Given the times in which we live, I guess it’s not surprising that some companies have added “risk factor” disclosure about the potential implications of an active shooter to their SEC filings. Here’s an excerpt from this WSJ article:

A handful of public companies have begun quietly warning investors about how gun violence could affect their financial performance. Companies such as Dave & Buster’s Entertainment Inc., Del Taco Restaurants Inc. and Stratus Properties Inc., a Texas-based real-estate firm, added references to active-shooter scenarios in the “risk factor” section of their latest annual reports, according to an analysis of Securities and Exchange Commission filings. The Cheesecake Factory Inc. has included it in its past four annual reports.

So, what do these risk factors look like? Here’s what The Cheesecake Factory said in its 2019 10-K (pg. 25):

Any act of violence at or threatened against our restaurants or the centers in which they are located, including active shooter situations and terrorist activities, may result in restricted access to our restaurants and/or restaurant closures in the short-term and, in the long-term, may cause our customers and staff to avoid our restaurants. Any such situation could adversely impact customer traffic and make it more difficult to fully staff our restaurants, which could materially adversely affect our financial performance.

Dave & Buster’s 10-K included identical language (pg. 23). The language in Del Taco’s 10-K (pg. 21), and Stratus’s 10-K (pg. 17) was a little different. While I understand why companies are doing this, I’m not sure this kind of thing is what risk factor disclosure is intended to capture. Our tendency (mine too) to throw any item that’s been added to our national anxiety closet into a risk factor isn’t very helpful to investors. The problem is that not all disclosure adds value – some just creates “noise.”

In the U.S., we’ve learned that an active shooter is the kind of random event could happen to anyone, and the effect of such an event on any business would be terrible. So to me, it’s sort of like getting struck by a killer asteroid. I think this is the kind of thing that Judge Easterbrook was getting at in this excerpt from his 1988 opinion in Weilgos v. Commonwealth Edison:

Issuers need not “disclose” Murphy’s Law or the Peter Principle, even though these have substantial effects on business. . . Securities laws require issuers to disclose firm-specific information; investors and analysts combine that information with knowledge about the competition, regulatory conditions, and the economy as a whole to produce a value for stock.

But let’s face it – you’re not going to change your approach here and neither am I. That’s because while we can debate risk factor metaphysics, the reality is that the explosive growth in event-driven securities class actions is a big part of our personal anxiety closets too.

Venture Capital: Snoop’s Got His Mind on His Money & His Money on His Mind

My kids think I’m dorkier than Ari Melber when I reference hip-hop. But there’s no way I’m not going to use a “Gin & Juice” reference in the title when this Pitchbook article says that Snoop Dogg is an investor in Swedish payment services provider Klarna, which is now Europe’s second most valuable VC-backed company with a $5.5 billion valuation following its recent $460 million capital raise. Here’s an excerpt:

Founded in 2005, Klarna provides consumer financing for purchases at third-party merchants. Rather than requiring consumers to pay in full via credit card at the time of sale, Klarna acts as a middleman to front the payment for a purchase, with merchants receiving the full amount upfront while the consumer repays Klarna over time.

The Swedish company is perhaps most recognizable for its partnership and investment relationship with Calvin Broadus, better known as Snoop Dogg. Broadus is front-and-center in Klarna’s recent marketing campaign, known as “Smoooth Dogg.” Such marketing efforts could prove beneficial as Klarna plans to use its new windfall to significantly expand in the US, Broadus’ home country and where his career grew rapidly in the 1990s.

Regular readers of this blog know that Snoop has some impressive culinary skills, but you also should note that this isn’t his first rodeo when it comes to venture capital. He’s an investor in both Reddit & the trading app Robinhood, and a general partner in Casa Verde Capital, which recently completed a $45 million capital raise & focuses on investments in – here’s a shock – the cannabis industry.

Cryptocurrencies: Kik Claps Back at SEC Complaint

In June, I blogged about the SEC’s decision to bring an enforcement action against Kik Interactive for its $100 million unregistered token deal. As that blog noted, Kik’s founders are crypto-evangelists who have raised a $5 million war chest to fund its defense against the SEC’s allegation that its tokens are “securities.” It recently filed a 130-page answer to the SEC’s complaint, in which it accuses the agency of “twisting the facts” about its Kin token. Check out this TechCrunch article for more details.

It’s not news to anyone reading this that the legal profession has big problems with depression, substance abuse, and other mental health issues. If you haven’t personally experienced any of these, you know friends or colleagues who have. But the question is, why are these problems so prevalent among lawyers?

This Law.com article is stirring up some controversy over its claims that when it comes to outside counsel, the problem is the client. Specifically, the article singles out law department attorneys as playing a big role in mental health issues among outside counsel. Here’s the gist of the argument:

Client demands for fast turnaround times, even on non-urgent matters, can leave outside counsel in constant crisis mode. That stress can lead to frayed relationships and mental health issues such as depression, addiction and anxiety, which firm lawyers are more likely to experience than corporate in-house counsel.

“We’re on this crisis level all the time because of the expectations coming from the clients,” said Dan Lukasik, the founder of Lawyers With Depression. He said “a change in the relationship” between firms and in-house clients is needed to improve law’s mental health culture.

Client demands are part of the stress equation, but so is the law firm environment, and I don’t think it’s at all fair to point the finger at in-house lawyers. If in-house attorneys set unreasonable expectations, it’s usually because their business people have set unreasonable expectations for them. In my experience, many in-house lawyers go out of their way to let you know if something they’re asking for isn’t urgent, and it’s exceedingly rare to find one who puts you through the ringer just for giggles.

I agree that most corporate lawyers operate “on a crisis level” all the time, but I think that has more to do with how we’re wired than it does with client demands or whether we’re in a law firm or a corporate setting. For instance, even if I know something’s not a crisis, I’ll often just assume the client needs me to attend to it immediately. That’s nuts, but I don’t think I’m alone. A lot of us are introverted, competitive, perfectionist, obsessive about our reputations & terrified of failure. Add in our professional bias toward catastrophic thinking, and you’ve got a bunch of gasoline-soaked rags just waiting for somebody to light a match when it comes to mental health problems.

Quick Poll: Why Do Lawyers Experience Mental Health Issues?

I just gave you my 2 cents about why I think so many of us struggle with mental health issues – check out this ABA Journal article for what other lawyers have to say about this topic. Here’s an anonymous poll so you can provide your thoughts:

survey tool

Transcript: “Joint Ventures – Practice Pointers”

We have posted the transcript for the recent DealLawyers.com webcast: “Joint Ventures – Practice Pointers.” We’ll have our second installment for this topic in an August 6th webcast: “Joint Ventures – Practice Pointers (Part II).”

There’s a great quote from the 5th Circuit’s 1981 decision in Huddleston v. Herman & MacLean that says that “to warn that the untoward may occur when the event is contingent is prudent; to caution that it is only possible for the unfavorable events to happen when they have already occurred is deceit.” That quote pretty much sums up the basis for the SEC’s enforcement proceeding against Facebook that was announced yesterday. Here’s an excerpt from the SEC’s press release:

The Securities and Exchange Commission today announced charges against Facebook Inc. for making misleading disclosures regarding the risk of misuse of Facebook user data. For more than two years, Facebook’s public disclosures presented the risk of misuse of user data as merely hypothetical when Facebook knew that a third-party developer had actually misused Facebook user data. Public companies must identify and consider the material risks to their business and have procedures designed to make disclosures that are accurate in all material respects, including not continuing to describe a risk as hypothetical when it has in fact happened.

The misleading disclosures arose out of Cambridge Analytica’s unauthorized use of Facebook user data. Facebook allegedly found out about Cambridge Analytica’s antics in 2015, but didn’t revise its disclosure until two years later. Facebook consented to a “neither admit nor deny” settlement that, among other things, enjoins it from future violations of Section 17(a)(2) and (3) of the Securities Act and Section 13(a) of the Exchange Act & various rules thereunder.

The company also agreed to pay $100 million to settle the charges, which sounds like a lot, but is chump change to Facebook. After all, the company also agreed yesterday to pay a $5 billion fine to settle FTC charges arising out of customer data privacy lapses. Still, it seems to me that the real elephant in the room may not be the size of the settlement, but the fact that no individuals were named.

The SEC almost always names individuals in corporate disclosure cases, although it didn’t do so in last year’s high-profile data privacy case against Altaba (Yahoo!). In any event, there’s nothing in the press release to suggest that actions against any individuals are contemplated – despite language in the complaint to the effect that “more than 30 Facebook employees in different corporate groups including senior managers in Facebook’s communications, legal, operations, policy, and privacy groups” were aware that Cambridge Analytica had improperly been provided with user data.

The FTC Gives Facebook a New Board Committee!

Speaking of that FTC settlement, Bloomberg’s Matt Levine points out in his column that it has imposed some interesting governance obligations on Facebook that may curb some of Mark Zuckerberg’s power. One of the conditions imposed under the terms of the settlement is a new board privacy committee that is intended to be difficult for Zuckerberg to mess with. Here’s an excerpt from the FTC’s statement on the settlement:

The order creates greater accountability at the board of directors level. It establishes an independent privacy committee of Facebook’s board of directors, removing unfettered control by Facebook’s CEO Mark Zuckerberg over decisions affecting user privacy. Members of the privacy committee must be independent and will be appointed by an independent nominating committee. Members can only be fired by a supermajority of the Facebook board of directors.

Here’s Matt’s take on the independent privacy committee requirement:

The upshot is … look, it is not entirely clear to me what the upshot is; we’ll see what happens. But my rough analysis is that if Zuckerberg wanted to do a bad privacy thing, and the independent privacy directors told him not to, he’d have a tough time of doing it. He couldn’t remove the independent privacy directors from their posts.

Perhaps he could remove them from the board, but he’d have a hard time replacing them, because the independent nominating committee has “the sole authority” to pick new directors. I suppose he could replace the nominating committee too. These provisions aren’t ironclad. But surely their purpose really is to take the final authority over one aspect of Facebook out of the hands of Zuckerberg.

BlackRock: “Move Along – Nothing to See Here. . .”

According to this recent Harvard Governance Blog from its Vice Chair, BlackRock would like you to know that it & the rest of the Big 3 are really small players in the grand scheme of things:

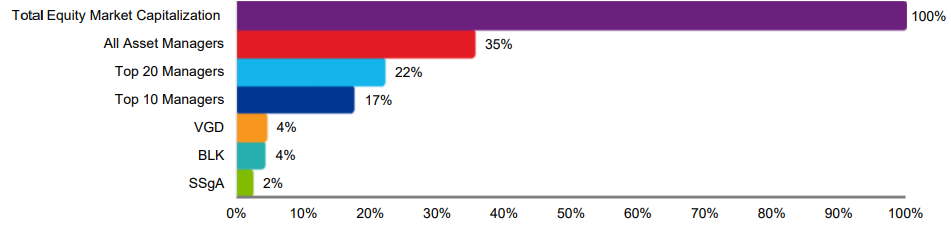

As index funds are currently growing more quickly than actively managed funds, some critics have expressed concern about increasing concentration of public company ownership in the hands of index fund managers. While it is true that assets under management (or “AUM”) in index portfolios have grown, index funds and ETFs represent less than 10% of global equity assets. Further, equity investors, and hence public company shareholders, are dispersed across a diverse range of asset owners and asset managers.

As of year-end 2017, Vanguard, BlackRock, and State Street manage $3.5 trillion, $3.3 trillion, and $1.8 trillion in global equity assets, respectively. These investors represent a minority position in the $83 trillion global equity market. As shown in Exhibit 1, the combined AUM of these three managers represents just over 10% of global equity assets.

Umm, gee – isn’t 10% of all the equity assets in the world kind of a lot? I don’t know why we’re supposed to take a lot of comfort from that number – particularly since the Big 3 reportedly control 25% of the stock in the S&P 500 and are on course to increase that stake to more than 40% over the next two decades. These numbers aren’t small.

The blog also says that those AUM numbers are misleading, because they represent “a variety of investment strategies, each with different investment objectives, constraints, and time horizons. For example, BlackRock has more than 50 equity portfolio management teams managing nearly 2,000 equity portfolios.” That’s great – but when Larry Fink comes out with annual letters telling boards of portfolio companies “how things are gonna be,” those 2,000 equity portfolios look pretty monolithic.

By the way, if this “50 portfolio managers/2,000 portfolios” pitch sounds familiar to you, it may be because at some point you heard the same pitch from one of the Big 3 when it was lobbying your client to allow it to go over a poison pill threshold. At least that’s where I first heard it.

It looks like a token issuer finally crossed the public offering goal line – at least when it comes to clearing Corp Fin’s review process. This Morrison & Foerster memo has the details. Here’s an excerpt:

On July 10, 2019, Blockstack Token LLC (“Blockstack”), a wholly-owned subsidiary of Blockstack PBC, a Delaware public benefit corporation, became the first company to have an offering of digital assets qualified by the U.S. Securities and Exchange Commission (“SEC”) under Regulation A.

Blockstack is a technology company that offers an open-source blockchain-enabled network for developers to build and publish their own decentralized applications. According to Blockstack’s website, over 165 applications have been built on the Blockstack platform. Purchasers of Blockstack’s tokens (“Stacks Tokens”) will be able to use the tokens on its platform.

Token offerings have been under increasing scrutiny, especially with respect to whether or not tokens are securities. In its offering circular disclosure, Blockstack acknowledges that the Stacks Tokens are characterized as investment contracts under the Howey test, while noting that the Stacks Tokens “will not have the rights traditionally associated with holders of debt instruments, nor…equity.” The disclosure, in its discussion about the nature of Blockstack’s decentralized network, also references the SEC’s recent guidance on evaluating whether digital assets constitute securities for purposes of the Securities Act of 1933.

Although there have been a boatload of Reg D token offerings, this is the first one that’s cleared SEC review. Here’s a copy of the company’s preliminary offering circular. As to how long the process took, the answer is about 3 months.

It appears that the initial Form 1-A filing was made on April 11, 2019. At least one substantive amendment to the filing was made in May, but the filing history is a little convoluted, because the deal originally involved a subsidiary entity & was converted to an offering by the parent company shortly before the SEC issued its qualification order. The subsidiary ultimately withdrew its filing, but the back & forth between two filers makes it difficult to determine how much of the time between filing and qualification was attributable to the Staff’s review process.

Registered ICOs: And Then There Were Two!

Blockstack may have been the first ICO to clear SEC review, but this Proskauer blog says that it had company just a day later:

The SEC also qualified the Regulation A offering circular of YouNow, Inc. (“YouNow”), for up to $50 million worth of Props Tokens (“Props”). Rather than solicit cash (or cryptocurrency) consideration for the sale of Props, YouNow and its affiliate, The Props Foundation Public Benefit Corporation, will use YouNow’s Regulation A program solely to distribute Props as rewards and grants to users, developers and other contributors within YouNow’s network of consumer-facing digital media applications.

Meanwhile, back in unregistered token deal land. . .

Blue Sky: New Jersey Sues Issuer of Unregistered Tokens

The SEC’s high-profile enforcement actions involving digital assets get most of the limelight, but as we’ve previously blogged, state securities regulators have been extremely active on the enforcement front when it comes to token deals. Last week, it was New Jersey’s turn to bring the hammer down. Here’s an excerpt from this “Modern Consensus” article describing the Garden State’s recent action:

New Jersey got in on the cryptocurrency offering enforcement action on July 18, suing blockchain-based online rental marketplace Pocketinns for an unregistered sale of securities last year. The state’s attorney general, Gurbir Grewal, was joined by the New Jersey Bureau of Securities today in announcing a three-count enforcement action against Princeton-based Pocketinns and its president, Sarvajnya Mada, over the January 15-31, 2018, sale of $410,000 in PINNS Tokens in an initial token offering.

The U.S. Securities and Exchange Commission (SEC) has brought several similar suits, initiating a high-profile action against blockchain instant messaging service Kik in June for its $100 million ICO in 2017. The agency released a long-awaited “plain English” guide defining when an ICO is a security in April.

Aside from violating the Garden State’s Uniform Securities Law by failing to register the offering, Grewal alleged that Mada acted as an unregistered agent and Pocketinns employed an unregistered agent during the sale.

The article says that the Pocketinns deal wasn’t very successful – it raised less than 1% of the $46 million it sought. But on the other hand, the company appears to have been extremely successful in buying itself all sorts of trouble.

Last week, Liz blogged about a recent rulemaking petition filed by a coalition of labor & progressive groups requesting the SEC to repeal & replace the Rule 10b-18 “safe harbor” under which most buybacks have been conducted.

The request to “repeal” 10b-18 is pretty straightforward, but what’s the “replace” part of the equation supposed to look like? The petitioners suggest that the SEC look at some 1970s-era proposals to limit buybacks, and point out that those proposals included:

– Limiting repurchases to 15 percent of the average daily trading volume for that security.

– Creating a narrower safe harbor and allowing repurchases that fall outside this safe harbor to be reviewed and approved on an individualized, case-by-case basis.

– Providing that repurchases inconsistent with the safe harbor are expressly “unlawful as fraudulent, deceptive, or manipulative.”

– Requiring various disclosures, including whether any officer or director is purchasing or disposing of the issuer’s securities, the source of funds to be used to effect the repurchases, the impact of the repurchases on the value of the remaining outstanding securities, and specific disclosures for large repurchases.

Companies continue to repurchase “massive amounts” of their own stock, and the market seems to be addicted to buybacks as well. So far, the SEC hasn’t seemed inclined to do much to further regulate buybacks, and tinkering with 10b-18 seems unlikely. But a presidential election’s looming, buybacks are getting clobbered in the media, & Democratic presidential hopefuls have them in the cross-hairs. When you throw into the mix the recent introduction of legislation that would ban open market buybacks, the SEC may at some point be faced with a situation where if it doesn’t act, Congress might.

ISS Policy Survey: Board Gender Diversity, Over-Boarding & More

Yesterday, ISS opened its “Annual Policy Survey.” In recent years, ISS used a 2-part survey, with a relatively high-level “governance principles survey” accompanied by a more granular “policy application survey.” This year, ISS is using a single survey with a more limited number of questions. ISS may have streamlined the process, but this excerpt addressing the topics covered in the survey shows that they’ve still covered quite a bit of ground:

Topics this year cover a broad range of issues, including: board gender diversity, director over-boarding, and director accountability relating to climate change risk, globally; combined chairman and CEO posts and the sun-setting of multi-class capital structures in the U.S.; the discharge of directors and board responsiveness to low support for remuneration proposals in Europe; and the use of Economic Value Added (EVA) in ISS’ quantitative pay-for-performance, financial-performance-analysis secondary screen for companies in the U.S. and Canada.

As always, this is the first step for ISS as it formulates its 2020 voting policies. In addition to the survey, ISS will gather input via regionally-based, topic-specific roundtables & calls. Interested market participants will also have an opportunity to comment on the final proposed changes to the policies.

SEC “Short- v. Long-Term” Roundtable: So What Happened?

Last week, the SEC hosted its roundtable on short-term v. long-term management of public companies. As Broc blogged when the roundtable was announced, the roundtable follows the SEC’s December 2018 request for comment on earnings releases & quarterly reporting. If you’re looking for a fairly detailed review of the discussion at the roundtable, check out this recent blog by Cooley’s Cydney Posner.

Following the lead of other federal law enforcement agencies, the SEC is looking to increase its capabilities when it comes to monitoring social media platforms. Here’s an excerpt from this GCN article:

The Securities and Exchange Commission also issued a sources sought notice for a commercial, off-the-shelf social media monitoring subscription to help it track emerging risk areas and activities of market participants to identify potential securities law violations.

Less interested in Twitter than the FBI, the SEC wants the ability to monitor Facebook, Instagram, YouTube, LinkedIn, and Reddit as well as public forums, blogs and message boards. It also requests sentiment analysis capabilities and the ability to identify bot accounts and fake user accounts. Data should be available through an application programming interface as well as through a browser.

I don’t know if anybody in SEC procurement is reading this, but I’ve got an idea that will save the taxpayers a lot of money. If you’re interested in “sentiment analysis capabilities,” don’t bother buying some crappy software license – just click on any random “Me on Facebook v. Me on Twitter” meme. It will tell you everything you need to know. You can Venmo me my reward money along with the thanks of a grateful nation.

Tomorrow’s Webcast: “Company Buybacks – Best Practices”

Tune in tomorrow for the webcast – “Company Buybacks: Best Practices” – to hear Skadden’s Josh LaGrange, Hunton Andrews Kurth’s Scott Kimpel, Simpson Thacher’s Lee Meyerson and Foley & Lardner’s Pat Quick provide practical guidance about how to conduct a stock repurchase program, including analysis of whether it’s the best use of funds.

FOIA Exemption 4 protects “trade secrets and commercial or financial information obtained from a person [that is] privileged or confidential.” However, most federal circuit courts have read in a “substantial competitive harm” test under which commercial information would be regarded as “confidential” only if its disclosure was likely to cause substantial harm to the competitive position of the person from whom it was obtained.

The substantial competitive harm requirement had its genesis in the D.C. Circuit’s 1974 decision in National Parks & Conservation Association v. Morton, and the standard had been widely adopted by other courts. But earlier this week, by a 6-3 vote, the SCOTUS invalidated the requirement in Food Marketing Institute v. Argus Leader Media. Here’s an excerpt from this Cleary Gottlieb memo that addresses the Court’s reasoning:

Notwithstanding that the lower courts have followed National Parks in one form or another for 45 years, the Supreme Court roundly rejected it. Writing for six members of the Court, Justice Gorsuch criticized the D.C. Circuit’s creation of the “substantial competitive harms test” based on its interpretation of legislative history as demonstrating a “casual disregard of the rules of statutory interpretation.”

Food Marketing Institute held that a court must begin its analysis of statutory terms by referencing the ordinary meaning and structure of the law itself, and when this leads to a clear answer, the court must not go further. The Court found that because there is “clear statutory language” in FOIA, legislative history should never have been allowed to “muddy the meaning” of this language.

The decision should substantially reduce the burden associated protecting confidential information submitted to the government, but the memo says that it also raises questions about how agencies and courts will apply existing regulations that incorporate the “substantial competitive harm” test, and whether they will need to revise such regulations or attempt to justify disclosure decisions on other grounds.

What Does the SCOTUS’s Decision Mean for CTRs?

The SEC is one of the agencies that will need to sort out how the SCOTUS’s decision to eliminate the “substantial competitive harm” standard impacts existing rules. In that regard, here are some insights that Bass Berry’s Jay Knight shared with us on how the Court’s decision complicates the SEC’s recently simplified CTR process:

As everyone may recall, in March the SEC adopted amendments to disclosure requirements for reporting companies, as mandated by the 2015 Fixing America’s Surface Transportation Act (the “FAST Act”). Among the amendments was a simpler CTR process, which now allows registrants to omit immaterial confidential information from acquisition agreements filed pursuant to Item 601(b)(2) of Regulation S-K and material contracts filed pursuant to Item 601(b)(10) of Regulation S-K without having to file a concurrent confidential treatment request. In short, registrants are permitted to redact provisions in such exhibit filings “if those provisions are both not material and would likely cause competitive harm to the registrant if publicly disclosed.” (emphasis added)

In the SEC’s adopting release, the SEC notes that it slightly revised the language of the amendment in the final rule to refer to information that “would likely cause competitive harm” to “more closely track the standard under FOIA.” (see page 25 of the adopting release) With the Supreme Court holding that FOIA exemption 4 does not have a competitive harm condition, it calls into question whether the “competitive harm” standard in Item 601 continues to be appropriate. (Other potential rules impacted are Exchange Act Rule 24b-2 and Securities Act Rule 406, which require that applicants for confidential treatment justify their nondisclosure on the basis of the applicable exemption(s) from disclosure under Rule 80, as well as Staff Legal Bulletin No. 1 and 1A, and Rule 83.)

Since that competitive harm standard is embedded in the SEC’s rules, at this point the prudent path for companies appears to be to continue to adhere the requirements of those rules until the SEC provides further guidance.

The Staff has informally advised us that they are evaluating the potential implications of the Food Marketing Institute decision on Rule 24b-2, Rule 406 & other rules that involve confidential treatment requests under FOIA. However, the Staff does not believe that Item 601(b) is implicated by the decision, since the new procedures relate to situations in which information need not to be filed with the SEC, rather than situations in which companies are seeking to use FOIA exemption 4 to protect information that has been filed.

Insider Trading: Lawyers Are Increasingly In the Cross-Hairs

Over the past year or so, we’ve blogged about a number of insider trading cases in which lawyers were involved directly or, sometimes, indirectly. If it seems like lawyers are being implicated more in insider trading cases, this Arnold & Porter memo says there’s a reason for that – they are:

A recent series of insider trading actions charging senior lawyers in legal departments of prominent public companies suggests that insider trading by lawyers may be on the rise. Over the past several months, the U.S. Securities and Exchange Commission has brought enforcement actions charging insider trading in advance of earnings announcements by senior lawyers at Apple and SeaWorld. In a third action, filed in early May 2019, the general counsel of Cintas Corporation was an unwitting victim of a house guest, a lifelong friend, who, the SEC alleges, surreptitiously pilfered merger related information from a folder in the lawyer’s home office.

These actions are noteworthy not only for the brazenness of the conduct involved, but because they suggest that insider trading by lawyers remains a “profound problem.” And, as the case of the Cintas general counsel demonstrates, innocent lawyers may also fall prey to others, such as close friends and family, looking to exploit their access to material nonpublic information, or MNPI.

Here at TheCorporateCounsel.net, we’re on record that if you’re a corporate officer who engages in insider trading, then – as one of my high school football coaches used to say – “you’re stuck on stupid.” But if you need more convincing, read the memo’s review of the recent proceedings involving lawyers, and the actions that companies & law departments can take to mitigate their insider trading risks.

Remember the classic scene in the movie “Network” in which Ned Beatty’s character, CEO Arthur Jensen, regales Howard Beale with his fire & brimstone “corporate cosmology” speech? It’s his vision of a “perfect world” led by “one vast and ecumenical holding company, for whom all men will work to serve a common profit, in which all men will hold a share of stock, all necessities provided, all anxieties tranquilized, all boredom, amused. . .”

If that’s your cup of tea, then I’ve got great news for you – a recent study says that fulfillment of Arthur Jensen’s vision may be right around the corner. Here’s an excerpt from an FT article on the study:

BlackRock, Vanguard and State Street Global Advisors are on course to control four votes out of every 10 cast at large US companies, as regulators and policymakers probe the wider consequences of their increasing dominance of the investment market. The influence of the Big Three, which have mopped up trillions of dollars of index investments in recent years, is being viewed by politicians as a possible antitrust issue. BlackRock, Vanguard and SSGA, which collectively manage more than $14tn, account for a quarter of votes cast at S&P 500 companies. This is set to grow to 34% over the next 10 years, and 41% in 20, according to academics at Harvard Law School.

The authors of this study are concerned that having the Big 3 control 40% of the S&P 500 will make them unduly deferential to management. I sure hope so – because it seems to me that a far more likely scenario is some variation of them telling us to “Kneel before Zod!”

I know I’ve mentioned this same scene from Network in at least one DealLawyers.com blog, but what can I say? My cultural frame of reference consists almost entirely of 1970s movies & TV shows. Throw in the “Superman II” reference in the last line & I have no choice but to admit that I’m a walking Dad Joke.

“Bad Actors”: Proposed Legislation Would Tighten SEC Waiver Process

Companies that run afoul of the antifraud provisions of the securities laws can find themselves barred from, among other things, using Reg D, Reg A, Form S-3, or qualifying for the forward looking statements safe harbor. In some instances, it isn’t necessarily equitable or in the best interests of investors or the market to impose these sanctions, and so the SEC has developed a waiver process.

Rep. Maxine Waters (D-Cal.), Chair of the House Financial Services Committee, recently introduced the “Bad Actor Disqualification Act of 2019,” which would significantly clamp down on the SEC’s ability to grant bad actor waivers. This excerpt from a recent Sidley memo summarizes the bill’s impact on the waiver process:

The Disqualification Act would eliminate the Commission staff’s ability to grant waivers and instead would impose a three-step process to obtain a permanent waiver. First, a company would need to petition the Commission for a temporary waiver, which the Commission could grant “if the Commission determines that such person has demonstrated immediate irreparable injury.” The temporary waiver would be for a period of 180 days, and all temporary waiver requests (whether granted or not) would be published with an explanation from the Commission as to the rationale for granting or not granting the waiver.

Second, the Commission would publish notice in the Federal Register “of the pendency of the waiver determination and … afford the public and interested persons an opportunity to present their views [on the waiver application], including at a public hearing.” Third, the Commission would hold a public hearing during which it would consider granting a permanent waiver. The Commission would not be able to consider the “direct costs to the ineligible person associated with a denial” and would need to find that the waiver “(i) is in the public interest; (ii) is necessary for the protection of investors; and (iii) promotes market integrity” in order to grant the waiver.

Rep. Waters issued a statement saying that the legislation is intended to protect investors by implementing a “rigorous, fair, and public process for waiving automatic disqualification provisions in the law.” But the Sidley memo contends that, among other things, it would further politicize the waiver process & make settlements with the Commission less attractive to companies.

Earnings Estimates: What If Your Analyst Estimates Are From “Fantasy Island?”

Few things cause more consternation in the C-suite than an analyst whose earnings estimates for your company are wildly out of line with management’s. If that happens to you, this Westwicke Partners blog offers some advice about how to respond.

A member followed up with a very good point – you need to keep Reg FD compliance in mind when you consider Westwick’s advice here!

Geez, I did it again – another 1970s pop culture reference in the title of this blog. I swear, at this point I’m not even conscious that I’m doing it.

While the Staff hasn’t said much about MD&A requirements in recent years, I think most lawyers appreciate that it’s really one of the cornerstones of the entire disclosure system. This recent blog from Bass Berry’s Kevin Douglas offers up 12 things that you need to know when you’re preparing your company’s MD&A. Here’s an excerpt with some tips on Item 303 of S-K’s trend disclosure requirements:

A core disclosure component of Item 303 of Regulation S-K (which sets forth the SEC disclosure requirements applicable to MD&A) is the requirement to provide an analysis of known material trends, uncertainties and other events impacting a registrant’s results of operations, liquidity or capital resources. Practice varies widely among registrants regarding the extent to which the disclosure of forward-looking statements is included in the MD&A.

While there may be reticence among some registrants to include overly expansive forward-looking disclosure (for example, based on concerns about liability exposure if such forward-looking information is not ultimately accurate), countervailing considerations include the fact that such disclosure may result in more useful disclosure as well as the fact that the failure to disclose known trends can give rise to exposure from Rule 10b-5 allegations from private parties as well as SEC civil actions.

The blog also points out that when companies include trend disclosure in their MD&A, they need to keep in mind that this disclosure may need to continue to be included and updated in subsequent periodic reports. Other topics include presentation and readability of MD&A disclosure, the interaction between MD&A and risk factor disclosure, and the use of non-GAAP financial measures in the MD&A.

Del. Sup. Ct. Says Plaintiff Pled Viable “Caremark” Claim

Breach of fiduciary duty allegations premised on a board’s failure to fulfill its oversight obligations are notoriously difficult to establish. One reason that these Caremark claims are so tough to make is that a plaintiff needs to show “bad faith,” meaning that the directors knew that they were not discharging their fiduciary obligations. But last week, in Marchand v. Barnhill, (Del. Sup.; 6/19), the Delaware Supreme Court overruled the Chancery Court and held that – at least for purposes of a motion to dismiss – a shareholder plaintiff stated a viable Caremark claim.

The case arose from a 2015 listeria outbreak at Blue Bell Creameries. In addition to being implicated in the deaths of three people, the outbreak resulted in a recall of all of the company’s products, a complete production shutdown, and a lay-off involving 1/3rd of its workforce. Ultimately, the financial fallout from this incident prompted the company to seek additional financing through a dilutive stock offering.

As a result, the plaintiff brought a derivative action against the board & two of the company’s executives. The plaintiff alleged that the board failed in its oversight duties, but the Chancery Court rejected those allegations. The Supreme Court disagreed, holding that the plaintiff had alleged shortcomings in board level oversight sufficient to survive a motion to dismiss:

When a plaintiff can plead an inference that a board has undertaken no efforts to make sure it is informed of a compliance issue intrinsically critical to the company’s business operation, then that supports an inference that the board has not made the good faith effort that Caremark requires.

Since Marchand involved a motion to dismiss, it’s hard to tell whether the case suggests that Caremark may be a more viable path to imposing liability than it has been in the past – but it’s worth noting that this decision is the second case in the last two years in which a Delaware court has characterized a Caremark claim against directors as being “viable.”

Board Minutes: “Not Too Long, Not Too Short, But Just Right. . .”

Here’s a recent blog from Bob Lamm that has some terrific insights into preparing board minutes. This excerpt contains Bob’s take on the issue of whether to prepare “long-form” minutes or “short form” minutes:

I believe that the proper course is what I call “Goldilocks Minutes.” Not too long, not too short, but just right. Minutes can (and IMHO should) give an indication as to what was discussed. For example, if the board is considering an acquisition, it’s not only OK – it’s actually a good idea – to reflect that the board discussed the merits and risks of the transaction, along with some examples of the factors discussed.

If you’re looking for more of a deep dive into issues surrounding board minutes, check out the March issue of The Corporate Counsel.

Zoom Video Communications is one of the year’s better performing tech IPOs, & now the video conferencing software provider is earning kudos for its effective use of technology to liven up the typically lackluster quarterly earnings call ritual. Here’s an excerpt from this recent Quartz article:

Earlier this month, Zoom disclosed its first quarterly results as a public company. After its press release went out, founder and CEO Eric Yuan and other senior executives hopped onto a Zoom video call to discuss the earnings with analysts, press, and investors. The interactive webinar showed off the company’s technology—and reinvented notions of what a quarterly earnings call should be.

The format introduced a greater degree of transparency between the company and analysts. It wasn’t just the executives whose faces appeared on the screen; when asking questions, the analysts on the call could also be seen—both by the executives and by everyone else on the call.

“You’re not just sort of talking into a box or a handheld—you’re actually looking at each other in the eye and you’re actually talking to feel like we’re connecting with a lot more people,” says Tom McCallum, Zoom’s head of investor relations.

The dynamics transformed the call from a presentation to more of a conversation, with executives and analysts essentially chatting face-to-face via video screens (journalists on the call were in view-only mode). The ability to see each speaker’s face brought a distinctly human touch to something that, with other companies, often feels like an anonymous, formulaic encounter steered by barely-human-sounding teleconference operators reading from scripts and frequently betraying their lack of familiarity with either the presenters or the callers on the line.

Here’s the presentation, which – while not exactly Avengers: Endgame – is more interesting to look at than the standard call. The Q&A is what you want to see, and that starts around the 20 minute mark. My one beef is that you have to rummage around the IR website a bit to find the presentation – while a link to the earnings release appears on the home page, the earnings presentation itself does not. You have to click on the “events” link to find it.

Board Recruitment: Assessing First Time Director Candidates

Many companies are finding themselves moving beyond the traditional pool of current & former CEOs to identify new directors – and many of these non-traditional candidates have never served on a public company board. So, how do you assess their qualifications? This SpencerStuart article has some suggestions. Here’s an excerpt about questions that nominating committees should ask covering areas that are key to the success of a new director:

– Interpersonal skills — Has the person demonstrated an ability to build relationships with all kinds of people? To influence and to gain trust and support from others? Can the candidate use diplomacy and tact? Listen and adjust appropriately to others’ input?

– Intellectual approach — Can the candidate handle complexity, or simplify issues to the essence to make sound, logical decisions? What is their comfort level with ambiguity? Does he or she have the

ability to look ahead? To transfer knowledge and experience to different environments?

– Integrity — Will the candidate adhere to an appropriate and effective set of core values and live by them? Is she or he honest and truthful? Is the person authentic, self-aware and confident enough to “be oneself”?

– Independent mindedness — Can the candidate set out and defend a position, even when this means going it alone? What about the ability to maintain positive relationships amid conflicts about ideas?

– Inclination to engage — Is the candidate motivated to invest time and effort in learning about the organization and staying up to date with it? Is she or he diligent enough to follow through with commitments?

A prospective director’s financial competence is also an important issue, and the article suggests that companies include the chair of the audit committee in interviews of a prospective candidate, in order to better assess the financial sophistication revealed by the questions the candidate asks.

D&O for Unicorns: Insurers Move to Public Company Model

High value private companies – i.e., “Unicorns” – are making insurers nervous. These are private companies, but their huge and volatile valuations, significant financing and resale transactions & other characteristics make them appear much riskier to insurers than the typical private company.

As a result, insurers are increasingly moving to public company-style policies for these companies. This Woodruff Sawyer blog reviews the implications of that trend. This excerpt says the biggest issue is the reduced scope of entity coverage found in the typical public company policy:

To be clear, both public and private company forms provide for entity coverage if the corporation is named in a securities claim. The definition of “securities claim” typically includes breach of fiduciary duty suits. As a practical matter, these are the types of claims for which D&O insurance is being purchased for high-value private companies (and public companies, too).

What you lose, however, when you move to the public company form is the expanded coverage for the corporation for other suits that name the corporate entity. For example, on the private company form, defense costs coverage may exist for the corporate entity if a regulator decides to take an enforcement interest in a corporation. Another example is corporate entity coverage for antitrust claims. These scenarios are almost entirely excluded from the public company form.

On the other hand, public company policies may provide greater coverage for D&Os, enhanced ability for the company to select its own counsel, broader coverage for regulatory investigations, and other more favorable policy terms.

{kind=link}