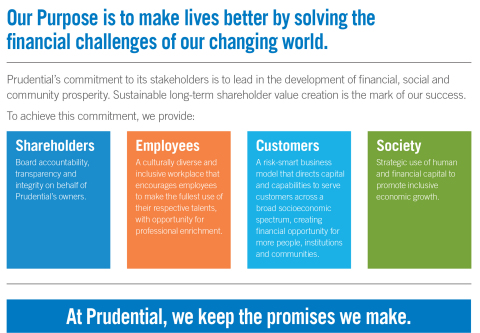

We’ve blogged a lot about the BRT’s redefined “statement of corporate purpose.” Many are frustrated that the topic is getting so much attention, given that the vast majority of directors & companies already view themselves as catering to multiple stakeholders in order to achieve long-term value. I blogged recently on “The Mentor Blog” about that disconnect and the resulting communications opportunity. One tangible thing that some companies are doing – regardless of whether their CEOs signed the BRT statement – is adopting a “statement of purpose” that shows the link between the company’s strategy and its consideration of stakeholder groups.

Last week, Prudential went one step further and also announced a “multi-stakeholder framework” that supports the company’s updated statement of purpose – and shows how the board considers shareholders, employees, customers and society. The press release emphasizes the board’s role in the stakeholder commitments and says that the company will report on the progress of its purpose-driven goals in its annual & sustainability reports. Here’s the infographic:

We’ll be covering more on this issue during our January 21st webcast – “Deciphering ‘Corporate Purpose.’” Join us to hear Morrow’s John Wilcox, Freshfields Bruckhaus’ Pam Marcogliese and Morris Nichols’ Tricia Vella discuss what the debate over “shareholder primacy” means for directors’ fiduciary duties and corporate accountability, and how companies can effectively set & communicate “stakeholder” commitments.

ESG Ratings Draw Nearly Universal Contempt

If there’s one thing that most people in our community can agree on, it’s that the proliferation of “ESG” ratings and funds is causing frustration and confusion. However:

ESG scores can play a key role in determining whether fund managers or exchange-traded funds buy a stock, how much companies pay on loans, and even if a supplier bids for a contract. They can also help verify whether a bond is really “green” or if a company is eligible for a stock benchmark. Investments in about $30 trillion in assets have relied in some way on ESG ratings.

That’s according to this recent Bloomberg article, which cites an MIT working paper. But ratings are difficult to compare and can vary widely. And the variation in how they’re employed – by “ESG” funds, in particular – only compounds the problem. Maybe that’s why the SEC is reportedly looking into these investors:

The SEC initiative is based out of the agency’s Los Angeles office, according to a person familiar with the matter. It has focused on advisers’ criteria for determining an investment to be socially responsible and their methodology for applying those criteria and making investments.

One letter the SEC sent earlier this year to an investment manager with ESG offerings asked for a list of the stocks it had recommended to clients, its models for judging which companies are environmentally or socially responsible, and its best- and worst-performing ESG investments, according to a copy of the letter viewed by The Wall Street Journal. It follows a similar examination letter sent last year to other asset managers, suggesting the regulator decided to broaden its examination.

It’s not clear what the end game would be for this type of examination. Increased disclosure? A standardized reporting framework? That’s a concept I’ve blogged about for companies. The EU already requires large companies to report on their sustainability policies – and within the next couple years will also encourage indexes and benchmark providers to disclose their ESG methodologies (see this White & Case memo and this Bloomberg article).

Government Shutdown Averted!

Good news – the Staff will be returning to work later this week. Congress passed spending bills that the President has now signed, averting a shutdown and keeping the federal government funded through next September. Here’s a short CBS News article about it.

Last year around this time, the government began what ended up being the longest shutdown in history. The SEC went down to a “skeletal staff” for most of January – which put companies in a real bind when it came to negotiating with shareholder proponents, trying to get through the registration process and resolving any Corp Fin comments.

We were blogging about it almost daily (here’s one of the later ones) – and fielded many posts in our “Q&A Forum.” For a reminder about what that was like at the SEC, see Broc’s blog about the deep hole Corp Fin found itself in after the shutdown and my blog wondering whether the shutdown led to Corp Fin reconsidering the Rule 14a-8 no-action request process.

Our own Susan Reilly notes: Before she gave birth to her second son, Liz blogged about her experience balancing pregnancy, parenthood & lawyering. In that vein, I thought I’d share a little about my life as a part-time, work-from-home securities lawyer and mom of three boisterous little boys. I’ve had this job for nearly 6 years now – and here are 5 things I’ve learned:

1. Set deadlines for yourself – The work I do now is dangerously flexible – most of my writing projects don’t have concrete deadlines, which is both a blessing (not having partners or clients breathing down my neck is amazingly liberating!) and a curse (it’s easy to let something that should take just a few hours drag on in drips and drabs for weeks).

While I’m grateful for the flexibility, I need a little structure in order to flourish, and setting deadlines for myself helps. Sometimes going a step further and communicating those expectations to your boss or client will really light a fire – that nagging law firm associate in me still cowers in fear of missing a deadline.

2. Establish office hours – A flexible job schedule has a sneaky way of making you think you can get your work done anytime. But there are always other tasks that jump to the top of the list if you let them – errands to run, appointments to schedule, laundry to fold – the list is endless. Scheduling specific working hours during the day, and being disciplined in keeping them, can keep that other non-urgent “life” stuff from chipping away at your productivity.

3. Enlist help – When my older two children made it to school age, I convinced myself that I didn’t need help with the baby – because I would just get my work done while he napped or after everyone was in bed (ha! – see #2). But I was completely at the mercy of this tiny human who demanded my full attention during his waking hours, whose sleeping hours were far too few.

Eventually I realized that I needed help, and my little guy now spends some time with a sitter a few days a week. When he’s there, I’m able to fully focus on the task at hand without constant interruptions. And when he’s home, I’m able to be a more attentive and less distracted parent.

4. It’s normal to feel disconnected – Because I only work part-time and from home, I can sometimes feel disconnected from my peers. It’s hard to fully relate to the stay-at-home moms or the full-time working moms – because I don’t fit neatly into either category. It’s a weird feeling, having one foot in each camp, but it’s one I’m slowly getting used to.

5. Never take it for granted – When Broc suggested I write a blog post about working part-time, I was both really excited to share my experience – but also a little nervous. I realize that I’m in a somewhat rare position of being able to continue pursuing my legal career while also having the flexibility to be home with my young children.

It’s not lost on me that the challenges I’ve faced with working part-time are ones I would have given my right arm for when I was working brutal hours at a firm – always on call, all the while learning how to be a new parent. Every once in a while, it’s important to take a step back and appreciate that meaningful and rewarding part-time work isn’t easy to come by – and to know a good thing when it comes your way.

Direct Listings: NYSE Files Revised Proposal!

That was fast. Earlier this week, I blogged that the SEC had rejected the NYSE’s proposed rule change to permit companies to sell newly issued primary shares via a direct listing – only 10 days after the exchange had submitted it. The SEC hasn’t made any public statements about why it rejected the proposal, so we still don’t know for sure whether it was because the Commission is fundamentally opposed to direct listings, believes that rulemaking is required, or if there was just something it wanted the NYSE to tweak. But the NYSE signaled that it would continue working on this initiative, and it’s now submitted this revised proposal. As this Davis Polk memo explains, it’s pretty similar to the original:

The new rule change proposal is substantially similar to the proposal the NYSE filed in November, except that issuers can meet the NYSE’s market value requirement by selling $100 million of shares (rather than $250 million under the initial proposal). Consistent with the initial proposal, the revised rule change proposal would provide the same flexibility for an issuer to sell newly issued primary shares into the opening auction in a direct listing, and would also delay the requirement that an issuer have 400 round lot holders at the time of listing until 90 trading days after the direct listing (subject to meeting certain conditions).

Stay tuned as to whether this revision addresses the SEC’s concerns. As Broc blogged when the original proposal was submitted, some are worried about investor protection issues for listings that occur outside of the traditional IPO process – but others note that there are a number of misconceptions about direct listings, including that a direct listing is even a “capital-raising” activity (see more from this Fenwick & West piece). We’re continuing to post memos in our “Direct Listings” Practice Area.

How to Attract & Retain New Lawyers

Law firms lose about $1 billion annually because of attrition, according to Thomson West. Being a young lawyer is marginally better than being a young investment banker (I have only landed in the hospital 2 or 3 times for overworking – I assume it’s a much more regular occurrence with bankers). But practicing law is still a tough gig.

And while my eyes usually glaze over whenever I see anything with “Millennial” in the title, this article connects some dots for scenarios that I’ve seen play out repeatedly. In the span of a couple years, our firm lost a cadre of young lawyers – not to other firms or companies – but to become distillery owners, grant-writers, ultimate Frisbee managers, MFA students… the list goes on.

Here are some pointers worth thinking about:

– A Millennial lawyer will leave a job, not just when he or she is unhappy, but when he or she is not happy enough.

– Give associates time & space to integrate their personal & professional lives (“work-life balance” is so Gen-X).

– Figure out a real way to mentor new lawyers.

– Empower associates to contribute immediately.

– Focus on “doing well by doing good.” The days of asking an associate, “If you can use the hours, I could really use your help on a new deal,” are over. Instead, try this approach: “If you’re interested in helping an interesting client, I’ve got a great deal for us.”

That last one made me laugh because that quote is specifically mentioned in Broc & John’s “101 Pro Tips – Career Advice for the Ages” (but not quite in the way that you’d think). One of the most empowering things you can do for these new lawyers is to help them take control of their own careers – and recognize the benefits of sticking with it. “Pro Tips” delves into the topics above and is a great resource for young lawyers – order it today. Here’s the “Table of Contents” so you can see what’s covered.

Programming Note: Lynn Jokela’s Blogging Debut!

Last month, I announced that Lynn Jokela has joined us as an Associate Editor for our sites. She brings a wealth of experience – here’s her bio. I’m now excited to share that Lynn will be making her blogging debut next week. Lynn’s email uses the domain from our parent company – it’s ljokela@ccrcorp.com – so keep an eye out for that in your inbox!

You likely saw this WSJ article last month, detailing an SEC investigation into one company’s end-of-quarter “earnings management” practices – e.g. leaning on customers to take early deliveries and rerouting products to book sales. The company says “everyone’s doing it” – and according to a McKinsey survey described in this Cleary blog, that’s not too much of an exaggeration:

Lest anyone think the SEC’s focus on “pulling in” revenues is an issue of limited relevance, note that approximately 27% of US public companies provide quarterly guidance, and evidence of widespread earnings management is not merely anecdotal. A broad survey by McKinsey reveals that, when facing a quarterly earnings miss, 61% of companies without a self-identified “long-term culture” would take some action to close the gap between guided and actual earnings, with 47% opting to “pull-in” sales. 71% of those companies would decrease discretionary spending (e.g., spending on R&D or advertising), 55% would delay starting a new project, even if some value would be sacrificed, and 34% would delay taking an accounting charge.

But the widespread nature of these practices doesn’t make the SEC more amenable to them – e.g. they imposed a $5.5 million fine and a cease-and-desist order in a recent enforcement action involving similar maneuvers. The blog notes:

The use of any of these techniques, if resulting in the obfuscation of a “known trend or uncertainty . . . that may have an unfavorable impact on net sales or revenues or income from continuing operations,” would presumably be equally objectionable to the SEC.

Accordingly, for those companies that are still providing earnings guidance, it would be prudent to make sure that your disclosure committee is having frank and frequent discussions with management about exactly what, if any, earnings management tools are being used, whether these tools fit squarely within the company’s revenue recognition policies, whether the company’s auditors are aware of the scope and persistence of these practices, and, most importantly, whether the use of the tools is, intentionally or not, masking a trend of declining sales, a declining market share, declining margins, or other significant uncertainties.

“Climate Accounting”: Exxon Prevails in Martin Act Suit

A couple months back, I blogged that Exxon Mobil was defending itself in New York state court against allegations that it had misled investors by saying publicly that it estimated higher future costs of climate change regulations when it evaluated potential oil & gas projects – when it was actually basing those decisions on current costs, and assumptions that the regulatory environment wouldn’t change.

Among other things, the complaint by the New York Attorney General alleged violations of the state’s Martin Act, which turns on whether there’s a misrepresentation or omission of material facts. The alleged misrepresentations were made by Exxon in reports that were published back in 2014 in exchange for the withdrawal of two shareholder proposals – and were then repeated in other reports such as the company’s “Corporate Citizenship Report.”

Earlier this week, the judge on the case issued this 55-page opinion in Exxon’s favor. Basically, the decision came down to a finding that investors didn’t care about the info – there was no market impact and the info wasn’t “material” when considered with the total mix available in the company’s 10-K and other disclosures. The judge also accepted Exxon’s argument that the company’s internal practices didn’t impact its financials.

This was a big victory, but it’s pretty fact-specific (as detailed in this “D&O Diary” blog) – and you’ve gotta wonder whether the outcome would be the same if the allegations were based on more recent disclosures, since current-day investors keep claiming they care about this stuff. Exxon continues to face other “climate change” lawsuits – including a consumer protection case in Massachusetts. And they aren’t alone. This Davis Polk blog notes that at least one D&O insurer is observing a growing number of climate-related claims – and that it will consider that risk during underwriting. Here’s an excerpt:

Among 28 countries, 75% of climate-related cases brought to date were in the United States alone. The firm anticipates that the failure to disclose climate change risks may drive claims in upcoming years. Moreover, a company’s lack of responsiveness to overall environmental, social and governance (ESG) issues, including ethical topics, can cause brand values to plummet. The insurer warns that, when gauging a company’s reputation, underwriters of D&O insurance will consider the nature and tone of comments made on social media relating to the company.

November-December Issue of “The Corporate Counsel”

We recently mailed the November-December issue of “The Corporate Counsel” print newsletter (try a no-risk trial). The topics include:

1. Hedging Disclosure Is Here—Are You Ready?

– Background of Hedging Disclosure Requirement

– What Item 407(i) of Regulation S-K Requires

– Applicability & Effective Dates

– Interpreting the New Hedging Disclosure Requirement

– Rule Applies to Broad Categories of Transactions

– Elaborate Policy Not Required

– Drafting Proxy Disclosure

– Evolution of the Staff’s Non-GAAP Comments

– What is “Tailored Accounting?”

– Where is the Staff Raising “Tailored Accounting” Comments?

– Comments On Acquisition-Related Adjustments

– Five Key Takeaways on Tailored Accounting

In response to investor pressure to issue an earnings release within the same time frame as prior years, the company announced its 2017 year-end financial results on March 8th and furnished its earnings release on Form 8-K. The company issued the earnings release despite the departure of senior finance and accounting managers, pervasive ERP implementation and internal control issues, and a seven-week delay in the filing of its third quarter 2017 Form 10-Q.

According to the SEC, the earnings release materially misstated, among other things, the company’s earnings for 2017.

On March 19th, the company filed a Form 8-K with the Commission disclosing that it expected its 2017 Financial Results to differ from what had been reported in the March 8th earnings release. The company’s shares declined over eight percent that day.

The company settled with the SEC for $250,000. The pain of dealing with an Enforcement action – and the loss of credibility – was likely an even greater punishment…

FCPA: DOJ Revises Policy to Encourage Self-Disclosures

A couple weeks ago, the DOJ revised its FCPA “Corporate Enforcement Policy” to encourage more self-disclosures to the Department. Here’s an excerpt from an O’Melveny memo that describes the change:

The DOJ eliminated language that appeared to require companies, in disclosing conduct, to characterize that conduct as a violation of criminal law. The DOJ also clarified that companies, when identifying information not in their possession, need only identify evidence actually known to the companies at the time. The changes respond to concerns raised by companies and the defense bar about language in the CEP, and reflect the current Administration’s push to make DOJ policy towards corporate enforcement more reasonable.

While the policy doesn’t apply to SEC Enforcement, the memo does note that the the DOJ’s Criminal Division has expanded the CEP beyond FCPA cases, and stated that it will act as non-binding guidance in Criminal Division cases involving healthcare, financial fraud, and other violations.

This Nixon Peabody memo blacklines the revisions – and explains they could be interpreted to encourage companies to share more information at an earlier stage of internal investigations in order to get full cooperation credit. We’re posting memos in our “FCPA” Practice Area as they come in…

California Consumer Privacy Act: FAQs

Ready or not, the CCPA takes effect January 1st. This memo from Womble Bond Dickinson lays out some “frequently asked questions” for companies that are trying to navigate compliance issues. Here’s one that could require some effort:

Question: Does the CCPA require changes to existing contracts?

Answer: If you are a business subject to the CCPA and do not want to be a data seller under the CCPA, then yes, you will need to amend contracts to add appropriate “service provider” language to the contract. If you are a service provider serving businesses subject to the CCPA, you can expect to receive requests from your customers described under the immediately preceding sentence. Also, where you yourself wear both hats, you may find you need to make both downstream and upstream changes to your agreements to comply with the CCPA.

Last week, the House passed the “Insider Trading Prohibition Act” by a vote of 410-13. John blogged about the bill back in June when it passed out of the House Financial Services Committee – it would broadly describe “wrongful” trading or communication of material non-public information by tying it to:

(A) theft, bribery, misrepresentation, or espionage (through electronic or other means);

(B) a violation of any Federal law protecting computer data or the intellectual property or privacy of computer users;

(C) conversion, misappropriation, or other unauthorized and deceptive taking of such information; or

(D) a breach of any fiduciary duty, a breach of a confidentiality agreement, a breach of contract, or a breach of any other personal or other relationship of trust and confidence.

The legislation would also require only that a defendant was aware or recklessly disregarded that the inside information was wrongfully obtained – rather than specific knowledge of how it was obtained or whether there was a “personal benefit” involved. It also leaves open the possibility that 10b5-1 transactions could be exempt from insider trading prosecution. Mostly, though, it pretty closely tracks current case law.

So what are the odds that this bill will become law? It appears to have “bipartisan” support – but it’s also been floating around in some form since 2015 and hasn’t made it to the finish line yet. The repetition certainly makes it easier to come up with headlines – I copied today’s from a 2017 write-up by John.

SEC Enforcement: “Cooperation” Becomes More Common

Last month, Broc blogged about the Enforcement Division’s annual report on its activities. This annual study from Cornerstone Research & NYU takes a closer look at the results for public companies & subsidiaries. Here’s some takeaways (also check out this Orrick blog saying that crypto & blockchain issues still appear to be enforcement priorities):

– While the number of enforcement actions rose more than 30% over the previous fiscal year, more than half of the new actions targeted investment advisers/investment companies or broker-dealers

– In FY 2019, the SEC noted cooperation by 76% of defendants, a record-high percentage and substantially higher than the FY 2010–FY 2018 average of 51%

– In the first half of FY 2019, the SEC brought 100% of enforcement actions as administrative proceedings; in the second half, this dropped to 84%

– Challenges to the constitutionality of protections preventing removal of the SEC’s administrative law judges (ALJs) continued in FY 2019 with a new defendant filing challenges following the August 2019 dismissal of Lucia v. SEC

– The average monetary settlement amount for public & subsidiary actions during the period was $16 million

When the SEC’s Enforcement Division released its annual stats last month, Broc blogged that some of the motivation behind the report might be for the SEC to show Congress that its money is going to good use. That hunch aligns with the recent recommendation by the Government Accountability Office that the SEC needs to do a better job of documenting its procedures for generating these reports – including procedures for compiling & verifying stats and documenting their implementation.

Since 2009, the Division of Enforcement (Enforcement) in the Securities and Exchange Commission (SEC) has made modifications to its reporting of enforcement statistics, including by releasing a stand-alone annual report beginning in fiscal year 2017. The Enforcement Annual Report included additional data on enforcement statistics not previously reported and narratives about enforcement priorities and cases. Enforcement staff told us the annual report was created to increase transparency and provide more information and deeper context than previous reporting had provided.

Enforcement has written procedures for recording and verifying enforcement-related data (including on investigations and enforcement actions) in its central database. However, Enforcement does not have written procedures for generating its public reports (currently, the annual report), including for compiling and verifying the enforcement statistics used in the report. To produce the report, Enforcement staff told GAO that staff and officials hold meetings in which they determine which areas and accomplishments to highlight (see figure). Enforcement was not able to provide documentation demonstrating that the process it currently uses to prepare and review the report was implemented as intended.

Developing written procedures for generating Enforcement’s public reports and documenting their implementation would provide greater assurance that reported information is reliable and accurate, which is important to maintaining the Division’s credibility and public confidence in its efforts.

That was fast. On Friday, Reuters and other sources reported that the SEC rejected the NYSE’s proposed rule change that would have permitted companies to sell newly issued primary shares via a direct listing – which had been submitted the week before.

Broc just blogged last week about the proposal being somewhat controversial. We aren’t sure what aspect of it prompted the rejection – but it’s not uncommon for these types of things to go through a few iterations and this Wilson Sonsini memo speculates that perhaps additional SEC rulemaking is necessary to make primary listings possible. The NYSE says it’s continuing to work with the SEC on a “direct listing product” – so it’s probably not the last we’ll hear of this path to going public.

Direct Listings: Nasdaq’s “Resale” Rule Extended to Its Global & Capital Markets

Last week, the SEC approved this recent Nasdaq proposal that will allow “resale” direct listings on the Nasdaq Global Market and the Nasdaq Capital Market – an extension of an already-existing rule that allows these types of direct listings on the Nasdaq Global Select Market.

This Wilson Sonsini memo summarizes the final rule – and explains how the valuation parameters for companies listing shares on Nasdaq’s Global and Capital Markets differ slightly from what applies to the Nasdaq Global Select Market.

Nasdaq Proposal: Excluding Restricted Shares from “Publicly Held” Calculation

The exchanges have been busy. A couple weeks ago, Nasdaq filed this rule proposal that would require listed companies to provide Nasdaq with info about the number of their non-affiliate shares that are subject to trading restrictions – e.g. due to lockups or standstills, private offering restrictions, etc. – if the exchange observes unusual trading activity that implies limited liquidity.

Under the proposed rule, Nasdaq could also halt trading in connection with the request and could require companies with inadequate “unrestricted public float” to adopt a plan to increase the number of unrestricted shares. Nasdaq already has a similar rule for initial listings, but this would extend the concept to continued listing rules.

The SEC posted the rule for comment last week, so we likely won’t know for at least a couple of months whether this rule will be approved in current form or at all.

Yesterday, Corp Fin unveiled its “Shareholder Proposal No-Action Responses Chart” – and posted the first “informal” no-action response under its new process for Rule 14a-8. DLA Piper’s Sanjay Shirodkar shared this Staff email that accompanied the response:

The staff completed its review of the company’s submission. Our response will be posted after 4:30 PM this afternoon in our 2019-2020 Shareholder Proposal No-Action Responses Chart, which is available on our website at https://www.sec.gov/divisions/corpfin/cf-noaction/14a-8.shtml. Copies of all correspondence relating to this submission will be made available at the same address after a short delay. If you have any questions, please call the Office of Chief Counsel in the Division of Corporation Finance at (202) 551-3520.

We also held a big webcast on this topic just yesterday – “Shareholder Proposals – What Now?” – with Corp Fin’s Chief Counsel David Fredrickson, Davis Polk’s Ning Chiu, Morrison & Foerster’s Marty Dunn and Gibson Dunn’s Beth Ising. If you missed it, the audio archive is already available – and the transcript should be coming a week or so after Thanksgiving.

“Say” Earnings Calls: Not Just For Retail Anymore!

We’ve blogged a couple of times about the “Say” platform that allows shareholders to submit questions during earnings calls, investor days, webinars and annual meetings. Originally, Say focused on increasing retail participation in these events – but it recently announced full access to its Q&A polling for institutional investors as well.

Say also announced that it would collaborate with “Just Capital” on a new type of “shareholder engagement” platform – quarterly calls that allow CEOs to speak with investors about ESG & “stakeholder” value. Last week, Paypal’s CEO broke ground as the first participant.

State “Securities Act” Litigation: Another One Bites the Dust

A few months ago, I blogged about a ’33 Act case being dismissed from state court in New York – offering some hope to companies who are worried about a deluge of state litigation due to the Supreme Court’s 2018 Cyan decision. This D&O Diary blog from Kevin LaCroix recounts another story of hope – this time, a recent dismissal in Connecticut. Here’s the takeaway:

These various dismissal motions rulings are of course themselves without precedential value and are subject to appeal. However, one can hope that these rulings may send a message that the plaintiffs should reconsider whatever perceived advantages they may think they have in proceeding in state court rather than federal court.

Unfortunately, despite these rulings, Cyan still creates significant risks for companies. This blog gives a real-life, recent example of a company facing a heap of lawsuits on the heels of its IPO. And because simultaneous state & federal securities lawsuits can’t be consolidated, it’s extra messy. Kevin notes that Congress could fix the problem by making a “simple” tweak to Section 22 of the ’33 Act that eliminates concurrent state court jurisdiction…

I’m very excited to announce that Lynn Jokela has joined us as an Associate Editor for our sites. Lynn has spent the last 11 years in the corporate secretary’s group of a Dow 30 company, following a stint in private practice and a prior career in finance & business. She brings tons of practical experience on all things “corporate & securities” and will be a fantastic addition to our team. Her email address is included in her bio if you want to drop her a line – and she’ll be blogging soon enough!

Transfer Agents: Market Share Leaders

A recent “Audit Analytics” blog highlights current market share leaders among transfer agents. Overall, not much has changed:

Since 2012, the market share for transfer agents engaged by active SEC registrants has remained fairly stagnant. This year proves to be no different; the same five transfer agents we have seen in the top for the past several years still reign. In fact, four of the five have managed to slightly increase their respective market share compared to last year’s results.

The exception, Wells Fargo Bank NA/TA, has shown an expected decrease in market share since our last analysis. As noted last year, Wells Fargo Bank sold its Shareowner Services to Equiniti Trust Co. (part of Equiniti Group plc). This may also explain the increase in market share for the non-top five transfer agents (Other), but only time will tell.

For more color on the industry players – and helpful new offerings by the top transfer agents – check out page 5 of the latest edition of Carl Hagberg’s “Shareholder Service Optimizer.” Carl notes that the market seems ripe for major comparison shopping…

Filing Fees: SEC Unveils New Template

Filing fees: they seem like such an easy task – until one of the 18 people involved in this “game of telephone” drops the ball on the required info. That’s why the SEC recently announced a new pre-populated “FedWire” template.

To make sure all necessary info is included – and avoid filing delays – the Commission is encouraging all companies to use the template when they submit info to their banks to initiate FedWire payments.

We’re very excited to have David Fredrickson – Corp Fin’s Chief Counsel – joining our other esteemed panelists on our webcast tomorrow: “Shareholder Proposals – What Now?” So tune in to hear David – along with Davis Polk’s Ning Chiu, Morrison & Foerster’s Marty Dunn and Gibson Dunn’s Beth Ising – discuss Corp Fin’s new approach for processing shareholder proposal no-action requests, what’s new due to Staff Legal Bulletin 14K and the potential impact of the SEC’s new 14a-8 rulemaking proposal. Don’t miss it!

“ESG” Funds: What’s in a Name?

Regular readers of this blog know that we write more than we want to about the rise of “responsible investing” – e.g. just yesterday. It’s not that we’re opposed to the trend, we just question how meaningful it is. Incidentally, that’s also what’s frustrating people who want it to grow faster.

But here’s the deal: investors want to feel good – but in the end, they also want their returns to match what they’d get by tracking a broad market index. The funds that meet those dual desires end up attracting the most cash, even though some of the “cleaner” funds have significantly outperformed the competition in recent years. This is America! It’s all about marketing.

That’s why, as this WSJ article points out, it’s pretty common for “sustainable funds” to invest in fossil fuel companies (the tagline of the article is that “8 of the 10 biggest US sustainable funds invest in oil & gas companies”). And if that still seems odd to you, the reconciling point is that they invest in the companies with the highest ESG ratings in their sectors – the “most sustainable” fossil fuel companies, if you will.

So when it comes to attracting ESG dollars, the key appears to be outperforming your industry peers – or producing the most information, as Doug Chia suggests. And the Journal explains why that’s unlikely to change any time soon:

Energy shares have often been among the few sectors to reliably produce gains—making them an important group for asset managers. That is especially true for asset managers whose products are aimed in part at institutional investors, which often have less room to miss their target returns. Also, an oil company that scores poorly on one element of ESG—say, the “E”—might do well on the other two elements, meriting its inclusion in a fund.

Transcript: “Sustainability Reporting – Small & Mid-Cap Perspectives”

We’ve posted the transcript for our recent webcast: “Sustainability Reporting – Small & Mid-Cap Perspectives.”

Recently, the “Governance & Accountability Institute” announced that 60% of the Russell 1000 are now publishing sustainability reports. The top half of that index aligns with the S&P 500 – where sustainability reporting has become mainstream – and 34% of the smaller companies have picked up the practice too. Here’s some other takeaways:

– Of the 60% of Russell 1000® companies that report, 72% were S&P 500® companies – and 28% were from the second half of companies in the index

– Of the 40% of Russell 1000® companies that do not report, 83% were the smaller half of companies by market cap – while only 17% of the non-reporters were S&P 500® companies

Like just about everything, this has become a political issue too. This Stinson blog reports that a right-wing org is asking the SEC to prohibit companies from making “materially false and misleading claims and statements related to global climate change.” Meanwhile, in the more mainstream world, the US Chamber is now focusing on sustainability disclosure – and has now released its own set of “best practices” for voluntary ESG reporting.

“Responsible Investors” Say ESG Isn’t a Fad

You have to wonder what’s driving sustainability reporting by smaller companies. They’re less likely than large companies to be doing it in response to proposals from “activist” shareholders. But there are also shareholders whose attention companies actually want to attract. A recent SquareWell Partners study says that providing ESG info is the “price of entry” for companies of all sizes that want to add big investors to their rosters – or keep them there. Here’s a few key findings:

– Nearly all of the top 50 asset managers (managing $50.6 trillion) are signatories to the UN “Principles of Responsible Investing” – committing to incorporate ESG factors into investment & ownership decisions

– Oddly, the Global Sustainable Investment Initiative reports “only” $30.7 trillion of sustainably invested assets last year – so it’s possible the PRI signatories aren’t following through on the principles

– One-third of the asset managers clearly disclose their approach to integrating ESG factors into fixed income;

– 64% of the asset managers are signatories to the recommendations of the Task Force on Climate-related Financial Disclosure (TCFD);

– Close to 80% of the asset managers engage with portfolio companies on ESG issues;

– 68% of the asset managers use two or more ESG research and data providers;

– Only 20% of the asset managers have a low receptivity to activist demands; and

– A quarter of the asset managers have gone public with their discontent at portfolio companies since January 2018.

For even more on this topic, see Aon’s 28-page report on responsible investing trends. Also check out this recap from Cooley’s Cydney Posner about a recent meeting of the SEC’s Investor Advisory Committee – where reps from AllianceBernstein, Neuberger Berman, SSGA and Calvert discussed how they’re using ESG data for all their portfolios and (for the most part) called for the SEC to guide companies toward more standardized disclosure.

On the debt side, take a gander at this recent PepsiCo announcement about a $1 billion “green bonds” offering where the proceeds will be used to finance the company’s “UN Sustainable Development Goals.” This Moody’s alert says that green bond issues could top $250 billion this year – much higher than what was originally forecast – and walks through some of the global trends. To keep track of memos on this growing trend, we’ve added a new “sustainable finance” subsection to our “Debt Financings” Practice Area.

E&S Risk Factors on the Rise

This NACD blog analyzes the increasing prevalence of “E&S” risk factors. Here’s what’s trending on climate change:

Thirty percent of Russell 3000 companies discussed climate change as a risk in their 10-K statement, with only 3 percent of companies discussing climate change risk in the MD&A section. Predictably, the energy and mining sector had the most disclosure on climate change risk. Retail and consumer sector companies, which are not thought of traditionally for being exposed to climate change risk, also had a high rate of disclosure, citing damage to their supply chain and access to raw materials as risks.

Disclosures for every sector focused on the risk of regulatory and market responses to climate change, including legislative regulation of air emissions, caps, and carbon taxes. Other companies were more detailed in their discussion of climate change risk as it relates to their specific operations, such as Monster Beverage Co.’s 10-K, which states that, “In addition, public expectations for reductions in greenhouse gas emissions could result in increased energy, transportation and raw material costs, and may require us to make additional investments in facilities and equipment. As a result, the effects of climate change could have a long-term adverse impact on our business and results of operations.”