Yesterday, as noted in this press release, the SEC proposed pay-for-performance rules as required by Section 953(a) of Dodd-Frank. The vote was 3-2, with Commissioners Gallagher & Piwowar dissenting. Here’s statements by Chair White and Commissioner Stein.

– Proposed rules rely on Total Shareholder Return (TSR) as the basis for reporting the relationship between executive compensation and the company’s financial performance.

– Based on the explicit reference to “actually paid” in Section 14(i), the proposed rules exclude unvested stock grants and options, thus continuing the trend to reporting realized pay. Executive compensation professionals will need to sharpen their pencils to explain the relationship between these figures and those shown in the Summary Compensation Table.

– For equity-based compensation, companies would use the fair market value on date of vesting, rather than estimated grant date fair market value, as used in the SCT.

– Proposed rules also would require the reporting and comparison of cumulative TSR for last 5 fiscal years (with a description of the calculations).

– Proposed rules would require a comparison of the company’s TSR against that of a selected peer group.

– Proposed rules would require separate reporting for the CEO and the others NEOs – allowing use of an average figure for the other NEOs.

– Proposed rules would require the use of an interactive data format (ie. XBRL)

– Compensation actually paid would not include the actuarial value of pension benefits not earned during the applicable year.

– Proposed rules would phase-in the number of years covered. For example, in the first year for which the requirements are applicable for larger companies, disclosure would be required for the last 3 years only – with it rising eventually to five years worth of information eventually. For smaller reporting companies, they would start with two years worth of information – eventually moving to three years worth.

– Proposed rules exclude foreign private issuers and emerging growth companies, but not smaller reporting companies. However, the proposed rules would phase in the reporting requirements for smaller companies, require only three years of cumulative reporting, and not require reporting amounts attributable to pensions or a comparison to peer group TSR.

The proposing release will be published in the Federal Register within the next week, followed by a 60-day comment period (here’s our checklist to guide you in drafting comments to the SEC on a rulemaking). Depending on the nature and extent of the comments received, it’s possible that the SEC could adopt final rules sometime in the Fall. Assuming everything goes smoothly, it’s possible that the rules could be in effect next year. As we all know, however, things rarely go as planned…

May-June Issue: Deal Lawyers Print Newsletter

This May-June Issue of the Deal Lawyers print newsletter includes:

– M&A Antitrust Playbook for In-House Counsel

– Managing Regulatory Risk in Bank M&A

– Rep & Warranty Insurance: Negotiating Tips & Market Trends

– European M&A Dos & Don’ts for Non-European Buyers

– Break-Up Fees in Delaware: A Delicate Balance for All Parties

If you’re not yet a subscriber, try a no-risk trial to get a non-blurred version of this issue on a complimentary basis.

Cap’n Cashbags: Just a Lil Case of Peer Envy

As noted in this 20-second video, Cap’n Cashbags is keeping a close eye on the pay levels of the other CEOs in his industry (stay til the end for the blooper!):

At ten companies where shareholders have cast votes on proxy access shareholder proposals this season, four companies received more votes in favor of the proposal than against it, while a majority of shareholders did not support the proposal at six companies.

Counting only “for” and “against” votes, Arch Coal’s proposal received the lowest support at 36%. The company had previously adopted proxy access bylaws allowing shareholders owning at least 5% of shares holding for three years to nominate access candidates, with a maximum number of 20 shareholders permitted to aggregate their holdings.

Other proposals that did not receive majority support ranged from 39% in favor at Apple, which we previously discussed here, and 42% to 46% support at Domino’s Pizza, PACCAR, Cabot Oil & Gas and VCA. At three companies, the shareholder proposals received 53% to 67% in support. AES had both the shareholder proposal and a separate non-binding management proposal to adopt proxy access with an alternative 5% ownership threshold. That management proposal was favored by 36% of shareholders, while the shareholder proposal received 66% of the “for” votes. The company also had two special meeting proposals – one shareholder proposal and one company version – on the ballot. For that topic, the company proposal permitting shareholders owning at least 25% to call a special meeting prevailed over the shareholder proposal seeking the right for 10% holders.

At this point, over 60 companies with proxy access shareholder proposals have filed proxy statements. More than 40 of those companies are simply opposing the shareholder proposal. Other variations include seven companies that have already adopted, or have indicated that they will adopt, their own version of proxy access provisions. Interestingly, two of those companies will have provisions with 3% ownership thresholds, but one company will allow only five shareholders to aggregate holdings and another limits the aggregation to 20 shareholders. It appears that the proponents for those shareholder proposals did not withdraw their proposals even though those companies are permitting ownership thresholds to be set at 3% of shares outstanding.

Two other companies are supporting the shareholder proposal and one company’s board has decided to take no position on whether shareholders should support or oppose it. There remains at least four companies that have both management and shareholder proposals, with different ownership thresholds, to be voted on.

In addition, at least a dozen companies have agreed to adopt proxy access and are no longer presenting those shareholder proposals at their annual meetings.

Whistleblowers: The SEC Gives the Max In 1st Retaliation Case

Yesterday, the SEC awarded the maximum amount it can – 30% – to the whistleblower in the Paradigm Capital Management case, the 1st retaliation case that the SEC announced nearly a year ago. Here’s a blog by Steve Quinlivan – and here’s a press release from Labaton Sucharow’s Jordan Thomas, the lawyer who represented the whistleblower…

Pay-for-Performance Rulemaking: Sneak Preview

This WSJ article and Bloomberg article previews the SEC’s open Commission meeting today (here’s my eight cents), during which the Dodd-Frank pay-for-performance rules will be proposed. Also see this blog from CompensationStandard.com’s “The Advisors’ Blog” for some historical perspective on this rulemaking. Also weigh in on this poll about whether you want us to conduct a webcast on this new proposal:

Thanks to those that participated in this survey – a hot topic! Below are the results from my recent survey on currency fluctuations for incentive comp:

1. Does your company adjust incentive goals/results for currency rate fluctuations?

– Yes, as a policy consistently applied – 24%

– Occasionally, as ad hoc decisions made across years – 15%

– No, we never do – 42%

– Not sure, it hasn’t come up – 20%

2. If your answer to #1 above was “yes,” what is the percent of impact currency rate fluctuations must have for neutralization (i.e. what is the swing/change in the metric due to the currency fluctuation before things get adjusted)?

– Less than 5% – 62%

– 5% to 9% – 10%

– 10% to 14% – 14%

– 15% to 19% – 0%

– 20% to 24% – 14%

– 25% or more – 0%

3. If your answer to #1 was “occasionally” or “never,” are your incentive compensation performance measures predominantly return measures?

– Yes – 32%

– No – 66%

– Not applicable (we don’t use performance measures for our incentive compensation) – 2%

4. If your company makes ad hoc decisions, is the issue decided on whether management raises the issue & how large the impact is?

– Yes – 42%

– No – 8%

– Not sure, it hasn’t come up – 50%

5. If you do adjust your incentive goals/results for currency rate fluctuations, to which type of incentive programs are these adjustments made?

– Short-Term – 61%

– Long-Term – 6%

– Both Short-Term & Long-Term – 33%

Will California Require Notice Filings For Regulation A Offerings?

This blog by Keith Bishop notes how the California Commissioner has yet to adopt a form of notice regarding Tier 2 offerings under Regulation A…

My good friend Barbara Blackford – well known in the Society of Corporate Secretaries – is riding 2500 miles on a bike to benefit “Cycling for Good.” You’ve read before in this blog about Cleary Gottlieb’s Julie Yip-Williams (see her blog about her battle with cancer). Next week, Barbara is riding for Julie and a colony cancer research foundation. Barbara is maintaining this blog – and here’s a description of the ride. Most important is this explanation of “Cycling for Good” and how you can donate…

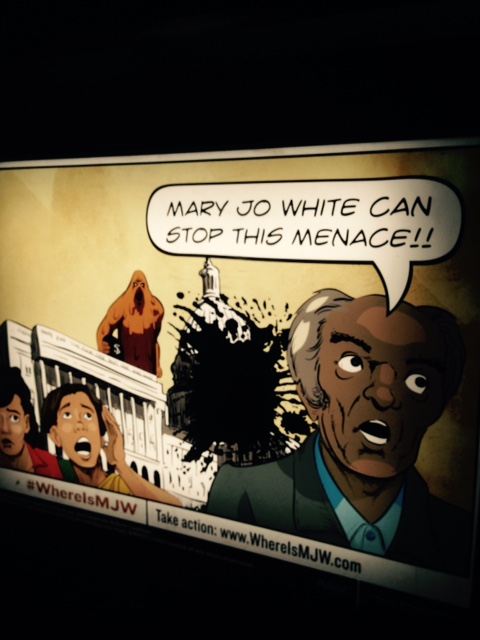

Even More on “Subway Marketing to the SEC Continues”

Just after I blogged about additional poster ads in the DC subway system, I found two more new ones – at a subway station that is not even near the SEC (ie. Metro Center station):

This blog by Elm Sustainability Partners certainly got my attention. It covers a new report by Global Witness & Amnesty International, which claims there is a noncompliance rate of 80% when it comes to the SEC’s conflict minerals reporting requirements. As the blog notes, these findings fly in the face of the numerous other studies of last year’s Form SDs (all of which are posted in our “Conflict Minerals” Practice Area – and were covered in this popular webcast recently).

The blog points out the inconsistencies in this new report – but unfortunately, the new report was widely covered in the mainstream media including this Bloomberg article and Reuters article. The damage wrought by poorly reported stories in Rolling Stone magazine & others has taught the media nothing…

There have been a number of questions posed in our “Q&A Forum” on conflict minerals reporting (eg. #8413; 8402). We have been struggling with providing answers for some of them due to the varied responses that companies appear to be taking. If you have input, please weigh in (you can do so anonymously). This recent webcast on conflict minerals also may be useful as it was very popular…

As a way to honor his extraordinary life, a group of luminaries has set up the “The Harvey J. Goldschmid Fund” at Columbia Law School. Pledges to the Goldschmid Fund may be made in a variety of ways and may be spread over five years.

Whistleblowers: Another $1+ Million Award to an Internal Auditor!

Last week, the SEC announced its 2nd whistleblower award to someone with an internal audit or compliance role, giving $1 million (see the memos about both of these awards in our “Whistleblowers” Practice Area)…

As I blogged yesterday, the SEC has calendared an open Commission meeting for Wednesday, April 29th to finally propose the pay-for-performance rules as required by Dodd-Frank. This rulemaking is important as it could become the new standard for measuring pay and performance.

We’ll have to see what exactly the SEC proposes when the proposing release is out – but if it comes out in a form as expected, here are my 8 points of analysis:

1. Companies can get the data and crunch the numbers. I don’t think that the actual implementation itself will be difficult.

2. But I think what could be particularly worrisome is having yet another metric to figure out what the CEO got paid and trying to explain all of it.

3. You know how companies have different schemes for granting equity, including type and timing. If the rules tend to try to fit everyone into a narrow bucket in order to try to line everyone up for comparability, and a company’s program doesn’t quite fit neatly into it, then the disclosure can get even more complicated.

4. There are two elements: compensation and financial performance. What is meant by “financial performance” for example? Maybe the SEC will just ask for stock price, maybe they’ll go broader.

5. A tricky part likely will be the explanation of what it all means – and how it works with the Summary Compensation Table.

6. I don’t think it will be difficult to produce the “math” showing the relationship of realized/realizable pay relative to TSR and other financial metrics, so long as:

– There’s a tight definition of realized pay

– We know what period to measure TSR (and if multiple periods can be used)

– We know what other performance measures can be included (if any) and if they can be as prominent in the disclosure as TSR

7. Another area of potential difficulty is explaining why there is not a tight or tighter correlation with TSR (“we use metrics other than TSR to drive our compensation; thus, the correlation is not very strong; on the other hand, our compensation is based on Revenue Growth and EBITDA Margin, and as Exhibit II demonstrates, the correlation is very significant”).

In addition, Dodd-Frank has no requirement for a relative ranking, and companies will need to decide if TSR and Pay should be put in some type of relative context (“relative to our peers, our realizable pay was well below the peers; so even though compensation is not tightly aligned with stock price performance the last 3 years, we did not pay our bums very much).

8. I think what may be the most difficult to address is a requirement to discuss what the Compensation Committee plans to change – and why is it now that it has performed the analysis?

– Keith Higgins Speaks: The Latest from the SEC

– The SEC’s New Pay-for-Performance Proposal

– Proxy Access: Tackling the Challenges

– Disclosure Effectiveness: What Investors Really Want to See

– Pay Ratio: What Now

– Peer Group Disclosures: The In-House Perspective

– Creating Effective Clawbacks (and Disclosures)

– Pledging & Hedging Disclosures

– The Executive Summary

– The Art of Communication

– Dave & Marty: Smashmouth

– Dealing with the Complexities of Perks

– The Big Kahuna: Your Burning Questions Answered

– The SEC All-Stars: The Bleeding Edge

– The Investors Speak

– Navigating ISS & Glass Lewis

– Hot Topics: 50 Practical Nuggets in 75 Minutes

Early Bird Rates – Act by the end of Friday, April 24th: Huge changes are afoot for executive compensation practices with pay ratio disclosures on the horizon. We are doing our part to help you address all these changes – and avoid costly pitfalls – by offering a special early bird discount rate to help you attend these critical conferences (both of the Conferences are bundled together with a single price). So register by the end of Friday, April 24th to take advantage of the 33% discount.

CD&A Template: CFA Institute Has Its 2.0

Last October, I blogged it was coming – and now it’s here (albeit a bit late for this proxy season). The CFA Institute has updated its CD&A Template, last issued in 2011. Here’s a blog from Matt Orsagh explaining the changes – particularly focusing on how the updated Template supports better pay-for-performance storytelling…

Happy Retirement! Lydia Beebe & Amy Goodman

Two of my favorites recently decided to retire, Chevron’s Lydia Beebe & Gibson Dunn’s Amy Goodman. They won’t totally disappear – but they will be unburdened from their day job. I saw both of them a few days ago at Lydia’s bash – they were looking good!

Here’s news from this blog by Davis Polk’s Ning Chiu:

Companies with proxy access shareholder proposals on their annual meeting ballots are confronting a notice of exempt solicitation filed by the California Public Employees Retirement System (CalPERS) and the New York City Pension Funds urging shareholders to vote in favor of the proposals. A notice of exempt solicitation is coded as PX14A6G and can be a surprise to companies when it appears on the company’s SEC EDGAR website.

The exempt solicitation argues that providing access to a company’s proxy to allow shareholders (or “shareowners” according to the notice) the ability to nominate directors to the board is “one of the most important rights given to the owners of a company.” Without proxy access, director elections are essentially “a ratification of corporate management’s slate of nominees.”

It defends the proposed terms of proxy access in the proposals that seek to give the rights to shareholders owning 3% for 3 years by citing to the SEC proxy access rulemaking in 2010. According to the notice, the SEC’s analysis in formulating that standard was carefully considered as appropriately balanced. The notice also refers to the CFA Institute study on proxy access which we previously discussed here, including the oft-quoted projection that proxy access has the potential to raise U.S. market capitalization by between $3.5 billion and $140.3 billion and also that proxy access is rarely used in the jurisdictions where it is available.

Finally, a number of companies of varying sizes, such as Abercrombie & Fitch, Bank of America, Big Lots, First Merit, General Electric, Kindred Healthcare, Prudential Financial, Splunk, Staples, Wendy’s, Whiting Petroleum, and Yum Brands, are listed as companies that are “voluntarily adopting” the provisions and “rejecting the common corporate assertion that proxy access is costly, distracting, and favored mainly by special interest groups.”

The letter is signed by Anne Simpson, senior portfolio manager-investments and director of CalPERS Global Governance, and Scott Stringer, New York City Comptroller. A proxy solicitor, Garland Associates, is listed as a contact for additional information.

The SEC’s “Pinterest” Page

The SEC continues to leverage social media – the latest being this Pinterest page with a handful of infographics. I haven’t posted much to my Pinterest page – but it will grow eventually. But I do have 54 Pins compared to just 4 for the SEC.

Meanwhile, this page lists 6 Twitter handles for the SEC, including two of the regional offices having their own handles…

Private Placement Brokers: FINRA Highlights In Annual Exam Letter

As covered in this Morrison & Foerster memo, FINRA has published a longer annual priorities letter than it typically does – and tackles a number of issues related to private placements including:

– Inadequate due diligence by broker-dealers in connection with private placements

– Inadequate suitability assessments

– Misleading offering documents

– Deficiencies in procedures in offerings that use escrow accounts

– Concerns in exempt offerings involving the use of general solicitation

Also check out this recent FINRA regulatory notice about the SEC approving FINRA’s rule change regarding payments to unregistered persons…

In the wake of poll results indicating a strong preference to having the full menu of our offerings available straight from our home page, I have reverted the home page back to whence it came. The new large tabs at the top are the same – and the home page is “cleaner” than it used to be – but for the most part, everything is back to how it was before the redesign. Not mobile friendly – so it’s gonna hurt our Google rankings – but I listened to you. Like before, the change in the home page doesn’t impact all the other content on the site.

One member’s reaction: “I feel the same sense of triumph I felt when “old Coke” returned.” And also note that I launched a redesign yesterday of the Section16.net home page using the same concept, much larger tabs at the top and other clean-up (but no changes to the underlying content)…

DOJ Emphasizes Role of Criminal Prosecution in Addition to Regulatory Enforcement

Here’s an excerpt of this blog by Mintz Levin’s Bridget Rohde:

The U.S. Department of Justice, through the Assistant Attorney General in charge of its Criminal Division, spoke forcefully on Tuesday regarding “the role of criminal law enforcement in prosecuting conduct that may also be subject to regulatory enforcement.” Speaking at a conference at New York University, AAG Leslie R. Caldwell discussed the sometimes “critical need” for criminal prosecution even where there are civil and regulatory options, noting that individuals may receive prison sentences and companies may suffer collateral consequences that are “the only just punishment” for the conduct at issue and that serve to deter others. Recognizing that there are different kinds of breaches, she spoke of calibrating the penalty to the nature of the breach and the entity’s history and culture. AAG Caldwell also stated that DOJ’s Criminal Division, unlike other authorities, requires entities to admit their misconduct when resolving a criminal matter by a Non-Prosecution Agreement, a Deferred Prosecution Agreement, or a guilty plea. She addressed the Criminal Division’s power – and resolve – when it suspects or finds non-compliance with an NPA or a DPA.

Fraud Indicators: Signature Size Matters

This article notes how a recent study shows that CFOs with big signatures are more likely to misreport…

Ever since I dealt with this in our “Q&A Forum” a few months ago (#8333), I’ve been meaning to blog about it. This is a sleeper for those with foreign subsidiaries because it’s an action item for you with an upcoming deadline. As noted in these memos posted in our “Foreign Subsidiaries” Practice Area, the Commerce Department’s Bureau of Economic Analysis (known as the “BEA”) has a deadline of the end of May (or the end of June if you have more than 50 foreign subs) for a survey about your company’s direct investment abroad. This survey is in the form of the “Form BE-10.” The last survey was conducted five years ago – and the BEA gave guidance on this new survey in this rulemaking last November.

Note that the BEA requires all entities subject to the reporting requirements to file responses, regardless of whether they are individually contacted by the BEA. Given that the scope of this survey has been expanded to cover many industries & companies that didn’t previously report, you should evaluate whether you are now required to submit a Form BE-10, even if you haven’t in the past…

US Sentencing Commission Approves Changes to Guidelines

A few weeks ago, the US Sentencing Commission approved changes to its sentencing guidelines. As noted in this memo, the major changes are:

– Revise the definition of “intended loss” at §2B1.1, comment (n.3(A)(ii)) to mean the pecuniary harm “that the defendant purposely sought to inflict”

– Revise the victims table at §2B1.1(b)(2) to incorporate “substantial financial hardship” as a sentencing enhancement factor

– Revise the meaning of the specific offense characteristic for “sophisticated means” contained in §2B1.1(b)(10)(C) to apply to the defendant’s individual conduct, rather than the overall scheme

– Revise Application Note 3(F)(ix), which sets forth a method for calculating loss in cases involving securities fraud; the revised guidelines provide that the formula set forth in the note is no longer a rebuttable presumption in calculating loss and allows the court to use any method that is appropriate and practicable under the circumstances, including the formula

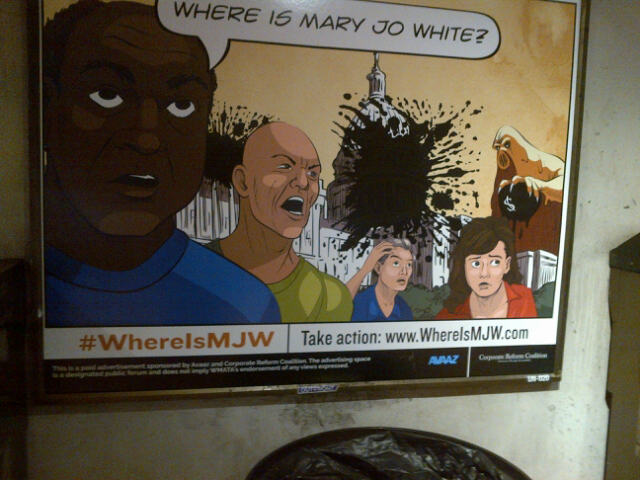

More on “Subway Marketing to the SEC Continues”

Folks were loving the pic on my blog Friday regarding the poster ads in the subway station near the SEC’s HQ – and a member sent in three more (below and at the bottom of this list):

On the heels of the news that a shareholder proposal about climate disclosure received support of over 98% at BP last week, comes the news that a group of 62 institutional investors has sent this 7-page letter to the SEC seeking better climate disclosure from oil & gas companies. The letter gets pretty specific about deficiencies in carbon asset risk disclosures. See this press release – and this Reuters article…

FINRA Pursues Reg M Enforcement Cases

This recent short-selling case demonstrates FINRA’s continued oversight of Rule 105/Regulation M practices…

California Companies Reincorporating in Nevada & Delaware

This blog by Keith Bishop describes how California continues to hemorrhage corporate charters to Delaware and Nevada. Here’s an excerpt:

The most recent potential emigrant is SJW Corp. which filed this proxy statement last week seeking shareholder approval of a reincorporation from California to Delaware. Can California and other states stanch the flow by offering licenses only to domestic corporations? Surely, there must be some constitutional bar to such a requirement – or maybe not? That question was answered last week by U.S. District Court Judge Lucy H. Koh in Nationwide Biweekly Admin., Inc. v. Owen, 2015 U.S. Dist. LEXIS 34558 (N.D. Cal. March 18, 2015).

Like last year, Verizon has put out a new “2015 Data Breach Investigations Report.” This year’s Verizon report is 69 pages, with a host of useful information as it relies on over 80,000 incidents from 70 organizations for it’s analysis. Also check out our checklists related to incident response planning, disclosure practices and risk management – as well as a chart of state laws related to security breaches.

CEO Drastically Cuts Own Pay & Raises Pay of All His Employees

Here’s the intro to this NY Times article that everyone is talking about:

The idea began percolating, said Dan Price, the founder of Gravity Payments, after he read an article on happiness. It showed that, for people who earn less than about $70,000, extra money makes a big difference in their lives.

His idea bubbled into reality on Monday afternoon, when Mr. Price surprised his 120-person staff by announcing that he planned over the next three years to raise the salary of even the lowest-paid clerk, customer service representative and salesman to a minimum of $70,000. “Is anyone else freaking out right now?” Mr. Price asked after the clapping and whooping died down into a few moments of stunned silence. “I’m kind of freaking out.”

If it’s a publicity stunt, it’s a costly one. Mr. Price, who started the Seattle-based credit-card payment processing firm in 2004 at the age of 19, said he would pay for the wage increases by cutting his own salary from nearly $1 million to $70,000 and using 75 to 80 percent of the company’s anticipated $2.2 million in profit this year. The paychecks of about 70 employees will grow, with 30 ultimately doubling their salaries, according to Ryan Pirkle, a company spokesman. The average salary at Gravity is $48,000 a year.

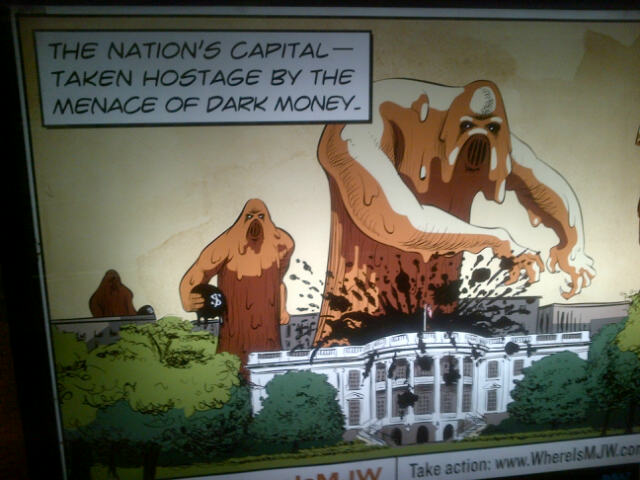

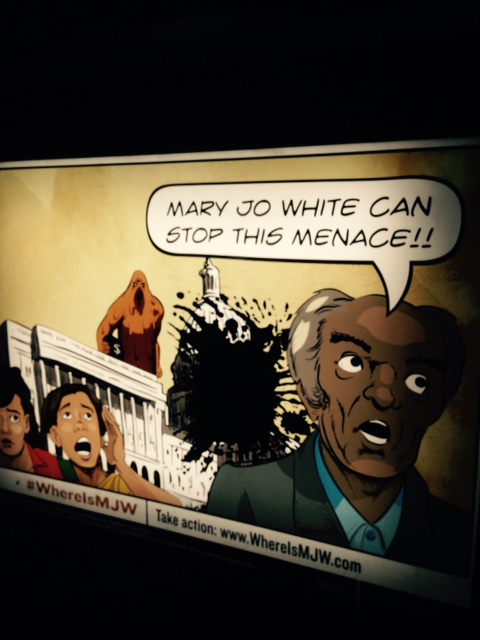

Subway Marketing to the SEC Continues

I’ve blogged before how some folks buy poster ads in the subway station near the SEC’s HQ (ie. Union Station) in an effort to influence the SEC. The latest poster is this one:

{kind=link}