Now that I’ve seen both Lyft’s prospectus & Uber’s recent filing, I’ve reached the conclusion that we here at TheCorporateCounsel.net need our own mission statement. Here’s what I’ve come up with: “Our mission is to end global warming, poverty & tooth decay by publishing online and print resources for corporate and capital markets lawyers.”

Does that mission statement seem a bit unrealistic given the nature of our business? Well, I think ours is arguably more tightly tethered to reality than what either of these two high profile tech companies cab dispatchers are peddling.

Lyft says its mission is to “Improve people’s lives with the world’s best transportation,” while Uber says that “our mission is to ignite opportunity by setting the world in motion.” Both companies extensively embellish on their mission statements, with Lyft contending that it is at the forefront of a “massive societal change,” while Uber counters with a statement that it “believes deeply” in its “bold mission” and has a “massive market opportunity.”

This is heady stuff for companies with core businesses based on an app that does what Danny DeVito did in the ’80s sitcom “Taxi” & whose financials suggest that they spend a lot of time shoveling money into a furnace. Although to be fair, Uber will also deliver your Pad Thai order, and it’s . . .you know. . . sorry about the other stuff.

These messianic mission statements & the puffery that accompanies them have become a cliché in tech deals. But it seems to me that they do little to aid investors and a lot to obfuscate what companies actually do. The whole approach reminds me of nothing so much as “The Great & Powerful Oz” exhorting Dorothy to “pay no attention to the man behind the curtain” – only what’s frequently behind the curtain in tech deals is an endless string of huge losses, and a path to future profitability that is far from certain.

By the way, there’s plenty of disclosure about what’s behind the curtain in these prospectuses, if you take a moment to look for it. For instance, Uber accompanies its announcement of the new millennium with a 46-page “Risk Factors” section, while Lyft’s “Risk Factors” section is 41 pages long. So investors who get carried away with the hype have only themselves to blame. Read the prospectus.

Regulation G: Coming to a CD&A Near You?

SEC Commissioner Robert Jackson recently co-authored a WSJ opinion piece calling for increased transparency about the use of non-GAAP numbers in setting executive pay. The article notes that Reg G generally requires companies to provide comparable GAAP information & a reconciliation, but acknowledges that this doesn’t apply to the CD&A discussion. The authors think it should:

Unfortunately, those requirements do not apply to the reports that compensation committees of corporate boards disclose to investors each year. Thus, committees choosing to use adjustments when deciding on payouts need not explain why an adjusted version of earnings is the right way to determine incentive pay for the company’s top managers. This increases the risk that adjustments will be used to justify windfalls to underperforming managers.

The SEC’s disclosure rules have not kept pace with changes in compensation practices, so investors cannot easily distinguish between high pay based on good performance and bloated pay justified by accounting gimmicks. That’s why we’re calling on the SEC to require companies to explain why non-GAAP measures are driving compensation decisions—and quantify any differences between adjusted criteria and GAAP. A few public companies already provide investors with this kind of transparency. Others can too.

Transcript: “The Top Compensation Consultants Speak”

We have posted the transcript for the recent CompensationStandards.com webcast: “The Top Compensation Consultants Speak.”

Last week the market inched closer to peak “Unicorn” frenzy when – after what felt like a decade of speculation – Uber filed the Form S-1 for its IPO. Reuters reported that it’s seeking to raise $10 billion, which would be the largest offering since Alibaba went public in 2014. John will give his take on the prospectus tomorrow. For today, we’re looking back on IPO trends leading up to this enormous deal.

As Proskaur’s 6th Annual IPO Study shows, Uber’s IPO would build on trends from last year. Nearly half of the 94 IPOs in the study were conducted by companies with a market cap of at least $1 billion – with many of those deals coming from tech & health care behemoths. The 168-page study looks at a subset of IPOs that had an initial base price of $50 million or more. It offers all kinds of data points – and analyzes trends over the last six years. Here’s a few takeaways (also see this “D&O Diary” blog and Proskauer’s press release):

– 46% of analyzed deals were in the $100-250 million range, 48% of companies had a $1 billion+ market cap at pricing, 86% were EGCs

– 82% of IPOs priced in or above range, and the over-allotment was at least partially exercised in 77% of deals

– 99% of companies used the confidential submission process

– Average number of days from initial filing to pricing was 139, up slightly from the year before

– Average number of first-round SEC comments was down to 20 – and the study looks at the prevalence of “hot-button” comment topics, comments by sector, etc.

– 26% of companies included “flash results” for a recently-completed period – that number jumped to 50% for companies that priced within 45 days of quarter-end

– 47% of companies issued stock in a private placement within a year of going public

– 46% of companies disclosed a material weakness and 22% had a going concern qualification

– 15% of companies had multiple classes of stock – mostly in the tech sector – and 92% had a classified board

– 88% of US IPO issuers were incorporated in Delaware, 16% of IPOs came from Chinese companies

Unicorn IPOs: The More The Merrier

With companies staying private much longer these days than they did even five years ago, there’s a lot of pent up demand for “Unicorns” – venture capital-backed companies valued at $1 billion or more before going public (in Uber’s case, 90-100x more). The reason investors are itching to buy stock is because the companies are considered “high growth.” That’s bank-speak for “losing money” – one study even showed that the less profitable unicorns are, the more people like them! And that’s just one way these offerings can differ from those conducted by “regular” companies.

This “Unicorn IPO Report” from Intelligize takes a look at last year’s trends in this space, concluding that these “wild & independent creatures” actually demonstrate a “herd mentality” on some data points – not just on pricing, which is something that’s been written about a lot in the last few weeks & months – but also on things like (lack of) board diversity and the speed of their IPO process. Here are a few takeaways from this Mayer Brown blog (also see Intelligize’s press release):

– There were 20 unicorn IPOs last year, compared to 13 the year before

– A 7% underwriting fee remained the norm – despite concerns of an SEC Commissioner and legislators that smaller and medium-sized companies are paying higher fees

– About 30% of unicorns had multi-class share structures

– Other than Dropbox, all 2018 unicorns went public as EGCs – and took advantage of those scaled disclosure accommodations

– Excluding one outlier, the average time from draft registration statement filing to IPO was 132 days (shortest was 61 days) – about 140 days was spent between filing the draft and the Form S-1, with 28 days from S-1 to effectiveness (for the broader market, the average time from filing the S-1 to trading was 49 days)

Audit Committees: Auditor Assessment Template

Is your audit committee asking the right questions when it reengages your independent auditor each year? As detailed in this Cooley blog, the CAQ recently announced an updated version of its “External Auditor Assessment Tool” – with sample questions that are organized by category:

– Quality of services and sufficiency of resources provided by the engagement team

– Quality of services and sufficiency of resources provided by the audit firm;

– Communication and interaction with the external auditor; and

– Auditor independence, objectivity, and professional skepticism

The tool also includes a sample form and rating scale for obtaining input from company personnel about the external auditor, as well as resources for additional reading.

Here’s something I blogged yesterday on CompensationStandards.com: When the SEC adopted the pay ratio rule four years ago, it repeatedly stressed that company-to-company comparisons would be meaningless. The adopting release said:

As we noted in the Proposing Release, we do not believe that precise conformity or comparability of the pay ratio across companies is necessarily achievable given the variety of factors that could cause the ratio to differ. Factors that could cause pay ratio to differ from one company to the next include differences in business type, variations in the way the workforces are organized to accomplish similar tasks, differences in the geographical distribution of employees, reliance on outsourced workers, and the variations in methodology for calculating the median worker. Consequently, we believe the primary benefit of the pay ratio disclosure is to provide shareholders with a company-specific metric that they can use to evaluate the PEO’s compensation within the context of their company.

That message stuck: most people seemed to understand that the ratio would be company-specific, and there was a pretty “ho-hum” reaction to the first year of pay ratio disclosure. But, you might say, “What about tracking changes to a particular company’s ratio over time, to monitor how CEO pay increases compare to everyone else’s? Won’t that be useful?” More than a few people predict that pay ratio will garner more attention going forward, because shareholders & others will compare a company’s current year number to prior years.

The problem with that, as this WSJ article points out, is that the same factors that make comparisons among different companies meaningless are also things that can change from one year to the next at a single company. And as I’m sure you can guess, those changes cause big swings in the ratio. So for many companies, pay ratio doesn’t even provide meaningful year-over-year info (at least, about the relationship between CEO & employee pay). Here’s a couple of examples from the article:

Median pay at Jefferies Financial jumped to $150,000 last year from $44,584 in 2017 after the holding company sold most of its stake in its National Beef meat-processing unit in June 2018, cutting its workforce to about 4,600 from 12,600. The 2017 median employee at the company, formerly called Leucadia National, was an hourly line worker at National Beef, while last year’s was a senior research associate in the company’s Jefferies LLC financial-services operation.

Coca-Cola slashed its median pay figure by two-thirds after it finished shifting North American bottling operations to franchisees and acquired a controlling interest in African operations. The 2017 median worker was an hourly full-timer in the U.S. making $47,312, while last year’s made $16,440 as an hourly full-timer in South Africa. In its proxy statement, Coca-Cola said it intends to shed the African operation again after making improvements and offered an alternative median employee excluding that unit: an hourly full-timer in the U.S. making $35,878, about 25% less than his or her 2017 counterpart.

I will say, companies are making the most of what they have to work with (thanks in large part to the flexibility the SEC incorporated into the rule). And for better or worse, the “median employee” data point might illustrate to people how company policies & strategies play out in the workforce. But a single data point can’t tell the whole story – and the pay ratio itself remains pretty useless.

Internal Auditors Worry Boards Aren’t Using Them Enough

This survey of chief audit executives & directors, compiled by the Institute of Internal Auditors, suggests that enhancing internal audit’s role could help directors identify & mitigate emerging risks. Here’s a few of their recommendations (also see this and this CFO.com article and this Cooley blog):

– While cyber and IT issues have grown to represent nearly 20% of the average audit plan, CAOs still think there’s a shortage in the resources and skills that would allow them to protect the company from significant cyber incidents. Audit committees should ask about obstacles to internal audit’s performance in this area.

– At about 60% of companies, internal audit either never reviews board materials, or does so only for unusual situations. Copying the CAO on board materials would allow them to provide negative assurance on its accuracy, completeness, timeliness, transparency, and reliability. According to this WSJ article, the lack of corroboration worries auditors, who feel that audit committees aren’t exercising “professional skepticism,” and aren’t ensuring that necessary controls are in place.

– Organizational monitoring of third-party relationships is viewed by nearly half of CAOs as ad hoc or weak. CAOs must elevate concerns about weak controls on third-party risks to the audit committee. These relationships require the same level of risk management as any that affect the organization directly.

– 75% of CAOs report to the CFO – which is concerning because they may focus disproportionately on financial risks and overlook areas such as reputational & cyber risk. Internal audit can take on a greater role in oversight of emerging risks by monitoring “key risk indicators” for the company.

– Variances in audit committee structure and responsibility create the real possibility that in some organizations internal audit is not involved with committees that handle critical issues, such as cybersecurity and overall risk governance. For example, in many organizations, risk and IT committees, not audit committees, are tasked with overseeing cybersecurity and cyber preparedness. Such conditions could handicap internal audit’s ability to deliver perspectives about those vital risk domains. CAOs should be present and able to share information at these committee meetings.

“Changes in Accounting Estimates” Linked to Low-Quality Financial Reporting

Accounting isn’t as “black & white” as people sometimes think. This Audit Analytics blog highlights the tendency for people to overlook the significant judgment calls that are involved in financial reporting – and it takes a look at what it can mean when those judgments change. Here’s an excerpt:

Changes in Accounting Estimates (CAEs) are a normal part of periodic reviews of both current and future benefits and obligations. These estimates are recorded as new information appears. From an accounting perspective, the disclosure is governed by ASC 250, which requires all material changes in estimates to be disclosed.

The PCAOB proposed amendments to ASC 250 a couple of years ago, because it views this area as one of the riskiest parts of an audit. The blog walks through three studies that lend support to the PCAOB’s belief – and encourages auditors to be very skeptical of CAEs. Here’s the conclusion:

All three working papers found evidence that CAEs can lead to lower quality of financial reporting. Whether it may be from opinion shopping, managerial opportunism or an unintentional misstatement, these CAEs have been positively associated to subsequent restatements. This can lead to poorer financial quality which, in turn, can impede the assessment of earnings quality making it harder to accurately assess a company’s performance.

It was twenty years ago today

Sgt. Pepper taught the band to play

They’ve been going in and out of style

But they’re guaranteed to raise a smile

So may I introduce to you

The act you’ve known for all these years

Sgt. Pepper’s Lonely Hearts Club Band

Can’t believe it’s been twenty years since I last left the SEC as a Staffer. At the time, I was working for a SEC Commissioner. So my “going away” party was held in the SEC’s “Closed Commission Room.” That’s the room where the Commissioners meet to discuss & vote upon the agency’s enforcement actions. Very cool.

That party was quite different than when I left the SEC after my first tour of duty – that one was morning juice & coffee for the dozen or so people in my “branch.” Both types of parties were beautiful in their own way. Anyway, I thought I would excerpt a blurb from this blog about why working at the SEC is such a special experience:

Although some aspects of each ‘going-away’ party at the SEC varies depending on the circumstances, the constant is that a supervisor(s) makes some kind remarks – and then the person leaving speaks. That alone is quite powerful and something that I haven’t experienced at my numerous other jobs during my career. These are not big drinking events. In fact, they traditionally are done on the SEC’s premises at the end of the workday and they end by 6 pm. So they are short & simple – they are a stark reminder that everyone that works at the SEC is on the same team…

Always Have a Vacation on the Calendar

Thought I would borrow the title from my blog yesterday on “Broc Tales” to note that I’m starting a 5-week sabbatical this Monday – completely unplugged. Starts to make up for all the missed vacations over the years to my dear wife…

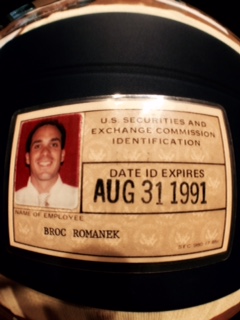

SEC IDs: Old School Style

Just found my SEC ID from my 1st tour of duty at the SEC back in the late ’80s:

We’ve blogged about how some companies have adopted a “Rooney Rule” in an effort to improve board diversity. Now, it might be easier to include diverse candidates for vacancies – because Heidrick & Struggles has announced that each year, half of their cumulative slate of board candidates presented to clients will be diverse.

Heidrick has reason to be confident they’ll meet that goal. In 2018, 52% of their North American board placements were diverse candidates. Hopefully, starting with change at the beginning of the recruitment process will result in real change – but the proof is in the pudding…

This WaPo article reports on Goldman Sachs’ efforts to improve gender diversity for both entry level & senior employee positions, which came about because the bank wants to improve its gender pay ratio (which is required to be reported in Britain).

Board Diversity: Illinois Considering Quotas

Recently, the Illinois House of Representatives passed “House Bill 3394” – which would amend the state’s Business Corporation Act to require public companies headquartered in the “Land of Lincoln” to have at least one female director and one African-American director on their boards by the end of next year. Companies that don’t comply would face fines of $100,000 (first-time offenders) or $300,000 (repeat offenders).

After a heated debate, the bill advanced to the Illinois Senate by a vote of 61-27. If it becomes law, companies can increase the size of their boards to comply. Illinois is home to some pretty well-known companies – e.g. Walgreens, Boeing, McDonald’s, Archer Daniels Midland – but I’m guessing that smaller companies will be more affected. UCLA’s Stephen Bainbridge is among those criticizing the bill. But there’s a reputational risk for companies that challenge the low bar that the legislation would establish.

Board Diversity Mandates: What’s the Impact?

It was pretty big news when California passed its board gender diversity law last year. And Illinois isn’t the only state that’s considering similar legislation. Earlier this year, Broc blogged about a bill in New Jersey, and this Bloomberg article reports on proposed legislation in Massachusetts and non-binding guidelines in other states. But if these types of statutes catch on in the US, how much will they move the needle? This Cooley blog analyzes Bloomberg’s findings – here’s an excerpt:

The Bloomberg analysis showed that the new law could mean that 692 more board seats open up for women. In addition, reports Bloomberg, if every state were to adopt a comparable law, “U.S. companies in the Russell 3000 would need to open up 3,732 board seats for women within a few years.” Meaning the number of women on boards nationwide would rise by almost 75 percent.

Currently, among the Russell 3000, men hold 21,424 board seats, while women hold 5,088 seats. And 99 percent of boards are majority male. Board seats are often filled by current or retired executives, who are most often men. In addition, when director slots open, they are often filled through personal connections, likewise most often male. Those are just two of the reasons why women make up only one-fifth of U.S. board directors.

As Bloomberg reports, without some kind of change, “it could take another two generations before the boardroom matches the workforce, which is about half female. The glacial rate of progress inspired the California law, which had wide support in the state legislature.” And, as discussed in this article in the WSJ, companies will need to “revamp the way they recruit female directors.” According to the chair of the NACD, the “‘system produces white male candidates unless board leaders deliberately do something different.’”

Beginning next year, CalPERS will likely vote “against” compensation committee members in the same year that the compensation plan fails its pay-for-performance quantitative model. That’s according to recommendations in a recent staff report to the pension fund’s Investment Committee. Here’s more detail on the executive compensation initiative that’s underway:

– Move from a 3-year to a 5-year quantitative model (developed in collaboration with Equilar) to assess pay-for-performance, and vote “against” bottom quartile of universe

– Vote “against” Compensation Committee members in the same year the compensation plan fails the pay-for-performance quantitative model (effective 2020 proxy season)

– Additional qualitative components will continue to be used to assess compensation plans – e.g. insufficient disclosure of goals, lack of clawback policy

– For this year, CalPERS expects its say-on-pay voting outcomes to be similar to 2018, where CalPERS voted against 43% of pay programs

The report also summarizes the status of CalPERS’ voting & engagement efforts with Climate Action 100+, and its push for board quality, board diversity and majority voting in director elections. Here’s the staff’s recommended enhancements for overboarding and refreshment:

– Vote “against” non-executive directors who sit on more than 4 boards. The current practice is to vote “against” non-executive directors who sit on more than 5 boards

– Vote “against” Nominating/Governance Committee members if the Board has more than 1/3 of directors with greater than 12-year tenure AND less than 1/3 of directors were appointed in the last 6 years

More on “SEC Chair Talks About ‘Human Capital’ Disclosure”

In February, I summed up then-recent remarks from SEC Chair Jay Clayton on the topic of human capital disclosure by saying:

Companies should focus on providing material information that a reasonable investor needs to make informed investment & voting decisions – Jay is wary of mandating rigid disclosure standards or metrics.

In remarks a couple of weeks ago to the SEC Investor Advisory Committee, it was pretty clear that Chair Clayton’s views still stand. Here’s an excerpt:

Disclosure should focus on the material information that a reasonable investor needs to make informed investment and voting decisions; yet, applying this and the other principles I mentioned to human capital in the way businesses assess and disclose, and investors evaluate, for example, revenue or costs of goods sold, is not a simple task. That said, the historical approach of disclosing only the costs of compensation and benefits often is not enough to fully understand the value and impact of human capital on the performance and future prospects of an organization.

With that as context, my view is that to move our framework forward we should not attempt to impose rigid standards or metrics for human capital on all public companies. Rather, I think investors would be better served by understanding the lens through which each company looks at its human capital. In this regard, I ask: what questions do boards ask their management teams about human capital and what questions do investors—those who are making investment decisions—ask about human capital?

These remarks came in response to an IAC subcommittee recommending that the SEC adopt additional disclosure requirements on the topic of human capital management. Here’s an excerpt (also see this Cooley blog, which summarizes several HCM rulemaking petitions & initiatives, and this Willis Towers Watson memo about the IAC recommendations):

There are a wide range of potentially material HCM disclosures and ways to integrate that information into current reporting. At the most basic, issuers could be required to comply with a principles-based disclosure requirement asking them to detail their HCM policies and strategies for competitive advantage and comment on their progress in meeting their corporate objectives. This would essentially augment existing principles-based requirements with explicit discussions of HCM.

The fact that board and managers routinely rely on a number of similar metrics suggests that they can add value for investors, at least within a given sector, similar to the “view from management” approach to MD&A disclosure. We offer a few examples here of disclosure that – based on research findings in the studies cited above — could be considered. They could be considered in rule-making or as part of routine disclosure reviews by Commission staff. At a minimum, application of existing SEC guidance on non-GAAP accounting, including efforts to prevent issuers from providing inconsistent or otherwise misleading HCM disclosures over time, could be specifically applied to HCM metrics.

In the category of “leading by example,” SEC Chair Jay Clayton structured his remarks at yesterday’s “SEC Speaks” Conference in the form of an MD&A. Here’s an excerpt that shows the importance of “human capital” at the SEC:

Employee pay and benefits was our largest expenditure in fiscal years 2018 and 2013. This is not surprising given that our human capital is by far our most important asset. Technology expenditures have increased in total dollars and as a percentage of the total budget over the last five years. This is a direct result of our commitment to maintaining and upgrading our information technology systems and enhancing the agency’s cybersecurity and risk management.

For fiscal year 2019, our current fiscal year, employee pay and benefits is expected to continue to account for a significant portion of our appropriation. As a result of a hiring freeze, Commission staffing is down more than 400 authorized positions compared to fiscal year 2016. To ensure we can continue to meet our mission objectives, the resources Congress provided the agency for fiscal year 2019 will allow us to lift the hiring freeze and add 100 much-needed positions. This would put our staffing level on par with where we were five years ago.

A few weeks ago, the SEC adopted rules to implement the “Fast Act” – and when the rules go effective next month, they’ll make the following changes to the cover pages for Form 10-K, Form 10-Q and Form 8-K:

– Forms 8-K and 10-Q will require disclosure of the national exchange or principal US market for their securities, the trading symbol, and the title of each class of securities

– Form 10-K will have a new field for disclosure of the trading symbol for any securities listed on an exchange

– Form 10-K will no longer have a checkbox to show delinquent Section 16 filers

To reflect these changes, we’ve updated the Word version of the Form 10-K cover page in our “Form 10-K” Practice Area, as well as the Word version of the Form 10-Q cover page in our “Form 10-Q Practice” Area, and the Word version of the Form 8-K cover page in our “Form 8-K” Practice Area. Note that the adopting release contains the new cover page captions starting on page 216 – but doesn’t indicate exactly where the new text will be added to Form 8-K and Form 10-Q. So we’ve made an educated guess of where this new language will appear. The rules are effective May 2nd – but it typically takes the Staff a few weeks or months to incorporate these types of updates to the PDF cover pages published on the SEC’s website.

For companies that are required to submit Interactive Data Files in Inline XBRL format under Reg S-T, the Fast Act rules also require every data point on the cover pages to be presented with Inline XBRL tags. Some of the “Cover Page Interactive Data File” can be embedded – and the remainder should be attached as an exhibit under Reg S-K’s new Item 601(b)(104). The phase-in for this requirement matches the phase-in for mandatory Inline XBRL compliance. So for large accelerated filers, that means this will first be required in reports for periods ending on or after June 15th. Accelerated filers have until next year – and everyone else has until 2021. We’ve updated our “Form 10-K Cover Page Requirements Checklist” for all of the Fast Act rules – and will be updating all of our Handbooks as well.

Unsurprisingly, BlackRock is now using a technology solution, provided by CorpAxe, to coordinate governance engagement requests. There was an announcement last year that BlackRock had selected CorpAxe as their “corporate access and research management solution,” but since it didn’t mention governance activities per se, it didn’t move onto my radar until BlackRock started redirecting companies that had reached out via email to request engagement. There is also a notice on their stewardship website that you should submit engagement requests through CorpAxe.

Podcast: “Legislation to Study Rule 10b5-1 Plans”

We blogged a few months ago about proposed legislation that flew through the House and would require the SEC to study – and potentially restrict – Rule 10b5-1 trading plans. In this 19-minute podcast, Scott McKinney of Hunton Andrews Kurth discusses the bill in more detail, as it awaits consideration by the Senate. Topics include:

– What is the status of the legislation?

– What are the concerns about Rule 10b5-1 plans the legislation is intended to address?

– What specific issues would the legislation require the SEC to consider?

– What should companies do now?

There’s a lot of sense in Nouriel Roubini’s column for Project Syndicate on ICO flimflam and it’s all undone by one big mistake: “The fact that everyone within a given country or jurisdiction uses the same currency is precisely what gives money its value. Money is a public good that allows individuals to enter into free exchange without having to resort to the kind of imprecise, inefficient bartering on which traditional societies depended.

That is precisely where the ICO charlatans would effectively take us – not to the futuristic world of “ The Jetsons,” but to the modern Stone Age world of “ The Flintstones” where all transactions occur through the barter of different tokens or goods. It is time to recognize their utopian rhetoric for what it is: self-serving nonsense meant to separate credulous investors from their hard-earned savings.”

No. This is wrong. The Flintstones has a currency. Clams.

Clam shells are subdivisory units of the sand dollar, which commonly trades for goods and services either in the form of a flower-like token or a paper bill that closely resembles the US dollar. The Flintstones franchise gives a clear and consistent representation of a fiat monetary system where shells and sand dollars themselves have no intrinsic or representative value, but exist within a sophisticated economy that includes a banking system, a shadow banking system and an insurance system. Clams function as the system’s standardised, centralised, universally accepted, frictionless, low latency and fully fungible stores of value.

Meanwhile, according to this article, a guy was cited for speeding in a neighborhood while he donned a Fred Flintstone costume and was driving a real-life “footmobile”…

Poll: Vote for Your Favorite Flintstones Characters

It’s never too late to vote in my long-standing poll about which Flintstones character you like best. Nearly 10,000 votes have been cast over the years – right now, Fred barely leads over Barney, with Wilma & Betty tied for third. Then, there’s Dino, Bamm-Bamm, Great Gazoo, Mr. Slate, Pebbles and Arnold the Paper Boy. And many more. Vote anonymously now – you can’t let Mr. Slate beat Pebbles!

Yesterday, Corp Fin Director Bill Hinman & Senior Advisor for Digital Assets Valerie Szczepanik issued a statement announcing new Staff guidance on when tokens & other digital assets will be regarded as “securities” subject to SEC regulation. Here’s an excerpt:

As part of a continuing effort to assist those seeking to comply with the U.S. federal securities laws, FinHub is publishing a framework for analyzing whether a digital asset is offered and sold as an investment contract, and, therefore, is a security. The framework is not intended to be an exhaustive overview of the law, but rather, an analytical tool to help market participants assess whether the federal securities laws apply to the offer, sale, or resale of a particular digital asset.

Also, the Division of Corporation Finance is issuing a response to a no-action request, indicating that the Division will not recommend enforcement action to the Commission if the digital asset described in the request is offered or sold without registration under the U.S. federal securities laws.

The 13-page “Framework for ‘Investment Contract’ Analysis of Digital Assets” represents the most detailed guidance that the Staff has provided on the application of the Howey test to digital assets. It walks through each element of the Howey test and identifies key characteristics of a digital asset that influence the Staff’s views about whether that asset involves an “investment contract.”

The guidance in the Framework is likely to be helpful to issuers planning token offerings. But it’s unlikely to please the crypto-evangelists who seek a light touch – or even a “hands-off” approach – from the SEC. That’s because the Framework makes it very clear that the SEC will continue to apply the Howey test to digital assets with considerable rigor. As they say, if you don’t like it, write to Congress.

Digital Assets: So What About That “TurnKey Jet” No-Action Letter?

Bill Hinman’s statement referenced a new no-action letter – TurnKey Jet (4/3/19) – in which Corp Fin said it wouldn’t recommend an enforcement action against an issuer if it proceeded with a token offering without registration. This is pretty earth-shattering news, right? Yeah, not exactly. Don’t get me wrong – it’s certainly a landmark, but it’s also a fairly prosaic application of the Howey test to a deal involving the sale of fully-functional tokens structured in such a way as to squeeze out any profit potential associated with their ownership.

Corp Fin’s response letter walks through the key factors in its decision, some of which are highlighted in this excerpt from the request letter explaining why there’s no expectation of profit involved with the tokens:

It will not be technically possible to trade and transfer Tokens from the Platform in a non-Platform secondary market at a premium. Further, it will be economically impractical to trade Tokens within the Platform in a secondary market since TKJ will offer continuous, ongoing Token sales at one USD per Token which should cause the market price of Tokens not to exceed one USD per Token. These restrictions on transfer are indicative of the consumptive nature of the Tokens.

The TKJ Program memberships are non-equity memberships and will be non-transferable. The Consumers will represent that they are obtaining the TKJ memberships and Tokens for their own use and not as an investment or to profit. The TKJ memberships and Tokens will not be marketed to the public as investments. The funds that the Consumers prepay for the on-demand air charter services will be nonrefundable and will be immediately redeemable for air charter services, so no Consumer will have a reasonable expectation of profit.

Gosh, that kind of takes all the fun out of it, doesn’t it?

A New SEC Commissioner Nominee: Allison Lee

Earlier this week, the White House announced that President Trump had nominated Allison Lee to fill the vacant Democratic slot on the SEC. Allison previously served in the SEC’s Division of Enforcement & as Counsel to former Commissioner Kara Stein. This WSJ article says it is unclear when the Senate will hold her confirmation hearing. If she’s confirmed, the SEC will operate with a full slate of members – something that’s been unusual in recent years.

This ABA Journal piece talks about the ethics laws and how they may – or may not – apply to lawyers who write on blogs as ghostwriters. I am certainly not well-versed in the ethics laws – but ghostwriting blogs wouldn’t seem to be much different than the myriad of other writings that junior lawyers do on behalf of senior lawyers, without much recognition? Law firm memos, legal briefs, articles published in print publications. You name it.

I’m not saying that the practice of “not giving credit where perhaps credit is due” is a good one. I am just saying that it’s fairly rampant. And it can be a complex issue. For example, a junior lawyer writes the first draft of something – and then a senior lawyer makes heavy edits. Co-authors, right? Anyway, perhaps it all doesn’t matter that much…

Ghostwriting Blogs? Does It Matter?

I say that perhaps it doesn’t matter because most legal blogs still miss the mark. They read like law firm memos – impersonal & cold. So they don’t connect with readers (meaning they are less likely to be read – and if they are read, quickly forgotten). I’ve been giving advice for years about how to blog – here’s an excerpt from this piece I wrote over a decade ago (see pages 8-9):

A much bigger concern than coming up with stories is whether you can find your blogging “voice.” This is the concept of blogging content that is written in a style far-removed from the style used to draft sterile press releases. I’m not suggesting that you write “unprofessionally” either. Rather, it’s a bit more informal than what you do for official corporate communications.

You may be a good writer, but blogging is a different kind of writing – it requires dynamic content with an active voice and punchy prose, knowing when (and how) to use links, and more. If you can’t do this, I wouldn’t bother blogging because you won’t earn trust if you can’t connect with your audience by making it seem like it’s coming from you and not a soulless company. Look at other blogs and see the ones that you like best. And I think you will know what I mean…

Transcript: “Conduct of the Annual Meeting”

We have posted the transcript for our recent webcast: “Conduct of the Annual Meeting.”