Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

Yesterday, ISS announced the 2019 updates to its proxy voting policies. We’re posting memos in our “Proxy Advisors” Practice Area (also see this blog from Exequity’s Ed Hauder – and this Davis Polk blog). Here’s the highlights for US companies – except as otherwise noted, the policies apply to meetings held on or after February 1st:

1. Board Diversity: Beginning in 2020 for Russell 3000 and S&P 1500 companies, the chair of the nominating committee (or other directors on a case-by-case basis) will receive an “against” recommendation when there are no women on the company’s board. Mitigating factors include a firm commitment in the proxy statement to appoint at least one female director in the near term, the presence of a female on the board at the preceding annual meeting, or other relevant factors.

2. Economic Value Added Data: During 2019, ISS research reports will feature Economic Value Added data as a supplement to GAAP-based measures that measure the alignment between CEO pay & company performance. Moving into 2020, ISS will consider the inclusion of EVA-based measurements as part of its Financial Performance Assessment methodology.

3. Board Meeting Attendance: ISS is codifying its case-by-case approach to chronic poor attendance without reasonable justification. In addition to voting against the director(s) with poor attendance, it will recommend voting against other directors. After three years of poor attendance, the policy applies to the chair of the nominating or governance committee; after four years, the full committee; and after five years, all nominees.

4. Management Proposals to Ratify Existing Charter or Bylaw Provisions: Similar to Glass Lewis’s new policy on conflicting & excluded proposals, ISS is codifying its policy to vote against individual directors, members of the governance committee, or the full board, where boards ask shareholders to ratify existing charter or bylaw provisions – taking into account factors such as the presence of a shareholder proposal addressing the same issue, the board’s rationale for seeking ratification, the actions to be taken by the board should the ratification proposal fail, whether the current provision was adopted in response to the shareholder proposal, previous use of ratification proposals to exclude shareholder proposals, the company’s ownership structure, etc.

5. Board Responsiveness to Ratification Proposals: ISS’s existing responsiveness policy is updated to reflect that failure to act on a failed “ratification” proposal will trigger a board responsiveness analysis at the next annual meeting.

6. Director Performance Evaluations: When identifying companies that have long-term underperformance, ISS will look at three- and five-year TSR during the initial screen – rather than using five-year TSR as part of a secondary step in the evaluation.

7. Reverse Stock Splits: ISS broadened its policy to allow analysts to take a case-by-case approach for companies that are not listed on major stock exchange and may have a legitimate need to carry out a reverse stock split. ISS is also broadening the factors it will consider for all companies – exchange listed and non-exchange listed, where substantial risks exist.

8. E&S Proposals: ISS is codifying its case-by-case approach to E&S proposals – to make more explicit that significant controversies, fines, penalties or litigation are considered.

Proxy Process Roundtable: Worthwhile Written Comments

Last week, I blogged about what it was like to attend the SEC’s “Proxy Process Roundtable” – you can also check out Cydney Posner’s blog for more details on the substantive discussions. One thing I noted was that there were many people on each panel. The SEC invited a lot of speakers in an effort to get a wide range of views. But since time was limited, not everyone got to delve into their specific recommendations – so at many points, people made reference to the written comments that they’d submitted.

During the ABA meeting the following day, Corp Fin Director Bill Hinman noted that over 80% of the comments came in during the last week – and the Staff thinks they’ve been very constructive. Here are some of the many submissions, from panelists and others:

We continue to post new items daily on our blog – “Proxy Season Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Math With Broker Non-Votes

– An Anti-ESG Campaign Begins

– Vote Tabulations: A Handy Primer

– Iran Disclosure: Impact of Latest Sanctions

– Revenue Recognition: Corp Fin Comments

Recently, the NYSE issued this proposal to change the price requirements for its shareholder approval rules so they would be similar to what the SEC just approved for Nasdaq. As noted in this Cooley blog, the NYSE proposal would:

– Change the definition of market value for purposes of the shareholder approval rule and

– Eliminate the requirement for shareholder approval of issuances at a price less than book value but greater than market value.

More on “Insider Trading: Congressman Allegedly “Tipped” Sellers”

A while back, John blogged about a federal grand jury indicting Congressman Chris Collins (R-NY) on a variety of fraud-related charges arising out of alleged insider trading. I just wanted to circle back to the case to highlight how an insider trading case can impact an entire family. As John noted, the case resulted in the Congressman’s son and father-in-law also being charged.

But they aren’t the only ones facing challenges. The son’s fiancee was suspended from appearing or practicing before the Commission as an accountant. For five years. She lost her job at PwC too. She is only 25 years old. And as noted in this article, her mother also had to pay some money to the SEC. Don’t do it. Don’t insider trade…

Audit Committee Disclosures: The Trends

From this report on audit committee disclosures from the “EY Center for Board Matters,” here are the latest trends:

– In 2018, 71% of companies disclosed the length of auditor tenure. In 2017, the percentage was 64%, and in 2012 it was 25%.

– Sixty-two percent of companies disclosed the factors used in the audit committee’s assessment of the external auditor qualifications and work quality, while in 2017 and 2012 the percentage was 58% and 18%, respectively.

– In 2018, the percentage of companies disclosing that the audit committee considers non-audit fees and services when assessing auditor independence increased to 89% from 86% in 2017. In 2012, 12% of companies disclosed this information.

– The percentage of companies providing an explanation for a change in all fees paid to the external auditor decreased slightly from 45% in 2017 to 44% in 2018, while just 10% of companies made these disclosures in 2012. However, in 2018 only 16% provide an explanation for a change in the audit fee itself.

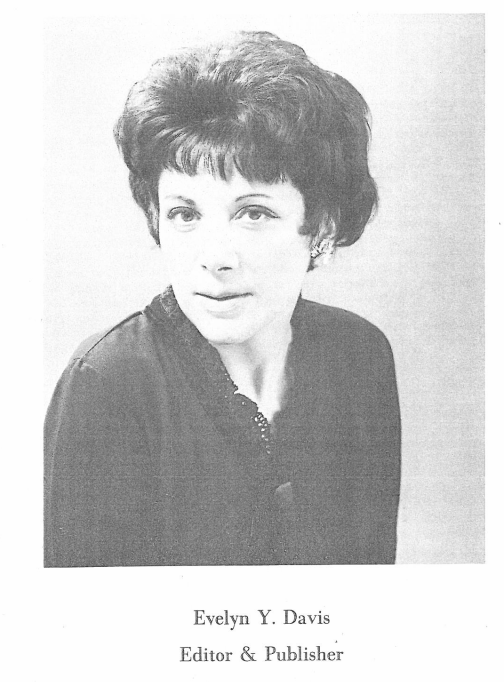

Over the years, I have blogged many times about Evelyn Y. Davis – one of the more well-known shareholder proponents of all-time. I am sad to say that Evelyn passed away a few days ago. Here’s the press release from her foundation. This CBS News article notes she was a concentration camp survivor. Here’s a few of the things I’ve blogged about EYD over the years:

1. Shareholder Proposals: Evelyn Y. Davis (“Dougie” Version)

From 2014: I’ve vowed to step up my style of making videos – and one of my new styles is the jump-cutting that has made the Green brothers so successful. So see if you like this new version of my educational video about Evelyn Y. Davis:

2. Evelyn Davis: Your Stories

From 2016: I’m starting to collect anecdotes about Evelyn – please send me your stories (as always, I won’t share them with attribution unless you give me permission). Here’s the first batch:

– You are aware of her prostitution arrest at the United Nations (sexpionage is what the press called it) and her “business services” at a Lexington Avenue hotel in New York. Brief accounts in editions of New York Post and New York Daily News. This one comes from Jim Patterson.

– When my father was 94 last year and found out that Evelyn was still around and kicking, he was shocked – “that woman was old when I was young!” He was CFO of a company 40 or so years ago and had to deal with her. Mostly, he had to stop her from attacking his outside lawyer, who was a very good looking guy.

– I remember her and Donald Trump going at it at the Alexander’s meeting many moons ago.

3. A Podcast with Evelyn Davis’ Former Husband

From 2016: In this podcast, Jim Patterson discusses the life of his former wife, Evelyn Y. Davis, including:

– Can you tell us about Evelyn’s childhood? For example, how did Evelyn’s childhood arrest with her mother and brother by the Nazis in Amsterdam in the final months of WWII affect her life?

– How did you meet Evelyn?

– Can you tell us a story to illustrate how Evelyn felt about her activism work?

– Can you tell us a story about how Evelyn liked to stir it up sometimes at annual shareholder meetings?

– What was her “contribution” to financial reporting/journalism?

– I know Evelyn was active with charitable efforts. Can you tell us about that?

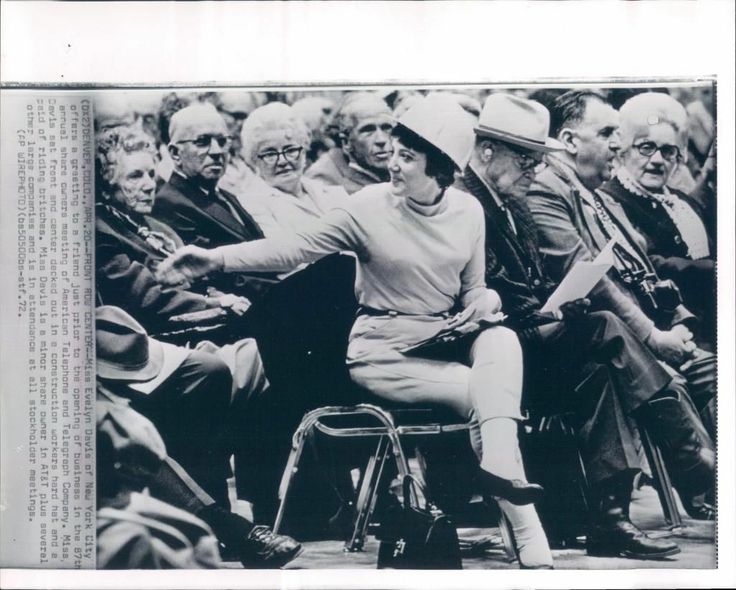

4. Evelyn Y. Davis: The Pictures

From 2016: Please send me your pictures of EYD too! From Jim Patterson, here’s a pic of Evelyn from her 1st issue of “Highlights & Lowlights”:

Here’s EYD at a 1972 AT&T annual shareholders meeting:

5. Evelyn Y. Davis: Retired?

From 2012: For many of you, the news that Evelyn Y. Davis is slowing down at age 82 will come as a mid-proxy season boost. As noted in this Reuters article, Evelyn has been skipping annual meetings this year – and even has halted production of her 47-year-old self-published newsletter “Highlights & Lowlights,” a $600-an-issue review of her governance battles that regularly features photos of her with bemused CEOs. Although Evelyn still has been submitting shareholder proposals to companies, I haven’t heard of her actually attending a meeting for the past two years.

For those of you who have never had the pleasure, go ahead and ask an old-timer for their favorite EYD story. Many of them are unsuitable for print in this family blog. I do note that she is partial to men, particularly if they are CEOs of a Fortune 50 company. Evelyn always had remarkable success with access to the powers that be – and making the CEO available to her often was a wise decision as it made it more likely that she wouldn’t turn your shareholders meeting into a complete spectacle. One day I’ll collect stories to post (including my own). I do note that Evelyn has been quite a philanthropist over the years, particularly in the effort to preserve Chicago history.

Until I post some stories, you’ll have to live with this great WaPo piece from ’03 – and this picture of Evelyn’s pre-bought tombstone in DC (I believe its two divorces behind):

A few months ago, I blogged about the dominance of white people in our industry. I heard some nice feedback. But I particularly liked this one from Carl Hagberg because he offered these concrete suggestions:

I agree that boards – and white people in general – are afraid to talk candidly about race and this needs to stop. In response to your request for ideas, here are a few things that enlightened companies can be doing about it:

– A growing number of companies have been demanding that the law firms they use must have a significant percentage of women and minority group members on the teams for every single company project they are awarded. Many law firms are struggling hard with this – which is precisely the point.

– Smart companies are bidding-out a growing percentage of their legal work – and not only demanding the same degree of diversity for the teams assigned to their projects, but awarding extra points in the evaluation of bids for pro-bono work – where it is easy to specify that diversity efforts and pro-bono work with minority groups will receive extra “extra points.”

– Companies should also be demanding – and rewarding strong diversity efforts – and actual results – at ALL of their service suppliers – like transfer agents, proxy solicitors and advisors, financial printers. And yes, in the selection of Inspectors of Election too.

I know that is extremely hard to diversify. I know from my own experience how hard it is – and why. Take a look at my article about “The Prevalence of Old White Men at Shareholder Meetings.” But if the clients don’t push harder for change, nothing WILL change!

And then Jenner & Block’s Jolene Negre sent me these common approaches:

– Mansfield Rule – Consider diverse candidates for open leadership positions (including board seats)

– Diversity training to give boards the tools they need to think and talk about race as it relates to their businesses

– Some major companies offer financial incentives to law firms staffing those companies’ matters with diverse legal teams (and penalize firms that do not)

“UTBMS”? What The…

Are “matter codes” frustrating – or practical? A new manual – “Best Practices for Using UTBMS Codes for Merger & Acquisition Transactions” – shows how codes can be used in the deal space. Having not been in a firm now for decades, I had no idea what “UTBMS” was. And my initial response was “there needs to be a manual for this!?!”

But I asked around – and here’s what I learned. “UTBMS” stands for the “Uniform Task Based Management System.” It’s how many big company clients wants you to enter your time now so that their outside consultants can flyspeck everything you bill – and it can be helpful for GCs who love all this data analytics stuff. It takes forever to enter your time now – client, matter, service code, and then an individual task code. If you talk with a client on the phone, you’ve got to enter code 9915, “Communicate (with client)”. You need to break down everything you do into these task codes e.g., “Review and Analyze,” “Research,” “Communicate (in firm),” “Communicate (opposing counsel).”

The list is endless – and god help you if you combine two service entries into a single code. The activity codes are useless for transactional work, but you still have to use them. Sounds like it’s not much fun… but that some firms have fully embraced project management now (see “SeyfarthLean” web page)…

ESG Risks Influences Foreign Sovereigns Ratings

As noted in this report, Moody’s says that changing environmental, social & governance considerations can affect sovereign ratings. Moody’s report points out that – while ESG is often spoken of as a single, homogeneous category of risk and while the three overlap in some respects – they are also quite distinct from one another. Of the three E, S and G risks, G has the strongest quantitative relationship with both sovereign ratings and Moody’s four methodology factors: economic strength, institutional strength, government fiscal strength, and susceptibility to event risk.

Yesterday, the SEC adopted rules to update how mining companies disclose their “property” – including how they disclose mineral resources & reserves – so that the SEC’s requirements are closer to what is required globally from mining companies. Here’s the SEC’s press release – and the 453-page adopting release.

The old rules – including the now-obsolete Guide 7 – permitted the disclosure of non-reserve estimates only in limited circumstances. But that will now change. There is a two-year transition period so that mining companies won’t need to comply with the new rules until its first fiscal year beginning on or after January 1, 2021. We will be posting memos in our “Mining Companies” Practice Area.

Say-on-Pay: Rite Aid With a 84% Vote “Against”!

As noted in this Bloomberg article, Rite Aid received a 84% vote ‘against’ on its say-on-pay. I was pretty sure that was a record low…but surprisingly, it’s not even the leader in the clubhouse for 2018! For example, Nuance Communications got only 10% in favor. Some bigger names also got clobbered – Wynn Resorts was at 20%, and Bed, Bath & Beyond was at 21%…

Our November Eminders is Posted!

We have posted the November issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

Back in August, President Trump asked the SEC to study the possibility of moving from quarterly to semi-annual reporting for public companies. We then blogged the reaction to this concept from a number of quarters. And a few weeks ago, SEC Chair Clayton indicated that the push for semi-annual reporting wouldn’t go too far.

Apparently, Chair Clayton’s comments may have been misinterpreted because the latest “Reg Flex Agenda” – posted last week – indicates that a proposal for semi-annual reporting is forthcoming (or at least, it’s in the “prerule” stage – as compared to the “proposed rule” stage). And since the Chair has indicated that his Reg Flex Agendas don’t need to be taken with a grain of salt, we really might expect to see a proposal from the SEC in the ‘shorter rather than longer’ term (meaning over the next year IMHO). In fact, a SEC spokesperson noted in this Reuters article that Chair Clayton was expecting to consider this type of rulemaking even before the President tweeted about it (hat tip to Cydney’s blog)!

And these open rulemakings remain on the ‘long-term’ burner: clawbacks; pay-for-performance; conflict minerals; universal proxy; board diversity disclosures; proxy plumbing – and a proposal based on the recent Rule 701/Form S-8 concept release…

– Average ratio for S&P 500 companies was 160:1

– For the Fortune 1000, it was 158:1

– For the Russell 3000, it was 71:1

– Median employee pay was $69,000 for S&P500 versus $108,000 for the tech industry

– Highest ratios were in retail, consumer discretionary and consumer staples and materials

– Lowest ratios were in financials, healthcare and utilities

– 19% of the Russell 3000 provided some sort of supplemental pay disclosure such as adjusted workforce, full-time only employees used to find median or adjusted CEO pay due to one-time awards

– Some companies noted a low pay ratio this year due to caveats to prepare for higher ratios in the future

“101 Pro Tips – Career Advice for the Ages” Paperback!

I just ordered a bunch more of our latest paperback – “101 Pro Tips – Career Advice for the Ages” Paperback – from the printers because they flew off our shelves. Here’s the “Table of Contents.” It’s free for members of TheCorporateCounsel.net (but it does cost $20 in shipping & handling).

This book is designed for fairly young lawyers – both in law firms and in companies. It’s written in an “easy to read” style, complete with some stories & anecdotes to make it interesting. A fairly unique offering in our field. This is a unique offering – and I’m pretty happy about how it came out. Members can request it now.

Yesterday, the SEC issued this Section 21(a) report about companies with deficient internal controls – in particular, nine unnamed companies that became victims of a cyberfraud called “business email compromises.” This fraud entails employees receiving spoofed or otherwise compromised electronic communications – and in response, employees wired large sums of money or paid fake invoices to the tune of at least $1 million. Two of them lost more than $30 million! Losses for the nine companies totaled nearly $100 million, almost all of which has not been recovered – and some of the frauds lasted a long time & weren’t discovered until the real vendor complained they hadn’t been paid yet.

As noted in this article, there were two kinds of business email compromises — emails from fake executives and ones from fake vendors. In schemes involving emails from fake executives – also called “executive impersonation” – fraudsters not affiliated with a company use spoofed email addresses to send communications that appeared to come from a company executive, typically the CEO. Sometimes, the spoofed emails used real law firm and attorney names. The executive impersonation emails often had these common elements:

1. Referred to time-sensitive “deals” that needed to be completed within days, emphasizing the need for secrecy from other company employees and sometimes suggested some form of government oversight.

2. Claimed that the requested funds were needed for foreign transactions – and all directed the wire transfers to foreign banks. The emails provided minimal details about the transaction – and while all of the companies had some foreign operations, these types of foreign transactions would have been out of the ordinary.

3. Typically went to mid-level personnel who rarely communicated with the executives being spoofed – and who typically were not involved in the supposed transactions.

4. Often included grammatical errors. Hint, hint.

Meanwhile, see this blog about how courts are wrestling with insurance coverage for cyber-related claims…

Governance Stats: Silicon Valley v. S&P 100

This Fenwick & West study surveys the landscape of Silicon Valley’s governance practices and compares them with those found at S&P 100 companies. Not surprisingly, the study found significant differences between Silicon Valley and Corporate America. Here are some highlights:

Annual Meeting Participation:

– An average of approximately 89.1% of shares of SV 150 companies was represented in person or by proxy at company annual meetings during the 2018 proxy season, similar to 2016. However, in addition to the approximately 10.9% not represented, an additional 14.5% were represented via proxy by brokers who did not receive instructions on voting for the bulk of matters for which broker discretionary voting is not permitted. This compares to 12.8% not represented and 13.9% broker non-votes in the S&P 100 in the same period.

– The ranges of representation and voting, though, were somewhat broader in the SV 150 than the S&P 100 (e.g., 52.9% –100% voting in the SV 150, compared to 71.3% – 93.9% voting in the S&P 100).

Director Elections:

– In the vast majority of cases, the elections of directors continue to be uncontested. One of the SV 150 companies and two of the S&P 100 companies had a contested election at its annual meeting in the 2018 proxy season (compared to one in each group in 2017).

– In the SV 150, the dissident stockholder was able to elect two of the three candidates sought.

– In the S&P 100, the dissident was able to have its candidate appointed after very narrowly losing the stockholder vote at Procter & Gamble, and Broadcom was forced to withdraw its slate at the 11th hour following CFIUS review.

Say-on-Pay:

– Opposition to named executive officer compensation reached 15% or more of votes cast (ignoring abstentions and broker non-votes) at 22.8% of SV 150 companies (compared to 13.8% of S&P 100 companies). Within those SV 150 companies with relatively lower levels of support, opposition reached 30% or more at 15 companies (of which nine had opposition of 40% or more, including seven companies where opposition exceeded 50%).

Other Proposals Voted On:

– Setting aside director elections, say-on-pay (as well as say-on-frequency) and auditor approval voting, stockholders at SV 150 companies were asked to vote on one other matter on average, while stockholders at S&P 100 companies averaged 2.5 other matters voted on. The difference is primarily driven by the fact that stockholder proposals are primarily a large company phenomenon. There were only four such proposals voted on by stockholders outside of the top 50 companies in the SV 150.

Company Proposals:

– Excluding director elections, say-on-pay (as well as say-on-frequency) and auditor approval voting, stockholders at SV 150 companies voted on 86 company-sponsored proposals in the 2018 proxy season, primarily in compensation-related subjects, as well as some governance matters (compared to 56 such proposals at S&P 100 companies).

Stockholder Proposals:

– The stockholder-sponsored proposals voted on in the SV 150 generally focused on governance matters or policy issues (this was also true in the S&P 100).

– The average support for stockholder-sponsored proposals was approximately 31.9% at the SV 150 companies (compared to approximately 27.3% at S&P 100 companies).

– The most common topic for stockholder-sponsored proposals in the SV 150 were proxy access (eight proposals, two of which succeeded) and anti-discrimination/diversity (eight proposals, none of which were successful).

– The most common such topic in the S&P 100 was regarding political/lobbying activities (31 proposals, none of which succeeded).

In a speech on Friday, Assistant Attorney General Brian Benczkowski of DOJ’s Criminal Division announced a newly updated policy to guide the Division’s decision-making on whether to require a monitor as part of a corporate criminal resolution. The updated policy codifies the principle that imposing a corporate monitor should be “the exception, not the rule.” Specifically, the policy requires a cost-benefit analysis, directing that a corporate monitor be imposed only where there is “a demonstrated need for, and clear benefit to be derived from,” a monitor when compared to the costs and burdens to the corporation. A monitor “will likely not be necessary” if a corporation’s compliance program is “demonstrated to be effective and appropriately resourced at the time of resolution.”

The new policy also mandates that, where a monitorship is imposed, its scope should be “appropriately tailored to address the specific issues and concerns that created the need for the monitor.” To ensure suitable tailoring, Criminal Division agreements must now include an explanation of the monitorship’s scope, along with a description of the process for replacing a monitor, if necessary. And AAG Benczkowski emphasized that Criminal Division prosecutors have an ongoing obligation to ensure that monitors are acting properly and effectively by “operating within the appropriate scope of their mandate.”

In the same speech, AAG Benczkowski announced that the Criminal Division will eliminate the position of compliance counsel – a role created to some fanfare in the last administration – citing the institutional limitations of relying on a single person as the repository of compliance expertise. But AAG Benczkowski hastened to emphasize that assessment of the compliance function will continue to be a key consideration in every corporate enforcement matter. Rather than hiring a new compliance counsel, the Criminal Division will institute a hiring and training program to cultivate “a workforce better steeped in compliance issues across the board.” Accordingly, this change does not signal a shift in DOJ’s approach to corporate enforcement nor does it diminish the importance of maintaining an effective compliance program.

Since I’ve been blogging so much about Edgar outages (here’s the latest), I decided to get a little more educated about the state of play for Edgar. About a year ago, the “Edgar Business Office” was created. This new office will eventually house “nearly everything Edgar” – including “Edgar Filer Support.” Among other things, the new “Edgar Business Office” is responsible for two main tasks: existing Edgar functions, as well as an Edgar redesign that will take several years to complete.

As for Edgar outages, my primary beef has been a lack of transparency as to when Edgar is down – and when it is back to being operational. As I understand it, this problem is more complicated than I realized. When Edgar is down, it might be just for a few companies (meaning Edgar works for most companies; but not all) – and it might be just for a few minutes. Another challenge for the SEC is that it might take them a little while to realize the magnitude of the problem. So you’re encouraged to contact “Edgar Filer Support” to report a problem.

Given all that, I can see how it would be challenging for the SEC to keep us apprised of what is happening with Edgar – unless there was such a big shortage that it would be apparent (and clearly material to our community as a whole). But there is good news! The SEC has started posting notices when Edgar problems impact the ability of filers to access Edgar – and when they are resolved. These notices are being posted on this “Edgar Systems Announcements” page…

For what it’s worth, this recent update to the “Edgar Filer Manual” addresses warning messages for incorrect XBRL tags, preventing the system from retrieving & exposing a return copy of a test or live submission…

More on “Do You Read Footnotes?”

Recently, I blogged about whether it’s okay to use footnotes when you write. I received many responses from members – and the poll that I ran was popular: 35% said they read them only when they’re in the mood; 41% always read them; 18% only read them for court opinions & SEC releases (no one never reads them – and 7% selected the joke answer of wishing their significant other had the temperament of a footnote).

One member shared the sage advice of his civil procedure professor at Cornell Law – the late & incomparable Rudolf Schlesinger – delivered with a wagging index finger: “The children of lawyers who do not read footnotes will starve.” And Allen Matkins’ Keith Bishop wrote this blog about whether it’s legal to use footnotes…

Will Google Face a SEC “Cybersecurity Disclosure” Enforcement Action?

Over the past few years, the SEC has conducted a number of cybersecurity disclosure investigations – but not much has come out of that other than last year’s action against Yahoo. As detailed in this blog by John Stark, perhaps that will change due to the circumstances involving a data breach at Google…

Steven’s book (“The CEO Pay Machine“) is an easy-to-read & entertaining dissection of how we got to where we are – and how we can fix it. His book is laden with stories that really “tell it like it is.” Please check it out & tell others that can help make a difference…

Tune in tomorrow for the webcast – “Proxy Solicitation: Nuts & Bolts” – to hear Morrow Sodali’s Tom Ball, Strategic Governance Advisors’ Mark Harnett, Kingsdale Advisors’ Lydia Mulyk and Alliance Advisors’ Reid Pearson discuss the art of proxy solicitation in this activism-heightened world.

ISS & CII Team Up Against Proxy Advisor Reform

As noted in this Davis Polk blog by Ning Chiu, ISS & CII recently teamed up to create “Protect the Voice of Shareholders” in an effort to oppose H.R. 4015, the ‘Corporate Governance Reform and Transparency Act,’ that passed the House last October (but never got further than that).

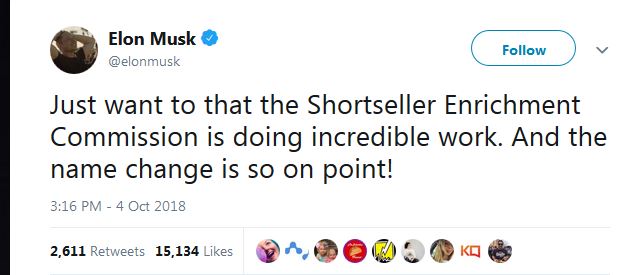

Less than a week into his settlement with the SEC over alleged securities law violations relating to his tweets, Tesla CEO Elon Musk took to Twitter to voice his displeasure with the SEC with this tweet:

Interestingly, in a speech that Liz will blog about next week, Steve Peikin – Co-Director of the SEC’s Enforcement – noted a few days ago that one of the remedies that the SEC obtained is a requirement that Tesla add an experienced securities lawyer to its legal department (see the 4th undertaking associated with fn 8; note that requirement wasn’t noted in the SEC’s press release). I can tell you that Tesla has had one of those already for years. And it doesn’t strike me that Musk is the kind of guy that will listen to his lawyers…

According to news reports, Mark Cuban urged Musk to settle. You may recall that Cuban battled the SEC for years over alleged insider trading – and then Cuban even showed up at the annual “SEC Speaks” conference afterwards. And I even had my own touch of fame after I blogged about Cuban’s settlement and he tweeted at me…

New “Disclosure Simplification” Rules: Effective November 5th

Yesterday, the SEC’s “Disclosure Simplification” rules were published in the Federal Register. They’ll be effective November 5th. I blogged last week about transition issues. We continue to post memos in our “Fast Act” Practice Area…