Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

Recently, a member claimed that he heard that the SEC’s Public Reference Room was closed. I was surprised to hear that – so I paid a visit to find out that it indeed still exists. It does – albeit it’s now subsumed into the SEC’s library, with daily hours reduced to 10 am – 3 pm.

Of course, the importance of the Public Reference Room has greatly diminished over time. Before Edgar came online, that was the place to go to obtain SEC filings. There were times when there was a huge line to merely gain access to it – and it was often bedlam as described in this NY Times article from 1982. And here’s a GAO report from 1989 about how to improve its operations – remember microfiche! Here’s a pic of the room from 1937. And even when Edgar first started, there were many SEC-related documents that could be found only there.

But at this point, it’s more of a historic relic as information is readily available online, for free or a fee. In fact, the Public Reference Room now consists of what essentially is a one-person office with a solitary filing cabinet in it, filled with Form 144s. And if the SEC eventually requires the electronic filing of those forms (which Jesse Brill has urged for quite some time in The Corporate Counsel and more recently in this rulemaking petition), I imagine the Public Reference Room will truly be history. Please send your memories of the place – I won’t share without your permission.

How’s the SEC’s Library Looking?

I did visit the SEC’s library, which always has been one of my favorite spots. How many of the old-timers out there remember the library being jammed with both Staffers and visitors? And more than one Staffer perhaps getting a little shut eye? A nice quiet place for a nap. Send me your fond memories (and I won’t attribute unless you want it).

Getting in there is not as simple as the old days, when you could just walk in off the street. You still can walk in off the street – but you first must go through security and then wait in the Visitor’s Office until a librarian comes to fetch you. But it’s worth the trip! Of course, the library’s staff spends most of its time managing the numerous electronic resources available to the entire SEC – so the book collection is not visited often. It’s more of a museum. But for securities law nerds, it’s full of classic resources.

An exclusive group of heavyweights is chosen to deliberate over an obscure, yet crucial, policy matter. Two players who didn’t make the membership cut take offense, and spurn an invitation to join the discussion. It’s the stuff of classic Washington power politics intrigue. In this case, the tussle over the shape of an advisory panel has set up a behind-the-scenes tiff between the country’s top markets regulator – the Securities and Exchange Commission — on the one side, and two of the country’s biggest exchanges — the New York Stock Exchange, and Nasdaq – on the other.

The two exchanges are so upset the SEC didn’t offer either of them a seat on the agency’s Equity Market Structure Advisory Committee that they have spurned offers by the panel to participate in policy deliberations held by its members behind closed doors, according to people familiar with the matter.

Our February Eminders is Posted!

We have posted the February issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

Spanking brand new. By popular demand, this comprehensive “Materiality Handbook” covers a wide range of scenarios, from how 8-K, press releases and Reg FD to 10-Ks and 10-Qs and securities offerings. This one is a real gem – 32 pages of practical guidance – and its posted in our “Materiality” Practice Area.

The FASB’s “Materiality” Rulemaking: Comments So Far

The two FASB proposals for determining materiality continues to stir controversy. For example, these proposals have raised the ire of investors, including the SEC’s Investor Advisory Committee (see this comment letter from CII and this NY Times column). In its proposals, the FASB has said materiality is a legal concept – and in essence, isn’t an accounting concept. The latter is debatable as many courts have cited to the FASB’s concept of materiality in their decisions – and materiality has been discussed in both legal cases and in the accounting literature (eg. SAB 99). Here’s the comments on the FASB’s proposal so far – check out this one from Jack Ciesielski.

Audit Committees: Regulators Change Bank Duties

This blog by Steve Quinlivan notes how the Federal Reserve, FDIC and OCC recently issued an advisory to indicate their support for the principles in Parts 1 and 2 of the Basel Committee on Banking Supervision’s March 2014 guidance on “External audits of banks” referred to as the “BCBS external audit guidance.” Steven notes that Matt Kelly has written two blogs about the advisory, including this one about the practical implications of it…

Check out this blog by Mike Gettelman to hear what Delaware Chief Justice Leo Strine said this week at the San Diego conference…

Here’s something from Abby Jones, who recently retired from QEP Resources as corporate secretary:

Investor Relations and corporate governance teams increasingly are receiving investor questions about ESG matters. What should these teams do if they receive a call or letter?

How We Got Here – ESG stands for Environmental, Social and Governance. ESG has become shorthand for investment methodologies that consider sustainability. The ESG investment theory posits that considering ESG factors offers portfolio managers added insight into the quality of a company’s management, culture, and risk profile. ESG investors want companies to increase their disclosure of environmental, social and governance information so that investors can make investment decisions with that information in mind.

In February 2010, the SEC issued an interpretive release titled “Commission Guidance Regarding Disclosure Related to Climate Change.” In response, few companies provided climate change disclosure in their 10-Ks. Fearing the SEC guidance was inadequate, advocacy groups including the Global Investor Coalition on Climate Change, the Climate Disclosure Standards Board, and the Sustainability Accounting Standards Board issued carbon asset risk disclosure guidelines.

And some sustainability advocacy groups – such as Ceres – claim that most companies have failed to provide meaningful carbon asset risk disclosures in response to these guidelines. In order to obtain information, some large investors with ESG goals have begun to contact investors directly. Hence the calls.

Who is Calling Whom? – Some large investors such as state pension funds and large institutions with specialized funds have ESG teams devoted to gathering ESG information. Their first point of contact is typically someone in Investor Relations or the Corporate Secretary’s department.

What Do Investors Want to Know? – The information these investors seek can be very specific. For example, some investors have recently asked for greenhouse gas (GHG) emission totals, plans to submit data to the Carbon Disclosure Project, internal GHG emission targets, plans to adopt a corporate sustainability plans, and other related data. Those asking the questions are often well-informed about the subject matter and the industry involved.

What Should I Do Upon Receiving a Call or Letter?

Here are my suggestions:

1. Make sure all internal stakeholders are aware your company has been contacted. This will generally include Investor Relations, the Operations and/or the Health Safety and Environmental (HSE) team, the governance team, the CEO and CFO. Obviously, the list will vary depending on the organization.

2. Determine whether any of the information is proprietary, and your company’s willingness to release it, whether narrowly or broadly.

3. Determine whether your company has the information sought, and whether you measure it the same way the requesting investors do.

4. Ascertain which department(s) are responsible for gathering and maintaining the information.

5. Put together a working group to assemble the data to be released and to answer the policy questions.

6. Decide whether your company wants to provide the information just to the investor who requested it – or more broadly.

7. Set up a time to talk with the investor representatives. Even if your company plans to broadly disseminate the information, you should take the time to speak with the investors who contacted your company.

8. If you plan to disclose to just the individual investors, review all data you plan to provide with legal counsel to ensure you do not run afoul of Regulation FD. Have that counsel present during the call in case the answer to a question prompts disclosure of additional information.

9. If you plan to disclose the information more broadly, work with the Legal Department Investor Relations, Financial Reporting, and Corporate Communications to ensure adequate and accurate disclosure.

10. Have employees who understand the subject matter on the phone for the call. They are best qualified to have these discussions – and to answer specific questions.

11. If you have good facts to tell, by all means tell them. Investors want you to answer their questions – but in my experience they also like to hear about innovative processes your company has developed to advance ESG goals. Don’t be afraid to go “off topic” to provide good news.

Examining Carbon Reduction ROI & Competitive Positioning

Here’s a great blog by Pam Styles that analyzes disclosures companies have made about their ROI when it comes to carbon reduction initiatives. It includes some good sample purchasing company disclosures…

Transcript: “Audit Committees in Action: The Latest Developments”

We have posted the transcript for our recent webcast: “Audit Committees in Action: The Latest Developments.”

In an insider-trading case that will be closely watched until it is decided before the end of June, the U.S. Supreme Court granted certiorari to decide critical open questions about what is required to establish insider trading by a remote “tippee”—specifically, what kind of personal benefit must a “tipper” receive, and what knowledge of that benefit must the “tippee” have, for a conviction or sanction to stand.

The case is Salman v. United States, No. 15–628, and it involves a criminal defendant who traded on the basis of stock recommendations given to him by the brother of a Citigroup investment banker. The banker had given material nonpublic information about pending M&A deals as a gift to benefit his brother, who in turn gave the information to the defendant, Salman. Salman was convicted, and on appeal, he urged the Ninth Circuit to follow the requirements adopted by the Second Circuit in 2014 in United States v. Newman: that the government must prove that a remote tippee like Salman knew of the “personal benefit” that the original tipper received in exchange for the tip; and that the benefit must be “objective, consequential, and represent at least a potential gain of a pecuniary or similarly valuable nature.” Affirming Salman’s conviction, the Ninth Circuit refused to follow Newman, and held that it was sufficient for the government to establish that the tipper had made “a gift of confidential information to a trading relative or friend.” In so holding, the Ninth Circuit created a significant circuit split over the proper scope of remote tippee liability for insider trading.

To resolve this conflict, the Supreme Court must revisit its 1983 decision in Dirks v. SEC. Dirks held that, to establish tippee liability, the government must show, first, that the tipper of inside information “personally will benefit, directly or indirectly, from his disclosure,” for “[a]bsent some personal gain, there has been no breach of duty”; and, second, that the “tippee knows or should know that there has been a breach.” The Ninth Circuit in Salman and the Second Circuit in Newman each grounded their decisions in Dirks, but drew divergent lessons from it.

The Court’s eventual answer will define the outer boundaries of insider trading liability in future cases. But as we advised in our memo on Newman, whatever the Court’s answer turns out to be, corporations and financial institutions that have established compliance policies and systems to prevent the misuse of confidential information by their employees should continue to maintain, and vigilantly enforce, such controls. Although Salman may well reshape the outer boundaries of the law in this area, the core proscriptions against disseminating material nonpublic information will remain firmly in place, and as the recent In the Matter of Marwood Group Research proceeding illustrates, companies can face significant liability for failing to maintain robust systems and procedures to prevent the misuse of confidential information.

XBRL: SEC Staff Updates FAQs on Calculations

Yesterday, the SEC’s Division of Economic & Risk Analysis updated these FAQs on XBRL calculations. I will never read them personally…and thankfully…

The federal government in DC is quasi-open today – including the SEC – due to the weekend snow storm. There is a 3-hour delay for federal DC workers – with an option for unscheduled telework or leave…

Webcast: “Best Efforts Offerings – Nuts & Bolts”

Tune in tomorrow for the DealLawyers.com webcast – “Best Efforts Offerings: Nuts & Bolts” – to hear from Hunton & Williams’ Greg Cope, Arnall Golden Gregory’s Bob Dow and Pillsbury’s Bob Robbins to learn the nuances of Rule 10b-9 and “best efforts” offerings. Here’s our “Best Efforts Offerings Handbook“…

By the way, don’t forget the annual ASECA dinner for SEC alumni is on Friday, February 19th in DC. You don’t have to be an alum to attend. I won’t be there as I’ll be on vaca but I can say that the cocktail party is always fun beforehand…

As noted in this memo, in a speech delivered last month at the AICPA national conference, SEC Chair White suggested that the SEC will continue to scrutinize the use of financial measures that do not conform with GAAP. Also see Randi’s blog today in “The Mentor Blog” about an uptick on the number of comments related to non-GAAP measures…

The federal government in DC is still closed today – including the SEC – due to the weekend snow storm. See my earlier blog about how this might impact the processing of your filings (& what you can do if you have a deal that must go forward now).

– FAQ #15: Problematic Pay Practices & Equity Plans – Will consider three-year average concentration ratios above 30% for the CEO – or above 60% for the NEOs in the aggregate – as a signal that an equity plan is not broad-based

– FAQ #59: Externally-Managed Issuers – More details about the minimum level of disclosure required to avoid an automatic “against” recommendation

– FAQ #61: Subsequent event handling – More details about how ISS will evaluate agreements or decisions subsequent to the fiscal year covered by the CD&A

Whistleblowers: SEC Grants $700k Award to Expert Outsider

As reflected by this recent SEC whistleblower award, the SEC is willing to provide an award to someone outside the company if they can provide useful information…

Webcast: “Alan Dye on the Latest Section 16 Developments”

Tune in tomorrow for the Section16.net webcast – “Alan Dye on the Latest Section 16 Developments” – to hear Alan Dye of Section16.net and Hogan Lovells discuss the most recent updates on Section 16, including new SEC Staff interpretations and Section 16(b) litigation.

Here are the latest survey results about annual meeting conduct:

1. To attend our annual meeting, our company:

– Requires pre-registration by shareholders – 3%

– Encourages pre-registration by shareholders but it’s not required – 16%

– Requires shareholders to bring an entry pass that was included in the proxy materials (along with ID) – 10%

– Encourages shareholders to bring an entry pass but it’s not required – 20%

– Will allow any shareholder to attend if they bring proof of ownership – 67%

– Will allow anyone to attend even if they don’t have proof of ownership – 30%

2. During our annual meeting, our company:

– We hand out rules of conduct that limit each shareholder’s time to no more than 2 minutes – 10%

– We hand out rules of conduct that limit each shareholder’s time to no more than 3 minutes – 24%

– We hand out rules of conduct that limit each shareholder’s time to no more than 5 minutes – 14%

– We announce a policy that limits each shareholder’s time to no more than 2 minutes (but rules are not handed out) – 10%

– We announce a policy that limit each shareholder’s time to no more than 3 minutes (but rules are not handed out) – 7%

– We announce a policy that limit each shareholder’s time to no more than 5 minutes (but rules are not handed out) – 3%

– There is no limit on how long a shareholder can talk (subject to the inherent authority of the Chair to cut off discussion at any time) – 31%

3. For our annual meeting, our company:

– Provides an audio webcast of the physical meeting, including posting an archive – 21%

– Provides an audio webcast of the physical meeting, but does not post an archive – 3%

– Has provided an audio webcast of the physical meeting in the past, but discontinued that practice – 0%

– Is considering providing an audio webcast of the physical meeting but haven’t decided yet – 0%

– Provides a video webcast of the physical meeting (or is considering doing so) – 7%

– Does not provide an audio nor a video webcast of the physical meeting – 69%

4. At our annual meeting, our company:

– Announces the preliminary results of the vote on each matter (unless special circumstances arise such as a very close vote) – 90%

– Doesn’t announce the preliminary results of the vote on each matter – 10%

In the Winter 2016 issue of the Compensation Standards Newsletter, here are 17 pieces of news & analysis from the last month culled from the three blogs on CompensationStandards.com:

– ISS Updates Burn Rate Tables for 2016

– Poll: Possible Downward Trend in Bonus Payouts for 2015 Performance

– ISS: Three New Sets of FAQs

– LTIP Survey: Balancing Shareholder Returns With Financial Metrics

– List of “Top of Mind” Regulatory Changes

– When Shareholder-Approved Equity Plans Run Dry: Can Inducement Grants Fill the Void?

– 5 Things That Comp Committees Need to Know

– Skadden’s Updated “Compensation Committee Handbook”

– FAS 123(R) 10 Years After: Its Impact & Practical Implications

– Stats: Pledging & Hedging Policies/Clawbacks/Stock Ownership Guidelines

– MTS Systems’ Bonus Plan Performance Measure Disclosure

– PriceSmart’s Use of Competitive Market Data

– Amgen’s Compensation Discussion and Analysis

– A Holiday Hodgepodge

– Accenture’s Proxy Summary

– Back to Work! Proxy Statements, Performance Goals & Adjusted Earnings

– Think Automatic Vesting on a Change in Control Isn’t Important? Ask This Former Employee

You can sign up to get any blog pushed out to you via email whenever there is a new entry by simply inputting your email address on the left side of that blog.

Yesterday, as noted in this press release, the SEC adopted two interim final rules as mandated by the FAST Act that revise Forms S-1 and F-1 for emerging growth companies to provide that as long as their registration statements include all required financial information at the time of the offering, the ECGs can omit certain historical period financial information prior to the offering.

The interim final rules also revise Form S-1 to allow smaller reporting companies to use incorporation by reference for future filings – along with a request for comment on whether the rules should be expanded to include other registrants or forms.

These interim final rules will become effective as soon as they are published in the Federal Register – so within the next week – and folks can comment for 30 days if they want to push the SEC to change these interim final rules before they become “final final”…

ESG: Coming Up on Earnings Calls

This blog by Pam Styles illustrates how sustainability has become a more frequent topic on quarterly earnings calls…

Spanking brand new. By popular demand, this comprehensive “Audit Response Letters Handbook” covers all you need to know about dealing with audit response letters (it’s now posted on our “Audit Response Letters” Practice Area). This one is a real gem – 48 pages of practical guidance.

Webcast: “Audit Committees in Action – The Latest Developments”

Tune in tomorrow for the webcast – “Audit Committees in Action: The Latest Developments” – to hear Morgan Lewis’ Rani Doyle, Deloitte’s Consuelo Hitchcock and Gibson Dunn’s Mike Scanlon catch us up on a host of new SEC, FASB & PCAOB developments that impact how audit committees operate – and more…

Cap’n Cashbags: The Call from the IRS

In this 40-second video, Cap’n Cashbags gets a surprising call from the IRS:

For those that can remember, as noted in this Davis Polk blog, it was the NYC Comptroller’s office who really took the proxy access movement to the next level last year. Now, the Comptroller has issued a new list of 72 companies that have received proxy access shareholder proposals – 36 of them repeats from last year’s list of the 75 that received shareholder proposals…

Webcast: “The Latest Developments – Your Upcoming Proxy Disclosures”

Tune in tomorrow for the CompensationStandards.com webcast – “The Latest Developments: Your Upcoming Proxy Disclosures” – to hear Mark Borges of Compensia, Alan Dye of Hogan Lovells and Section16.net, Dave Lynn of CompensationStandards.com and Morrison & Foerster and Ron Mueller of Gibson Dunn discuss all the latest guidance about how to overhaul your upcoming disclosures in response to say-on-pay-including the latest SEC positions-and the other compensation components of Dodd-Frank, as well as how to handle the most difficult ongoing issues that many of us face.

Sqoop: How Journalists Might Be Viewing Your SEC Filings

I have no idea if this new service aimed at journalists is taking off – most new services don’t – but I found it interesting. It’s called “Sqoop” (but I have no idea how that is pronounced) – and here’s their description of how it works:

Simply execute a search for a company, executive or interest, and Sqoop will deliver search results that click through to detail pages that are far more useful that those from Edgar. For the Form 4, Sqoop translates the codes and does the math so you don’t need to. On all other forms, we provide filing along with any exhibits in expandable view, all within one page. Not only does this help you more quickly assess the news value, but it’s also a better reader experience than linking to dumb Edgar pages where exhibits are inaccessible.

I have no idea why Sqoop is targeting journalists specifically with this service. It seems like it could be useful to others who consume SEC filings. And of course, for those that draft SEC filings, it’s good to keep track of how your end-product may be consumed…

In this podcast, Jim Patterson discusses the life of his former wife, Evelyn Y. Davis, including:

– Can you tell us about Evelyn’s childhood? For example, how did Evelyn’s childhood arrest with her mother and brother by the Nazis in Amsterdam in the final months of WWII affect her life?

– How did you meet Evelyn?

– Can you tell us a story to illustrate how Evelyn felt about her activism work?

– Can you tell us a story about how Evelyn liked to stir it up sometimes at annual shareholder meetings?

– What was her “contribution” to financial reporting/journalism?

– I know Evelyn was active with charitable efforts. Can you tell us about that?

Evelyn Davis: Your Stories

I’m starting to collect anecdotes about Evelyn – please send me your stories (as always, I won’t share them with attribution unless you give me permission). Here’s the first batch:

– You are aware of her prostitution arrest at the United Nations (sexpionage is what the press called it) and her “business services” at a Lexington Avenue hotel in New York. Brief accounts in editions of New York Post and New York Daily News. This one comes from Jim Patterson.

– Bob Lamm of Gunster notes: When my father was 94 last year and found out that Evelyn was still around and kicking, he was shocked – “that woman was old when I was young!” He was CFO of a company 40 or so years ago and had to deal with her. Mostly, he had to stop her from attacking his outside lawyer, who was a very good looking guy.

– I remember her and Donald Trump going at it at the Alexander’s meeting many moons ago.

Evelyn Y. Davis: The Pictures

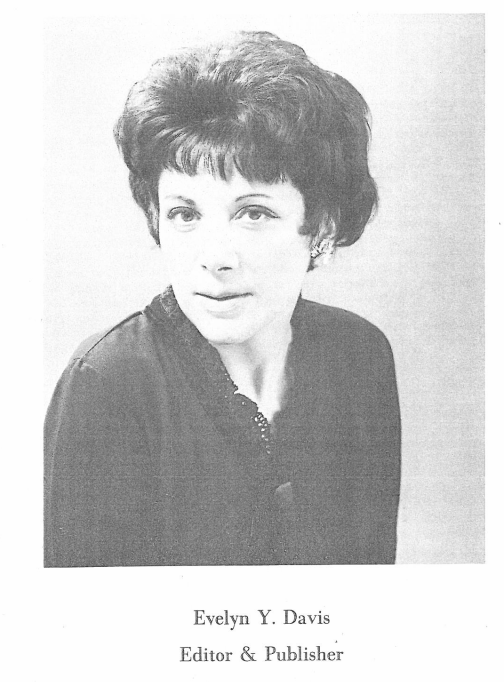

Please send me your pictures of EYD too! From Jim Patterson, here’s a pic of Evelyn from her 1st issue of “Highlights & Lowlights”:

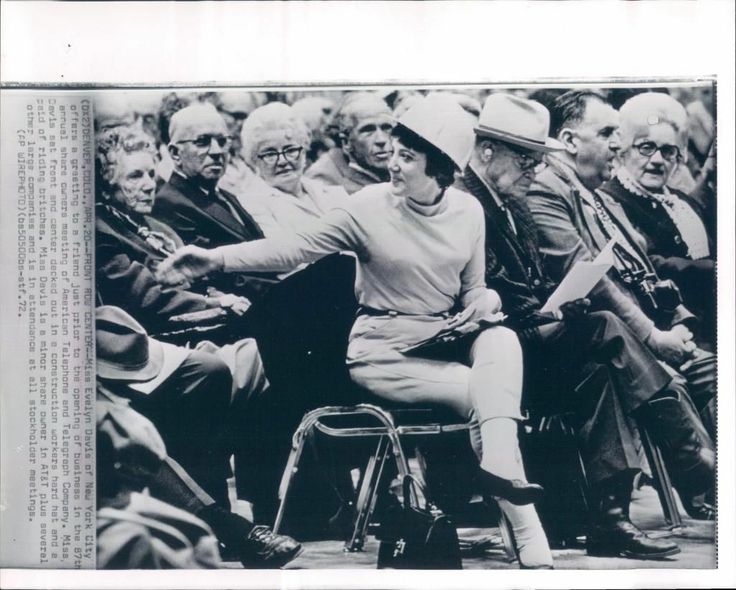

Here’s EYD at a 1972 AT&T annual shareholders meeting: