Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

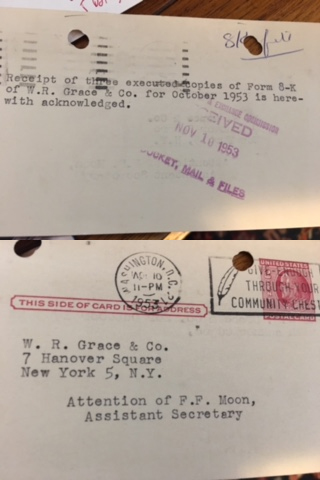

Big hat tip to Sean Dempsey for sending me this awesome receipt – stamped by the SEC – acknowledging the filing of a Form 8-K by his company, W.R. Grace in 1953:

I love hearing stories from old-timers about making filings before Edgar was born. Personally, I remember being on the Corp Fin Staff in the ‘80s & going outside to get a little fresh air on days that happened to be 10-Q or 10-K filing deadline days. The line of FedEx trucks went on for blocks. I barely noticed…

Another Cool License Plate!

Check out this license plate from Jim McRitchie, who has run the “CorpGov.net” website forever (his wife is part-Hawaiian; hence the turtle-themed plate holder):

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Board Evaluations: How They Are Evolving

– Multi-Class Companies: CII Appeals to Delaware

– Crisis Management: Public Relations Considerations

– D&O Insurance: Outlook for 2020

– Gov. Investigations: Key Questions When You Get An Investigative Request

Recently, I blogged about when a SEC Staffer kicks off their public remarks with a disclaimer that their remarks are their own and not those of the Commission. I mused that the origins of this disclaimer seem to have been forgotten. I then heard from a number of members with remembrances and their own research on this topic.

(b) Reference to official position. An employee who is engaged in teaching, speaking or writing as outside employment or as an outside activity shall not use or permit the use of his official title or position to identify him in connection with his teaching, speaking or writing activity or to promote any book, seminar, course, program or similar undertaking, except that:

(2) An employee may use, or permit the use of, his title or position in connection with an article published in a scientific or professional journal, provided that the title or position is accompanied by a reasonably prominent disclaimer satisfactory to the agency stating that the views expressed in the article do not necessarily represent the views of the agency or the United States; and

And former SEC General Counsel Dan Goelzer dug back even further – noting that the disclaimer appears in “Rule 4 (Outside Employment and Activities)” of the SEC’s “Regulation Concerning Conduct of Members and Employees and Former Members and Employees of the Commission.” Rule 4(d)(2)(ii)(A) contains the current version of the disclaimer:

Therefore, such publication or speech shall include at an appropriate place or in a footnote or otherwise, the following disclaimer of responsibility: “The Securities and Exchange Commission disclaims responsibility for any private publication or statement of any SEC employee or Commissioner. This [article, outline, speech, chapter] expresses the author’s views and does not necessarily reflect those of the Commission, the [other] Commissioners, or [other] members of the staff.”

Dan isn’t quite sure when the disclaimer originated, but he does know it was prior to 1980. In 1980, the SEC made various revisions to that conduct regulation – and while a number of changes to Rule 4 are described in that ’80 release, the disclaimer is not one of them. Therefore, we think that the disclaimer was in the pre-1980 version of Rule 4 as well. To bolster the point, Dan sent over two pre-1980 speeches – by Al Sommer (a SEC Commissioner at the time) and Alan Mostoff (then the IM Director) – that include the disclaimer. So it goes way, way, back…

How to Submit Comments on the SEC’s Rulemaking

Among the hundreds of “checklists” posted on our site is this one about how to submit comments on a SEC’s rulemaking. Now the SEC has posted this 90-second video about how easy it is to submit comments on a rule proposal. It has over 350 views within a few months…

Our October Eminders is Posted!

We’ve posted the October issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

Wow! All that is new is “old” again! When I first joined Corp Fin in 1988, there were a half dozen or so “pods” – each with two branches – that were devoted to specific industries. Each pod was headed by an Assistant Director, which was a difficult job to obtain because a slot only opened when someone retired (back then, it was quite rare for an AD to leave the SEC before retirement). Over time, the Division’s “groups” (as they were eventually renamed from “pods”) grew and the number of them nearly doubled. Now, with this Corp Fin announcement on Friday, we’re going back to the way we were.

Here’s some things to note:

1. Cutting the Number of Groups Nearly in Half – Corp Fin is realigning some of industry groups and reducing them in number from 11 to 7. The groups are now called “Offices” – led by a “Chief” and a “Senior Advisor.”

2. Improving (& Streamlining) the Review Process – Led by an “Office of Assessment & Continuous Improvement,” the teams within Corp Fin that will review filings look to be leaner under this new realigned group structure. There have been fewer comments issued in recent years by the Staff as companies have gotten better observing comment trends and adjusting their disclosures according (not to mention the sheer number of public companies has shrunk a whole lot). Corp Fin will continue to focus on improving the comment process in an effort to be more relevant, timely & consistent.

3. Focus on “Hot” Comment Areas – Led by an “Office of Risk & Strategy,” Corp Fin will focus on emerging issues in their comments – think Libor, cybersecurity and Brexit as recent examples. This Office will review filings for good (or bad) examples of disclosure and then share those internally. It’s something the Staff has already been doing – but it’s now formalizing that function.

4. What Group Is Your Company In? – These seven new groups took effect yesterday – so you can find your new industry group by looking on Edgar for your filing history and noting what “Office” is listed. For example, you’ll see in the 4th line down that Microsoft belongs in the “Office of Technology” group. In many cases, your company’s group will be the same. And if you have a filing that is being actively reviewed right now, the Staffers reviewing your filing aren’t going to change – even if the Office that your company belongs in has changed.

Corp Fin has pulled down its org chart – at least for now. We just deleted our own more comprehensive Corp Fin org chart. I’ve maintained it for 17 years but it’s become too hard to keep up. That was a harder task than you would think – very few people even within Corp Fin know the identities of all the middle managers, etc. A constant game of “Where’s Waldo”…

SEC Proposes to Modernize the OTC Market

Last Thursday, the SEC proposed to modernize the over-the-counter market (OTC) by proposing changes to Rule 15c2-11, which sets out certain requirements with which a broker-dealer must comply before it can publish quotations for securities in the OTC market. Here’s the 228-page proposing release.

Moody’s “Governance” Framework for Credit Ratings

Recently, I blogged how Moody’s was getting into the governance ratings business – but as I noted in that blog, Moody’s has scored governance for quite some time for their credit ratings business. Recently, Moody’s issued a framework to help understand key aspects of governance that are incorporated into all Moody’s credit ratings and analysis, including two taxonomies: a private taxonomy, which applies to non-financial corporates, financial institutions, infrastructure, structured finance and certain competitive government-owned enterprises; and a public taxonomy, which applies to sovereign, sub-sovereign and municipal issuers…

In our “Q&A Forum,” we have reached query #10,000 (although the “real” number is much higher since many queries have others piggy-backed upon them). So crazy. There was a time that I thought I should quit this gig when we hit 5000. For me, answering the questions is one of the hardest parts of this job. The first 14 years handling the queries was rough (even with help from many folks, including Alan & Dave) – but since John came on board three years ago, it’s been easy for me because he’s been the master handling that task.

Anyway, I know this is patting ourselves on the back – but it’s 17 years of sharing expert knowledge and it’s quite a resource. Combined with the “Q&A Forums” on our other sites, there have been well over 30,000 questions answered. We beat Alan Dye to the punch, as he has over 9600 questions answered over on Section16.net. He’ll get to 10,000 soon enough…

You are reminded that we welcome your own input into any query you see. And note there is no need to identify yourself if you are inclined to remain anonymous when you post a reply (or a question). And of course, remember the disclaimer that you need to conduct your own analysis & that any answers don’t contain legal advice.

It’s funny to me that this is even considered news. But it is rare these days. Corp Fin has posted a broad notice that it’s hiring lawyers with varying levels of experience. My 5-minute video about how to land a job at the SEC is exactly 10 years old. I looked a lot younger then…

Yesterday, ISS released the results of its benchmarking survey for the annual update of its voting policies. Here’s a summary:

1. Board Gender Diversity– Responses to ISS’ question about views on the importance of gender diversity on boards showed that majorities of both investors (61 percent) and non-investors (55 percent) agreed that board gender diversity is an essential attribute of effective board governance regardless of the company or its market. Among those who did not agree with that view, investors tended to favor a market-by-market approach and non-investors tended to favor an analysis conducted at the company level.

2. Director Overboarding – Investors and non-investors diverged on the question of measurement of how many boards is too many for an individual director. A plurality (42 percent) of investor respondents selected four public-company boards as the appropriate maximum limit for non-executive directors. A plurality of investor respondents (45 percent) also responded that two total board seats is an appropriate maximum limit for CEOs (i.e., the CEO’s “home” board plus one other). A plurality of non-investors responded that a general board seat limit should not be applied to either non-executives (39 percent) or CEOs (36 percent), and that each board should consider what is appropriate and act accordingly.

3. Climate Change Risk Oversight – A majority (60 percent) of investor respondents answered that all companies should be assessing and disclosing climate-related risks and taking actions to mitigate them where possible. 35 percent of investor respondents answered “Maybe” to the following statement about how companies should approach this issue: each company’s appropriate level of disclosure and action will depend on a variety of factors including its own business model, its industry sector, where and how it operates, and other company-specific factors and board members.

Only 5 percent of investors indicated that the possible risks related to climate change are often too uncertain to incorporate into a company-specific risk assessment model. Non-investor responses to those same three issues were 21 percent, 68 percent and 11 percent respectively. The actions that investors considered most appropriate for shareholders to take at companies assessed to not be effectively reporting on or addressing their climate-related risks were engagement with the company (96 responses), and considering supporting shareholder proposals on the topic (94 responses). Based on the number of non-investor responses, these two options were also ranked first and second in popularity by non-investors.

4. Mitigating Factors for Companies with Zero Women on Boards – ISS announced in 2018 that it is introducing a new U.S. Benchmark Voting Policy for 2020 to generally vote against or withhold from the chair of the nominating committee (or other directors on a case-by-case basis) at companies when there are no women on the company’s board, but with some mitigating factors that may be taken into account.

Respondents this year were asked whether ISS should consider other mitigating factors, beyond a firm commitment to appoint a woman in the near-term and having recently had a woman director on the board, when assessing such companies. Investor respondents were less likely than non-investor respondents to say that other mitigating factors (such as adopting an inclusive Rooney Rule-style procedure for candidate searches or maintaining an active recruitment process despite the absence of a boardroom vacancy) should be considered and may be sufficient to avoid a negative recommendation on directors.

5. Combined CEO/Chair– Investor respondents cited poor company responsiveness to shareholder concerns as the most commonly chosen factor that strongly suggested the need for an independent board chair. This was followed by governance practices that weaken or reduce board accountability to shareholders (such as a classified board, plurality vote standard, lack of ability to call special meetings and lack of a proxy access right). For non-investors, the most commonly chosen factor was a poorly-defined lead director role, followed by poor company responsiveness to shareholder concerns.

Is the SEC Seeking to Replace PCAOB’s Kathleen Hamm?

As I’ve blogged about several times over the years, one of the oddest provisions of Sarbanes-Oxley was Congress creating the PCAOB with a dotted line to the SEC. That means the SEC decides who gets appointed to the Board of the PCAOB. That has resulted in a few battles over time. Here’s an excerpt from this MarketWatch article by Francine McKenna:

Kathleen Hamm says her work as a member of the Public Company Accounting Oversight Board, the audit-industry regulator, is not done. But the Securities and Exchange Commission apparently thinks otherwise, and posted for her job over the summer. Hamm stepped into a term in 2017 that had approximately two years remaining, expiring this October. She is eligible for reappointment to the second five-year term, through 2024, but now she’s had to reapply for her job and she’s not sure why.

“I am seeking reappointment to continue the important work I began 20 months ago,” Hamm said in a statement provided by the PCAOB spokeswoman to MarketWatch. “My efforts have centered on protecting investors by applying my expertise and experience in technology, risk management, and compliance to upgrading and modernizing the PCAOB’s approach to cybersecurity and emerging technologies, both at the board and among the audit firms we oversee.”

Hamm was appointed to the PCAOB board after the SEC announced in December 2017 that it would appoint a full slate of five new members to replace all incumbents. The SEC had never before declined to reappoint PCAOB members who were eligible to serve another term, and it was the first time in the PCAOB’s 15-year history that the entire board was replaced all at once.

The new board members came on with staggered terms to fill out. Hamm is the second board member to have her term come up; Duane DesParte was renewed without fanfare after his original term expired after six months. Hamm said she’s pushed for an increased focus on the control systems that auditors use to ensure that they consistently deliver high-quality audits for the benefit of the investing public. “I would like the opportunity to continue to drive this vital initiative as well,” she said in her statement.

Jim Daly Retires!

Happy retirement to long-time Staffer Jim Daly! As noted in this press release, Jim served in Corp Fin for 38 years in a variety of positions – the latest being Associate Director – and mentored hundreds of folks as they came up through the ranks. He surely will be missed!

Recently, the PCAOB sanctioned PWC as a result of partners having a financial relationship with a bank the firm audited. Then the firm lied to the banks audit committee when it sent a letter to the committee saying there were no independence issues. The rules on this issue is not new. The SEC sanctioned another of the Big 4 firms – EY – as a result of similar problems some 30 years ago.

I too have served on an audit committee where a Big 4 firm sent us a letter saying there were no independence issues, only to find out the firm was aware of issues they withheld from the committee. This is a huge issue for audit committees and investors. The PCAOB’s sanction of $100k is a slap on the wrist in this instance. Which perhaps explains why we continue to see this type of behavior by the firm’s go unabated.

Does the PCAOB Undermine Auditor Professionalism?

Congrats to Dan Goelzer & Tom Riesenberg for launching their new blog – “The Audit Blog.” Here’s the intro from Dan’s blog about the PCAOB’s impact on auditor professionalism:

In 2002, the Sarbanes-Oxley Act created the Public Company Accounting Oversight Board and transformed public company auditing in the United States from a self-regulated, to a regulated, profession. The PCAOB’s statutory mission is to “further the public interest in the preparation of informative, accurate, and independent audit reports” — in other words, to improve audit quality. Based on objective measures, such as frequency of restatements and magnitude of financial reporting failure market losses, most observers would probably agree that the PCAOB has made considerable progress toward accomplishing that goal.

A separate issue is how PCAOB oversight has affected the experience of being a public company auditor and auditors’ perceptions of their professionalism. Three academic researchers, Kimberly D. Westermann, California Polytechnic State University, Jeffrey Cohen, Boston College, and Greg Trompeter, University of Central Florida, have undertaken to explore that topic. Their findings raise questions about the long-term impact of PCAOB oversight on the auditing profession.

CAMs: Snapshot of Filings By Types of Disclosures

Recently, Deloitte put together this nifty chart indicating what types of matters where deemed “CAMs” in recent filings by large accelerated filers. Check it out…

For the many of you that have registered for our Conferences coming up next Monday, September 16th, we have posted the “Course Materials” (attendees received a special ID/PW last week via email that will enable access to them; note that copies will be available in New Orleans). The Course Materials are better than ever before – with numerous sets of talking points. We don’t serve typical conference fare (ie. regurgitated memos and rule releases); our conference materials consist of originally crafted practical bullets & examples. Our expert speakers certainly have gone the extra mile this year!

Here’s some other info:

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take a few hours to post the video archives after the panels are shown live). A prominent link called “Enter the Conference Here” – which will be visible on the home pages of those sites – will take you directly to the Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: HTML5, Windows Media or Flash Player).

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here are the conference agendas; times are Central.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if it’s possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see our “CLE Credit By State” list.

– Register Now to Watch Online: There is still time to register for our upcoming pair of executive pay conferences – which starts on Monday, September 16th – to hear Keith Higgins, Meredith Cross, etc. If you can’t make it to New Orleans to catch the program in person, you can still watch it by video webcast, either live or by archive. Register now to watch it online.

– Register to Watch In-Person in New Orleans: Starting next Thursday, you will no longer be able to register online to attend in New Orleans – but you can still register to attend when you arrive in New Orleans! You just need to bring payment with you to the conference and register in-person. Through the end of next Thursday, you can still register online to attend in-person in New Orleans. And you can always register online to watch the conference online…

More on “Directors, How Well Do You Really Know the Shareholders You Represent?”

Recently, I blogged about a cute little cocktail party story where a director failed to follow-up with probing questions to a retail shareholder he met at a party. One of our members had this comment in reaction:

David Shaw’s story likely is the fault of lawyers. Indeed, many lawyers routinely tell directors they have no right to speak for the corporation and have no obligation to do so. These lawyers proceed, telling clients that a corporation must speak with one or two – perhaps three (for example, CEO, CFO and IR head) voices – and no more. Threat of liability is the clear concern, but perhaps overstated today relative to the need for companies – and their directors – to understand the perspectives of other stakeholders.

SEC Sanctions for 10-K Misrepresentation on Loan Covenant Compliance

In this blog, Stinson’s Steve Quinlivan describes the facts behind the SEC’s recent enforcement action against a company – Omega Protein – for its 10-K disclosure that it “was in compliance with all of the covenants contained” in its borrowings (repeated in three subsequent 10-Qs)…

A few months ago, we blogged about how Corp Fin was considering changing how their “referee” role. Well, that change has happened. On Friday, Corp Fin announced that some of its no-action responses going forward may be in oral form rather than in writing. A written response can be expected if Corp Fin “believes doing so would provide value, such as more broadly applicable guidance about complying with Rule 14a-8.”

Here’s a few “food for thought” items to start with (thanks to Ron Mueller & Dave Lynn for their 10 cents on some of these):

1. Will There Really Be No Writings?– Good lawyers like to see things documented, particularly if they achieve a result they seek. So mere oral responses may feel like kissing your sister. Surely, Corp Fin will have some type of writing somewhere about their decision?

This announcement seems like the kind of approach that Corp Fin’s accounting staff has employed over the years for financial statement waivers – and that Chief Counsel’s office has used with S-3 eligibility waivers. In both situations, I believe the Staff still puts an internal (ie. nonpublic) note up on Edgar, so maybe they will do the same thing here. Of course, if this writing is nonpublic, that’s not doing you much good…

2. Can I Record My Conversation With Corp Fin? – If a Staffer leaves a voicemail as its oral response, you’ll at least have some sort of “writing” that you can archive and share with your working group. But what if you pick up the phone when they call? Can you tape it? Or should you just write a memo to the file memorializing the conversation?

I guess you’ll find out when you ask (I wouldn’t record the convo without the Staffer’s permission). But I threw this item in here so I can go back in the day to when I started in Corp Fin in the late ’80s. Back before computers. We wrote comment letters by hand – they would eventually get typed up by a secretary. But the Corp Fin “branches” had one secretary for about 10 lawyers. So comment letters didn’t get typed up until the deal went to market in most cases. Instead, Staffers would call and read off their comments over the phone – and the law firm on the other side would record the conversation and transcribe it. So there is some sort of precedent…

3. What Happens If Corp Fin Doesn’t Take Any Position? – Corp Fin’s announcement states that the Staff’s failure to take a position on a no-action request should not be construed as an indication that the company’s failure to include a shareholder proposal in its proxy materials is a violation of Rule 14a-8. As noted in this Gibson Dunn blog, the Staff may now more frequently decline to give a definitive response. That used to be rare – perhaps now it will be more common.

Gibson Dunn notes: “In considering whether to omit a proposal in such situation, a company will need to consider the potential reaction of its shareholders, the risk of adverse publicity, possible reactions from proxy advisory firms (discussed below), the risk of litigation, and the possibility that including the proposal in its proxy statement will attract more proposals in future years.”

4. Why Bother Seeking No-Action Relief At All? – Unfortunately, this Corp Fin position doesn’t change anything for companies in terms of spending resources to seek no-action relief. (Remember that a no-action response only means that Corp Fin won’t refer the matter to the SEC’s Enforcement Division if a company excludes a shareholder proposal from the proxy. It ain’t a “get out of jail free” card).

Companies still are required by Rule 14a-8 to notify Corp Fin that they intend to omit a proposal and the “reasons” for excluding it, and since (at this point at least) we don’t have a good sense of when Corp Fin will respond with a definitive position, companies still have to make as strong of a case as they can because you don’t want to be so unconvincing that Corp Fin says (whether orally or in writing) that they don’t concur.

5. Will Corp Fin’s Announcement Result in More Lawsuits? – Corp Fin’s announcement notes – as has always been the case – that proponents & companies are free to seek adjudication of the Staff’s positions in federal court. Personally, I don’t think we’ll see more lawsuits.

For the bigger investors that have submitted shareholder proposals in the past, they may gravitate to other methods to pressure companies in the wake of the Staff’s new position – for example, engage in more “just vote no” campaigns or more joint activities with other investors to apply pressure. Lawsuits take too long, cost too much and the judges involved typically don’t know the nuances of the securities laws. But you never know, maybe we’ll see more litigation after all…

6. Will Corp Fin Give Broader Guidance More Frequently? – As noted in this Gibson Dunn blog, “The Staff announcement indicates that one instance in which the Staff will issue response letters will be to provide “more broadly applicable guidance about complying with Rule 14a-8.”

Although the Staff has on occasion used a Rule 14a-8 no-action response to elaborate on its interpretation of the rule, historically the Staff has utilized Staff Legal Bulletins to provide “more broadly applicable guidance” regarding its interpretation of Rule 14a-8. The Staff’s announcement appears to suggest that it now will more commonly spring guidance on the shareholder proposal community in the middle of the season and in the context of specific factual situations, which may make such guidance harder to apply in other contexts than if the Staff addressed such issues more generally.”

Tomorrow’s Webcast: “Secrets of the Corporate Secretary Department”

Tune in tomorrow for the webcast – “Secrets of the Corporate Secretary Department” – to hear Norfolk Southern’s Ginny Fogg and Home Depot’s Stacy Ingram debunk myths on how to run the corporate secretary department, as well as provide oodles of practice pointers on how to leverage outside resources & technology; tips for caring of the board; managing a budget; streamlining the board materials process; optimizing director orientation & education; and much more.

Poll: Desirability of Receiving Oral Responses to No-Action Requests?

Please take a moment to participate in this anonymous poll:

With reputational issues continuing to emerge as a real risk for companies, I wonder if we might someday see risk factors about high profile leaders within a company being politically active on one side of the partisan fence or the other. A case in point is Stephen Ross, the board chair of the parent company for Equinox and SoulCycle – Ross held a fundraiser for the President and, as noted in this article, members of those fitness centers have been cancelling their memberships in droves.

With a Presidential election only about a year away – and the influence of social media these days – I imagine this sort of thing is bound to happen more frequently. With real-world implications for a company’s bottom line…

Risk Factors: Gun Violence

Last week, John blogged about “active shooters” causing companies to consider risk factors about gun violence. In addition to the recent shootings causing people to take to the streets to protest the lax gun laws in this country, with the rising number of shareholder proposals targeting gun violence in recent years, it shouldn’t be a surprise that risk factors focusing on this topic are surfacing. Here’s the intro from this WSJ article:

A handful of public companies have begun quietly warning investors about how gun violence could affect their financial performance. Companies such as Dave & Buster’s Entertainment, Del Taco Restaurants and Stratus Properties, a Texas-based real-estate firm, added references to active-shooter scenarios in the “risk factor” section of their latest annual reports, according to an analysis of Securities and Exchange Commission filings. The Cheesecake Factory Inc. has included it in its past four annual reports.

The disclosures come as fatalities in mass public shootings have surged in recent years. Between 2016 and 2018, active shooter incidents left 306 people dead and 850 wounded, according to the Federal Bureau of Investigation. That’s up from the previous three years, when active shooters killed 136 and wounded 181. The FBI defines an active shooter incident as one or more shooters attempting to kill people in a crowded area.

How to Track Changes on Corp Fin’s CDIs Pages

A few days ago, I was moaning about the challenges of determining which CDIs were updated when Corp Fin makes a change. My good friend – McKesson’s Jim Brashear – reminded me about the tracking software available out there. For many years, I used Copernic to track many pages on the SEC’s site – but then that software was no longer supported and I got lazy and stopped tracking anything.

Jim informs us that there are some SAAS apps that provide similar functionality to Copernic. Some of the more prominent ones are ChangeTower, Distill.io, Fluxguard, Sken.io, Versionista, Visualscalping and Wachete..

I imagine I could place “better than sex” in the title for any blog and it would wind up as the most popular blog for the year. So thank me for not using that type of trick on the regular. But yes, the SEC did issue guidance on proxy advisors yesterday. Proxy advisors. A topic that many can’t get enough of. So that truly is gold for bloggers looking for attention. I didn’t really need the “better than sex” hook I guess. But I “doubled down” anyway.

Here’s what the SEC did:

1. The SEC issued this 14-page interpretive release about how the proxy rules impact proxy advisors. It forces proxy advisors to take more steps to disclose how they craft their recommendations – and the SEC issued a broad warning for when they convey incorrect information.

2. The SEC issued this 26-page interpretive release about proxy voting responsibilities for investment advisors, providing steps that mutual fund managers should consider if they become aware of potential factual errors or weaknesses in a proxy advisor’s analysis. (Here’s the press release about both of the SEC’s new interpretive releases – and here’s a WSJ article.)

3. Each piece of guidance passed with a vote of 3-2, with the two Democrat Commissioners dissenting (Robert Jackson & Allison Herren Lee).

4. All five of the SEC Commissioners pushed out their opening statements about the new guidance promptly – they came out even before the SEC’s press release. I believe that was a first…