July 11, 2019

Universal Proxies: Dissidents Win Board Control for First Time!

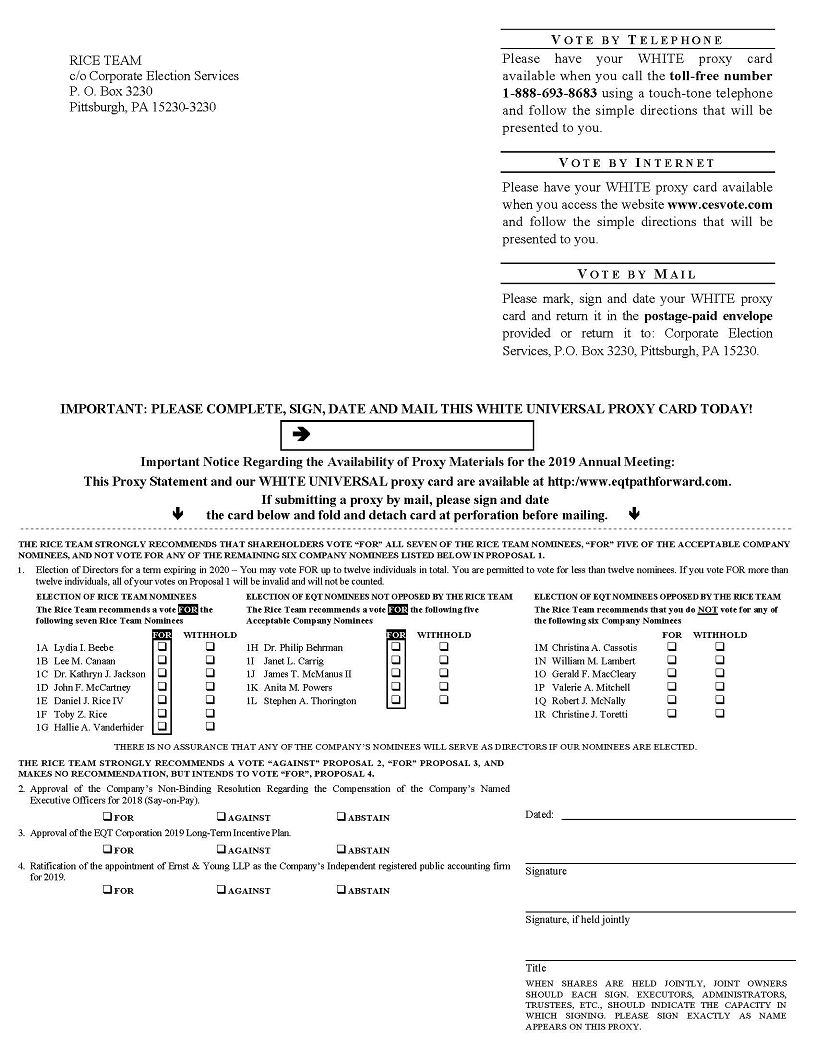

As John blogged today on the DealLawyers.com Blog, here’s big news on the universal proxy front: yesterday, at EQT Corporation’s annual meeting, a dissident group won control of the company’s board through a proxy fight waged using a universal proxy card. According to this Olshan memo, this marks the first time that such a card was successfully used in a control proxy contest in the US. Here’s an excerpt:

The universal ballot adopted by both EQT and the Rice Team named both EQT’s and the Rice Team’s nominees on their respective proxy cards. The only difference related to the presentation of the two cards, in which each side highlighted how it desired shareholders to vote. Copies of the two cards can be found here (Rice Team) and here (EQT).

As shown, the Rice Team made clear on its proxy card a recommendation for all seven of its nominees and for five of the Company’s nominees that it did not oppose, to permit shareholders to vote for all 12 available spots. Similarly, the Company recommended a vote for all 12 of its nominees and against the Rice Team’s nominees, other than existing director, Daniel Rice IV, who was nominated by both EQT and the Rice Team.

The Rice Team obtained public support from many of EQT’s largest shareholders, including T. Rowe Price Group Inc., D.E. Shaw & Co., Kensico Capital Management Corp. and Elliott Management Corp., along with proxy advisory firms Institutional Shareholder Services (“ISS”) and Egan-Jones Ratings.

The use of a universal ballot for a majority slate of directors is unprecedented and, in our view, may become more common in future proxy contests given the Rice Team’s success here. In fact, ISS noted the following in its report recommending that shareholders vote for all of the Rice Team’s nominees on that team’s universal proxy card:

“The adoption of a universal card was an inherently positive development for EQT shareholders (as it would be in any proxy contest), in that it will allow shareholders to optimize board composition by selecting candidates from both the management and dissident slates.”

{kind=link}

{kind=link}

Despite pushing for the adoption of universal proxies, some activists had recently cooled on their potential use. For instance, as we blogged last fall, Starboard Value’s CEO Jeff Smith expressed concern that in its current form, the universal ballot might tip the playing field in management’s favor. It will be interesting to see if the outcome of yesterday’s EQT vote causes people to recalibrate that assessment.

Looking at Vote Requirements

Here’s an interesting piece from ISS Analytics’ Kosmas Papadopoulos about vote requirements. Here’s the intro:

At the general meeting of Tesla Inc. on June 11, 2019, two management proposals seeking to introduce shareholder-friendly changes to the company’s governance structure failed to pass, despite both items receiving support by more than 99.5 percent of votes cast at the meeting. To get official shareholder approval, the proposals needed support by at least two-thirds of the company’s outstanding shares. However, only 52 percent of the company’s share capital was represented at the general meeting; based on turnout alone, there was no possible way for the proposal to pass.

As strange as the voting outcome at Tesla may seem, it is not a very unusual result. Every year, dozens of proposals are not considered to be “passed,” even though they receive support by an overwhelming majority of votes cast at the meeting. Supermajority vote requirements may be responsible for a large portion of these failed votes with high support levels (62 percent of instances since 2008). However, using a base of all outstanding shares for the vote requirement is an even more common corresponding factor (92 percent of instances). The increase in failed majority-supported proposals in recent years can be directly attributed to the change in the rules pertaining to the treatment of broker non-votes.

The History of Proxy Solicitation

This piece by Alliance Advisors’ Michael Mackey – published in Carl Hagberg’s “Shareholder Service Optimizer” – coincides with two of my favorite topics: history and proxy solicitation. Here’s the bottom line of the piece:

The most important takeaway for readers, as we have often noted here; this is ultimately a “people business” – where all the talent leaves the business every night – but where “the people at the top of the house” – and the people who are assigned to you own account – are the most important factors, we say, in choosing a solicitor…as the record clearly indicates if one studies the many ups and downs with care.

– Broc Romanek

Blog Preferences: Subscribe, unsubscribe, or change the frequency of email notifications for this blog.

UPDATE EMAIL PREFERENCESTry Out The Full Member Experience: Not a member of TheCorporateCounsel.net? Start a free trial to explore the benefits of membership.

START MY FREE TRIAL