Every 2-3 months this year, the PCAOB has been publishing resources to explain the “critical audit matters” disclosure that’ll appear in upcoming audit reports (here’s our blog about their May guidance). The latest two pieces came out last week – one is directed to investors and the other is directed to audit committees – in addition, the CAQ also published this primer on CAMs for investor relations teams.

Here’s a couple responses to “frequently asked questions” that the PCAOB has gotten from audit committees about CAMs (also see pg. 6 for a list of questions that audit committees should ask auditors):

1. Will the new requirement of the auditor to communicate CAMs change required audit committee communications?

Other than a new requirement for the auditor to provide and discuss with the audit committee a draft of the auditor’s report, the PCAOB’s requirements for audit committeecommunications remain the same. Any matter that will be communicated as a CAM should have already been discussed with the audit committee and, therefore, the information should not be new.

2. Does the audit committee have a role in determining and ap-proving CAM communications?

No. While the auditor is required to share the draft auditor’s report including any CAMs identified with the audit committee, CAMs are the sole responsibility of the auditor. The standard is designed to elicit more information about the audit directly from the auditor. As the auditor determines how best to comply with the communication requirements, the auditor could discuss with management and the audit committee the treatment of any sensitive information.

COSO’s “ERM” Framework Now Includes “ESG”

This DFin memo summarizes current trends in ESG reporting & oversight. On pages 11-14, it points out that COSO’s enterprise risk management framework was updated last fall to include risk-related ESG controls & analysis. Here’s an excerpt:

As boards are expected to provide oversight of ERM, the COSO framework supplies important considerations for boards in defining and addressing risk oversight responsibilities. The COSO ERM – ESG framework is built on the five pillars of existing ERM reporting.

5. Information, Communication & Reporting for ESG-Related Risks

Tomorrow’s Webcast: “How to Handle Hostile Attacks”

Tune in tomorrow for the DealLawyers.com webcast – “How to Handle Hostile Attacks” – to hear Goldman Sachs’ Ian Foster, Cleary Gottlieb’s Jim Langston & Innisfree’s Scott Winter provide insights into the art of responding to a hostile attack.

Yesterday, I blogged about how a dissident group won control of EQT’s board through a proxy fight that was waged using a universal proxy card. According to this Olshan memo, this marked the first time that such a card was successfully used in a control proxy contest in the US.

In the wake of the blog, a member asked this in our “Q&A Forum” (#9949):

In today’s blog, it says it’s the first time a dissident won control of a company’s board after a proxy fight using a universal proxy card. What about SandRidge Energy last year? SandRidge was considered the first company in the U.S. to let an activist board nominee onto its ballot. I didn’t follow that proxy fight very closely, but thought Carl Icahn ended up taking over SandRidge’s board.

After conferring with Andrew Freedman of Olshan, I provided this response:

Yes, there actually is a big distinction. SandRidge used a universal proxy, but Icahn could not. It relates back to the issue that Olshan covers in their alert about how company counsel is using advance notice bylaws and/or director nominee questionnaires to extract “consents” from dissident nominees, while not agreeing to provide reciprocal consents for the Company’s nominees to the dissident. Thereby creating a one-way advantage for the company to use a universal proxy card – while the dissident is left with a card that can only name the dissident’s nominees. The Rice Team & Olshan didn’t let EQT get away with that – they went to court.

The Challenges of Disclosing a CEO’s Illness

Over the years, I have blogged numerous times about the challenges of disclosing an illness for a senior executive (see this blog – and this blog). My good friend Bob Lamm delves into this sensitive topic in this blog about some recent CEO illnesses and the related disclosures…

Abigail Disney’s “Mini-Crusade” Against Disney’s Pay Ratio

I was out hiking in Laguna Beach the day Abigail Disney began her mini-crusade against Disney’s CEO pay ratio of 1,424-to-1. She laid it all out in a bunch of tweets. “Jesus Christ himself isn’t worth 500 times median workers’ pay,” she had said just weeks earlier.

Supporters and critics quickly jumped into their respective trenches. The former decried capitalism. The latter brushed off her remarks as socialist propaganda. (I exaggerate, but you get the point.)

Among her critics was Jeff Sonnenfeld, the ever-present Yale management professor. He pointed to Disney’s 580% stock return under Iger and the 70,000 jobs it’s created, and that the CEO’s pay still pales in comparison to that of some hedge fund managers, who don’t really create anything. “When pay and performance is properly aligned as it is at Disney, we need to recognize it,” he wrote.

What most of Abigail’s critics, including Sonnenfeld himself, failed to grasp was her actual point: That the wealth Disney’s created hasn’t been shared equitably with most of its employees.

In her lengthy series of tweets, she took a swipe at the shareholder-centric model of running companies and the consequences that sometimes follow for workers, the environment and surrounding communities. “When does the growing pie feed the people at the bottom?” she rhetorically asked the universe.

This question about what’s a fair sharing ratio — how much of the monetary gains of a successful company should be reaped by the single person in charge — is something I will explore in a series of stories later this year. (A sneak peek would be my piece from April about the CEO of a tiny California bank who took home twice as much as Jamie Dimon last year.)

As John blogged today on the DealLawyers.com Blog, here’s big news on the universal proxy front: yesterday, at EQT Corporation’s annual meeting, a dissident group won control of the company’s board through a proxy fight waged using a universal proxy card. According to this Olshan memo, this marks the first time that such a card was successfully used in a control proxy contest in the US. Here’s an excerpt:

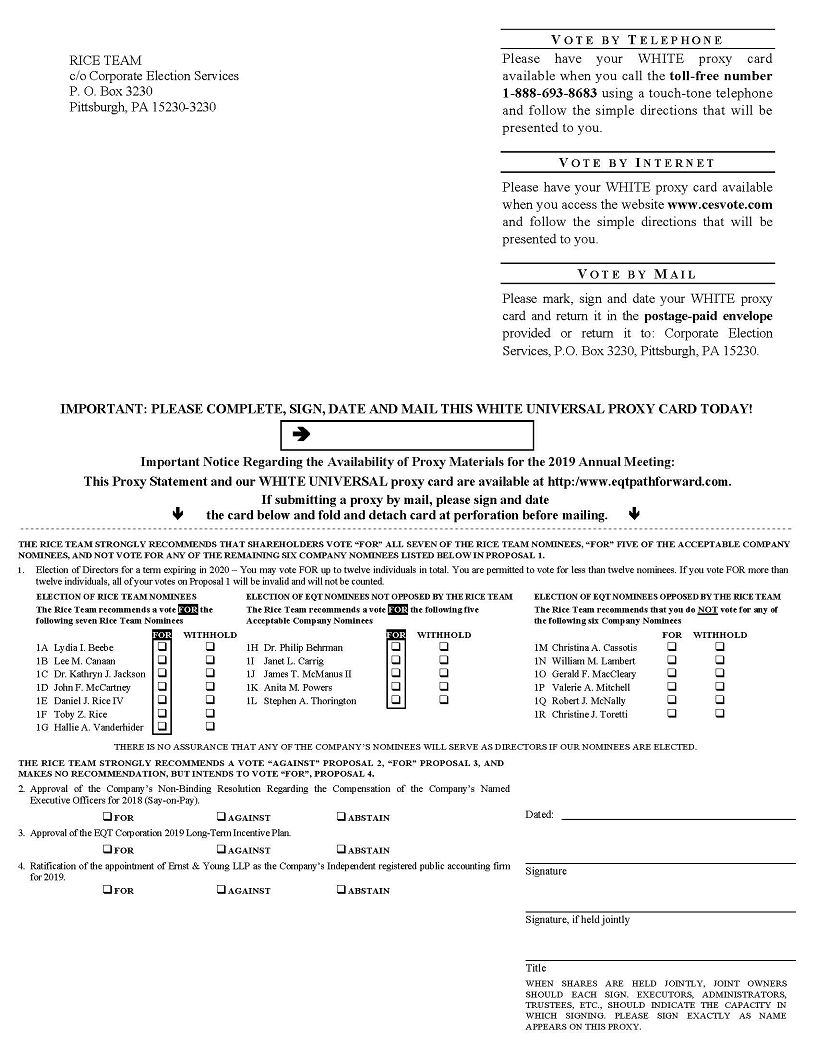

The universal ballot adopted by both EQT and the Rice Team named both EQT’s and the Rice Team’s nominees on their respective proxy cards. The only difference related to the presentation of the two cards, in which each side highlighted how it desired shareholders to vote. Copies of the two cards can be found here (Rice Team) and here (EQT).

As shown, the Rice Team made clear on its proxy card a recommendation for all seven of its nominees and for five of the Company’s nominees that it did not oppose, to permit shareholders to vote for all 12 available spots. Similarly, the Company recommended a vote for all 12 of its nominees and against the Rice Team’s nominees, other than existing director, Daniel Rice IV, who was nominated by both EQT and the Rice Team.

The Rice Team obtained public support from many of EQT’s largest shareholders, including T. Rowe Price Group Inc., D.E. Shaw & Co., Kensico Capital Management Corp. and Elliott Management Corp., along with proxy advisory firms Institutional Shareholder Services (“ISS”) and Egan-Jones Ratings.

The use of a universal ballot for a majority slate of directors is unprecedented and, in our view, may become more common in future proxy contests given the Rice Team’s success here. In fact, ISS noted the following in its report recommending that shareholders vote for all of the Rice Team’s nominees on that team’s universal proxy card:

“The adoption of a universal card was an inherently positive development for EQT shareholders (as it would be in any proxy contest), in that it will allow shareholders to optimize board composition by selecting candidates from both the management and dissident slates.”

Despite pushing for the adoption of universal proxies, some activists had recently cooled on their potential use. For instance, as we blogged last fall, Starboard Value’s CEO Jeff Smith expressed concern that in its current form, the universal ballot might tip the playing field in management’s favor. It will be interesting to see if the outcome of yesterday’s EQT vote causes people to recalibrate that assessment.

Looking at Vote Requirements

Here’s an interesting piece from ISS Analytics’ Kosmas Papadopoulos about vote requirements. Here’s the intro:

At the general meeting of Tesla Inc. on June 11, 2019, two management proposals seeking to introduce shareholder-friendly changes to the company’s governance structure failed to pass, despite both items receiving support by more than 99.5 percent of votes cast at the meeting. To get official shareholder approval, the proposals needed support by at least two-thirds of the company’s outstanding shares. However, only 52 percent of the company’s share capital was represented at the general meeting; based on turnout alone, there was no possible way for the proposal to pass.

As strange as the voting outcome at Tesla may seem, it is not a very unusual result. Every year, dozens of proposals are not considered to be “passed,” even though they receive support by an overwhelming majority of votes cast at the meeting. Supermajority vote requirements may be responsible for a large portion of these failed votes with high support levels (62 percent of instances since 2008). However, using a base of all outstanding shares for the vote requirement is an even more common corresponding factor (92 percent of instances). The increase in failed majority-supported proposals in recent years can be directly attributed to the change in the rules pertaining to the treatment of broker non-votes.

The History of Proxy Solicitation

This piece by Alliance Advisors’ Michael Mackey – published in Carl Hagberg’s “Shareholder Service Optimizer” – coincides with two of my favorite topics: history and proxy solicitation. Here’s the bottom line of the piece:

The most important takeaway for readers, as we have often noted here; this is ultimately a “people business” – where all the talent leaves the business every night – but where “the people at the top of the house” – and the people who are assigned to you own account – are the most important factors, we say, in choosing a solicitor…as the record clearly indicates if one studies the many ups and downs with care.

Two days ago, Delaware Chief Justice Leo Strine announced that he would retire from the bench. This isn’t a surprise. It’s been kind of an open secret in Delaware for the past several months – he didn’t hire clerks for the next term. Leo isn’t quite “retirement age,” so I imagine we will see grander things yet from this very grand lawyer. As noted in this article, there is speculation that Leo will run for governor in Delaware in 2024.

Over on the DealLawyers.com blog yesterday, John gave a nice summary of just how important Leo has been to the Delaware judiciary for the last few decades. And here’s a statement from SEC Chair Clayton…

SEC Approves Nasdaq’s “Liquidity” Proposal

Here’s the intro from this blog by Cooley’s Cydney Posner:

The SEC has approved, on an accelerated basis, the recent Nasdaq proposal (as amended by new amendment no. 3) to revise its initial listing standards to improve liquidity in the market. Prior to the amendments, under the initial listing rules, to list its equity on any Nasdaq tier, a company was required to have a minimum number of publicly held shares, calculated to include restricted securities. Nasdaq proposed, among other things, to revise the initial listing criteria to exclude “restricted securities” from the calculations of a company’s publicly held shares, market value of publicly held shares and round lot holders, given that restricted securities are not freely transferable and are generally illiquid.

To that end, the Nasdaq proposal added new definitions for “restricted securities,” “unrestricted publicly held shares” and “unrestricted securities.” As a result of these changes, only securities that are “freely transferable will be included in the calculation of publicly held shares to determine whether a company satisfies the Exchange’s initial listing criteria under these rules.” No changes were proposed to the continued listing requirements. To allow companies adequate time to complete in-process transactions based on the existing rules, the changes will become effective 30 days after approval (July 5) by the SEC (August 4).

California Reports on Mandatory Women Directors

Here’s the intro from this blog by Allen Matkins’ Keith Bishop:

As noted yesterday, the California Secretary of State published a report on its website concerning publicly domestic or foreign corporations with principal executive offices are located in California. This report was required to document the number of these corporations “who [sic] have at least one female director”. Cal. Corp. Code § 301.3(c). The report, which is in the form of Excel spreadsheets, includes two tables. The first, entitled “SB 826 Corporations By SEC Data”, lists some 537 corporations. The second, entitled “Reporting in Compliance”, lists 184 corporations.

It is hard to know what these tables actually represent. For example, the second table identifies Ball Corporation among the 184 corporations “reporting in compliance”. However, Ball Corporation doesn’t appear on the first list of “SB 826 Corporations By SEC Data”. That isn’t too surprising if one looks at the cover sheet of Ball Corporation’s most recently filed Form 10-K which identifies it as an Indiana corporation with its principal executive offices located in Colorado. As such, it would not be subject to SB 826. That of course begs the question of why it is listed among the compliant and the more philosophical question of whether a corporation that is not subject to the law can be considered compliant.

Last week, SEC Chair Clayton issued this statement indicating that Enforcement will process settlement offers at the same time that “bad actor” waiver requests are made if so requested by the settling party. Here’s an excerpt from the Chair’s statement (we’re posting memos in our “SEC Enforcement” Practice Area):

I have consulted with the Office of the General Counsel and the Division of Enforcement regarding the mechanics of the Commission’s consideration of a simultaneous offer of settlement and waiver request. Based on these discussions, I generally expect that, in a matter where a simultaneous settlement offer and waiver request are made and the settlement offer is accepted but the waiver request is not approved in whole or in part, the prospective defendant would need to promptly notify the staff (typically within a matter of five business days) of its agreement to move forward with that portion of the settlement offer that the Commission accepted.

In the event a prospective defendant does not promptly notify the staff that it agrees to move forward with that portion of the settlement offer that was accepted (or the defendant otherwise withdraws its offer of settlement), the negotiated settlement terms that would have resolved the underlying enforcement action may no longer be available and a litigated proceeding may follow.

Tomorrow’s Webcast: “Current Developments in Capital Raising”

Tune in tomorrow for the webcast – “Current Developments in Capital Raising” – to hear Skadden’s Ryan Dzierniejko, Locke Lord’s Rob Evans, Shearman & Sterling’s Lona Nallengara and Wilson Sonsini’s Allison Berry Spinner explore the latest developments in raising capital and all the various alternatives, including ICOs, PIPEs and registered direct offerings, “at-the market” offerings, equity line financings and rights offerings.

Financial Reporting Structures: The Charts

Here’s an odd page that a member spotted on the SEC’s website. It contains three charts related to financial reporting structures: a blue print; a flow chart; and a segment chart. They were authored in the Spring of 2018 by Wes Bricker and Ying Compton from the SEC’s Office of Chief Accountant. Even though most companies will have their own unique circumstances, these could be useful as a “gut check”…

The SEC will hold a roundtable next Thursday – July 18th – to address short-term vs. long-term “isms.” There are two panels – one for each “ism.” This follows the SEC’s “request for comment” in December about the nature, content and timing of earnings releases & quarterly reports – see the comments submitted to the SEC on that so far. And here’s the related memos we have posted…

Meanwhile, Sagar Teotia has been named the SEC’s Chief Accountant – he had been serving as “Acting” in that capacity for a while…

Usable Disclosure: Plain English Helps

Here’s a nice short piece by Third Creek Advisors’ Adam Epstein about how smaller companies can become more effective storytellers. Here’s an excerpt:

If your company’s storytelling acumen is high, your test subjects will quickly and accurately grasp the zeitgeist of your company. If they struggle, it’s likely that lots of small-cap investors – many of whom are generalists – don’t sufficiently understand what your company does either.

One way to dramatically increase messaging effectiveness is through website videos. Notwithstanding the fact that in excess of five billion videos are watched daily on YouTube, a surprising number of small-cap companies don’t have an “about us” video easily accessible on the home page of their corporate websites. This is a big mistake; a two-minute, professionally-produced, easy-to-understand video can pay for itself almost immediately.

Corp Fin Updates “Financial Reporting Manual” (Again)

Last week, Corp Fin indicated that it has updated its “Financial Reporting Manual” to remove guidance related to presentation of selected financial data & acquired business financial statements in a Form 10 filed by a “Smaller Reporting Company”; clarify the application of Rule 3-13 and Note 5 to Rule 8-01 of Regulation S-X; and provide revisions for certain technical amendments (e.g., update EGC revenue threshold pursuant to SEC Release 33-10332 and replace FASB ASU references with the applicable ASC Topics).

At the Society of Corporate Governance’s conference last week, Skadden’s Hagen Ganem had an idea. Why not run a cute dog contest? Genius. So here is our first annual contest (vote for the cutest dog; not the cutest owner of a dog) – the poll is at the bottom of this blog:

1. Skadden’s Hagen Ganem – Teddy the “Snoozer”

2. Morrison & Foerster’s Dave Lynn – Jack the “Ripper”

3. PJT Camberview’s Shannon Johnson – Mia the “Mini Bernedoodle”

4. Gibson Dunn’s Ron Mueller – Jack & Morgan the “Love Bugs”

5. TheCorporateCounsel.net’s Broc Romanek – Willa the “Wonderful”

Vote Now: “Cutest Dog Contest”

Vote now in this poll – anonymously – for the dog that you think is the cutest:

A long, long while back, I blogged a story about an IPO prospectus that contained the term “certified pubic.” Here are a few more reactions from members about disclosure gaffes:

While I hadn’t heard of the “certified pubic accountant” goof previously, I can vouch for the IPO red herring that was circulated in the early 1970s with an “initial pubic offering” statement on the cover page. I never did see the SEC comment letter to know whether or not the Staff examiner commented on it.

I’m sitting here chuckling at my desk. I guess “certified pubic accountant” does beat “commom stock.” I admit I have caught the “pubic accountant” terminology a couple of times before the SEC filing was made. Given the number of times it is found on Edgar, I think we all need to include that global search in our checklists.

Sneaker Exchange & Other Online Marketplaces

Back when the Web was born in the mid-90s, I remember working on some no-action letters related to trading various things on this new thing called the “Internet.” Complex securities law issues – novel stuff. Flash forward twenty years and we have an amazing array of online marketplaces worth billions, as noted in this NY Times article…

Transcript: “Proxy Season Post-Mortem – The Latest Compensation Disclosures”

We’ve posted the transcript for the recent CompensationStandards.com webcast: “Proxy Season Post-Mortem – The Latest Compensation Disclosures.” Mark Borges, Dave Lynn & Ron Mueller shared their latest takes on these topics:

1. Say-on-Pay Results

2. Performance-Based Compensation Disclosure

3. Shareholder Responsiveness Disclosure

4. Perquisites Disclosure

5. Director Compensation Disclosure

6. CEO Pay Ratio Trends

7. Hedging Disclosure Rule

8. Status of Other Dodd-Frank Rulemaking

9. Shareholder Proposals

10. Proxy Advisors

11. Proxy Strike Suits

One of the stranger things in this field is hearing a SEC Staffer start off their public remarks by providing the “standard” disclaimer that their remarks are their own and not those of the Commission. It seems silly because I would argue that it’s implicit that a Staff member was not speaking for the Commission, but was simply expressing their own thoughts. And in a way, it’s embarrassing for them because it could be heard as “I’m not worthy of being here because what I say doesn’t really matter.”

Luckily, we are used to hearing the disclaimer – so we don’t hear it like that. We have come to expect it – and it even provides a bit of levity to the proceedings because everyone in the room recognizes how silly it is. Including the Staffer forced to utter it. I say “forced” because the Staff is forced to say it. That has been the case for as long as I can remember. It was the case when I spoke as a Corp Fin Staffer back in the ’90s.

But I have checked with some old-timers and they swear they didn’t provide a disclaimer when they spoke in the ’80s. So sometime between the ’80s & the ’90s, something must have happened that caused generations of Staffers to utter such nonsense…

From a member: “For some reason, this disclaimer blog reminded me of the honor pledge we had to write at law school. Whenever we took an exam, we had to write out the following pledge on the cover of the bluebook: “On my honor as a student, I have neither given nor received aid on this examination nor did I have prior knowledge of its contents.” Then you had to sign your name.

You could always tell the law students who’d gone to my school as undergrads, because while the rest of us were dutifully scribbling out all 25 words of the pledge, they were just scrawling “pledged” and signing their names to it. Anyway, maybe the Staffers who’ve been at the SEC for a long time should just say “disclaimed” and get on with their speeches.”

Poll: What Caused the SEC Staff to Start Providing a Disclaimer?

So what is your guess as to why the SEC Staff was forced to starting providing a “public speaking” disclaimer? Please provide your answer via this anonymous poll:

polls

Our July Eminders is Posted!

We have posted the July issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

FOIA Exemption 4 protects “trade secrets and commercial or financial information obtained from a person [that is] privileged or confidential.” However, most federal circuit courts have read in a “substantial competitive harm” test under which commercial information would be regarded as “confidential” only if its disclosure was likely to cause substantial harm to the competitive position of the person from whom it was obtained.

The substantial competitive harm requirement had its genesis in the D.C. Circuit’s 1974 decision in National Parks & Conservation Association v. Morton, and the standard had been widely adopted by other courts. But earlier this week, by a 6-3 vote, the SCOTUS invalidated the requirement in Food Marketing Institute v. Argus Leader Media. Here’s an excerpt from this Cleary Gottlieb memo that addresses the Court’s reasoning:

Notwithstanding that the lower courts have followed National Parks in one form or another for 45 years, the Supreme Court roundly rejected it. Writing for six members of the Court, Justice Gorsuch criticized the D.C. Circuit’s creation of the “substantial competitive harms test” based on its interpretation of legislative history as demonstrating a “casual disregard of the rules of statutory interpretation.”

Food Marketing Institute held that a court must begin its analysis of statutory terms by referencing the ordinary meaning and structure of the law itself, and when this leads to a clear answer, the court must not go further. The Court found that because there is “clear statutory language” in FOIA, legislative history should never have been allowed to “muddy the meaning” of this language.

The decision should substantially reduce the burden associated protecting confidential information submitted to the government, but the memo says that it also raises questions about how agencies and courts will apply existing regulations that incorporate the “substantial competitive harm” test, and whether they will need to revise such regulations or attempt to justify disclosure decisions on other grounds.

What Does the SCOTUS’s Decision Mean for CTRs?

The SEC is one of the agencies that will need to sort out how the SCOTUS’s decision to eliminate the “substantial competitive harm” standard impacts existing rules. In that regard, here are some insights that Bass Berry’s Jay Knight shared with us on how the Court’s decision complicates the SEC’s recently simplified CTR process:

As everyone may recall, in March the SEC adopted amendments to disclosure requirements for reporting companies, as mandated by the 2015 Fixing America’s Surface Transportation Act (the “FAST Act”). Among the amendments was a simpler CTR process, which now allows registrants to omit immaterial confidential information from acquisition agreements filed pursuant to Item 601(b)(2) of Regulation S-K and material contracts filed pursuant to Item 601(b)(10) of Regulation S-K without having to file a concurrent confidential treatment request. In short, registrants are permitted to redact provisions in such exhibit filings “if those provisions are both not material and would likely cause competitive harm to the registrant if publicly disclosed.” (emphasis added)

In the SEC’s adopting release, the SEC notes that it slightly revised the language of the amendment in the final rule to refer to information that “would likely cause competitive harm” to “more closely track the standard under FOIA.” (see page 25 of the adopting release) With the Supreme Court holding that FOIA exemption 4 does not have a competitive harm condition, it calls into question whether the “competitive harm” standard in Item 601 continues to be appropriate. (Other potential rules impacted are Exchange Act Rule 24b-2 and Securities Act Rule 406, which require that applicants for confidential treatment justify their nondisclosure on the basis of the applicable exemption(s) from disclosure under Rule 80, as well as Staff Legal Bulletin No. 1 and 1A, and Rule 83.)

Since that competitive harm standard is embedded in the SEC’s rules, at this point the prudent path for companies appears to be to continue to adhere the requirements of those rules until the SEC provides further guidance.

The Staff has informally advised us that they are evaluating the potential implications of the Food Marketing Institute decision on Rule 24b-2, Rule 406 & other rules that involve confidential treatment requests under FOIA. However, the Staff does not believe that Item 601(b) is implicated by the decision, since the new procedures relate to situations in which information need not to be filed with the SEC, rather than situations in which companies are seeking to use FOIA exemption 4 to protect information that has been filed.

Insider Trading: Lawyers Are Increasingly In the Cross-Hairs

Over the past year or so, we’ve blogged about a number of insider trading cases in which lawyers were involved directly or, sometimes, indirectly. If it seems like lawyers are being implicated more in insider trading cases, this Arnold & Porter memo says there’s a reason for that – they are:

A recent series of insider trading actions charging senior lawyers in legal departments of prominent public companies suggests that insider trading by lawyers may be on the rise. Over the past several months, the U.S. Securities and Exchange Commission has brought enforcement actions charging insider trading in advance of earnings announcements by senior lawyers at Apple and SeaWorld. In a third action, filed in early May 2019, the general counsel of Cintas Corporation was an unwitting victim of a house guest, a lifelong friend, who, the SEC alleges, surreptitiously pilfered merger related information from a folder in the lawyer’s home office.

These actions are noteworthy not only for the brazenness of the conduct involved, but because they suggest that insider trading by lawyers remains a “profound problem.” And, as the case of the Cintas general counsel demonstrates, innocent lawyers may also fall prey to others, such as close friends and family, looking to exploit their access to material nonpublic information, or MNPI.

Here at TheCorporateCounsel.net, we’re on record that if you’re a corporate officer who engages in insider trading, then – as one of my high school football coaches used to say – “you’re stuck on stupid.” But if you need more convincing, read the memo’s review of the recent proceedings involving lawyers, and the actions that companies & law departments can take to mitigate their insider trading risks.

{kind=link}

{kind=link}