In the wake of poll results indicating a strong preference to having the full menu of our offerings available straight from our home page, I have reverted the home page back to whence it came. The new large tabs at the top are the same – and the home page is “cleaner” than it used to be – but for the most part, everything is back to how it was before the redesign. Not mobile friendly – so it’s gonna hurt our Google rankings – but I listened to you. Like before, the change in the home page doesn’t impact all the other content on the site.

One member’s reaction: “I feel the same sense of triumph I felt when “old Coke” returned.” And also note that I launched a redesign yesterday of the Section16.net home page using the same concept, much larger tabs at the top and other clean-up (but no changes to the underlying content)…

DOJ Emphasizes Role of Criminal Prosecution in Addition to Regulatory Enforcement

Here’s an excerpt of this blog by Mintz Levin’s Bridget Rohde:

The U.S. Department of Justice, through the Assistant Attorney General in charge of its Criminal Division, spoke forcefully on Tuesday regarding “the role of criminal law enforcement in prosecuting conduct that may also be subject to regulatory enforcement.” Speaking at a conference at New York University, AAG Leslie R. Caldwell discussed the sometimes “critical need” for criminal prosecution even where there are civil and regulatory options, noting that individuals may receive prison sentences and companies may suffer collateral consequences that are “the only just punishment” for the conduct at issue and that serve to deter others. Recognizing that there are different kinds of breaches, she spoke of calibrating the penalty to the nature of the breach and the entity’s history and culture. AAG Caldwell also stated that DOJ’s Criminal Division, unlike other authorities, requires entities to admit their misconduct when resolving a criminal matter by a Non-Prosecution Agreement, a Deferred Prosecution Agreement, or a guilty plea. She addressed the Criminal Division’s power – and resolve – when it suspects or finds non-compliance with an NPA or a DPA.

Fraud Indicators: Signature Size Matters

This article notes how a recent study shows that CFOs with big signatures are more likely to misreport…

Ever since I dealt with this in our “Q&A Forum” a few months ago (#8333), I’ve been meaning to blog about it. This is a sleeper for those with foreign subsidiaries because it’s an action item for you with an upcoming deadline. As noted in these memos posted in our “Foreign Subsidiaries” Practice Area, the Commerce Department’s Bureau of Economic Analysis (known as the “BEA”) has a deadline of the end of May (or the end of June if you have more than 50 foreign subs) for a survey about your company’s direct investment abroad. This survey is in the form of the “Form BE-10.” The last survey was conducted five years ago – and the BEA gave guidance on this new survey in this rulemaking last November.

Note that the BEA requires all entities subject to the reporting requirements to file responses, regardless of whether they are individually contacted by the BEA. Given that the scope of this survey has been expanded to cover many industries & companies that didn’t previously report, you should evaluate whether you are now required to submit a Form BE-10, even if you haven’t in the past…

US Sentencing Commission Approves Changes to Guidelines

A few weeks ago, the US Sentencing Commission approved changes to its sentencing guidelines. As noted in this memo, the major changes are:

– Revise the definition of “intended loss” at §2B1.1, comment (n.3(A)(ii)) to mean the pecuniary harm “that the defendant purposely sought to inflict”

– Revise the victims table at §2B1.1(b)(2) to incorporate “substantial financial hardship” as a sentencing enhancement factor

– Revise the meaning of the specific offense characteristic for “sophisticated means” contained in §2B1.1(b)(10)(C) to apply to the defendant’s individual conduct, rather than the overall scheme

– Revise Application Note 3(F)(ix), which sets forth a method for calculating loss in cases involving securities fraud; the revised guidelines provide that the formula set forth in the note is no longer a rebuttable presumption in calculating loss and allows the court to use any method that is appropriate and practicable under the circumstances, including the formula

More on “Subway Marketing to the SEC Continues”

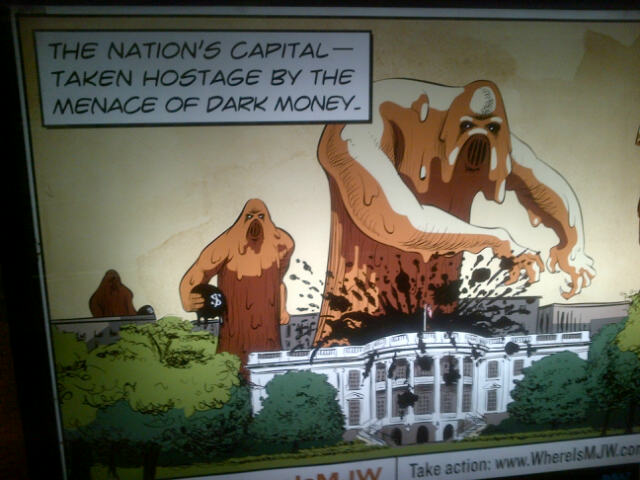

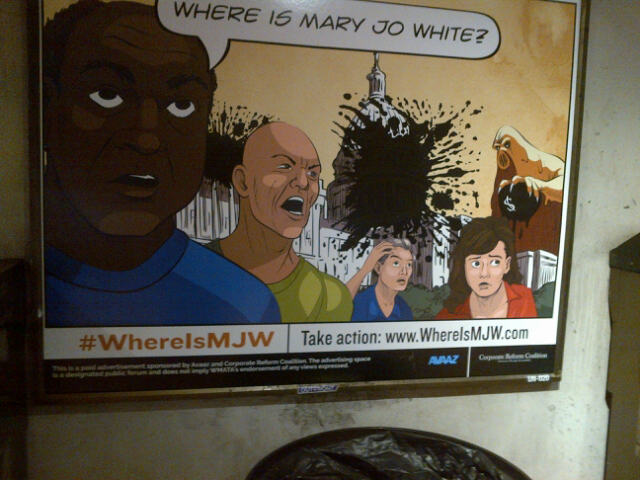

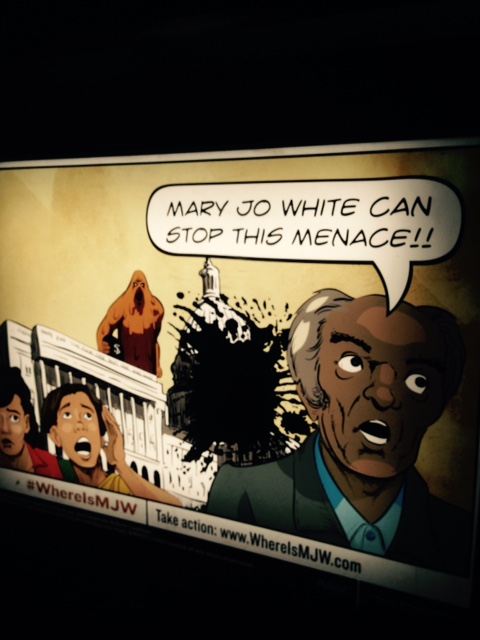

Folks were loving the pic on my blog Friday regarding the poster ads in the subway station near the SEC’s HQ – and a member sent in three more (below and at the bottom of this list):

On the heels of the news that a shareholder proposal about climate disclosure received support of over 98% at BP last week, comes the news that a group of 62 institutional investors has sent this 7-page letter to the SEC seeking better climate disclosure from oil & gas companies. The letter gets pretty specific about deficiencies in carbon asset risk disclosures. See this press release – and this Reuters article…

FINRA Pursues Reg M Enforcement Cases

This recent short-selling case demonstrates FINRA’s continued oversight of Rule 105/Regulation M practices…

California Companies Reincorporating in Nevada & Delaware

This blog by Keith Bishop describes how California continues to hemorrhage corporate charters to Delaware and Nevada. Here’s an excerpt:

The most recent potential emigrant is SJW Corp. which filed this proxy statement last week seeking shareholder approval of a reincorporation from California to Delaware. Can California and other states stanch the flow by offering licenses only to domestic corporations? Surely, there must be some constitutional bar to such a requirement – or maybe not? That question was answered last week by U.S. District Court Judge Lucy H. Koh in Nationwide Biweekly Admin., Inc. v. Owen, 2015 U.S. Dist. LEXIS 34558 (N.D. Cal. March 18, 2015).

Like last year, Verizon has put out a new “2015 Data Breach Investigations Report.” This year’s Verizon report is 69 pages, with a host of useful information as it relies on over 80,000 incidents from 70 organizations for it’s analysis. Also check out our checklists related to incident response planning, disclosure practices and risk management – as well as a chart of state laws related to security breaches.

CEO Drastically Cuts Own Pay & Raises Pay of All His Employees

Here’s the intro to this NY Times article that everyone is talking about:

The idea began percolating, said Dan Price, the founder of Gravity Payments, after he read an article on happiness. It showed that, for people who earn less than about $70,000, extra money makes a big difference in their lives.

His idea bubbled into reality on Monday afternoon, when Mr. Price surprised his 120-person staff by announcing that he planned over the next three years to raise the salary of even the lowest-paid clerk, customer service representative and salesman to a minimum of $70,000. “Is anyone else freaking out right now?” Mr. Price asked after the clapping and whooping died down into a few moments of stunned silence. “I’m kind of freaking out.”

If it’s a publicity stunt, it’s a costly one. Mr. Price, who started the Seattle-based credit-card payment processing firm in 2004 at the age of 19, said he would pay for the wage increases by cutting his own salary from nearly $1 million to $70,000 and using 75 to 80 percent of the company’s anticipated $2.2 million in profit this year. The paychecks of about 70 employees will grow, with 30 ultimately doubling their salaries, according to Ryan Pirkle, a company spokesman. The average salary at Gravity is $48,000 a year.

Subway Marketing to the SEC Continues

I’ve blogged before how some folks buy poster ads in the subway station near the SEC’s HQ (ie. Union Station) in an effort to influence the SEC. The latest poster is this one:

You should register soon for our popular conferences – “Tackling Your 2016 Compensation Disclosures: Proxy Disclosure Conference” & “Say-on-Pay Workshop: 12th Annual Executive Compensation Conference” – to be held October 27-28th in San Diego and via Live Nationwide Video Webcast. Here are the agendas – 20 panels over two days, including:

– Keith Higgins Speaks: The Latest from the SEC

– Proxy Access: Tackling the Challenges

– Disclosure Effectiveness: What Investors Really Want to See

– Pay Ratio: What Now

– Peer Group Disclosures: The In-House Perspective

– How to Improve Pay-for-Performance Disclosure

– Creating Effective Clawbacks (and Disclosures)

– Pledging & Hedging Disclosures

– The Executive Summary

– The Art of Communication

– Dave & Marty: Smashmouth

– Dealing with the Complexities of Perks

– The Big Kahuna: Your Burning Questions Answered

– The SEC All-Stars: The Bleeding Edge

– The Investors Speak

– Navigating ISS & Glass Lewis

– Hot Topics: 50 Practical Nuggets in 75 Minutes

Early Bird Rates – Act by April 24th: Huge changes are afoot for executive compensation practices with pay ratio disclosures on the horizon. We are doing our part to help you address all these changes – and avoid costly pitfalls – by offering a special early bird discount rate to help you attend these critical conferences (both of the Conferences are bundled together with a single price). So register by April 24th to take advantage of the 33% discount.

PCAOB Approves Auditing Standard Reorganization

Recently, the PCAOB approved the reorganization of its auditing standards, adopting amendments to its rules and standards to implement a topical system that integrates existing interim and PCAOB-issued auditing standards. The SEC now has to approve the reorg…

Coming in Spring 2016: Resource Extraction Rules

This recent WSJ article notes that the SEC recently noted in a court filing that it will not be considering its resource extraction rule proposal until Spring 2016.

Yesterday, just a week after oral argument, the 3rd Circuit overturned the district court in the much-awaited Trinity Wall Street v. Wal-Mart case. Here’s the news from Skadden:

The U.S. Court of Appeals for the Third Circuit issued a decision earlier today that reversed a U.S. District Court opinion and vacated a permanent injunction that would have required Wal-Mart Stores to include a controversial shareholder proposal in its 2015 annual meeting proxy statement. The court’s decision allows Wal-Mart to exclude the proposal from its proxy materials and appears to adhere to the SEC staff’s longstanding interpretation of Exchange Act Rule 14a-8(i)(7), commonly referred to as the “ordinary business exception.”

The shareholder proposal under consideration by the court requested that Wal-Mart’s board of directors amend the charter of its Compensation, Nominating and Governance Committee to provide that the committee oversee “the formulation and implementation of, and the public reporting of the formulation and implementation of, policies and standards that determine whether or not [Wal-Mart] should sell a product that: 1) especially endangers public safety and well-being; 2) has the substantial potential to impair the reputation of [Wal-Mart]; and/or 3) would reasonably be considered by many offensive to the family and community values integral to [Wal-Mart]’s promotion of its brand.” Wal-Mart excluded the proposal from its proxy materials in reliance on the written concurrence of the SEC staff with the company’s view that the proposal interfered with its ordinary business operations by impacting the products and services for sale by the company. The shareholder proponent challenged these determinations in an action in the U.S. District Court for the District of Delaware.

The opinion of the Court of Appeals has not been released yet. When it is available, the court’s views on the careful balance that the SEC and its staff have struck between the rights of shareholders under Rule 14a-8 and the authority granted to directors to manage the business and affairs of corporations under state corporate law will be closely analyzed. Members of the corporate governance community have closely monitored this legal action because of the concern that an unfavorable result could have encouraged shareholders to submit proposals that relate to ordinary business matters by framing them as requests for corporate governance reform. An expansion of Rule 14a-8 in this way would increase costs and expenses and disrupt management and board efforts to effectively manage the proxy process and corporations’ day-to-day business affairs.

BlackRock Speaks Out Against Knee-Jerk Buybacks

This DealBook column notes how BlackRock’s CEO has sent letters to the CEOs of 500 companies about buybacks and other issues. Here’s a memo from Marty Lipton on these letters…

How Audit Reports Look in Other Countries

This Fortune article by Jack Ciesielski does a nice job explaining how audit report reform has gone forward in many countries as it has stalled here in the US. Here’s an excerpt:

In January, the International Auditing and Assurance Standards Board (IAASB), an independent standard-setting body supported by the International Federation of Accountants (IFAC), issued its new standard auditor’s report to be used by adopting countries – and the new audit report bears little resemblance to the tired opinion investors see in the United States. How so?

First of all, there will be an entirely new section that will inform investors in publicly-traded companies about key audit matters – issues that the auditor judged the most significant in performing the audit of the current period financial statements. That’s probably the single most dramatic change, and one that’s sure to grab investor attention: the views of an auditor about the trickiest part of an audit. It gets back to the basic relationship between the auditor and the shareholder: The auditor is supposed to be inside party for the shareholder, and this new communication puts them in touch with each other in a big way, one that’s completely neglected these days.

The new report will also expand on ongoing matters – issue of whether or not the financial statement presentation makes sense, in view of the company’s ability to continue operating. If needed, the new information will describe the material uncertainties related to ongoing concerns going concern issues, and auditors will be called upon to state that a company is not a going concern if they disagree with management’s cheerier view. Expect to see more amplification about the auditor’s independence and ethical responsibilities, too – and the name of the engagement partner. All of this new information will appear in auditor’s reports on 2016 December year-end financial statements.

Recently, I blogged about SEC Commissioner Piwowar’s speech entitled “A Fair, Orderly, and Efficient SEC” – which included a section calling for shorter adopting releases and perhaps even breaking rulemakings into smaller parts.

I ran two surveys on that blog: one asked about reducing the amount of guidance in releases (34% voted ‘yes’ and 63% voted ‘no’) and one asked about whether the SEC should break up rulemakings into smaller, multiple pieces (53% voted ‘yes’ and 36% voted ‘no’). I’m surprised that even 34% want less guidance because then we wind up with guidance at the Staff level, which some Commissioners ironically have griped about over the years.

Here’s feedback that I received from a member that pretty much sums up my feelings on the subject:

I don’t think breaking rulemakings into smaller parts is realistic. Having done a stint in Corp Fin’s Office of Rulemaking, I know that there is a lot that of administrative stuff that has to go into each separate rulemaking. It just doesn’t seem practical to increase the volume of separate rulemakings given the environment and how that process works these days. Breaking things into smaller parts would just result in less rules getting adopted

As far as length, I agree that they are probably too long – but a lot of that is the back-end, driven by the cost-benefit analysis and what’s going on in the courts. I think they could actually give some more interpretative advice. A lot of times, there is a lot of words and background – but not a whole lot of really useful interpretation. Examples of the application of new rules could be very useful in certain circumstances. Whenever there is something like that in a rulemaking, it is pretty helpful and avoids the need for Staff level interpretations. I was just reading the Regulation M release from the 1990s yesterday for this purpose! In an ideal world, maybe the rules could be so clear that interpretation wouldn’t be needed – but I don’t see us getting there anytime soon. So I would think that a Commissioner might prefer to have Commission-level clarifications out there rather than needing the Staff to do it.

Supreme Court Holds that Agencies Can Amend or Repeal Interpretive Rules Without Notice-and-Comment Procedures

The U.S. Supreme Court recently held that agencies are not required to follow notice-and-comment rulemaking procedures when amending or repealing their interpretations of existing regulations. The Court ruled that the D.C. Circuit’s longstanding Paralyzed Veterans doctrine, which required agencies to follow notice-and-comment procedures when changing interpretive rules, was contrary to the text of the Administrative Procedure Act and exceeded the scope of judicial review authorized by Congress. The Court suggested, however, that changed interpretations should be subject to more searching review by courts, especially when regulated entities have extensively relied on the prior interpretation, and may face limitations in retroactive application. Three Justices wrote separately to question the fundamental appropriateness of judicial deference to agencies’ interpretations of their own regulations. Though the Court directed that an agency will need to provide a more substantial justification for its new interpretation if the new interpretation has engendered serious reliance interests or if it is based on factual findings contrary to prior findings, yesterday’s decision may make it easier for an agency to modify or even reverse its interpretation of existing regulations.

By the way, you might want to read Keith Bishop’s blog entitled “Did The SEC Violate The Administrative Procedure Act?”

Should Law Firms Go Public?

This DealBook column raises a topic that I blogged about a while back. The column summarizes the arguments supporting the idea made in this article. Law firm IPOs! I don’t have an opinion one way or another (although the notion of shareholders pressuring law firms – who are supposed to be advocates for their clients – seems like a big hurdle), but I would love to see what type of names would be drummed up by the new law firm corporations! I imagine using nomenclature consisting of last names would go the way of the Dodo…

On an ongoing basis, the International Monetary Fund undertakes assessments of the financial regulatory arrangements of countries around the world, which is called the “Financial Sector Assessment Program.” A few weeks ago, the IMF published its FSAP review of the United States, covering banking, insurance and securities. As part of this process, the various regulatory agencies prepare a self-assessment of how they think their agency stacks up against international standards. Here’s the SEC Staff’s self-assessment. It is a remarkable document – 700 pages of the Staff describing its various programs. Principle 16 regarding eliciting disclosure starts on page 244.

Insider Trading: Second Circuit Declines to Review Newman Insider Trading Decision

A few weeks ago, the US Court of Appeals for the Second Circuit denied Preet Bharara’s request that the court reconsider United States v. Newman. By declining to reconsider Newman, the Second Circuit left in place a sharply narrowed definition of insider trading that limits the government’s ability to prosecute insider trading cases (at least in the Second Circuit). The government must now decide whether to appeal to the Supreme Court and/or rely on Congress to adopt legislation providing a statutory definition of illegal insider trading for the first time. As noted in this DealBook column, this is even more notable given that it’s Judge Rakoff that sided with the SEC.

First, the knowledge element could make things very difficult for the SEC and the Justice Department in remote tippee cases. The defendants in Newman, for example, were far removed from the original sources of the information. As the court put it:

“[T]he Government presented absolutely no testimony or any other evidence that Newman and Chiasson knew that they were trading on information obtained from insiders, or that those insiders received any benefit in exchange for such disclosures, or even that Newman and Chiasson consciously avoided learning of these facts.”

One of the things that enterprising inside traders might do as a result is to create some distance between the sources of material, nonpublic information and those who ultimately trade on that information. A person or two in between could mean that the actual traders never know the personal benefit, if any, that accrues to the original tipper. Structuring insider trading chains in this way could become part of the general business model. I mean, this is what people do. The court does seem to allow for liability, as it probably must, if defendants “consciously avoid[] learning of these facts.” But one thing about conscious avoidance – it can be pretty hard to prove! Not impossible, but hard.

Leveraged Loans: Looks Like Securities But Not Regulated?

This Bloomberg article entitled “Loans Look Like Securities Yet Escape Oversight From SEC” is worth reading. Here’s an excerpt:

Leveraged loans look and trade like securities — yet the regulator in charge of overseeing securities doesn’t consider them as such. These loans, usually made to companies with high debt and speculative-grade credit ratings, are made for commercial or consumer — not investment — purposes, according to lawyers and bankers who argue they are not securities. At the same time, the $800 billion leveraged-loan market has become an increasingly popular asset class for pension and mutual funds to invest in. About a third of new loans last year were bought by mutual funds, up from 15 percent in 2012, according to Loan Syndications & Trading Association data.

“If they are syndicating this to investors and indicating there is going to be some liquidity in a secondary market, those are the red flags that make it look very much like a security,” said Thomas Lee Hazen, an expert in securities law at the University of North Carolina School of Law. The U.S. Securities and Exchange Commission’s authority in this market is limited to loans that meet the legal definition of a security, which requires a case-by-case review, according to John Nester, an SEC spokesman.

Here’s an excerpt from this blog by Cooley’s Cydney Posner:

The Corporation Law Section of the Delaware Bar has approved, substantially as proposed, the amendments to the Delaware General Corporation Law proposed by the Delaware Bar’s Corporation Law Council regarding fee-shifting and forum selection provisions in Delaware governing documents. (See this post.) Accordingly, it is anticipated that the proposals would be introduced for consideration by the Delaware General Assembly.

More specifically, the proposed amendments would invalidate, in Delaware charters and bylaws, fee-shifting provisions in connection with internal corporate claims. “Internal corporate claims” are claims, including derivative claims, that are based on a violation of a duty by a current or former director or officer or stockholder in such capacity or as to which the corporation law confers jurisdiction on the Court of Chancery. These claims would include claims arising under the DGCL and claims of breach of fiduciary duty by current or former directors or officers or controlling stockholders of the corporation, or persons who aid and abet those breaches. However, as discussed in this post, federal securities class actions would not be included. The proposed amendments also expressly authorize the adoption of exclusive forum provisions for internal corporate claims, as long as the exclusive forum is in Delaware. Although the proposed amendment does not address the validity of a provision that selects, as an additional forum, a forum other than Delaware, the synopsis indicates that it would invalidate “a forum selection provision selecting the courts in a different State, or an arbitral forum, if it would preclude litigating such claims in the Delaware courts.” Accordingly, the legislation would not allow Delaware corporations to select another state as the exclusive forum.

While not exactly topics roiling the Delaware Bar, a few other matters are addressed in the proposed legislation. For example, with regard to public benefit corporations (see these news briefs and these posts), the proposed amendments would reduce the voting requirement for a corporation to become a public benefit corporation from 90% of the outstanding shares to 2/3 of the outstanding shares (still a rather high hurdle, especially if the company is already public) and provides a market out (applicable to listed companies and companies with over 2,000 record holders) to the provisions allowing appraisal for stockholders that did not vote in favor of the transaction.

Other proposed amendments relate to issuance of stock and options. These proposed amendments clarify that the board may authorize stock to be issued in “at the market” programs without having to separately authorize each individual stock issuance and that the amount of consideration to be received for stock or options may be determined by a formula that references or depends on the operation of extrinsic facts, such as market prices or averages of market prices on one or more dates.

The proposed amendments would also clarify a number of issues in connection with the new Delaware statutes, Sections 204 and 205, that authorize ratification of defective corporate acts by the corporation and the Delaware courts, respectively. Among other things, these amendments would address the situation in which the initial board was not named in the original certificate or properly appointed, allow listed companies to provide certain notices by making public filings, clarify the requirements for certificates of validation, clarify the term “validation effective time” (including allowing the board to designate a future time in some circumstances), clarify that the board may adopt a single set of resolutions ratifying multiple defective corporate acts, and clarify that holders of shares of putative stock would not be considered stockholders entitled to vote or to be counted for purposes of a quorum in any ratification vote and that the only stockholders entitled to vote on ratification are the holders of record of valid stock as of the record date (i.e., ratification of a defective corporate act will not result in putative shares being retroactively validated so that they become entitled to vote).

Meanwhile, the “Delaware Rapid Arbitration Act” has been enacted – see this memo…

Revenue Recognition: FASB Tentatively Decides to Delay New Rules for One Year

Last week, the FASB tentatively decided to defer the effective date of its new standard on revenue recognition for one year. The FASB’s tentative decision will be published for public comment before the Board makes a final decision(see the memos in our “Revenue Recognition” Practice Area).

Webcast: “Proxy Access: The Halftime Show”

We have posted the transcript for our recent webcast: “Proxy Access: The Halftime Show.” Also see the blog I just posted on “The Proxy Blog” running down the stats of how 64 of the companies that received proxy access proposals handled them…

Last week, the SEC brought this enforcement action against Polycom’s former CEO (who was fired in 2013). The company was charged with inadequate proxy disclosure from 2010 to 2013 and improper internal controls. The SEC complaint is filled with striking details (if true) of how the CEO at Polycom created false expense reports so the company would pay for his personal expenses, such as this example:

On July 7, 2012, Miller directed his administrative assistant to buy him two tickets to an August 3, 2012 performance of the Broadway musical Jersey Boys in New York City. On July 24, 2012, Miller emailed his administrative assistant to ask if she had the tickets, and during that exchange he represented, “I am giving the JB tickets as a prize in a NYC PLCM office sales contest…. On PCARD place NYC PLCM Q3 Sales Incentive Contest[.]” At Miller’s direction, his assistant charged $576.20 to her P-Card for two tickets to the show, and submitted the expense for reimbursement with the description that Miller had provided. But Miller’s description of the expense was false, as he again used the tickets to attend the theatre with his girlfriend, and did not give them away to Polycom’s New York sales team or anyone else. Indeed, Miller’s August 3, 2012 night out with his girlfriend in New York cost Polycom more than $1,000. In addition to the tickets, Miller charged more than $275 to his Polycom credit card for post-theatre dinner and later, although he had eaten alone with his girlfriend, emailed his administrative assistant a bogus business description for the meal, including the names of purported attendees from a Polycom customer. Miller also directed his administrative assistant to book a limousine service to take him to the theatre and dinner, for which she charged more than $160 on her P-Card, at his direction, and obtained reimbursement from Polycom.

There are plenty of other examples to pique anyone’s interest. It’s another sad tale of what would seem to be, entitlement and fraud.

The SEC also penalized Polycom $750,000 and issued a cease and desist. The company’s proxy statement said: “No Excessive Perquisites” (emphasis in original) and explaining that “[a] small amount of perquisites are provided to our executives, consistent with the practices of our peer companies.” False and misleading statements, books and records violations, internal accounting controls failure, etc.

And in the complaint, the SEC stated: “Polycom employees discovered that Miller had expensed more than $800 worth of spa gift cards as purported gifts to Polycom employees, but that Miller had actually used the gift cards, at least in part, for himself. In response, Polycom’s CFO raised the issue directly with Miller and suggested a system for further review of Miller’s expense reports to avoid problems in the future. Miller reacted angrily at being second-guessed. On June 26, 2011, the CFO sent Miller an email emphasizing the importance of Miller’s and the company’s disclosure obligations, including a detailed description of the relationship between Miller’s expenses, rules requiring that Polycom disclose all perks he received, and the company’s proxy statements. Notwithstanding the clear instructions provided in Polycom’s annual financial reporting questionnaires, which Miller signed, and the CFO’s personal explanation in June 2011, Miller continued to charge and hide personal expenses from Polycom.”

CII’s New Policy: Automatic Accelerated Vesting of Unearned Equity

Last week, the Council of Institutional Investors approved a policy opposing automatic accelerated vesting of unearned equity in the event of a merger or other change-in-control. The recommended best-practice policy states that boards should have discretion to permit full, partial or no accelerated vesting of equity awards not yet awarded, paid or vested.

Transcript: “The Top Compensation Consultants Speak”

We have posted the transcript for the recent CompensationStandards.com webcast: “The Top Compensation Consultants Speak.”

{kind=link}