Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

Recently, Corp Fin posted this no-action response to Apple about “engage multiple outside independent experts or resources from the general public to reform its executive compensation principles and practices.” The retail investor proponent – Jing Zhao – appears to have represented himself in rebutting the company’s (i)(3), (i)(6) and (i)(7) arguments. Corp Fin’s response to the ordinary business argument is that “the proposal focuses on senior executive compensation.”

The proponent’s supporting statement cites Professor Thomas Piketty of France, the darling of the income inequality movement. There likely will be more income inequality-oriented proposals in the coming years…

In this no-action letter, Apple also lost its battle to exclude a proxy access shareholder proposal from Jim McRitchie…

Crowdfunding: So Where’s the Crowd?

This blog from Montgomery McCracken’s Ernie Holtzheimer reviews the first five months of crowdfunding under Regulation CF. So far, the results have been underwhelming:

In its first thirty days, Reg CF got off to a promising start with forty companies raising a total of about $2 million. Although the total amount of money raised was not large by Uber’s standards, the number of offerings was more than double the amount of Reg A offerings made between 2009 and 2012. Since the first month, however, only ten more companies have filed a Reg CF offering, leading to the question – where is the crowd?

Reg CF’s critics point to its $1 million funding cap as a reason for this lackluster performance. And some companies seem to be opting to use new Reg A+ – with its much higher funding limits – instead of Reg CF.

Poll: How Many Comp Consultants Should Apple Hire?

Keying off the shareholder proposal mentioned above, please participate in this anonymous poll:

On the heels of Corp Fin’s announcement back in January that it would no longer scan & post glossy annual reports on Edgar, Corp Fin issued this CDI on Wednesday (note that the CDI is unnumbered):

Question: Exchange Act Rule 14a-3(c) and Rule 14c-3(b) require registrants to mail seven copies of the annual report sent to security holders to the Commission “solely for its information.” A similar provision in Form 10-K requires certain Section 15(d) registrants to furnish to the Commission “for its information” four copies of any annual report to security holders. Can a registrant satisfy these requirements by means other than physical delivery or electronic delivery pursuant to Rule 101(b)(1) of Regulation S-T?

Answer: Yes. The Division will not object if a company posts an electronic version of its annual report to its corporate web site by the dates specified in Rule 14a-3(c), Rule 14c-3(b) and Form 10-K respectively, in lieu of mailing paper copies or submitting it on EDGAR. If the report remains accessible for at least one year after posting, the staff will consider it available for its information.

This is good news as there has been a ton of confusion, as evident from a few threads in our “Q&A Forum” over the years (see #8728 and #7894). Companies have had the option to Edgarize their annual report & have that count as furnishing the 7 copies for a while – but that’s a real hassle & can be costly with graphics, etc. So this is an early holiday present from the Staff. I’ll be posting an updated “Annual Report & 10-K Wrap Handbook” next week – including addressing the issue that I just blogged on the “Proxy Season Blog” about “The NYSE Doesn’t Think ‘Proxy Materials’ Includes the Glossy Annual Report?“…

You might wonder what the Corp Fin Staff does with all those glossy annual reports over the years. They’re stuffed into metallic cabinets & rarely touched – at least back in my day (when the ’34 Act reviews were fairly rare). There was a stir back then after Mustang Ranch tried to go public in ’89 – and I can’t remember what the filing was, perhaps the red herring – but it was in a cabinet for some reason & created a stir…

Form S-3’s “Baby Shelfs”: A New CDI

As noted in this Cooley blog, Corp Fin also issued this new CDI 116.25 about Form S-3’s General Instructions I.B.1 to I.B.6 a few days ago:

Question: An issuer with less than $75 million in public float is eligible to use Form S-3 for a primary offering in reliance on Instruction I.B.6, which permits it to sell no more than one-third of its public float within a 12-month period. May it sell securities to the same investor(s), with a portion coming from a takedown from its shelf registration statement for which it is relying on Instruction I.B.6 and a portion coming from a separate private placement that it concurrently registers for resale on a separate Form S-3 in reliance on Instruction I.B.3, if the aggregate number of shares sold exceeds the Instruction I.B.6 limitation that would be available to the issuer at that time?

Answer: No. Because we believe that this offering structure evades the offering size limitations of Instruction I.B.6, the securities registered for resale on Form S-3 should be counted against the issuer’s available capacity under Instruction I.B.6. Accordingly, an issuer may not rely on Instruction I.B.3 to register the resale of the balance of the securities on Form S-3 unless it has sufficient capacity under Instruction I.B.6 to issue that amount of securities at the time of filing the resale registration statement. If it does not, it would need to either register the resale on Form S-1 or wait until it has sufficient capacity under that instruction to register the resale on Form S-3.

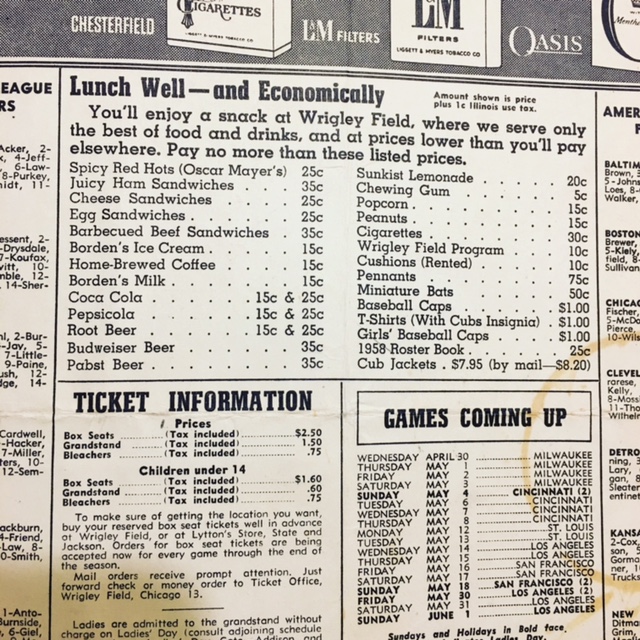

17 Years of Cubs Programs

Growing up near Wrigley Field, I’m gloating with this 10-second video displaying my 17 years of Cubs programs (went to Lane Tech High after Walt Disney Magnet for grade school):

Here’s the inside cover of the 1958 program. Back when you could order a cheese sandwich for only a quarter & a beer was just 10¢ more…

Here’s 8 things I learned at my “Proxy Disclosure Conference” last week in Houston (video archives now available):

1. My experiment with post-panel commentaries was well-received. These were 10-minute sessions with two different experts than the ones that were on the original panel – and the duo of post-panel commentators highlighted what was most important. And filled in some holes.

2. For the longer panels, I gave silly musical intros for each panelist. For Brian Breheny, I said that he could “dispense life wisdom in 5 words or less.” Then I asked him to dispense some. His wisdom was spot on: “Oh, I wasn’t ready for that.” Perfect! Isn’t that truly what life is all about!!!

3. During the “SEC All-Stars” panel, I loved listening to the five former senior Corp Fin Staffers analyze what the next composition of SEC Commissioners might look like. It could be a real shake-up and not resemble any past Commission ever – which could truly impact how the SEC does business!

4. I broke up the long morning with a relaxing 5-minute guided meditation for everyone. It should be a “must” for all conferences. It raises the positive energy in the room, brings stress levels down & improves focus.

5. Most of my panelists have worked over 10 years together at this conference. Their chemistry can’t be beat – enabling them to deliver practical guidance within the shorter & shorter timeframes that I provide them. Tough to fit in 17 panels in a 9-hour day (with 75 minutes devoted to lunch). But many of my afternoon panels are quite short – forcing the speakers get right to the point.

6. Similarly, these panelists have mastered the art of providing their written talking points in straight-forward bullet points – resulting in 180 pages worth of valuable course materials. I believe that bullet points are easier to learn compared to long, drawn-out narrative. It’s also easier to take notes on.

7. Each year, Dave & Marty make their annual 10-minute gag session funnier than the last. Last year, it was the “CEO pay ratio” puppet show. This year, we got more cowbell!

8. Nearly all of the in-person attendees are in-house folks – while nearly all of the folks who watch by video are from law firms. Conference trivia!

See ya next year in Washington DC, where the conference will be held in mid-October! It’s gonna be a big one with pay ratio coming online…

Revenue Recognition: Start Planning Now

This blog – and these memos posted in our “Revenue Recognition” Practice Area – make it clear that your accounting teams should be already planning for compliance with the new standard that must be implemented 15 months from now…

We have posted the transcript for our recent webcast: “Virtual-Only Annual Meetings: Nuts & Bolts.” The agenda included:

– Overview of Virtual-Only Meetings (& How Many Companies Do Them)

– Options When Holding a Virtual-Only Meeting

– Voting Safeguards for Virtual-Only Meetings

– Concerns Over Holding Virtual-Only Meetings

– Contingency Planning for Snafus

– Location of Inspector of Elections During Virtual-Only Meetings

– Who Should Sign Off on Changing Format to Virtual-Only

– Timeline & Preparations for Virtual Meetings

– Preparing for the Q&A

– Board & Auditor Roles During Meeting

– Shareholder Proposals Against Virtual Meetings

– Lessons Learned

Yesterday, ISS released draft policy changes for comment in 15 areas spanning the globe (based on these survey results from constituents) – the deadline for comment is November 10th. It’s expected that ISS will release its final policies in late November (although burn rate thresholds & pay-for-performance quantitative concern thresholds are typically announced through updated FAQs in mid-December; here’s info about the ISS policy process).

For US companies, there are several significant proposals to be aware of:

Director elections:

1. Director election vote recommendations for directors at companies that impose undue restrictions on shareholders’ ability to amend bylaws:

– ISS proposes to amend its director election policy to include a provision to issue adverse vote recommendations on governance committee director elections where companies have placed “undue” restrictions on shareholders’ ability to amend the company’s bylaws.

– Examples of these restrictions include the outright prohibition on the submission of binding shareholder proposals, or share ownership requirements or holding periods in excess of SEC Rule 14a-8.

– Adverse vote recommendations will continue until the restrictions are completely lifted.

2. Director election vote recommendations for directors that have taken unilateral board actions or maintain unequal voting rights:

– ISS proposes to clarify its director election policy to state that, upon a company holding an IPO with a multi-class capital structure with unequal voting rights or other problematic governance provisions, ISS will generally issue adverse director vote recommendations unless there is a “reasonable” sunset provision on the unequal structure or the problematic provisions.

– The key change is that ISS will no longer consider the results of shareholder votes on problematic features when issuing vote recommendations; instead, ISS will only consider the inclusion of “reasonable” sunset provisions.

US-listed cross-market companies (companies listed in the US, but incorporated outside):

1. General share issuance proposals at companies listed in the US, but incorporated outside the US:

– ISS proposes to recommend in favor of general share issuance authorities up to 20 percent of currently issues capital, as long as the duration of the issuance authority is reasonable and clearly disclosed.

2. Executive compensation proposals at companies listed in the US, but incorporated outside the US:

– ISS proposes to implement, on a case-by-case basis, US policy in the evaluation of all compensation proposals on the ballots of companies listed in the US, but incorporated elsewhere.

– For proposals where there is no applicable US policy, the ISS policy from the country requiring the ballot item will be used.

– For clarification, say-on-pay proposals from most markets will be evaluated under the US Management Say-on-Pay voting policy.

Failure to Detect Fraud: EY Pays $12 Million Fine

Recently, EY agreed to pay $12 million to the SEC for failure to detect auditing fraud at a client. The client paid a $140 million penalty to the SEC for using deceptive income tax accounting…

Happy 25th! A Tear-Jerker…

Proving that some good things do happen on Facebook, here’s a note that my son in college posted about our 25th wedding anniversary this week:

A child’s parents are their first glimpse into the world of human interaction, the primary source in their subconscious thesis on how to deal with other people. Lucky then, that my social foundations are anchored in a relationship such as the one you two have – one born from love, empathy, and mutual respect.

The decency with which you treat each other is something I’ve learned a great deal from, and the effort you give to make each other happy is something I strive to replicate every day. You’ve taught me that any kind of relationship, whether it be a friendship or a romantic endeavor, isn’t something you passively observe – but is instead something you work on and maintain. It takes time, energy, and genuine care.

25 years later and Dad’s still tearing up at dinner about how much he loves Mom. That’s pretty hard to beat. If I’m lucky enough to find even half of what the two of you have, I would count myself as blessed.

Happy 25th Anniversary Mom and Dad, sending love and laughter on your special day!

By the way, the video archive is up for yesterday’s “”Say-on-Pay Workshop” – the ‘SEC All-Stars’ panel spent a chunk of time on the more recent non-GAAP comment letter trends. You can still register to access the archives. Catch-up now!

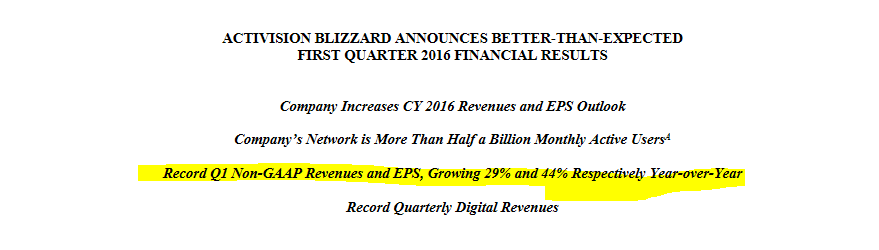

Non-GAAP: “Equal Prominence” Applies to Percentages Too…

Hat tip to Bass Berry’s Jay Knight for providing this recent Corp Fin comment to Activision Blizzard’s Q1 earnings release that reinforces that non-GAAP equal prominence rules apply to percentages also:

Form 8-K filed May 5, 2016; Exhibit 99.1

2. Your headline references “Record Q1 Non-GAAP Revenues and EPS, Growing 29% and 44% Respectively Year-over-Year” but does not provide an equally prominent descriptive characterization of the comparable GAAP measure. We also note several instances where you present a non-GAAP measure without presenting the comparable GAAP measure. This is inconsistent with Question 102.10 of the updated Compliance and Disclosure Interpretations issued on May 17, 2016 (“the updated C&DI’s”). Please review this guidance when preparing your next earnings release.

Response: We acknowledge the Staff’s comment and will review and reflect the guidance included in the updated C&DI’s when preparing our next earnings release.

John & I had a lot of fun taping our 2nd “news-like” podcast. This 8-minute podcast is about disclosure overload & the new Fall TV season. I highly encourage you to listen to these podcasts when you take a walk, commute to work, etc. And as we tape more of these, it’s inevitable we’ll figure out how to be more entertaining…

This podcast is also posted as part of our “Big Legal Minds” podcast series. Remember that these podcasts are also available on iTunes or Google Play (use the “My Podcasts” app on your iPhone and search for “Big Legal Minds”; you can subscribe to the feed so that any new podcast automatically downloads…

Today is the “Say-on-Pay Workshop: 13th Annual Executive Compensation Conference”; yesterday was the “Tackling Your 2017 Compensation Disclosures: Proxy Disclosure Conference” (video archive is now posted). Note you can still register to watch online by using your credit card and getting an ID/pw kicked out automatically to you without having to interface with our staff. Both Conferences are paired together; two Conferences for the price of one.

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take about a day to post the video archives after it’s shown live). A prominent link called “Enter Conference Here” – on the home pages of those sites – will take you directly to today’s Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: Windows Media or Flash Player). Here are the “Course Materials,” filled with 180 pages of talking points & practice pointers.

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here is today’s conference agenda; times are Central.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if that is possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see this “List: CLE Credit By State.”

Shareholder Proposals: An Influx When the Crisis Hits

In most cases, a company facing a crisis will receive more shareholder proposals than when it’s not. For example, many of the larger banks received a slew of shareholder proposals in the wake of the ’07 financial crisis. Another example is the likelihood of Wells Fargo receiving a bunch of new proposals in the wake of its $185 settlement with the CFPB – see this Reuters article about some of those proposals that the company recently received (also see this ICCR press release).

It’s wise to warn the board that they should be expecting a proposal “windfall” if a crisis hits…

Survey: How Many Shareholder Proposals Do You Think Wells Fargo Will Receive for ’17?

Please participate in this anonymous survey by guessing how many shareholder proposals will Wells Fargo receive (some of which may be withdrawn or negotiated out):

Today is the “Tackling Your 2017 Compensation Disclosures: Proxy Disclosure Conference”; tomorrow is the “Say-on-Pay Workshop: 13th Annual Executive Compensation Conference.” Note you can still register to watch online by using your credit card and getting an ID/pw kicked out automatically to you without having to interface with our staff. Both Conferences are paired together; two Conferences for the price of one.

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take about a day to post the video archives after it’s shown live). A prominent link called “Enter Conference Here” – on the home pages of those sites – will take you directly to today’s Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: Windows Media or Flash Player). Here are the “Course Materials,” filled with 180 pages of talking points & practice pointers.

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here is today’s conference agenda; times are Central.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if that is possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see this “List: CLE Credit By State.”

I couldn’t help repeating this creative haiku about the CDIs, from this blog by Gunster’s Gus Schmidt:

Question 128C.01

A “CACM”

That reasonably reflects pay

Can be utilized

Question 128C.02

Hourly pay rates

Can we use to calculate?

No! These will not work

Question 128C.03

To calculate it

You must use recent data

90-day limit

Question 128C.04

Furloughed employees?

You must include them too, but

Use annualized pay

Question 128C.05

What about ICs?

Ignore classification

If you set their pay

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Restatements Hit a New Low

– ISS’ “2016 Board Practices Study”

– Is Tracking Stock Making a Comeback?

– Audit Report Transparency: Netherlands Trumps US – Hands Down

– Omnicare Applied to Audit Reports

Yesterday, as noted in this Cooley blog, Corp Fin issued one new – and two revised – CDIs dealing with Rule 701 as well as the Rule 144(d) holding period. The 701 CDIs are:

This recent Equilar blog has a nifty chart about the relative trends among industries to have “financial experts” on the audit committee. Interesting, the blog notes that S&P 500 companies had a median of two financial experts in ’15 (with 27% composed solely of financial experts) – up about a third since ’11. Learn more about this topic in our “Audit Committee Disclosure Handbook“…

SOX Compliance Costs & Audit Fees: Continue to Rise

Here’s something from Dan Goelzer of Baker & McKenzie:

Recently, consulting firm Protiviti released its “2016 Survey of Sarbanes-Oxley Act Compliance Costs.” As in its 2015 and 2014 surveys, Protiviti found that, for many companies, costs associated with SOX compliance continue to rise. And, similar to prior years, significant numbers of respondents point to the PCAOB’s inspection program as the cause of these cost increases.

Survey Highlights

– Internal compliance costs – The average annual internal cost of SOX compliance for the largest public companies (large accelerated filers) was $1.335 million. For the next tier of public companies (accelerated filers), average annual internal costs averaged $914,000, while still smaller companies (non-accelerated filers) averaged $1.219 million. The highest costs were incurred by emerging growth companies –smaller, recently-public companies – at $1.430 million. On an industry basis, healthcare payers had the highest internal SOX compliance costs ($2.31 million), while media companies had the lowest ($856,000).

– External audit fees – Half of large accelerated filers reported that their external audit fee increased in fiscal 2015, while 8 percent reported a decrease, and 42 percent said the fee remained the same. For non-accelerated filers, 41 percent reported an increase, and 52 percent reported a decrease.

– External auditor reliance on the work of others – High percentages of companies of all sizes reported that their external auditor was relying “to the fullest extent possible” on the work of others (e.g., internal audit) for the testing of controls over medium- and low-risk processes. For example, 81 percent of accelerated filers indicated that this was the case, as did 95 percent of non-accelerated filers.

– Number of entity-level and process-level SOX controls – The average number of entity-level controls reported by survey respondents was 50, of which 60 percent were classified as “key.” The average number of process-level controls reported was 96, of which 63 percent were deemed key.

– Changes in SOX compliance – The compliance area in which the highest percentage of respondents reported “extensive/substantial” change in 2016 was process control documentation for high-risk processes. In addition, 26 percent of respondents reported extensive/substantial increases in the testing of controls over management judgments and estimates.

– Cybersecurity disclosure impact – One-fifth of respondents stated that their company made a cybersecurity disclosure in fiscal 2015, in accordance with the SEC’s staff’s guidance on disclosure obligations relating to cybersecurity risks and cyber incidents. The significance of this figure is tempered by the fact that 42 percent of respondents didn’t know whether or not such a disclosure had been made. Of those who reported a cybersecurity disclosure, 47 percent said that total hours devoted to Sarbanes-Oxley compliance increased 11 percent or more as a result.

Role of the PCAOB

As was reported in last year’s survey, many respondents blame increases in their Sarbanes-Oxley compliance costs on the activities of the PCAOB. Of those respondents who said that their audit firm required changes to the company’s Sarbanes-Oxley compliance procedures in 2015, 44 percent attributed those changes to the PCAOB’s inspection program. Across all respondents, significant percentages thought that PCAOB inspection reports had an effect on the organization’s Sarbanes-Oxley compliance costs in specific areas. For example, 50 percent thought that the PCAOB’s inspections reports had an extensive/substantial impact on the costs of testing reports and other information generated by the company’s systems; 46 percent thought that the PCAOB had caused increases in the testing of review controls.

The compliance cost impact of the PCAOB’s new related party auditing standard also seems to have been significant. Fifty-eight percent of respondents reported that the company was required to update its documentation to identify related parties as a result of Auditing Standard No. 18 (ASC 2410, which governs the auditing of related party transactions). This documentation updating increased total Sarbanes-Oxley compliance hours by an average of 8 percent.

Not surprisingly in light of the cost impact that respondents thought the PCAOB was having, 75 percent of public company respondents reported that someone in the company was “keeping abreast of guidance on PCAOB inspections issued by the PCAOB.”

Role of the Audit Committee

Protiviti also asked who in the organization had primary responsibility for “executive sponsorship” of Sarbanes-Oxley compliance and who had primary responsibility for “execution.” As to executive sponsorship, 46 percent indicated that the audit committee was the sponsor, while 39 percent identified executive management. These numbers reflect a surprising shift to audit committee responsibility during the past 12 months. In the 2015, only 25 percent pointed to the audit committee as the executive sponsor. With respect to execution responsibility for Sarbanes-Oxley compliance, 14 percent of respondents identified the audit committee in 2016, compared to only 2 percent last year.

Comment: Audit committees may have opportunities to consider whether there are ways to convert some of their company’s SOX compliance costs into an investment in more effective and efficient financial reporting and information gathering processes. Sixty-seven percent of public company respondents believe that the company’s internal control over financial reporting has “significantly/moderately improved” since ICFR auditing was required.

Broken down by size, majorities of companies with revenues over $5 billion and under $500 million agreed with that statement. The survey results indicate that large companies have done better than midsize companies at generating value from SOX compliance. In Protiviti’s view “SOX compliance requires a significant investment for many organizations in terms of budget and hours. But the results reflected [in the 2016 survey] * * * reinforce the reasons these investments are needed and the value they create.”

Yesterday, the SEC posted a Sunshine Act notice for an open Commission meeting to propose universal proxy ballots next Wednesday, October 26th. This controversial rulemaking has been in the works for years, with the House of Representatives going so far to vote a few months ago to stop the rulemaking. Check out this piece on page 5 of the November-December 2014 issue of the Deal Lawyers print newsletter entitled “The Quest for Universal Ballots: Might Boards Benefit Too?”…

In addition, the SEC will vote to adopt rules to facilitate intrastate & regional offerings (amendments to Rule 147 & 504) – and to repeal Rule 505 of Regulation D…

How is Morale at the SEC? A 2016 Job Satisfaction Survey

Here’s the SEC’s “2016 Federal Employee Viewpoint Survey.” You can see how the various Divisions & Offices within the SEC compare to each other, as well as how the responses compare to a government wide ratio. The overall number of responses is pretty high, over 3200 Staffers. Compare the results to the 2014 survey…

“Material Plan Amendment” When You Increase Tax Withholding Rate? Nasdaq’s New FAQ

Yesterday, the Nasdaq posted this new FAQ #1269 regarding shareholder approval of plans (also see this Mike Melbinger blog about it):

Question: Is an amendment to an equity compensation plan to increase the withholding rate to satisfy tax obligations, such as from the minimum tax rate to the maximum tax rate, considered a material amendment?

Answer: Generally, an amendment to increase the withholding rate to satisfy tax obligations would not be considered a material amendment to an equity compensation plan. Allowing the holder of an award to surrender unissued shares to pay tax withholdings is similar to settling the award in cash at market price, and neither creates a material increase in benefits to participants nor increases the number of shares to be issued under the plan.

This type of change also is not an expansion in the types of awards provided under the plan. This analysis is the same regardless of whether the plan allows the shares surrendered for tax withholdings to be added back to the pool of shares available for issuance as future awards. Accordingly, an amendment to an equity compensation plan to increase the withholding rate to satisfy tax obligations would not be considered a material amendment to the plan.

Just in time for our “Proxy Disclosure Conference” coming up on Monday – in Houston & by video webconference – Corp Fin issued these 5 CDIs on Item 402(u) yesterday (we’re posting memos in our “Pay Ratio” Practice Area on CompensationStandards.com):

Evaluating these Compliance & Disclosure Interpretations will be among the many “pay ratio” discussions taking place over 20-plus panels. Register now!

Transcript: “Board Refreshment & Recruitment”

We have posted the transcript for our recent webcast: “Board Refreshment & Recruitment” – which tackled board diversity disclosure & more!

Should Say-on-Pay Votes Be Binding?

Here’s an excerpt from this blog – “Should Say-on-Pay Votes Be Binding?” – by two Canadians about the effectiveness of non-binding say-on-pay votes (I’ve recently blogged about binding SOP heading perhaps to the UK):

Some findings reveal disturbing and unintended consequences. For instance, studies suggest that shareholders base their votes on the performance of a company’s stock rather than on an analysis of the firm’s compensation policies and practices. If company shares do better than those of its peers, almost any compensation package will be approved. This perverse result tends to increase the pressure on management to focus on short-term stock performance, sometimes through decisions that may negatively affect future performance.

This is not surprising, though. It has become far harder to read and understand the particulars of executive compensation. Indeed, for the 50 largest (by market cap) companies on the Toronto Stock Exchange in 2015 that were also listed back in 2000, the median number of pages needed to describe their executives’ compensation rose from six in 2000 to 34 in 2015, with some compensation descriptions consuming as many as 66 pages. Investors holding shares in hundreds of different firms face a formidable task. The simplest approach is to vote according to the stock’s performance or, more likely, to rely on the recommendations of proxy advisory firms, which also base their “advice” in part on relative stock market performance.

Thus, 66 percent of corporate directors do not agree that say-on-pay resulted in a “right-sizing” of CEO compensation. Yet 83 percent of directors very much agree or somewhat agree that say-on-pay increased the influence of proxy advisors, according to a 2016 PwC and Cleary Gottlieb survey: Boards, shareholders, and executive pay.