Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

Recently, I blogged about a study that tracks whether mutual funds & proxy advisors are reading your proxy online. I threw in an aside that “If I was an institutional investor, I would still be asking for paper as that seems like a far easier way to actually read a proxy.” It might be easier to read a proxy if you did a straight read – but the reality is that investors drill down into the areas that they are most interested in.

In other words, investors typically read proxies electronically. They like the ability to word search. They like the ability to quickly move around. In fact, they like it when you provide links in your “executive summary” of the proxy to more detailed discussions. Karla Bos of Aon provides even more wisdom:

1. Another big reason that investors use electronic proxies (aside from sheer volume) – governance teams often cut & paste sections of the proxy into emails or other materials for their portfolio managers & proxy committees

2. Investors want links from the table of contents (no links there often means the rest of the proxy and perhaps the company’s governance are “old school” — first impressions count)

3. When investors analyze your proposals, before going to your proxy, many rely on proxy advisor reports or data feeds (for the facts, not their recommendations), so remember that if investors can’t quickly find what they need, the proxy advisors may not either

4. On word searches – ensuring your investors can quickly find what they want means you have to know them and the terms & content they’re looking for

5. I like how GE uses internal links – and even includes an index of frequently requested information right up front. But proxies don’t have to have all the bells & whistles that GE’s does to make navigation more shareholder friendly.

So there you have it, several more “pro tips” to learn from this blog. And yes, I was wrong. And you were right…

Revenue Recognition: Corp Fin Comments Begin

Just yesterday, I blogged that Corp Fin planned a lighter touch when issuing comments on the new revenue recognition standard – and now Steve Quinlivan has blogged about how the comments have begun rolling in…

Big Four Audit Quality Review Results Decline

As the Big Four appear to continue to push back against the PCAOB regulating them here in the US (the PCAOB’s budget was cut in December & much of the senior staff has been let go since), here is sobering news from the UK’s Financial Reporting Council:

The Big Four audit practices must act swiftly to reverse the decline in this year’s audit inspection results if they are to achieve the targets for audit quality set by the Financial Reporting Council (FRC). Overall results from the most recent inspections of eight firms by the FRC show that in 2017/18 72% of audits required no more than limited improvements compared with 78% in 2016/17. Among FTSE 350 company audits, 73% required no more than limited improvements against 81% in the prior year.

Across the Big 4, the fall in quality is due to a number of factors, including a failure to challenge management and show appropriate scepticism across their audits, poorer results for audits of banks. There has been an unacceptable deterioration in quality at one firm, KPMG. 50% of KPMG’s FTSE 350 audits required more than just limited improvements, compared to 35% in the previous year. As a result, KPMG will be subject to increased scrutiny by the FRC.

Meanwhile, two editorial pieces – this one by the financial editor of the Times and this one by a senior editor at Bloomberg – has suggested that the Big 4 might need to be broken up…

This nice blog from Cooley’s Cydney Posner offers a bunch of interesting nuggets from an interview with SEC Chair Jay Clayton and Corp Fin Director Bill Hinman at a recent WSJ event. Here are the highlights:

1. Corp Fin’s Approach to Revenue Recognition Comments – Hinman reportedly said that the staff understands that the rule is complex to apply and is focused on helping issuers comply; the staff doesn’t “have a particular agenda or standard comments…We don’t expect to repeat the same comment for five different companies.” He contrasted the staff’s approach to revenue recognition with its approach to compliance with the SEC’s guidance on non-GAAP financial measures or compliance with GAAP, where the staff would often issue standard comment letters.

2. Talk to Staff for Reg S-X 3-13 Waivers – Hinman reportedly advised issuers to skip the 30-page treatises; first talk with the staff.

3. Mandatory Auditor Rotation Not Priority – Although some European regs require mandatory auditor rotation every 10 years, Clayton also noted that “mandatory rotation of company auditors ‘is not something that is front and center in my mind.’”

4. Fine-Tuning Dodd-Frank; Not Overhauling It – Clayton, speaking at the annual meeting of the WSJ’s CFO Network, said that “regulators are evaluating how postcrisis rules have performed in practice, and that he had concerns about some of the unintended side effects from some regulations. But any changes will be around the edges, keeping the core of postcrisis overhauls in place, he added. ‘I don’t think Dodd-Frank is changing a great deal, just to put a pin in it.’

Corp Fin Director Hinman Talks Cybersecurity Disclosures

Bill Hinman, director of the SEC’s Division of Corporation Finance, said the staff is looking closely at companies’ risk disclosure surrounding cybersecurity in this year’s filings following the update to the SEC’s cyber guidance that was issued in February. At the PCAOB’s recent Standing Advisory Group meeting, he noted that some aspects of the guidance have been controversial, so he explained some of the Commission’s thinking behind the guidance.

Hinman said that the staff wanted to focus the guidance on a few areas to which it wanted to draw more attention. The first area was internal controls and how companies were designing internal controls so that when a cyber incident occurs, there were the right procedures in place to escalate the issue.

Companies should not just have IT personnel looking at cyber risks anymore, he said. The issues now should be brought to the attention of disclosure experts at the company, as well as the general counsel. Hinman said the staff wanted to remind companies that they should have procedures in place that would cause escalation to occur, so it was added to the guidance.

May-June Issue of “The Corporate Executive”

We recently mailed the May-June issue of “The Corporate Executive” – and it includes articles on:

– Court Decisions Breathe New Life into Lawsuits over Directors’ Compensation—And What You Need to Do about It

– Understanding the New Qualified Equity Grant Deferrals

– Elon Musk’s Mega Grant

– Rule 701 Disclosure Threshold Finally Increased

Last week, Corp Fin Director Bill Hinman delivered this speech on digital assets as “securities” – which caused a stir. Here’s an excerpt from this Debevoise & Plimpton memo about it (also see this WSJ article):

Certain digital assets are not, today, securities. Director Hinman expressly noted during the speech that the virtual currencies Bitcoin and Ether, as offered and sold today, are not securities. This is the first time that an SEC official has publicly indicated that a virtual currency, other than Bitcoin, does not constitute a security and, importantly with respect to Ether, notwithstanding a history of fundraising that accompanied its creation. Underlying his view is the fact that applying the disclosure regime of the U.S. federal securities laws to current transactions in these virtual currencies would add little value because the underlying software platforms are sufficiency decentralized and sufficiently functional. In other words, there is no informational asymmetry between founder/sponsor/promoter, on the one hand, and investors, on the other, that puts investors at risk.

Other digital assets may not, today, be securities. Director Hinman covered three additional points during the speech that may help to bring additional virtual currencies and other digital assets out of the regulatory “shadows.” First, he allowed that there may be other sufficiently decentralized networks and systems where regulating the tokens or coins that function on them as securities may not be required. Second, he made clear his view that “whether something is a security is not static and does not strictly inhere to the instrument.” Consistent with relevant case law and the SEC’s long-stated views, the economic substance of the transaction in question always determines the legal analysis, and this cuts both ways:

– A digital asset that was originally distributed in a securities offering may later be sold in a manner that does not constitute an offering of a security; and

– Digital assets with utility that function solely as a means of exchange over a decentralized network could be packaged and sold as an investment strategy that can be a security.

Finally, Director Hinman laid out a framework containing two sets of non-exclusive factors that the SEC considers in assessing whether a digital asset is offered as an investment contract and is thus a security. The critical underpinnings of the Hinman Factors are: (i) the role that a third party, whether a person, entity or coordinated group of actors, plays in driving an expectation of an investment return and (ii) whether the economic substance of the transaction indicates that the digital asset truly functions more like a consumer item and less like a security.

As an aside, here’s something wild: The best “wallets” for cryptocurrency are glorified USB drives. So since the exchanges aren’t secure, the traders download their “keys” to the drive every night and lock it in a safe. Blockchain! So easy! And then there’s this guy’s story – forgot his pin, tried a bunch of stuff to recall it (including hypnosis) and then paid someone almost $4k to hack the drive…

More on “First Universal Proxy Card!”

Last week, Liz blogged about the first US-incorporated company to use a universal proxy card – and as an aside, she mused about whether this was a strategy by Sandridge Energy. A member responded with these thoughts:

I suppose a key element of the strategy could involve the grant of discretionary authority to the proxies appointed on the universal card. Specifically, even shareholders wishing to support (partially or fully) the Icahn group will appoint management proxies to vote in their discretion on such other business as may properly come before the meeting or any adjournment or postponement thereof.

I am not certain, but suspect, that if a card were returned with fewer than seven “for” votes in the election of directors, the proxies also would be able to vote in accordance with the board’s recommendation. Thus, if the shareholder cast five votes in favor of Icahn nominees (and cast no votes for any of the Company nominees), the proxies likely can cast two votes in favor of two Company nominees. If correct, there could be controversy because the proxies might be able to distribute those votes in a way to knock out one or more Icahn nominees. Interesting stuff.

HBO’s “Succession”: Duty to Disclose CEO’s Illness

Spoiler alert! The title of this blog already gave away the end of the first episode of HBO’s new show – “Succession.” Sorry about that. Anyway, I thought I would turn off “Succession” about five minutes into the first episode given that we already hear too much about powerful, white, rich families. But I have found it interesting.

For starters, it’s close to home in that I work for a family-owned company that has successfully lived through a recent transition in senior management (Jesse Brill has turned over running the company to his son, Nathan). Then, I am in the midst of my own long-term succession planning as I train Liz about the facets of this job (John isn’t the heir apparent – he & I are the same age).

More importantly, the show grapples with issues that arise for many of you reading this blog. The show’s family-owned business is a publicly-held media empire (but supposedly not based on the Murdochs). As the title of the show suggests, the main premise of the show is about how to handle CEO succession planning. And Episode 2 mainly deals with the duty to disclose a CEO’s illness.

In Episode 2, several characters discuss the CEO’s illness & whether investors should be told. Some of the statements are inaccurate of course. It’s a tricky topic. The most inaccurate statement is that the SEC has a rule compelling disclosure of a CEO’s illness (ie. an affirmative duty to disclose). There is a more accurate statement about the NYSE having a standard that requires disclosure of the CEO’s illness (it’s clearly material in this case). And then there are multiple references to Steve Jobs – as Apple’s decision to be mum about Steve’s health is held up as precedent as part of the argument to do the same in the show.

Here are my three main blogs on the securities law aspects of this topic:

For quite some time, there has been a movement away from quarterly earnings guidance – and maybe towards foregoing quarterly reporting altogether (for example, see this blog from a few years back) – and John recently ran a blog entitled “Should We Lose the 10-Qs?”

Now, the Business Roundtable (BRT) (press release), the National Association of Corporate Directors (NACD) (press release) and the National Investor Relations Institute (NIRI) (press release) have joined the chorus – calling for an end to short-termism by eliminating quarterly earnings guidance. Also see this op-ed by Jamie Dimon and Warren Buffett supporting this view.

Insiders Selling More After Buyback Announcements?

In a recent speech, SEC Commissioner Robert Jackson called for rule changes to discourage insider sales during buybacks. Commissioner Jackson believes the Rule 10b-18 safe harbor – which protects companies from fraud liability if a share repurchase meets certain conditions – shouldn’t be available if the company allows executives to sell stock during a buyback. Here’s an excerpt from this WSJ article (also see this Cooley blog and Wachtell Lipton memo):

Insiders who sell stock into buyout bounces aren’t trading illegally, of course, and Mr. Jackson isn’t accusing them of that. And other investors also have the opportunity to take advantage of the bumps. But these price surges can be especially beneficial to corporate executives holding large chunks of corporate stock looking for an uptick to unload shares. “The SEC gives an exemption from market-manipulation rules to companies doing a buyback,” Mr. Jackson said in an interview. “The SEC shouldn’t be making it easier for executives to use them to cash out.”

Mr. Jackson, a former law professor, examined stock trades at 385 companies that announced buybacks in 2017 through this year’s first quarter. He found the percentage of insiders selling shares more than doubled immediately following their companies’ buyback announcements as many of the stocks popped. Daily stock sales by the insiders rose from an average of $100,000 before the buyback announcements to $500,000 after them. The sellers received proceeds totaling $75 million more than had they sold before the announcement, the study concluded. At 32% of the companies, at least one insider sold in the first 10 days after the buyback announcement.

And this blog from Steve Quinlivan notes that Commissioner Jackson is also attuned to the potential connection between buybacks & executive pay:

Commissioner Jackson also stated his view that corporate boards and their counsel should pay closer attention to the implications of a buyback for the link between pay and performance. In particular, the company’s compensation committee should be required to carefully review the degree to which the buyback will be used as a chance for executives to turn long-term performance incentives into cash. If executives will use the buyback to cash out, the committee should be required to approve that decision and disclose to investors the reasons why it is in the company’s long-term interests, according to Commissioner Jackson.

The hilarious picture below made me want to discuss the topic of “whether it’s okay to use footnotes when you write.” My take is that it depends on the context. In my opinion:

1. They’re okay for court opinions, SEC releases and research papers when authority needs to be cited.

2. But it’s not okay to bury substantive commentary in footnotes, even in the types of documents in #1 above. If it’s important enough to include in a document, put it in the body – don’t bury it in a footnote.

3. It’s never okay for informational articles. You might notice that nearly all of our content doesn’t include footnotes. For example, authority is cited within the body of our Handbooks. And commentary that might be considered as an “aside” is mentioned as an aside within the main body of our stuff. We don’t force our readers to dig around.

The Footnote of All Time

Saw this wonderful picture on @footnoted’s Twitter feed (courtesy of @AcademiaObscura). The footnote in the picture makes fun of footnotes (click the image to enlarge it & read footnote 1 at the bottom):

Poll: The Appropriateness of Footnotes

Take a moment for this anonymous poll to indicate your feelings towards footnotes:

I was excited to get an email from the SEC last night with the title of “Technical Issue Resolved.” Figuring that the SEC was finally ready to be transparent when Edgar goes down – yes, Edgar was down again yesterday – I eagerly opened the email. It said:

A technical issue that arose during routine maintenance caused a cache of previously issues materials to be be resent. The issue has been resolved but you may receive a limited number of additional outdated emails. We regret any inconvenience to you.

In other words, the SEC is willing to be transparent when it accidentally sends out old press releases – but the agency is still not willing to address the “elephant in the room.” As I have been doing for some time (see this blog for one of many), I will continue to hammer home the importance of fixing Edgar – and also hammer home the much easier fix of just informing us when Edgar is down (and then back up)…

More on “Big Brother’ is Watching You (Reading That Proxy)”

Got a number of interesting responses to my blog a few days ago about the SEC’s Edgar logs. This one was my favorite:

In its 2008 interpretive release about ‘use of company websites,’ the SEC was adamant that companies not track visitors to IR websites, in order to maintain anonymity of site visitors – but the SEC not only captures similar information on Edgar but actually makes that information publicly available. I’m baffled by the logic.

Director Compensation: Post-Investor Bancorp Reversal World Ain’t Pretty

We are beginning to see the impact of the Delaware Supreme Court’s reversal in the Investors Bancorp case – and it is not pretty. Two companies/boards recently agreed to settle lawsuits over non-employee director compensation and the attorneys for the parties and the Chancery Court Judge acknowledged that the settlement was influenced by Investors Bancorp.

In Solak v. Barrett, the lawsuit alleged that the directors of Clovis Oncology paid themselves excessive compensation in breach of their fiduciary duties and wasted corporate assets. According to the complaint, non-employee directors received an average of $617,700 in 2015, which was more than twice the average compensation of non-employee directors in the Fortune 50. Clovis is well outside the Fortune 500.

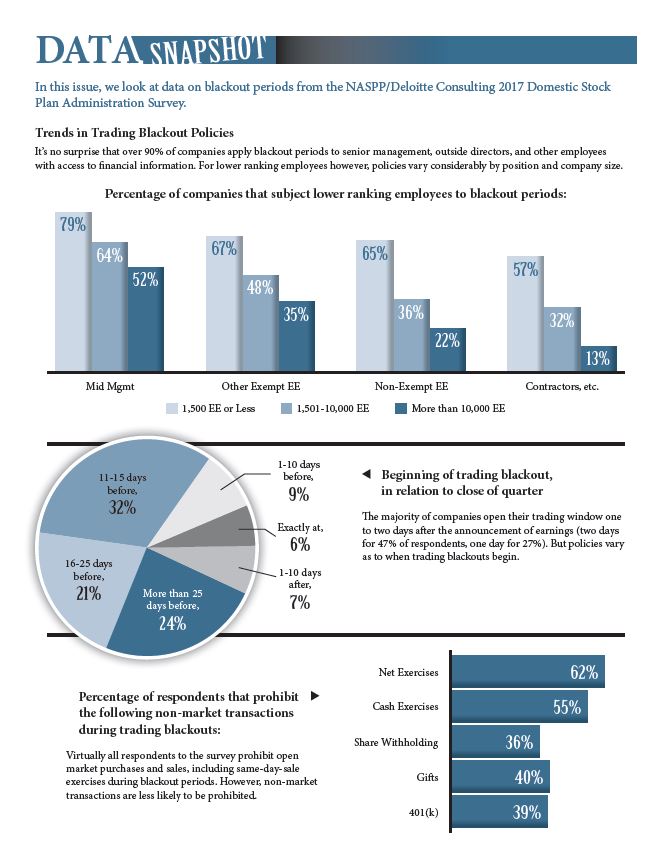

One of the areas that companies most frequently benchmark themselves is insider trading policies/blackout periods. We’ve surveyed that area over a dozen times over the past 15 years. We’re holding our semi-regular webcast about this area next month: “Insider Trading Policies & Rule 10b5-1 Plans.”

Another good source is the NASPP’s “Domestic Stock Plan Administration Survey” that it conducts every three years or so with Deloitte Consulting. Last year’s NASPP survey revealed that 100% percent of respondents to have an insider trading policy – and these other tidbits:

– 81% require officers/directors to acknowledge understanding and/or receipt of the policies of the insider trading compliance program

– 85% require insiders to pre-clear their trades

– 94% prohibit hedging

– 94% also prohibit trading in puts, calls, and similar derivatives

– 80% prohibit pledging

– In-house counsel is most commonly responsible for preparing Section 16 filings (64% of respondents), followed by stock plan administration (31%) and corporate secretary (21%). This was a ‘check-all-that-apply’ question; at some companies, multiple people might have this responsibility.

Insider Trading Policies: The Infographic

Here’s a nifty infographic from the NASPP with some of the survey stats:

Making IPOs Easier: Latest Congressional Activity

This Davis Polk blog lists all the latest attempts by Congress to pass legislation that would enable companies to go public more easily. Also see this Cooley blog about attempts by other organizations to push IPO reform…

Then there is this Kevin LaCroix blog about John Coffee’s views: “Is Over-Regulation Really the Reason There are Fewer IPOs?”…

Recently, John blogged about a Bloomberg piece that covered a study that uses Edgar’s logs – which are publicly available! – to track which SEC filings are being read by hedge funds. The upshot is that you can then infer whether a big name investor was looking into a particular company.

There also is this study that tracks whether mutual funds or proxy advisors are reading your proxy. Here’s an excerpt:

For 97 large mutual fund families and 3,706 companies over seven years, we can determine the precise times when each investor accessed each SEC filing for each company. In addition, for the three most recent calendar years within our sample, we also observe the number of times the largest proxy advisory service company, Institutional Shareholder Services (ISS), accessed each company filing.

We build our dataset using the publicly provided server log files from EDGAR. These files include partially masked internet protocol (IP) addresses, which do not reveal the full identity of the user but which are sufficiently detailed to enable a mapping to the IP address blocks held by institutional investors. Several contemporaneous papers similarly rely on this approach, including for example Chen, Cohen, Gurun, Lou, and Malloy (2017) to study investment decisions; Crane, Crotty and Umar (2018) to study hedge funds; Bozanic, Hoopes, Thornock, and Williams (2017) to study the IRS; and Gibbons, Iliev, and Kalodimos (2018) to study sell-side analysis. However, we are the first to use these data to study the governance-related fundamental research performed by key investors.

The problem is that this approach of using Edgar logs is quite limited. Folks might be accessing SEC filings posted directly on a company’s IR web page. Or in the case of proxies, posted directly on Broadridge’s platform. And of course, folks might be reading proxies in paper. If I was an institutional investor, I would still be asking for paper as that seems like a far easier way to actually read a proxy…

Corp Fin Hires an “Digital Assets & Innovation” Associate Director

As noted in this press release, Corp Fin has hired Valerie Szczepanik as an Associate Director & Senior Advisor for “Digital Assets & Innovation.” Valerie will coordinate efforts across all SEC offices regarding the application of the securities laws to emerging digital asset technologies & innovations, including ICOs and cryptocurrencies. She was hired away from the SEC’s Enforcement Division where she most recently served as an Assistant Director in their Cyber Unit…

Our “Section 16 Forums”: Only a Few Weeks Away!

In response to those doing Section 16 work who have told us that they want to network with those similarly-situated, we are holding a pair of “Section 16 Forums” in June – one on each coast. Hosted by Alan Dye, these are one-day events for all Section 16 practitioners – not just beginners.

Another overseas stock exchange has gotten into the “unilateral” listing business (here’s a blog about the older ones; here’s our “Practice Area” about this stuff). Here’s the intro from this Skadden memo about the latest:

In April 2018, the Moscow Exchange, reportedly the largest exchange in Russia, announced that it intends to admit securities of approximately 50 major U.S. and other foreign companies to public trading in the non-quotation section of the list of securities admitted to trading. The intent of this move is apparently to provide Russian investors with access to a wider range of financial instruments.

Under Russian securities laws, a Russian stock exchange can unilaterally admit foreign securities to trading without the consent of the issuer of such securities. In the last several years, the St. Petersburg Stock Exchange admitted securities of a number of foreign companies to trading in a similar fashion.

Importantly, in the event of such unilateral listing by a Russian stock exchange, responsibilities for public reporting and disclosure requirements, and associated costs, rest with the Russian stock exchange, and issuers of the relevant securities are relieved from such responsibilities and costs.

Insider Trading: Greed Kills

Whenever an i-banker is involved in an insider trading case, I’m shocked. This latest one from the SEC is no different. The dude worked at Goldman Sachs!

According to this article, in 2016, a good performing VP at a bulge bracket firm could expect to make between $375-975k per year – and you know Goldman ain’t at the low end of that. How stupid do you have to be to throw that away? And as noted in this Bloomberg article, some of his inside trades resulted in paltry returns…

1. The SEC All-Stars: A Frank Conversation

2. Parsing Pay Ratio Disclosures: Year 2

3. Section 162(m) & Tax Reform Changes

4. Pay Ratio: How to Handle PR & Employee Fallout

5. The Investors Speak

6. Navigating ISS & Glass Lewis

7. Proxy Disclosures: The In-House Perspective

8. Clawbacks: What to Do Now

9. Dealing with the Complexities of Perks

10. Disclosure for Shareholder Plan Approval

11. The SEC All-Stars: The Bleeding Edge

12. The Big Kahuna: Your Burning Questions Answered

13. Hot Topics: 50 Practical Nuggets in 60 Minutes

14. Dave & Marty: True or False?

15. Steven Clifford on “The CEO Pay Machine”

Reduced Rates – Act by June 29th: Huge changes are afoot for executive compensation practices with pay ratio disclosures on the horizon. We are doing our part to help you address all these changes – and avoid costly pitfalls – by offering a reduced rate to help you attend these critical conferences (both of the Conferences are bundled together with a single price). So register by June 29th to take advantage of the discount.

Although pay ratio didn’t seem to initially capture the imagination of journalists, there has been a wave of local reporting about the pay ratios at specific companies over the past week. Here’s some of the articles about how pay levels – particularly pay ratios – look this year, based on this season’s proxy statements (Mark Borges, Barbara Baksa & I are quoted in the first piece):

Yes, Edgar Is Still Broken (& We’re Not Being Told About It)

Sorry, but until the problem is fixed, I’m going to keep blogging about how the SEC’s Edgar continues to have problems (here’s a recent one) – and how the SEC isn’t telling us about it when it does. My hope is that by continuing to highlight the problems, the SEC will at least set up some sort of communication vehicle (a blog perhaps?) where it can inform the general public when Edgar is down (and when it’s back up). Here’s a note that I received from a member a few days ago:

Due to the volume of filings being received by the EDGAR system, the SEC confirmed that they are experiencing delays with filings disseminating. Filings are being accepted and acceptance notifications are returning. Please be assured that this is an SEC issue and the delay in posting does not alter the date/time of a live acceptance.

By the way, Edgar was having problems again this morning. You could make filings but could not access them on sec.gov…

A Tool to Propel Climate Change Disclosure

As this Davis Polk blog notes, the Financial Stability Board’s “Task Force on Climate-Related Financial Disclosure” has launched the “TCFD Knowledge Hub.” The Hub currently contains 300 different documents or other resources organized by the four thematically related areas for disclosure…

Speaking of databases, the SEC recently launched “SALI” (“SEC Action Lookup for Individuals”) so that anyone can research whether the person trying to sell them investments has a judgment or order entered against them in an enforcement action…