Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

In response to the mechanical questions about how to handle the Inline XBRL for ’34 Act filings – including the exhibit index – Corp Fin issued a set of 9 CDIs yesterday in the area. Here’s a Gibson Dunn blog about them. Hopefully, this will be the last time I ever blog about Inline XBRL…

By the way, the new CDIs don’t show up under “What’s New” on the Corp Fin page. And the way the relatively new CDI section is constructed, the only way to sleuth which CDIs are new – when the SEC pushes out an email indicating there is something new – is to click on each section of the CDIs and look at the “update” date. Something for which I receive a handful of complaints from members each time any CDIs are added or changed…

SEC Brings First Reg FD Case In Nearly Six Years

Yesterday, the SEC brought this Reg FD enforcement case against TherapeuticsMD based on its sharing of material, nonpublic information with sell-side analysts without also disclosing the same to the public. This should be one of the least controversial FD actions the SEC has brought – with pretty clear “selective disclosure” violations of FD on two occasions. Really egregious conduct including the fact that the company didn’t have FD policies or procedures. The company was fined $200k…

The SEC hadn’t brought a Reg FD case since September 2013 (the SEC never did bring a Reg FD enforcement action against Elon Musk for his tweets last year) – here’s a list of the 16 SEC enforcement actions involving Reg FD over the years…

Mandatory Gender Quotas for Boards: California Gets Sued

As noted in this press release, Judical Watch has sued the State of California over its new law that requires up to three women being placed on the boards of companies incorporated in that state. The primary claim of the lawsuit is that the law is unconstitutional. Here’s an article from the “Sacramento Bee” – and see this Cooley blog…

Yesterday, the Business Roundtable got a ton of press by issuing this statement with its view that the “purpose” of a corporation should be changed so that “shareholder primacy” is a thing of the past. Nearly 200 CEOs signed onto the BRT’s statement. Bye-bye Milton Friedman’s decades-old theory to “maximize value for shareholders.” How many of you will need to cover your tattoo of that phrase?

Shifting from shareholder primacy would be quite a change in focus for management & boards – from one devoted primarily to shareholders to one that would be a mix of stakeholders, including employees, customers, suppliers, the environment, communities and shareholders. Under the BRT’s new formulation, companies say they’ll consider the competing interests of the stakeholders (presuming they’re not conflicted). While most state corporate law already allows for this in some form, things like promoting employee welfare at the short-term expense of shareholders are typically justified by boards & management as something that will also improve long-term shareholder value (some shareholders are more amenable to that than others).

Elizabeth Warren loves the idea – she proposed legislation along these lines last year. But understandably, large shareholders aren’t happy about the BRT’s move – here’s a statement from the Council of Institutional Investors.

A few years back, I was at a non-business cocktail party, chatting with someone I had just met. It was a great conversation, as I recall, until I learned that he was a board member of a company in which I held stock, and I shared that fact with him. My holdings were small, comparatively, but large enough to be very relevant to me. This may have been a wonderful opportunity for this board member to ask some questions of me, get my opinions — you know, get to know one of the owners. The other parts of our conversation had been vigorous and interesting.

You can guess what happened, of course. The conversation died out quickly, and drinks needed refilling. And we didn’t speak again that night, or any other time. Fully understanding the desires and goals of shareholders is a key to good company governance, and in this regard directors at publicly traded companies can take a lesson or two from their private company counterparts, especially when it comes to the growing conversations around environmental, social and governance (ESG) issues.

Transcript: “Current Developments in Capital Raising”

We’ve posted the transcript for our recent webcast: “Current Developments in Capital Raising.”

Hats off to Stinson’s Steve Quinlivan for listing recent SEC filings with CAMs in them. Steve notes that “there are a number of audit reports from smaller accounting firms on smaller issuers which indicate no CAMs were identified. Some may think this will change when the Big 4 start issuing reports on those beneath the large accelerated filer tier. That may be the case, but large accelerated filers by their nature seem to have complex accounting, which may not be true for smaller issuers and a finding of no CAMs may be appropriate.” And note this quote from this article by MarketWatch’s Francine McKenna:

Even though CAMS should, in theory, “enhance the informativeness of the audit report,” the researchers caution that their findings suggest that business priorities “may discourage auditors from disclosing important direct-to-investor communications that might make their clients look bad, and instead encourage auditors to withhold such information.”

Are Companies Punishing Their Auditors for Flagging Their Material Weaknesses?

As reflected in this article by MarketWatch’s Francine McKenna, this new study about internal controls reporting by independent auditors is getting a lot of press. Here’s the intro from this “Accounting Today” article (also see this WSJ article):

Auditing firms that tend to find material weaknesses in companies’ internal controls are seen as less attractive in the audit market, according to a new study. The study, by Stephen P. Rowe and Elizabeth N. Cowle of the University of Arkansas, looked at 13 years of data from 885 local offices of 358 audit firms in the U.S., and found offices that reported material weaknesses in internal controls over financial reporting for one or more clients in the course of a year saw their average fee total in the following year grow by about 8 percent less than would have been the case had they issued none. That decline was in addition to lost fees from clients who were found to have internal control material weaknesses, or ICMWs, and responded by switching auditors, which was something that companies tagged with ICMWs were often found to do by the researchers.

“Don’t Make Me Look Bad: How the Audit Market Penalizes Auditors for Doing Their Job.” That’s the title of a study being presented at this week’s annual meeting of the American Accounting Association. While it may not portray companies in the most favorable light, at the same time it’s merely the latest suggestion that auditors might not necessarily lean toward rendering unbiased opinions on paying clients.

“Presumably, audits that provide useful information to users of financial statements should serve to increase the credibility of financial statements and, in turn, increase auditor reputation,” the study’s authors write. But the research found exactly the opposite, at least with respect to one essential service auditors are required to perform: flagging material weaknesses in companies’ internal controls over financial reporting, a responsibility mandated by the Sarbanes-Oxley Act (SOX).

It’s a subject that has come up before, but now there is research that suggests that women CEOs are at higher risk of a brush with an activist than their male counterparts. Because these activists have the ear of institutional shareholders and strike fear in the heart of board members, creating a concrete plan for confronting these threats should top the to-do list of any female CEO. Nelson Peltz, a well-known activist who has targeted his share of female CEOs, told CNBC he is “gender blind.” Whether a firm lives up to its potential is all he cares about, he says. If it’s performing up to expectations, he’ll leave it be. If it ain’t making the numbers, he swoops in.

An investment banker who works on activist issues told me this week that Messrs. Icahn and Peltz could look at three dozen or so criteria in evaluating whether to launch a campaign against a company. “Whether the CEO is a man or woman is absolutely, positively not on that list.” Academics started taking a look for potential bias after a string of prominent women leaders—including Marissa Mayer (Yahoo), Mary Barra (GM), Meg Whitman (HP), Indra Nooyi (Pepsi) and Sandra Cochran (Cracker Barrel)—had battles with activists, who are almost exclusively men. Former Mondelez International Inc. CEO Irene Rosenfeld told The Wall Street Journal in 2015 that dealing with Mr. Peltz consumed 25% of her time. Ursula Burns relinquished Xerox Corp.’s CEO title after a confrontation with Mr. Icahn. Ellen Kullman led Dupont’s successful fight against Mr. Peltz in 2015, but abruptly retired five months later amid deteriorating results.

Recently, a member asked this in our “Q&A Forum” on CompensationStandards.com (#1287):

Instruction 10 to Item 402(u) provides that, where there is a CEO transition, the registrant may use the “PEO serving in that position on the date it selects to identify the median employee and annualize that PEO’s compensation.” Since the new CEO would, of course, not have been the CEO when the Year 1 median employee was selected, would this mean that, whenever the registrant has a CEO transition and wishes to annualize the new CEO’s compensation for purposes of the pay ratio, it needs to identify a new median employee on a date when the new CEO was serving? Thanks.

In response, I noted:

This was a fairly common point of discussion this past year – and just this week – at the JCEB meeting and the consensus was that the change in CEO is not intended to override the ability to use the prior year’s median employee determination process. This is just one area where language in the rule is imprecise in a number of areas when applied in the ‘Year 2’ context.

What’s the “Latest Practicable Date” for S-4 Comp Tables?

Some of us have been internally debating what the “latest practicable date” means for purposes of S-4 compensation disclosures. There often are public-public deals with S-4 filings that are updated and amended four or five times before going effective six months after the S-4 is first filed with the SEC. In these S-4s, they start describing all the compensation arrangements as they are back at signing – but six months later, the company is still using some date that is quite a bit earlier (or, in some cases, a future date that is expected to be the closing) to show compensation “as of the latest practicable date.”

Here are various thoughts from folks that I reached out to:

– For a long time, I’ve trying to connect the dots of “latest practicable date” and compensation disclosures and S-4. I can’t find anywhere in S-4 itself that references “latest practicable date” and I only found a few references of it in Item 402 of Regulation S-K – (1) with respect to not being able to calculate salary or bonus and so you would provide it in a Form 8-K, and (2) with respect to golden parachute compensation. I don’t think item (1) would apply for an S-4 as an issuer would theoretically already have get this squared away for its 10-K. As such, I assume we are referring to calculating golden parachute payments where we pick a triggering date as of the latest practicable date and that the payment is based on a price that is not yet determined (such as a stock price).

– My personal approach to “latest practicable date” (a similar term is used in Item 403 for stock ownership tables – “most recent practicable date”) is to update the information so that by the time the registration statement is declared effective, it provides substantively materially accurate information within a reasonable period of time. In other words, as always said by the SEC, “it depends on the facts and circumstances” and don’t make any material misstatement or omissions. My goal would be to set up a calculation so that you can plug in the variable for the answer. This means your comp information could be within 1-3 weeks of going effective (based on filing and amendment and then getting SEC sign-off). If it makes sense, you could also use a variable approach showing payments at different levels based on different assumptions (e.g., high/medium/low).

Generally, executive comp tables must include the last completed fiscal year. Consider CDI Regulation S-K, Ques. 117.05 with regards to updating comp tables in an S-1 or an S-3. Also make sure you are comfortable that there are no material misstatements or omissions. I would also consider providing updates to the extent that there have been changes made in disclosures pursuant the acquisition agreement (e.g., in the disclosure schedules).

– Our view is that (leaving aside how material the volume of comp data really is), we would go with less is more so would leave it until there’s a specific rule or comment to change it. If there’s no SEC comment, we think a lot of S-4 issuers leave well enough alone, so they don’t have to take another cut at comp beyond once for S-4 purposes. Even if perhaps “latest practicable date” means that comp really should be updated to final, that’s easier said than done and sometimes impacts the type of prospectus that can be used and seems more trouble than it’s worth (not to mention the legal costs)).

– If the deal straddles two fiscal years, and forward incorporation by reference is not available, I would probably advise the registrant to roll forward when new annual numbers become available. Otherwise I’ve never thought of the executive compensation tables as ones that had to be updated more frequently than that.

– In most other contexts where “latest practicable date” or “recent practicable date” is used, I’ve had the Corp Fin Staff comment if it wasn’t in the last month or two. I would think the other issue, from a shareholder vote perspective (for deals where there is a vote) is making sure the s/h has all the material information they need to make an informed vote.

– I assume this is talking about the golden parachute comp disclosures, in which case it doesn’t seem like the Staff is too focused on those and my hunch is that companies get away with sticking with the initial date used in the first filing. The few deals I’ve been involved in that have included this disclosure haven’t been updated, but none of those were long registration processes. But I bet if you actually asked the Staff, they’d say it should be updated as time passes.

My blog earlier this week about Inline XBRL caused a stir. It appears that a majority of large accelerated filers forgot to make changes caused by Inline XBRL to the exhibit index for the 2nd quarter 10-Qs they recently filed. We’ve fielded a number of follow-up questions in our “Q&A Forum” (see #9960). If you’re wondering what you should do, check that out. If you already filed a 10-Q without expressly referencing exhibit 104, it’s not something to be too concerned about as I highly doubt this is a high priority for the SEC Staff…

SEC Chair Clayton on Short-Termism & ESG Disclosure

In this blog, Cooley’s Cydney Posner summarizes SEC Chair Clayton’s “E&S disclosure” thoughts captured recently in this “Directors & Boards” article. Cydney notes his commentary is nuanced – and it dovetails with a number of prior remarks on this topic by Chair Clayton and Corp Fin Director Hinman…

Our August Eminders is Posted!

We’ve posted the August issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

Last week, Moody’s Investors Service published a scoring framework for assessing the governance characteristics of public companies not in the financial service area. Moody’s has scored governance for quite some time, but that was for their credit ratings business – this is a new “governance ratings” framework that stands alone. In other words, Moody’s has long incorporated governance issues into their credit ratings, but this is a new “Governance Assessment” which is separate from their credit ratings. But of course, the analysis for the two types of ratings will be somewhat related – you can think of it as a more comprehensive evaluation of the relevant governance factors that already contribute to a rating.

The new “GAs” provide stand-alone assessments of certain aspects of governance risk relative to defined benchmarks considered from the perspective of the potential impact on creditors. Five key components underpin Moody’s GA scores – ownership and control, compensation design and disclosure, board of director oversight and effectiveness, financial oversight and capital allocation, and compliance, controls and reporting. Each of the five components are scored by assessing several subcomponents.

GAs are expressed using a four-point scale between GA-1 and GA-4. Companies assessed at GA-1 have overall governance practices that generally score at the highest level based on our framework. Companies assessed at GA-4 have overall governance practices that generally score at a lower level.

Data used to conduct GA are sourced only from public disclosures like regulatory filings and investor presentations. Where disclosure is lacking, Moody’s GA will penalize the company and result in a less favorable score relative to the benchmark.

5 Takeways From the Proxy Season

In our “Proxy Season Developments” Practice Area,” we are posting the many reports recapping the recent proxy season as usual – including this note from EY’s Center for Board Matters that lists the top five takeaways…

Also see this blog by BlackRock’s Barbara Novick that has a host of stats for the proxy season…

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– What’s the “Long Term Stock Exchange”?

– Director Overboarding: The Latest Stats

– Board Recruitment: More Companies Looking for IR Expertise

– Attorney-Client: Preserving Privilege in a Crisis

– Expert Witnesses Aren’t Always Experts at Being Expert Witnesses

These Principles have also been updated to address SRD II with ‘avoidance’ added to ‘management’ of conflicts-of-interest with regard to the policy which should be disclosed. It also responds to feedback from the 2019 BPP Stakeholder Advisory Panel, acknowledging that conflicts of interest will always exist; therefore it is incumbent upon the BPP Signatories to have proper policies in place to try to avoid such conflicts wherever possible and when they do arise, to be transparent and manage them properly. The 2019 BPP Review Stakeholder Advisory Panel also reiterated the importance of the more stringent updated “Apply and Explain” approach for BPP Signatories to follow in light of SRD II Article 3j in relation to the Principles.

Another further area the updated Principles focused on was delineating the scope of proxy advisors’ responsibilities versus those of investors, in light of continued market misperceptions regarding the alleged overinfluence of proxy advisors and/or alleged “robo-voting” on the part of investors.

CEO Removals: Reputation Beats Financial Performance? Does Your Clawback Match?

During our upcoming “Proxy Disclosure Conference,” we have a panel devoted to the #MeToo era and how it might impact how your clawbacks (should) work. This PwC study shows how more CEOs were dismissed in the last calendar year for ethical lapses than for financial performance or conflicts with the board. So updating your clawback policies might be appropriate…

Reduced Rates Expire at End of This Friday: Our “Proxy Disclosure Conference”

– The SEC All-Stars: A Frank Conversation

– Hedging Disclosures & More

– Section 162(m) Deductibility (Is There Really Any Grandfathering?)

– Comp Issues: How to Handle PR & Employee Fallout

– The Top Compensation Consultants Speak

– Navigating ISS & Glass Lewis

– Clawbacks: #MeToo & More

– Director Pay Disclosures

– Proxy Disclosures: 20 Things You’ve Overlooked

– How to Handle Negative Proxy Advisor Recommendations

– Dealing with the Complexities of Perks

– The SEC All-Stars: The Bleeding Edge

– The Big Kahuna: Your Burning Questions Answered

– Hot Topics: 50 Practical Nuggets in 60 Minutes

Reduced Rates – Act by August 2nd: Proxy disclosures are in the cross-hairs like never before. With Congress, the SEC Staff, investors and the media scrutinizing disclosures, it is critical to have the best possible guidance. This pair of full-day Conferences will provide the latest essential—and practical—implementation guidance that you need. So register by August 2nd to take advantage of the discount.

Don’t forget that Inline XBRL (known as “iXBRL”) tagging will be required for Form 10-Q filings by large accelerated filers this quarter, following the June 15th phase-in period set by the SEC. This means that for many large calendar year-end companies, second quarter 10-Qs should be tagged with iXBRL, as well as the cover page of any “subsequently filed” Form 8-K. Skadden’s Ryan Adams reminds us of a few items that may have gone under the radar as companies begin to implement these changes, including a few potentially surprising new requirements in the exhibit index:

The Instructions to 601(b)(101) of Regulation S-K were recently amended to require that for Interactive Data Files, the exhibit index must include the word “Inline” within the title description for any XBRL-related exhibits. This comes along with an amendment to require a new Exhibit 104 containing cover page iXBRL data. As a result, all 10-Qs filed by companies that are required to comply with iXBRL should include both an Exhibit 101 and an Exhibit 104 – although the EDGAR Filer Manual provides that Exhibit 104 can be included in the Interactive Data File covered by Exhibit 101.

In addition, all 8-Ks that are required to comply with iXBRL should include an Exhibit 104. Not only are these changes somewhat unheralded, but eCFR currently has an incorrect version of the Item 601(a) table – showing that Exhibit 104 isn’t required for 10-Qs or 10-Ks. This is causing a lot of confusion as second quarter 10-Qs get filed.

“Gaming” Tokens Not Securities: Corp Fin’s No-Action Response

Any no-action letter signing off on a token is probably worth noting. Corp Fin issued this no-action response to “Pocketful of Quarters” last week indicating that – based on the facts presented – it wouldn’t recommend enforcement action if the company didn’t register its “gaming” tokens as securities. So this is a “definition of securities” no-action letter. See this blog by Stinson’s Steve Quinlivan…

Brexit Disclosure: New Developments to Consider

Here’s the intro from this blog by Cooley’s Cydney Posner:

With Boris Johnson as the UK’s new PM—and given his enthusiasm for Brexit and threat to leave the EU by October 31 even with a “hard” Brexit—it might make sense for companies to revisit the observations of SEC officials regarding the critical need for thoughtful and specific disclosures about Brexit. Note that the designated new head of the EU commission has said that “another extension [beyond the deadline of October 31] could be granted ‘if good reasons are provided’—such as holding a general election or second referendum.”

Reports from yesterday, however, indicated that Johnson’s election “has been greeted in Brussels with a rejection of the incoming British prime minister’s Brexit demands and an ominous warning by the newly appointed European commission president about the ‘challenging times ahead.’” To be sure, in terms of potential disruption, some practitioners have likened the havoc that Brexit could create to the chaos anticipated from the Y2K bug! But even if that analogy turns out to be a bit too apocalyptic, there’s no question that Brexit, especially a hard Brexit, could have a significant impact on many companies—and not just those based in the UK and EU. With that in mind, companies may want to reexamine and update their disclosures about the potential impact of Brexit on their businesses.

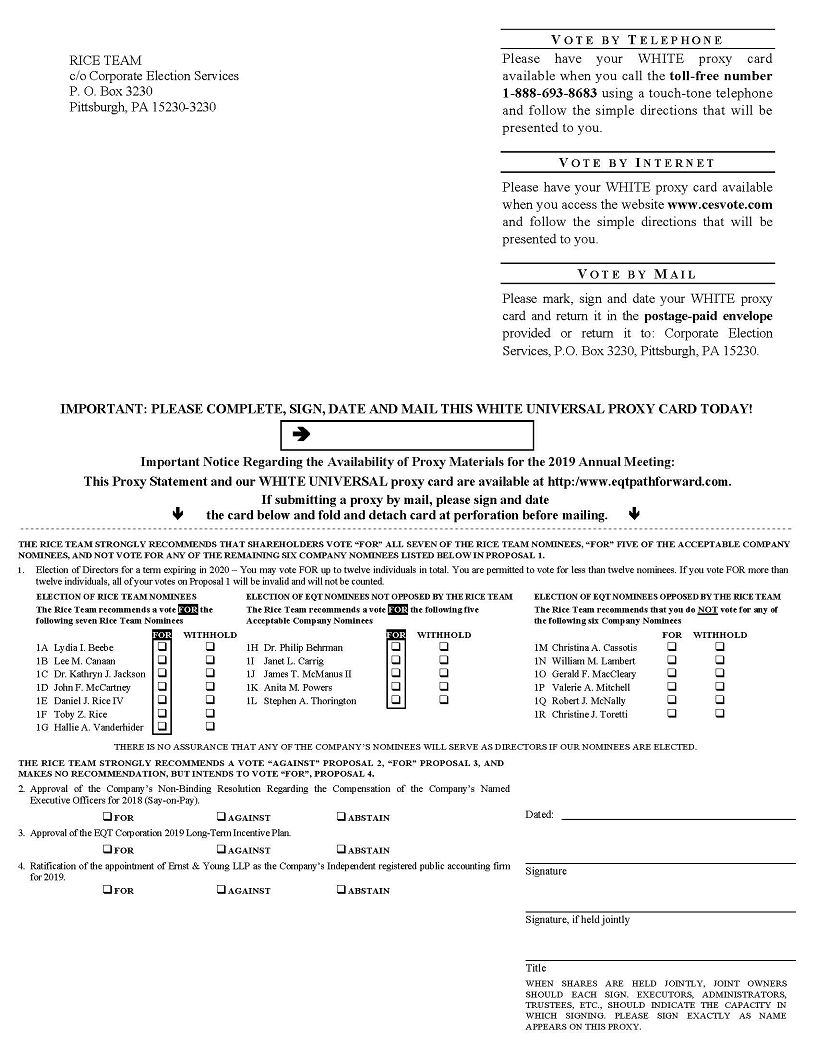

Yesterday, I blogged about how a dissident group won control of EQT’s board through a proxy fight that was waged using a universal proxy card. According to this Olshan memo, this marked the first time that such a card was successfully used in a control proxy contest in the US.

In the wake of the blog, a member asked this in our “Q&A Forum” (#9949):

In today’s blog, it says it’s the first time a dissident won control of a company’s board after a proxy fight using a universal proxy card. What about SandRidge Energy last year? SandRidge was considered the first company in the U.S. to let an activist board nominee onto its ballot. I didn’t follow that proxy fight very closely, but thought Carl Icahn ended up taking over SandRidge’s board.

After conferring with Andrew Freedman of Olshan, I provided this response:

Yes, there actually is a big distinction. SandRidge used a universal proxy, but Icahn could not. It relates back to the issue that Olshan covers in their alert about how company counsel is using advance notice bylaws and/or director nominee questionnaires to extract “consents” from dissident nominees, while not agreeing to provide reciprocal consents for the Company’s nominees to the dissident. Thereby creating a one-way advantage for the company to use a universal proxy card – while the dissident is left with a card that can only name the dissident’s nominees. The Rice Team & Olshan didn’t let EQT get away with that – they went to court.

The Challenges of Disclosing a CEO’s Illness

Over the years, I have blogged numerous times about the challenges of disclosing an illness for a senior executive (see this blog – and this blog). My good friend Bob Lamm delves into this sensitive topic in this blog about some recent CEO illnesses and the related disclosures…

Abigail Disney’s “Mini-Crusade” Against Disney’s Pay Ratio

I was out hiking in Laguna Beach the day Abigail Disney began her mini-crusade against Disney’s CEO pay ratio of 1,424-to-1. She laid it all out in a bunch of tweets. “Jesus Christ himself isn’t worth 500 times median workers’ pay,” she had said just weeks earlier.

Supporters and critics quickly jumped into their respective trenches. The former decried capitalism. The latter brushed off her remarks as socialist propaganda. (I exaggerate, but you get the point.)

Among her critics was Jeff Sonnenfeld, the ever-present Yale management professor. He pointed to Disney’s 580% stock return under Iger and the 70,000 jobs it’s created, and that the CEO’s pay still pales in comparison to that of some hedge fund managers, who don’t really create anything. “When pay and performance is properly aligned as it is at Disney, we need to recognize it,” he wrote.

What most of Abigail’s critics, including Sonnenfeld himself, failed to grasp was her actual point: That the wealth Disney’s created hasn’t been shared equitably with most of its employees.

In her lengthy series of tweets, she took a swipe at the shareholder-centric model of running companies and the consequences that sometimes follow for workers, the environment and surrounding communities. “When does the growing pie feed the people at the bottom?” she rhetorically asked the universe.

This question about what’s a fair sharing ratio — how much of the monetary gains of a successful company should be reaped by the single person in charge — is something I will explore in a series of stories later this year. (A sneak peek would be my piece from April about the CEO of a tiny California bank who took home twice as much as Jamie Dimon last year.)

As John blogged today on the DealLawyers.com Blog, here’s big news on the universal proxy front: yesterday, at EQT Corporation’s annual meeting, a dissident group won control of the company’s board through a proxy fight waged using a universal proxy card. According to this Olshan memo, this marks the first time that such a card was successfully used in a control proxy contest in the US. Here’s an excerpt:

The universal ballot adopted by both EQT and the Rice Team named both EQT’s and the Rice Team’s nominees on their respective proxy cards. The only difference related to the presentation of the two cards, in which each side highlighted how it desired shareholders to vote. Copies of the two cards can be found here (Rice Team) and here (EQT).

As shown, the Rice Team made clear on its proxy card a recommendation for all seven of its nominees and for five of the Company’s nominees that it did not oppose, to permit shareholders to vote for all 12 available spots. Similarly, the Company recommended a vote for all 12 of its nominees and against the Rice Team’s nominees, other than existing director, Daniel Rice IV, who was nominated by both EQT and the Rice Team.

The Rice Team obtained public support from many of EQT’s largest shareholders, including T. Rowe Price Group Inc., D.E. Shaw & Co., Kensico Capital Management Corp. and Elliott Management Corp., along with proxy advisory firms Institutional Shareholder Services (“ISS”) and Egan-Jones Ratings.

The use of a universal ballot for a majority slate of directors is unprecedented and, in our view, may become more common in future proxy contests given the Rice Team’s success here. In fact, ISS noted the following in its report recommending that shareholders vote for all of the Rice Team’s nominees on that team’s universal proxy card:

“The adoption of a universal card was an inherently positive development for EQT shareholders (as it would be in any proxy contest), in that it will allow shareholders to optimize board composition by selecting candidates from both the management and dissident slates.”

Despite pushing for the adoption of universal proxies, some activists had recently cooled on their potential use. For instance, as we blogged last fall, Starboard Value’s CEO Jeff Smith expressed concern that in its current form, the universal ballot might tip the playing field in management’s favor. It will be interesting to see if the outcome of yesterday’s EQT vote causes people to recalibrate that assessment.

Looking at Vote Requirements

Here’s an interesting piece from ISS Analytics’ Kosmas Papadopoulos about vote requirements. Here’s the intro:

At the general meeting of Tesla Inc. on June 11, 2019, two management proposals seeking to introduce shareholder-friendly changes to the company’s governance structure failed to pass, despite both items receiving support by more than 99.5 percent of votes cast at the meeting. To get official shareholder approval, the proposals needed support by at least two-thirds of the company’s outstanding shares. However, only 52 percent of the company’s share capital was represented at the general meeting; based on turnout alone, there was no possible way for the proposal to pass.

As strange as the voting outcome at Tesla may seem, it is not a very unusual result. Every year, dozens of proposals are not considered to be “passed,” even though they receive support by an overwhelming majority of votes cast at the meeting. Supermajority vote requirements may be responsible for a large portion of these failed votes with high support levels (62 percent of instances since 2008). However, using a base of all outstanding shares for the vote requirement is an even more common corresponding factor (92 percent of instances). The increase in failed majority-supported proposals in recent years can be directly attributed to the change in the rules pertaining to the treatment of broker non-votes.

The History of Proxy Solicitation

This piece by Alliance Advisors’ Michael Mackey – published in Carl Hagberg’s “Shareholder Service Optimizer” – coincides with two of my favorite topics: history and proxy solicitation. Here’s the bottom line of the piece:

The most important takeaway for readers, as we have often noted here; this is ultimately a “people business” – where all the talent leaves the business every night – but where “the people at the top of the house” – and the people who are assigned to you own account – are the most important factors, we say, in choosing a solicitor…as the record clearly indicates if one studies the many ups and downs with care.

{kind=link}

{kind=link}

{kind=link}