. For the March update, the Secretary plans to provide a separate list of companies that report compliance but do not have principal executive offices located in California.

We should expect that some timing issues will continue to affect the March 1, 2020 update report. Notably, given the process the Secretary is following, current information from the California Statement regarding compliance for 2019 may not be available for the 2020 update report for companies with calendar-year FYEs, among others. For example, companies with calendar-year FYEs will have filed their California Statements in the first half of 2019, but if they do not add a female director and become compliant until, say, the third quarter of 2019, they will not have reported that compliance on their California Statements in time for the March 1, 2020 update (unless they were to file early). As of now, the Secretary does not intend to develop a new separate filing for purposes of soliciting the relevant information on board gender diversity on a more timely basis, but it can’t be ruled out. However, the Secretary does contemplate some revisions to the California Statement, currently expected to be in place by the beginning of 2020. Keep in mind also, that, no fines should be imposed until the Secretary adopts appropriate regulations, and my understanding is that the process of developing regulations has not yet begun.

California won’t be the only state requiring reports on board diversity – the Illinois General Assembly recently passed its own “Diversity Disclosure Bill,” which will require companies headquartered in that state to include diversity info in annual reports filed with the Secretary of State. However, as this Vedder Price memo explains, the version of the statute that ultimately passed in the “Land of Lincoln” doesn’t mandate the inclusion of women or minorities on boards or fine companies that fail to achieve a statutory target, which had been part of the original bill. At the federal level, the House Financial Services Committee has also passed a couple bills on the topic…

{kind=link}