Yesterday, the SEC announced this New Year’s gift: proposed amendments to Rule 2-01 of Reg S-X that would “modernize” the auditor independence rules and codify Staff consultations – which have been influencing how the rules are interpreted since they were adopted in 2000 and last amended in 2003. If adopted, the proposed amendments would:

– Amend the definitions of affiliate of the audit client, in Rule 2-01(f)(4), and Investment Company Complex, in Rule 2-01(f)(14), to address certain affiliate relationships, including entities under common control

– Amend the definition of the audit and professional engagement period, specifically Rule 2-01(f)(5)(iii), to shorten the look-back period, for domestic first time filers in assessing compliance with the independence requirements

– Amend Rule 2-01(c)(1)(ii)(A)(1) and (E) to add certain student loans and de minimis consumer loans to the categorical exclusions from independence-impairing lending relationships

– Amend Rule 2-01(c)(3) to replace the reference to “substantial stockholders” in the business relationship rule with the concept of beneficial owners with significant influence

– Replace the outdated transition and grandfathering provision in Rule 2-01(e) with a new Rule 2-01(e) to introduce a transition framework to address inadvertent independence violations that only arise as a result of merger and acquisition transactions

– Make certain miscellaneous updates

The announcement runs through a couple of hypos that show how the proposal would address interpretive issues that have been popping up. As always, there’ll be a 60-day comment period that runs from when the proposing release is published in the Federal Register. Also see the summary in this Cooley blog…

Audit Committee Role & Reminders: Statement from SEC & Corp Fin

Also yesterday, this statement from SEC Chair Jay Clayton, Chief Accountant Sagar Teotia and Corp Fin Director Bill Hinman was issued to remind audit committees of their oversight responsibilities in financial reporting – and to remind companies that audit committees need adequate resources & support to fulfill their obligations. Here’s an excerpt:

– Non-GAAP Measures – Non-GAAP measures and other metrics used to gauge company performance, when used appropriately in combination with GAAP measures, can provide decision-useful information to investors on the company’s performance from management’s perspective. It is important that audit committees understand whether—and how and why—management uses non-GAAP measures and performance metrics, and how those measures are used in addition to GAAP financial statements in the company’s financial reporting and in connection with internal decision making. We encourage audit committees to be actively engaged in the review and presentation of non-GAAP measures and metrics to understand how management uses them to evaluate performance, whether they are consistently prepared and presented from period to period and the company’s related policies and disclosure controls and procedures.

– Reference Rate Reform (LIBOR) – The expected discontinuation of LIBOR could have a significant impact on financial markets and may present a material risk for many companies. The risks associated with this discontinuation and transition will be exacerbated if the work necessary to effect an orderly transition to an alternative reference rate, a process often referred to as reference rate reform, is not completed in a timely manner. We encourage audit committees to understand management’s plan to identify and address the risks associated with reference rate reform, and specifically, the impact on accounting and financial reporting and any related issues associated with financial products and contracts that reference LIBOR.

– Critical Audit Matters – Beginning in 2019, certain public companies’ auditors are required to communicate critical audit matters (CAMs) in the auditor’s report. While the independent auditor is solely responsible for writing and communicating CAMs, we encourage audit committees to engage in a substantive dialogue with the auditor regarding the audit and expected CAMs to understand the nature of each CAM, the auditor’s basis for the determination of each CAM and how each CAM is expected to be described in the auditor’s report. In short, we would expect that the discussion of the CAM in the auditor’s report will capture and be consistent with the auditor-audit committee dialogue regarding the relevant matter. We encourage audit committees to continue their efforts to understand the new standard and remain engaged with auditors in the implementation process.

We’re Gonna Party Like It’s…

Who else is in shock that we’re 20 years into this century?! Our flip from 2019 to 2020 feels momentous in its own right – but we’re lacking in catchy tunes to celebrate. When in doubt, tune to Prince:

My resolution this year is to finally visit Paisley Park…I live just down the road and I’m still kicking myself for never making it to one of “The Artist’s” impromptu parties. I did, however, join thousands of my closest friends outside First Ave the night he died, where he was honored by lots of local talent, including Lizzo before many people knew who Lizzo was – quite the scene with everyone singing along to “Purple Rain.”

Last week, the SEC issued this notice to approve changes to FINRA Rule 5110. This Mayer Brown blog gives a high-level overview of topics covered by the amendments – which are intended to reduce compliance costs:

(1) filing requirements; (2) filing requirements for shelf offerings; (3) exemptions from filing and substantive requirements; (4) underwriting compensation; (5) venture capital exceptions; (6) treatment of non-convertible or non-exchangeable debt securities and derivatives; (7) lock-up restrictions; (8) prohibited terms and arrangements; and (9) defined terms

Corporate Musicals: Ready for a Revival?

If you haven’t watched “Bathtubs Over Broadway” on Netflix, make it your New Year’s resolution. In this review for The New Yorker, Richard Brody concludes that high-budget corporate musicals like J&J’s “sunscreen disco” inspired countless “mid-level business people” to be heroes in their profession.

Is a revival of this genre the key to positive corporate culture that so many companies & shareholders say they want? For enough money, I’m pretty sure Kristin Chenoweth would sing about insurance policies, medical devices or self-driving vehicles. For some “short form” entertainment, check out Blackstone’s holiday video – 6 minutes and in the style of “The Office,” with a joke for us SEC geeks around the 4:30 mark.

Songs For Our Time

On second thought, maybe over-the-top, optimistic musicals aren’t a good fit for this day & age. What today’s workers would identify with is an album with songs like “The Perils of Mobile Connectivity” – from a derivatives trader who’s spent the best years of his life in an office tower. I’m here to report that Jason Pilling’s “White Collar Melodies” has all that & more…

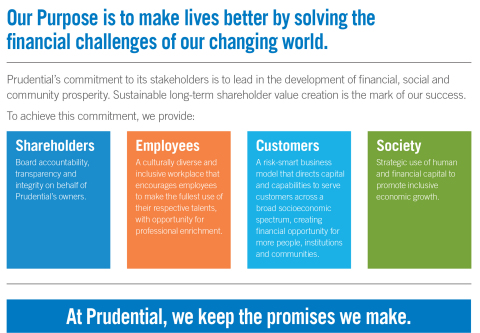

We’ve blogged a lot about the BRT’s redefined “statement of corporate purpose.” Many are frustrated that the topic is getting so much attention, given that the vast majority of directors & companies already view themselves as catering to multiple stakeholders in order to achieve long-term value. I blogged recently on “The Mentor Blog” about that disconnect and the resulting communications opportunity. One tangible thing that some companies are doing – regardless of whether their CEOs signed the BRT statement – is adopting a “statement of purpose” that shows the link between the company’s strategy and its consideration of stakeholder groups.

Last week, Prudential went one step further and also announced a “multi-stakeholder framework” that supports the company’s updated statement of purpose – and shows how the board considers shareholders, employees, customers and society. The press release emphasizes the board’s role in the stakeholder commitments and says that the company will report on the progress of its purpose-driven goals in its annual & sustainability reports. Here’s the infographic:

We’ll be covering more on this issue during our January 21st webcast – “Deciphering ‘Corporate Purpose.’” Join us to hear Morrow’s John Wilcox, Freshfields Bruckhaus’ Pam Marcogliese and Morris Nichols’ Tricia Vella discuss what the debate over “shareholder primacy” means for directors’ fiduciary duties and corporate accountability, and how companies can effectively set & communicate “stakeholder” commitments.

ESG Ratings Draw Nearly Universal Contempt

If there’s one thing that most people in our community can agree on, it’s that the proliferation of “ESG” ratings and funds is causing frustration and confusion. However:

ESG scores can play a key role in determining whether fund managers or exchange-traded funds buy a stock, how much companies pay on loans, and even if a supplier bids for a contract. They can also help verify whether a bond is really “green” or if a company is eligible for a stock benchmark. Investments in about $30 trillion in assets have relied in some way on ESG ratings.

That’s according to this recent Bloomberg article, which cites an MIT working paper. But ratings are difficult to compare and can vary widely. And the variation in how they’re employed – by “ESG” funds, in particular – only compounds the problem. Maybe that’s why the SEC is reportedly looking into these investors:

The SEC initiative is based out of the agency’s Los Angeles office, according to a person familiar with the matter. It has focused on advisers’ criteria for determining an investment to be socially responsible and their methodology for applying those criteria and making investments.

One letter the SEC sent earlier this year to an investment manager with ESG offerings asked for a list of the stocks it had recommended to clients, its models for judging which companies are environmentally or socially responsible, and its best- and worst-performing ESG investments, according to a copy of the letter viewed by The Wall Street Journal. It follows a similar examination letter sent last year to other asset managers, suggesting the regulator decided to broaden its examination.

It’s not clear what the end game would be for this type of examination. Increased disclosure? A standardized reporting framework? That’s a concept I’ve blogged about for companies. The EU already requires large companies to report on their sustainability policies – and within the next couple years will also encourage indexes and benchmark providers to disclose their ESG methodologies (see this White & Case memo and this Bloomberg article).

Government Shutdown Averted!

Good news – the Staff will be returning to work later this week. Congress passed spending bills that the President has now signed, averting a shutdown and keeping the federal government funded through next September. Here’s a short CBS News article about it.

Last year around this time, the government began what ended up being the longest shutdown in history. The SEC went down to a “skeletal staff” for most of January – which put companies in a real bind when it came to negotiating with shareholder proponents, trying to get through the registration process and resolving any Corp Fin comments.

We were blogging about it almost daily (here’s one of the later ones) – and fielded many posts in our “Q&A Forum.” For a reminder about what that was like at the SEC, see Broc’s blog about the deep hole Corp Fin found itself in after the shutdown and my blog wondering whether the shutdown led to Corp Fin reconsidering the Rule 14a-8 no-action request process.

Yesterday, Corp Fin added to its “CF Disclosure Guidance Topic” series with two new topics. “Topic No. 8: Intellectual Property & Technology Risks Associated with International Business Operations” explains the Staff’s views on what companies should consider disclosing about their reliance on technology & intangible assets if they conduct business in places that don’t have robust IP laws – and where that disclosure would appear. Here’s an excerpt:

Although there is no specific line-item requirement under the federal securities laws to disclose information related to the compromise (or potential compromise) of technology, data or intellectual property, the Commission has made clear that its disclosure requirements apply to a broad range of evolving business risks in the absence of specific requirements. In addition, a number of existing rules or regulations could require disclosure regarding the actual theft or compromise of technology, data or intellectual property if it pertains to assets or intangibles that are material to a company’s business prospects. For example, disclosure may be necessary in management’s discussion and analysis, the business section, legal proceedings, disclosure controls and procedures, and/or financial statements.

The guidance includes examples of risks that might arise from business relationships – e.g. idiosyncratic license terms that favor the other party or compromise the company’s control over proprietary info, regulatory requirements that require companies to store data locally or use local services or technology. It also includes a laundry list of questions companies should ask themselves to assess risks. We’ll be posting memos in our “Cybersecurity” Practice Area.

Corp Fin’s New “Disclosure Guidance”: Confidential Treatment Requests

RIP, Staff Legal Bulletins No. 1 and 1A. Yesterday’s new “CF Disclosure Guidance Topic No. 7: Confidential Treatment Applications Under Rules 406 & 24b-2” supersedes that guidance. It addresses how and what to provide when submitting a “traditional” confidential treatment request – i.e. outside of the accommodations from earlier this year that now allow companies to simply redact immaterial confidential information from exhibits. The new disclosure guidance also applies to filings where traditional CTRs remain the only available method to protect private information – e.g. Schedule 13D or exhibits required by Item 1016 of Reg M-A.

After filing the exhibit on Edgar with redactions that show where confidential info is omitted, here’s what companies now need to do for written applications (we’ll be posting memos in our “Confidential Treatment Requests” Practice Area):

1. Provide one unredacted copy of the contract required to be filed with the Commission with the confidential portions of the document identified;

2. Identify the Freedom of Information Act[6] exemption it is relying on to object to the public release of the information and provide an analysis of how that exemption applies to the omitted information. Often, this is the exemption provided by Section 552(b)(4)[7] of the FOIA, which protects “commercial or financial information obtained from a person and privileged or confidential.” If this is the case, the Supreme Court’s decision in Food Marketing Institute v. Argus Leader Media, 139 S.Ct. 2356 (2019) addresses the definition of confidential and may be helpful in providing this analysis;

3. Justify the time period for which confidential treatment is sought;

4. Explain, in detail, why, based on the applicant’s specific facts and circumstances, disclosure of the information is unnecessary for the protection of investors. This generally is encompassed in a materiality discussion, addressed below;

5. Provide written consent to the furnishing of the confidential information to other government agencies, offices or bodies and to the Congress;

6. Identify each exchange, if any, with which the material is filed (required in applications under Rule 24b-2 relating to Exchange Act filings only); and

7. Provide the name, address and telephone number of the person with whom the Division should communicate and direct all issued notices and orders.

What’s the Deal with “CF Disclosure Guidance”?

A while back, Corp Fin was on a roll with this format for guidance – issuing six topics from 2011 to 2013 (here’s Broc’s blog from when this format first debuted). But yesterday’s new topics were the first in over six years.

They’ve always included a “Supplementary Information” disclaimer at the beginning to emphasize that the guidance isn’t a rule and hasn’t been approved by the Commission. Of course, lately there’s been even more back & forth about the role of “guidance” versus rules – and as Broc blogged last month, a recent executive order severely restricted most federal agencies’ ability to practice “regulation by guidance.” So to be extra clear that these publications aren’t rules, the disclaimer for yesterday’s two topics includes this new sentence:

This guidance, like all staff guidance, has no legal force or effect: it does not alter or amend applicable law, and it creates no new or additional obligations for any person.

SEC & Edgar Closed Tuesday & Wednesday

This executive order announces that all federal agencies – including the SEC – will be closed on Tuesday for Christmas Eve (Christmas Day was already designated as a Federal Holiday, so the SEC is closed that day too). The SEC announced that this means Edgar will be closed too – so you’ve got until December 26th to make filings that would be due on Tuesday or Wednesday.

This blog from Alan Dye points out that it isn’t clear whether the 24th is still counted as a “business day” for purposes of calculating filing deadlines that fall later in the week. Based on last year’s precedent, it wouldn’t be considered a “business day” for purposes of calculating filing deadlines – and Alan was told in a phone call with the Staff that they’d take the same position this year.

As anticipated, yesterday the SEC voted to propose amendments to the definition of “accredited investors.” The proposed amendment, issued upon a 3-2 vote, will allow more investors to participate in private offerings by adding more natural persons that will qualify based on their professional knowledge, experience or certifications. Interestingly, the proposal contemplates that these categories could be established by the SEC by order, rather than the rule itself – which would allow the SEC to establish the criteria in the future without notice & comment. Also, the proposed amendments expand the list of entities that may qualify as accredited investors.

During the summer, Liz blogged about the SEC’s concept release that included discussion of the accredited investor definition. As the concept release generated a flurry of comment letters, it’s hard to say whether this proposal will please everyone. As this Cooley blog notes, the statements of dissent from Commissioners Rob Jackson and Allison Lee – compared to the statements of support from Commissioners Hester Peirce and Elad Roisman – highlight the differences in views that exist about the fundamental purposes of the securities laws.

The proposal doesn’t raise the income and wealth thresholds that have existed since 1982 or suggest adjustments for inflation in the future. This WSJ article says that the lack of an inflation adjustment has contributed to the current number of qualifying households rising over time – from 1.3 million in 1983 to 16 million this year. And among the 69 questions that the SEC specifically requests people to comment on is whether the standards should be tied to geographic reasons to account for potentially lower costs of living.

We’ll be posting memos in our “Accredited Investor” Practice Area to help everyone stay up to date with the latest on the proposed changes.

SEC Proposes Expanding QIB Def’n

As mentioned in the press release about the proposed expansion of the “accredited investor” definition, the SEC also proposed expanding the definition of “qualified institutional buyers” under Rule 144A. The expanded definition would add LLCs and RBICs (Rural Business Investment Companies) to the types of entities eligible for QIB status if they meet the securities owned and investment threshold in the definition. There’s also a new ‘catch-all’ category that would permit institutional accredited investors under Rule 501(a), of an entity type not already included in the QIB definition, to qualify as QIBs when they satisfy the $100 million threshold.

Keeping step with the fast-approaching year-end rush, yesterday the SEC also voted to propose rules requiring mining companies to disclose payments made to foreign governments or the U.S. government for the commercial development of oil, natural gas or minerals.

The Commission is statutorily obligated to issue a rule in this area. And, as outlined in the SEC press release about the proposed rules and in Broc’s blog back a couple of years ago, the path to these new proposed rules has been anything but smooth. Here’s an excerpt from the SEC press release:

The Commission first adopted rules in this area in 2012, as mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”). The 2012 rules were vacated by the U.S. District Court for the District of Columbia. The Commission then adopted new rules in 2016, which were disapproved by a joint resolution of Congress pursuant to the Congressional Review Act.

As Liz blogged last week, the NYSE proposal to allow “direct listings” for primary offerings has been revised and is back on the table, and it’s led to a lot of chatter and head-scratching about how exactly this path would work. This 12-page memo from Gibson Dunn is a good up-to-date resource that outlines benefits, issues to consider and current rules that apply. The memo has a nice tabular overview of the various listing standards so that you can compare different alternatives (as Liz also blogged last week, Nasdaq now has a rule that allows secondary direct listings on its Global Select, Global and Capital Markets).

At this point, we still don’t know why the SEC rejected the first NYSE proposal – was it something that the NYSE adequately addressed in its revised proposal, or does the SEC think there’s a fundamental problem with primary direct listings, for investor protection or other reasons? Stay tuned, we’ll be blogging more on this topic as it develops.

Improving Board Oversight of Risk

The board’s role in risk oversight continues to be top of mind – not only for directors, but also for shareholders, legislatures & proxy advisors. If you’re looking for a pretty comprehensive resource, Wachtell recently issued a 24-page memo on the topic. It includes these recommendations:

– Assess whether the company’s strategy is consistent with agreed-upon risk appetite and tolerance for the company

– Review with management whether adequate procedures are in place to ensure that new or materially changed risks are properly and promptly identified, understood and accounted for in the actions of the company

– Review the risk policies and procedures adopted by management, including procedures for reporting matters to the board and appropriate committees and providing updates, to assess whether they are appropriate and comprehensive

– Review with management the quality, type and format of risk-related information provided to directors

– Review with management the primary elements comprising the company’s risk culture, including establishing “a tone from the top” that reflects the company’s core values and the expectation that employees act with integrity and promptly escalate non-compliance in and outside of the organization

Over Confidence about Risk Management?

As reported in a recent Navex blog, a survey from the Institute of Internal Auditors found that boards are over confident about the effectiveness of an organization’s risk management program. According to the survey results, the board “has more faith in the company’s ability to manage risks than the company’s executives do.”

As the blog high-lights, this can present problems when the board believes the company is effectively managing a risk, such as third-party risk, and the board then voices approval for growing the business in an area that relies heavily on effective third-party risk management. As the business expands or grows, a breakdown can occur and then questions will arise about an apparent weakness in risk management, and perhaps whether management was transparent with the board prior to the breakdown.

Navex offers tips for aligning management’s and the board’s views on risk management. Tips for starting a conversation with the board include:

– Discuss whether the board has the right structure and right people

– Evaluate whether the company has good escalation procedures so that the right information gets delivered to the board

– Does management speak in a unified way about risk to help ensure transparency?

– Does the company have a single, trusted source of risk information – starting with the same data set of information is key

Always a high-interest topic, check out Equilar’s blog on GC compensation trends – including a list of the top 10 highest paid general counsel. The info is based on the “Equilar 500” – 500 largest US-headquarter companies by reported revenue that trade on one of the 3 major US stock exchanges. Here are several tidbits from the findings:

– Median general counsel pay was $2.6 million in 2018, a 3.7% increase from 2017

– Although general counsel pay has risen through the years, it lags the rise in CEO compensation, which increased 8% from 2017

– Among the top 10 highest paid general counsel, the technology sector had the highest representation

– Since 2015, male general counsel have earned 11% more on average than female general counsel, and in 2018, this figure grew to over 18%

When the SEC raised the “smaller reporting company” threshold to $250 million last year, one point of contention was that it didn’t make an analogous change to the “accelerated filer” definition. So as confirmed in a set of CDIs from Corp Fin, a company can now be both a “smaller reporting company” and an “accelerated filer.” And although the SEC proposed amendments to both the “accelerated filer” and “large accelerated filer” definitions earlier this year, the proposed rules haven’t been adopted and there would still be some overlap between the filer categories.

Our members have asked a lot of questions about this over the last year. It’s hard to parse through all the rules! I was happy to see that this Ackerman memo lays out a chart for those companies that find themselves navigating this dual status.

For each Item of Reg S-K that applies to periodic reports, the chart compares general disclosure requirements to the rules that apply to smaller reporting companies – and shows whether or not “dual status” companies can take advantage of scaled disclosure accommodations. The memo also highlights that companies holding “dual status” need to comply with accelerated filer filing deadlines – i.e. 75 days after year end for their Form 10-K and 40 days after quarter end for their Form 10-Qs. Don’t forget about our “Disclosure Deadlines” Handbook if you’re looking for more in-depth info.

Audit Fees Keep Rising Due to “New” Standards

Last year, Liz blogged that audit fees had increased due to implementing new revenue recognition and lease standards. Those efforts have continued, so it’s not too surprising that companies are seeing higher fees again this year – according to a recent survey that’s summarized in this “Accounting Today” article. Unfortunately, the article also says that finance teams don’t feel like they’re seeing much in the way of benefits from the extra work & fees:

Over half of finance teams saw substantial audit cost increases over the past two years, primarily due to new accounting rules. The vast majority of companies that have adopted the new revenue recognition standard said that it has had a negative impact on their audit, audit costs increased and the audit required more time to complete – all leading to increased stress and frustration.

Last week, the PCAOB released this Staff report with observations about how the CAMs are looking so far. Here’s an excerpt from this blog by Stinson’s Steve Quilivan:

As a starting matter, the PCAOB’s report seems to implicitly and perhaps explicitly assume that its audit standard requiring the reporting of CAMs provides “more useful and timely information.” That assumption is not backed up with any empirical data or observations.

The PCAOB apparently reviewed 12 of 189 audit reports through November 30, 2019 containing CAMs and there is no information about whether this observation set is statistically significant. The report promises that fuller analysis will follow. The observations reported by the PCAOB are general in nature and far from startling or, perhaps to many, useful.

Open Commission Meeting: Resource Extraction & Accredited Investors/QIBs

According to this notice, the SEC will hold an open Commission meeting this Wednesday to propose resource extraction rule changes and also to propose changes to the “accredited investor” and “QIB” definitions.

State of the SEC: A Few Nuggets from the Chair’s Testimony

Recently, SEC Chair Jay Clayton delivered this 33-page testimony to the Senate Banking Committee in a hearing about SEC oversight. Here are a few nuggets:

1. The SEC has 4400 employees. I’m always intrigued by keeping track of that stat for some reason. 140 positions were filled over the agency’s last fiscal year.

2. 34 rulemakings were advanced – quite a big number considering the government was closed for a month.

3. Proxy plumbing rulemakings took place. Been a lot of talk about proxy plumbing for over a decade. But this year saw a lot of concrete action.

4. Facilitating capital formation – a lot of action also took place here over the past year. “Testing the waters,” Fast Act, etc.

5. Human capital disclosure – on page 9, the Chair offers his own personal observation on this topic. Clearly, he believes in modernizing this area of disclosure.

Contingency Disclosures: Corp Fin’s Comments on Boeing

In this blog, Bass Berry’s Jay Knight analyzes how Corp Fin recently commented upon Boeing’s contingency disclosures. It serves as a nice reminder about the Fast Act rule changes…

Our own Susan Reilly notes: Before she gave birth to her second son, Liz blogged about her experience balancing pregnancy, parenthood & lawyering. In that vein, I thought I’d share a little about my life as a part-time, work-from-home securities lawyer and mom of three boisterous little boys. I’ve had this job for nearly 6 years now – and here are 5 things I’ve learned:

1. Set deadlines for yourself – The work I do now is dangerously flexible – most of my writing projects don’t have concrete deadlines, which is both a blessing (not having partners or clients breathing down my neck is amazingly liberating!) and a curse (it’s easy to let something that should take just a few hours drag on in drips and drabs for weeks).

While I’m grateful for the flexibility, I need a little structure in order to flourish, and setting deadlines for myself helps. Sometimes going a step further and communicating those expectations to your boss or client will really light a fire – that nagging law firm associate in me still cowers in fear of missing a deadline.

2. Establish office hours – A flexible job schedule has a sneaky way of making you think you can get your work done anytime. But there are always other tasks that jump to the top of the list if you let them – errands to run, appointments to schedule, laundry to fold – the list is endless. Scheduling specific working hours during the day, and being disciplined in keeping them, can keep that other non-urgent “life” stuff from chipping away at your productivity.

3. Enlist help – When my older two children made it to school age, I convinced myself that I didn’t need help with the baby – because I would just get my work done while he napped or after everyone was in bed (ha! – see #2). But I was completely at the mercy of this tiny human who demanded my full attention during his waking hours, whose sleeping hours were far too few.

Eventually I realized that I needed help, and my little guy now spends some time with a sitter a few days a week. When he’s there, I’m able to fully focus on the task at hand without constant interruptions. And when he’s home, I’m able to be a more attentive and less distracted parent.

4. It’s normal to feel disconnected – Because I only work part-time and from home, I can sometimes feel disconnected from my peers. It’s hard to fully relate to the stay-at-home moms or the full-time working moms – because I don’t fit neatly into either category. It’s a weird feeling, having one foot in each camp, but it’s one I’m slowly getting used to.

5. Never take it for granted – When Broc suggested I write a blog post about working part-time, I was both really excited to share my experience – but also a little nervous. I realize that I’m in a somewhat rare position of being able to continue pursuing my legal career while also having the flexibility to be home with my young children.

It’s not lost on me that the challenges I’ve faced with working part-time are ones I would have given my right arm for when I was working brutal hours at a firm – always on call, all the while learning how to be a new parent. Every once in a while, it’s important to take a step back and appreciate that meaningful and rewarding part-time work isn’t easy to come by – and to know a good thing when it comes your way.

Direct Listings: NYSE Files Revised Proposal!

That was fast. Earlier this week, I blogged that the SEC had rejected the NYSE’s proposed rule change to permit companies to sell newly issued primary shares via a direct listing – only 10 days after the exchange had submitted it. The SEC hasn’t made any public statements about why it rejected the proposal, so we still don’t know for sure whether it was because the Commission is fundamentally opposed to direct listings, believes that rulemaking is required, or if there was just something it wanted the NYSE to tweak. But the NYSE signaled that it would continue working on this initiative, and it’s now submitted this revised proposal. As this Davis Polk memo explains, it’s pretty similar to the original:

The new rule change proposal is substantially similar to the proposal the NYSE filed in November, except that issuers can meet the NYSE’s market value requirement by selling $100 million of shares (rather than $250 million under the initial proposal). Consistent with the initial proposal, the revised rule change proposal would provide the same flexibility for an issuer to sell newly issued primary shares into the opening auction in a direct listing, and would also delay the requirement that an issuer have 400 round lot holders at the time of listing until 90 trading days after the direct listing (subject to meeting certain conditions).

Stay tuned as to whether this revision addresses the SEC’s concerns. As Broc blogged when the original proposal was submitted, some are worried about investor protection issues for listings that occur outside of the traditional IPO process – but others note that there are a number of misconceptions about direct listings, including that a direct listing is even a “capital-raising” activity (see more from this Fenwick & West piece). We’re continuing to post memos in our “Direct Listings” Practice Area.

How to Attract & Retain New Lawyers

Law firms lose about $1 billion annually because of attrition, according to Thomson West. Being a young lawyer is marginally better than being a young investment banker (I have only landed in the hospital 2 or 3 times for overworking – I assume it’s a much more regular occurrence with bankers). But practicing law is still a tough gig.

And while my eyes usually glaze over whenever I see anything with “Millennial” in the title, this article connects some dots for scenarios that I’ve seen play out repeatedly. In the span of a couple years, our firm lost a cadre of young lawyers – not to other firms or companies – but to become distillery owners, grant-writers, ultimate Frisbee managers, MFA students… the list goes on.

Here are some pointers worth thinking about:

– A Millennial lawyer will leave a job, not just when he or she is unhappy, but when he or she is not happy enough.

– Give associates time & space to integrate their personal & professional lives (“work-life balance” is so Gen-X).

– Figure out a real way to mentor new lawyers.

– Empower associates to contribute immediately.

– Focus on “doing well by doing good.” The days of asking an associate, “If you can use the hours, I could really use your help on a new deal,” are over. Instead, try this approach: “If you’re interested in helping an interesting client, I’ve got a great deal for us.”

That last one made me laugh because that quote is specifically mentioned in Broc & John’s “101 Pro Tips – Career Advice for the Ages” (but not quite in the way that you’d think). One of the most empowering things you can do for these new lawyers is to help them take control of their own careers – and recognize the benefits of sticking with it. “Pro Tips” delves into the topics above and is a great resource for young lawyers – order it today. Here’s the “Table of Contents” so you can see what’s covered.

Programming Note: Lynn Jokela’s Blogging Debut!

Last month, I announced that Lynn Jokela has joined us as an Associate Editor for our sites. She brings a wealth of experience – here’s her bio. I’m now excited to share that Lynn will be making her blogging debut next week. Lynn’s email uses the domain from our parent company – it’s ljokela@ccrcorp.com – so keep an eye out for that in your inbox!

You likely saw this WSJ article last month, detailing an SEC investigation into one company’s end-of-quarter “earnings management” practices – e.g. leaning on customers to take early deliveries and rerouting products to book sales. The company says “everyone’s doing it” – and according to a McKinsey survey described in this Cleary blog, that’s not too much of an exaggeration:

Lest anyone think the SEC’s focus on “pulling in” revenues is an issue of limited relevance, note that approximately 27% of US public companies provide quarterly guidance, and evidence of widespread earnings management is not merely anecdotal. A broad survey by McKinsey reveals that, when facing a quarterly earnings miss, 61% of companies without a self-identified “long-term culture” would take some action to close the gap between guided and actual earnings, with 47% opting to “pull-in” sales. 71% of those companies would decrease discretionary spending (e.g., spending on R&D or advertising), 55% would delay starting a new project, even if some value would be sacrificed, and 34% would delay taking an accounting charge.

But the widespread nature of these practices doesn’t make the SEC more amenable to them – e.g. they imposed a $5.5 million fine and a cease-and-desist order in a recent enforcement action involving similar maneuvers. The blog notes:

The use of any of these techniques, if resulting in the obfuscation of a “known trend or uncertainty . . . that may have an unfavorable impact on net sales or revenues or income from continuing operations,” would presumably be equally objectionable to the SEC.

Accordingly, for those companies that are still providing earnings guidance, it would be prudent to make sure that your disclosure committee is having frank and frequent discussions with management about exactly what, if any, earnings management tools are being used, whether these tools fit squarely within the company’s revenue recognition policies, whether the company’s auditors are aware of the scope and persistence of these practices, and, most importantly, whether the use of the tools is, intentionally or not, masking a trend of declining sales, a declining market share, declining margins, or other significant uncertainties.

“Climate Accounting”: Exxon Prevails in Martin Act Suit

A couple months back, I blogged that Exxon Mobil was defending itself in New York state court against allegations that it had misled investors by saying publicly that it estimated higher future costs of climate change regulations when it evaluated potential oil & gas projects – when it was actually basing those decisions on current costs, and assumptions that the regulatory environment wouldn’t change.

Among other things, the complaint by the New York Attorney General alleged violations of the state’s Martin Act, which turns on whether there’s a misrepresentation or omission of material facts. The alleged misrepresentations were made by Exxon in reports that were published back in 2014 in exchange for the withdrawal of two shareholder proposals – and were then repeated in other reports such as the company’s “Corporate Citizenship Report.”

Earlier this week, the judge on the case issued this 55-page opinion in Exxon’s favor. Basically, the decision came down to a finding that investors didn’t care about the info – there was no market impact and the info wasn’t “material” when considered with the total mix available in the company’s 10-K and other disclosures. The judge also accepted Exxon’s argument that the company’s internal practices didn’t impact its financials.

This was a big victory, but it’s pretty fact-specific (as detailed in this “D&O Diary” blog) – and you’ve gotta wonder whether the outcome would be the same if the allegations were based on more recent disclosures, since current-day investors keep claiming they care about this stuff. Exxon continues to face other “climate change” lawsuits – including a consumer protection case in Massachusetts. And they aren’t alone. This Davis Polk blog notes that at least one D&O insurer is observing a growing number of climate-related claims – and that it will consider that risk during underwriting. Here’s an excerpt:

Among 28 countries, 75% of climate-related cases brought to date were in the United States alone. The firm anticipates that the failure to disclose climate change risks may drive claims in upcoming years. Moreover, a company’s lack of responsiveness to overall environmental, social and governance (ESG) issues, including ethical topics, can cause brand values to plummet. The insurer warns that, when gauging a company’s reputation, underwriters of D&O insurance will consider the nature and tone of comments made on social media relating to the company.

November-December Issue of “The Corporate Counsel”

We recently mailed the November-December issue of “The Corporate Counsel” print newsletter (try a no-risk trial). The topics include:

1. Hedging Disclosure Is Here—Are You Ready?

– Background of Hedging Disclosure Requirement

– What Item 407(i) of Regulation S-K Requires

– Applicability & Effective Dates

– Interpreting the New Hedging Disclosure Requirement

– Rule Applies to Broad Categories of Transactions

– Elaborate Policy Not Required

– Drafting Proxy Disclosure

– Evolution of the Staff’s Non-GAAP Comments

– What is “Tailored Accounting?”

– Where is the Staff Raising “Tailored Accounting” Comments?

– Comments On Acquisition-Related Adjustments

– Five Key Takeaways on Tailored Accounting