Here’s something John blogged last week on DealLawyers.com: Don’t look now, but the Delaware Chancery Court just upheld another Caremark claim in the face of a motion to dismiss. In his 50-page opinion in In re Clovis Oncology Derivative Litigation, (Del. Ch.; 10/19), Vice Chancellor Slights held that the plaintiffs had adequately pled that the board breached its fiduciary duties by failing to oversee a clinical trial for the company’s experimental lung cancer drug and then allowing the company to mislead the market regarding the drug’s efficacy.

In declining to dismiss the case, the Vice Chancellor observed that Delaware courts are more likely to find liability under Caremark for oversight failures involving compliance obligations under regulatory mandates than for those involving oversight of ordinary business risks:

Caremark rests on the presumption that corporate fiduciaries are afforded “great discretion to design context- and industry-specific approaches tailored to their companies’ businesses and resources.” Indeed, “[b]usiness decision-makers must operate in the real world, with imperfect information, limited resources, and uncertain future. To impose liability on directors for making a ‘wrong’ business decision would cripple their ability to earn returns for investors by taking business risks.”

But, as fiduciaries, corporate managers must be informed of, and oversee compliance with, the regulatory environments in which their businesses operate. In this regard, as relates to Caremark liability, it is appropriate to distinguish the board’s oversight of the company’s management of business risk that is inherent in its business plan from the board’s oversight of the company’s compliance with positive law—including regulatory mandates.

As this Court recently noted, “[t]he legal academy has observed that Delaware courts are more inclined to find Caremark oversight liability at the board level when the company operates in the midst of obligations imposed upon it by positive law yet fails to implement compliance systems, or fails to monitor existing compliance systems, such that a violation of law, and resulting liability, occurs.”

VC Slights cited the Delaware Supreme Court’s recent decision in Marchand v. Barnhill, and noted that that case “underscores the importance of the board’s oversight function when the company is operating in the midst of ‘mission critical’ regulatory compliance risk.”

Caremark requires a plaintiff to establish that the board either “completely fail[ed] to implement any reporting or information system or controls” or failed to adequately monitor that system by ignoring “red flags” of non-compliance. While the board’s governance committee was responsible for overseeing compliance with regulatory requirements applicable to the clinical trial, the Vice Chancellor held that the plaintiff adequately pled that it knowingly ignored red flags indicating that the company was not complying with those requirements. Accordingly, he declined to dismiss the case.

Ann Lipton has some interesting perspectives on VC Slights’ distinction between business & legal compliance risks over on her Twitter feed. Check it out.

Caremark still may be, as former Chancellor Allen put it, “possibly the most difficult theory in corporation law upon which a plaintiff might hope to win a judgment.” But after decades of routinely dismissing Caremark claims at the pleading stage, this marks the second time this year that the Delaware courts have declined to do so – and it’s the third case in the last two years in which they’ve characterized a Caremark claim as “viable.”

Is Caremark becoming a more viable theory of liability, or is board’s conduct in these cases just more egregious than in prior cases? It’s hard to say based on the limited evidence we have. For now, maybe the ’60s band Buffalo Springfield put it best – “There’s something happening here. What it is ain’t exactly clear. . .”

ISS Proposes Policy Changes: Comment By October 18th!

Yesterday, ISS announced a public comment period for proposed policy changes that would apply to next year’s annual meetings. For the US, the proposed changes are:

1. Clarifying a maximum 7-year sunset and other parameters for multi-class capital structures at newly public companies

2. Codifying ISS’s existing approach to “independent chair” shareholder proposals by identifying factors that will weigh in favor of a “For” recommendation – e.g. a “weak or poorly defined lead director role” – and moving some info into the “Policy FAQs”

3. Adding safeguards against “abusive practices” to the policy to vote “For” management proposals for buyback programs – e.g. the use of buybacks to boost EPS-based pay metrics

Submit comments to policy@issgovernance.com by next Friday – October 18th. Unless otherwise specified in writing, all comments will be disclosed publicly upon release of final policies – which is expected during the first half of November.

Ransomware: Preparing for a Growing Threat

According to a recent NYT article, more than 40 municipalities have been victims of ransomware attacks this year, including the 23 towns in Texas that were hit recently. This Wachtell Lipton memo predicts that ransomware is a growing threat for companies too – and offers these preparation & response tips (also see the suggestions in this “Accounting Today” article):

Before an attack:

– Reduce ransomware exposure by implementing reliable backup processes for IT systems & critical data

– Get cyber insurance that covers costs associated with ransomware incidents

– Implement incident response plans – including elevation procedures

– Foster pre-attack relationships with law enforcement

Responding to an attack:

– Protect attorney-client privilege by assigning legal counsel a leadership response role & engaging other advisers through counsel

– Assess disclosure obligations – e.g. state & international data breach notifications, SEC and industry-specific disclosure requirements

– Determine notice requirements for insurers, vendors and customers

– Approach the decision whether to pay a ransom with great caution & careful deliberation

On that last point about whether to pay a ransom, this ProPublica article outlines the pros & cons for victims – and suggests insurers have an incentive to accommodate the attackers even if (or because?) doing so leads to more incidents. According to the article, cyber insurance is now a $7-8 billion/year market, and insurers know that could fall apart if nobody is worried about getting hacked.

What a freak show the now-aborted WeWork IPO wound up being. For example, this falls into the “news of the weird” category – check out this excerpt from this article about the role the CEO’s spouse played in preparing the company’s Form S-1:

An S-1 is meant to be a bland financial document, but WeWork’s took a different direction. With Adam’s encouragement, Rebekah became unusually involved in the artistic presentation of the document. “The traditional approach to producing an S-1 is bankers and lawyers hashing this out, but the process was continually usurped by Rebekah’s involvement,” one executive said, echoing a sentiment expressed by multiple people who worked on the project. “She treated it like it was the September issue of Vogue.”

WeWork had hired a former director of photography at Vanity Fair, and Rebekah insisted on selecting the photographers chosen to take photos of WeWork offices and members, and approved every photo that appeared in the S-1, of which WeWork included many more than most companies that go public. (She wasn’t the only picky one: Adam Kimmel, the company’s chief creative officer, became unhappy with how the company’s offices looked in its official pictures, so new photographers were sent around the world to reshoot them.)

As the summer wore on, WeWork employees found themselves making so many trips to meet with Rebekah at the Neumanns’ home in Amagansett that “He’s ‘out east’ tomorrow” became a euphemism for describing a colleague spending their day driving to and from the Hamptons. “The thing that’s so damning about all that is that it’s just not the point of the document,” a person who worked on the project said. “That’s the thing about WeWork: You’re spending all this time working on the surface of it instead of the actual truth of the thing.”

CalPERS Votes Against 53% of Pay Plans!

This blog by Jim McRitchie is mindblowing! Here’s a summary:

CalPERS, the largest U.S. pension fund which manages more than $380 billion in assets, has already started implementing its new compensation framework. In an effort to drive more accountability and improved pay for performance alignment, CalPERS reports voting against 53% of compensation plans at portfolio companies during the 2019 proxy season. That is up from 43% last year.

This September-October issue of the Deal Lawyers print newsletter was just posted – & also mailed – and includes articles on:

– Five Observations on Recent Use of Universal Proxies

– Delaware Chancery Upholds Waiver of Appraisal Rights

– Does Your Acquisition Agreement Trigger a Form 8-K?

– Disclosure of Projections: Will Delaware’s Approach Still Rule the Roost?

Right now, you can subscribe to the Deal Lawyers print newsletter with a “Free for Rest of ‘19” no-risk trial. And remember that – as a “thank you” to those that subscribe to both DealLawyers.com & our Deal Lawyers print newsletter – we are making all issues of the Deal Lawyers print newsletter available online. There is a big blue tab called “Back Issues” near the top of DealLawyers.com – 2nd from the end of the row of tabs. This tab leads to all of our issues, including the most recent one.

And a bonus is that even if only one person in your firm is a subscriber to the Deal Lawyers print newsletter, anyone who has access to DealLawyers.com will be able to gain access to the Deal Lawyers print newsletter. For example, if your firm has a firmwide license to DealLawyers.com – and only one person subscribes to the print newsletter – everybody in your firm will be able to access the online issues of the print newsletter. That is real value. Here are FAQs about the Deal Lawyers print newsletter including how to access the issues online.

As it has for the past few election cycles, executive compensation is working itself into the 2020 Presidential campaign. Bernie Sanders announced a proposal this week that would increase the corporate tax rate if a large company’s pay ratio is 50x or more (it would apply to any public or private company with more than $100 million in revenue). Here’s some news articles about it:

If you follow the SEC’s Enforcement actions, you find quite a few that can be entertaining. As Cooley’s Cydney Posner blogs, this one involving Marvell Technology is interesting because the company ran a “revenue management scheme” and the SEC took action not because of the scheme itself, but rather because the company failed to publicly disclose the scheme in its MD&A (or to disclose its likely impact on future performance). The SEC’s order demonstrates that, even if a scheme involving unusual sales practices may not amount to chargeable accounting fraud, failure to disclose may be actionable..

More on “Proxy Season Blog”

We continue to post new items on our blog – “Proxy Season Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Firearms Responsibility: Will Shareholders Show Renewed Interest?

– Proxy Voting: Impact of Mutual Fund Board Connections

– Uncontested Director Elections: Impact of Negative ISS Recommendations

– Proxy Plumbing: Recommendations From SEC’s “Investor” Subcommittee

– Shareholder Engagement: A UK Study of Investor Trends

Here’s a blog that I drafted before Corp Fin made its recent announcement about how it will process Rule 14a-8 requests for shareholder proposals going forward – it’s still worth sharing: Last month, I had lunch with a friend who started foaming at the mouth about the need for Corp Fin to remove itself as the referee in the no-action process for shareholder proposals. After his foam had dried, I replied that Corp Fin would like nothing more. The problem historically has been that whenever Corp Fin suggests that it diminish its role, participants on all sides scream bloody murder.

Processing no-action requests under Rule 14a-8 is labor intensive in Corp Fin. Most requests come in during a short window and are time sensitive. The Staffers working on them still have their regular workload to deal with (at least when I served in Corp Fin). Being placed on the “Shareholder Proposal Task Force” feels like punishment. Long hours. Very long. Highly sensitive situations in some cases – the kind that can derail your career. And not exactly intellectually rewarding.

Here’s an excerpt from the SEC’s adopting release in 1998, the last time the SEC significantly changed Rule 14a-8:

Some of the proposals we are not adopting share a common theme: to reduce the Commission’s and its staff’s role in the process and to provide shareholders and companies with a greater opportunity to decide for themselves which proposals are sufficiently important and relevant to the company’s business to justify inclusion in its proxy materials. However, a number of commenters resisted the idea of significantly decreasing the role of the Commission and its staff as informal arbiters through the administration of the no-action letter process. Consistent with these views, commenters were equally unsupportive of fundamental alternatives to the existing rule and process that, in different degrees, would have decreased the Commission’s overall participation.

Processing Shareholder Proposals: Life Can Be Rough

A story to illustrate. When I first joined Corp Fin in ’88 for my first tour of duty at the SEC, I was right out of law school. That was typical back then. And each branch was required to contribute one person to the Shareholder Proposal Task Force. You were “it” if you were the newest person in the branch. So the Task Force was comprised of a dozen people who were right out of law school.

Nothing was electronic back then. We wrote out our analysis & recommendation for each no-action request by hand. There was only one computer for the entirety of Corp Fin. So you would have to wait until “after hours” to be able to access it and print out precedent to support your analysis (the Division had a Lexis account on this prized computer that sat over in the Office of Chief Counsel). To top off this charmed experience, I was chewed out by a crazed supervisor over one of my first recommendations. By the end of his diatribe, he realized he had gone over the top and invited me out to go drink whiskey (I declined).

I wouldn’t blame him except I was right out of law school. My training when I arrived consisted of my boss handing me a rulebook and saying “here, read this over the next week.” So I read S-K – and the ’33 Act &’34 Act rules – straight. Those things are not meant to be read straight. So I learned nothing, Other than that the SEC’s rules & regulations are not written in anything close to plain English. There was literally no training. If you got lucky, your office mate was experienced & willing to teach. Yes, life was tough in the old days…

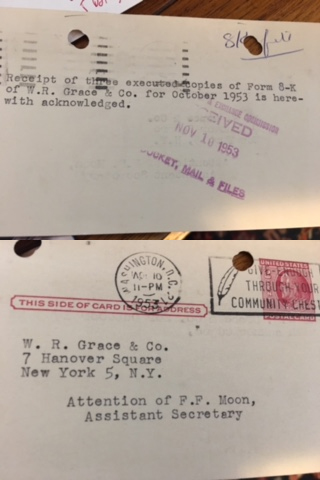

Big hat tip to Sean Dempsey for sending me this awesome receipt – stamped by the SEC – acknowledging the filing of a Form 8-K by his company, W.R. Grace in 1953:

I love hearing stories from old-timers about making filings before Edgar was born. Personally, I remember being on the Corp Fin Staff in the ‘80s & going outside to get a little fresh air on days that happened to be 10-Q or 10-K filing deadline days. The line of FedEx trucks went on for blocks. I barely noticed…

Another Cool License Plate!

Check out this license plate from Jim McRitchie, who has run the “CorpGov.net” website forever (his wife is part-Hawaiian; hence the turtle-themed plate holder):

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Board Evaluations: How They Are Evolving

– Multi-Class Companies: CII Appeals to Delaware

– Crisis Management: Public Relations Considerations

– D&O Insurance: Outlook for 2020

– Gov. Investigations: Key Questions When You Get An Investigative Request

Recently, I blogged about when a SEC Staffer kicks off their public remarks with a disclaimer that their remarks are their own and not those of the Commission. I mused that the origins of this disclaimer seem to have been forgotten. I then heard from a number of members with remembrances and their own research on this topic.

(b) Reference to official position. An employee who is engaged in teaching, speaking or writing as outside employment or as an outside activity shall not use or permit the use of his official title or position to identify him in connection with his teaching, speaking or writing activity or to promote any book, seminar, course, program or similar undertaking, except that:

(2) An employee may use, or permit the use of, his title or position in connection with an article published in a scientific or professional journal, provided that the title or position is accompanied by a reasonably prominent disclaimer satisfactory to the agency stating that the views expressed in the article do not necessarily represent the views of the agency or the United States; and

And former SEC General Counsel Dan Goelzer dug back even further – noting that the disclaimer appears in “Rule 4 (Outside Employment and Activities)” of the SEC’s “Regulation Concerning Conduct of Members and Employees and Former Members and Employees of the Commission.” Rule 4(d)(2)(ii)(A) contains the current version of the disclaimer:

Therefore, such publication or speech shall include at an appropriate place or in a footnote or otherwise, the following disclaimer of responsibility: “The Securities and Exchange Commission disclaims responsibility for any private publication or statement of any SEC employee or Commissioner. This [article, outline, speech, chapter] expresses the author’s views and does not necessarily reflect those of the Commission, the [other] Commissioners, or [other] members of the staff.”

Dan isn’t quite sure when the disclaimer originated, but he does know it was prior to 1980. In 1980, the SEC made various revisions to that conduct regulation – and while a number of changes to Rule 4 are described in that ’80 release, the disclaimer is not one of them. Therefore, we think that the disclaimer was in the pre-1980 version of Rule 4 as well. To bolster the point, Dan sent over two pre-1980 speeches – by Al Sommer (a SEC Commissioner at the time) and Alan Mostoff (then the IM Director) – that include the disclaimer. So it goes way, way, back…

How to Submit Comments on the SEC’s Rulemaking

Among the hundreds of “checklists” posted on our site is this one about how to submit comments on a SEC’s rulemaking. Now the SEC has posted this 90-second video about how easy it is to submit comments on a rule proposal. It has over 350 views within a few months…

Our October Eminders is Posted!

We’ve posted the October issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!

Wow! All that is new is “old” again! When I first joined Corp Fin in 1988, there were a half dozen or so “pods” – each with two branches – that were devoted to specific industries. Each pod was headed by an Assistant Director, which was a difficult job to obtain because a slot only opened when someone retired (back then, it was quite rare for an AD to leave the SEC before retirement). Over time, the Division’s “groups” (as they were eventually renamed from “pods”) grew and the number of them nearly doubled. Now, with this Corp Fin announcement on Friday, we’re going back to the way we were.

Here’s some things to note:

1. Cutting the Number of Groups Nearly in Half – Corp Fin is realigning some of industry groups and reducing them in number from 11 to 7. The groups are now called “Offices” – led by a “Chief” and a “Senior Advisor.”

2. Improving (& Streamlining) the Review Process – Led by an “Office of Assessment & Continuous Improvement,” the teams within Corp Fin that will review filings look to be leaner under this new realigned group structure. There have been fewer comments issued in recent years by the Staff as companies have gotten better observing comment trends and adjusting their disclosures according (not to mention the sheer number of public companies has shrunk a whole lot). Corp Fin will continue to focus on improving the comment process in an effort to be more relevant, timely & consistent.

3. Focus on “Hot” Comment Areas – Led by an “Office of Risk & Strategy,” Corp Fin will focus on emerging issues in their comments – think Libor, cybersecurity and Brexit as recent examples. This Office will review filings for good (or bad) examples of disclosure and then share those internally. It’s something the Staff has already been doing – but it’s now formalizing that function.

4. What Group Is Your Company In? – These seven new groups took effect yesterday – so you can find your new industry group by looking on Edgar for your filing history and noting what “Office” is listed. For example, you’ll see in the 4th line down that Microsoft belongs in the “Office of Technology” group. In many cases, your company’s group will be the same. And if you have a filing that is being actively reviewed right now, the Staffers reviewing your filing aren’t going to change – even if the Office that your company belongs in has changed.

Corp Fin has pulled down its org chart – at least for now. We just deleted our own more comprehensive Corp Fin org chart. I’ve maintained it for 17 years but it’s become too hard to keep up. That was a harder task than you would think – very few people even within Corp Fin know the identities of all the middle managers, etc. A constant game of “Where’s Waldo”…

SEC Proposes to Modernize the OTC Market

Last Thursday, the SEC proposed to modernize the over-the-counter market (OTC) by proposing changes to Rule 15c2-11, which sets out certain requirements with which a broker-dealer must comply before it can publish quotations for securities in the OTC market. Here’s the 228-page proposing release.

Moody’s “Governance” Framework for Credit Ratings

Recently, I blogged how Moody’s was getting into the governance ratings business – but as I noted in that blog, Moody’s has scored governance for quite some time for their credit ratings business. Recently, Moody’s issued a framework to help understand key aspects of governance that are incorporated into all Moody’s credit ratings and analysis, including two taxonomies: a private taxonomy, which applies to non-financial corporates, financial institutions, infrastructure, structured finance and certain competitive government-owned enterprises; and a public taxonomy, which applies to sovereign, sub-sovereign and municipal issuers…

Yesterday, the SEC announced that it had adopted final rules permitting all companies to gauge market interest in a possible initial public offering or other registered securities offering to “test the waters” by reaching out to certain institutional investors before filing a registration statement. Previously, only EGCs had been able to engage in this activity under applicable provisions of the JOBS Act. Here’s an excerpt from the fact sheet included in the press release summarizing the rule:

Securities Act Rule 163B will permit any issuer, or any person authorized to act on its behalf, to engage in oral or written communications with potential investors that are, or are reasonably believed to be, QIBs or IAIs, either prior to or following the filing of a registration statement, to determine whether such investors might have an interest in a contemplated registered securities offering. The rule is non-exclusive and an issuer may rely on other Securities Act communications rules or exemptions when determining how, when, and what to communicate about a contemplated securities offering.

Under the rule:

– there are no filing or legending requirements;

– the communications are deemed “offers”; and

– issuers subject to Regulation FD will need to consider whether any information in a test-the-waters communication would trigger disclosure obligations under Regulation FD or whether an exemption under Regulation FD would apply.

In a public statement accompanying the announcement of the new rule, SEC Chair Jay Clayton said that it will allow issuers to “better identify information that is important to investors and enhance the ability to conduct a successful registered offering, ultimately providing both Main Street and institutional investors with more opportunities to invest in public companies that, in turn, provide ongoing disclosures to their investors.” The new rule will become effective 60 days after publication in the federal register.

Auditor Independence: Flurry of SEC & PCAOB Enforcement

Earlier this week, the Division of Enforcement announced a settled enforcement proceeding with PwC arising out of alleged violations of the SEC’s independence rules. PwC’s Mexican affiliate was also sanctioned for independence violations by the PCAOB in August. The SEC’s action against PwC comes on the heels of another settled proceeding late last month involving RSM US LLP. Earlier this month, the PCAOB sanctioned another two accounting firms for independence violations.

So, what’s with this recent spate of enforcement proceedings? It’s hard to say for sure, but this may have been coming for quite some time. Broc blogged last year that Lynn Turner reported that there was “trouble brewing” at the PCAOB & SEC over independence issues. The PCAOB apparently discovered a number of independence issues in its 2016 inspection reports, and noted that many of these were not reported to the audit committee as required under PCAOB rules.

Earlier this year, the PCAOB came out with additional guidance on what the rules require auditors to communicate to audit committees when they identify independence issues, and the failure to comply with independence disclosure requirements is at the heart of both the PCAOB & SEC enforcement proceedings involving PwC.

PCAOB: Board Laying Low in Wake of KPMG Scandal?

Speaking of the PCAOB, according to this article by MarketWatch.com’s Francine McKenna, the PCAOB continues to be in transition in the wake of the KPMG scandal – and its board has apparently decided to keep a very low profile, even if that appears to violate the PCAOB’s bylaws:

The PCAOB board is staying out of the public eye in 2019, in violation of bylaws established by the law that created the PCAOB, the Sarbanes-Oxley Act of 2002. The law requires the PCAOB to hold at least one public meeting of its governing board each calendar quarter. However, the PCAOB board has held no public meetings of its governing board since December 20, 2018.

MarketWatch asked the PCAOB to comment on its apparent lack of compliance with its bylaws regarding open board meetings. A PCAOB spokeswoman told MarketWatch, “Consistent with long-standing practice, the Board holds open meetings to take action on business such as standard-setting or voting on its budget and strategic plan. We expect to hold two open meetings in the coming months to address our 2020 budget and a proposed concept release related to our quality control standards.”

Even by current D.C. standards, the PCAOB’s response leaves much to be desired. It’s not a denial, and it isn’t even a “non-denial denial.” By the way, it isn’t just the board – the article says that the PCAOB’s two outside advisory groups haven’t met in 2019 either.

I have a friend who keeps trying to persuade me to buy a Tesla. He owns one, and I guess there’s some kind of bounty the company pays to Tesla owners who convince other people to pony up for their own E-Z-Go on steroids. I’ve told him he’s barking up the wrong tree. I’ve always driven a beater. My current ride is a 2012 Chevy Equinox with 140,000 miles on it. It goes through 2 quarts of oil a month and I’m still determined to keep it for at least another couple of years.

But I also confess that even if I was in the market for a new car, I just can’t see buying one from Elon Musk. The guy’s antics really rub me the wrong way. So it pains me to have to blog about him again – but I do. This time, Elon and his board have gotten themselves sideways with Tesla shareholders in the Delaware Chancery Court, and the issue isn’t his tweets, it’s his comp.

Last year, the Tesla board – and shareholders – signed-off on a pay deal that would provide Musk with a potentially gargantuan payout if its stock hit some very aggressive market cap & operational goals. How gargantuan? Try more than $50 billion. A shareholder subsequently filed a lawsuit against Musk and the Tesla board alleging that the comp award was a breach of fiduciary duty.

By way of background, the Chancery Court decided last year that Musk was a “controlling shareholder” of Tesla in an unrelated case, despite the fact that he owned only around 20% of the stock. So, for purposes of the motion to dismiss filed in this case, the parties treated him as if he was a controller. That complicates things considerably, because the default standard for reviewing for transactions between a company and its controlling shareholder – even comp decisions – is the demanding “entire fairness” standard and not the deferential business judgment rule.

Delaware has laid out a path to the business judgment rule for these transactions, but in his 40-page opinion denying the defendants’ motion to dismiss, Vice Chancellor Slights found that despite the approval of the comp award by Tesla’s shareholders, the process wasn’t good enough to allow this award to make the cut:

Had the Board ensured from the outset of “substantive economic negotiations” that both of Tesla’s qualified decision makers—an independent, fully functioning Compensation Committee and the minority stockholders—were able to engage in an informed review of the Award, followed by meaningful (i.e., otherwise uncoerced) approval, the Court’s reflexive suspicion of Musk’s coercive influence over the outcome would be abated. Business judgment deference at the pleadings stage would then be justified. Plaintiff has well pled, however, that the Board level review was not divorced from Musk’s influence. Entire fairness, therefore, must abide.

The Vice Chancellor held that the defendants were unable to establish that the award was entirely fair at the pleading stage, so he declined to dismiss the plaintiff’s breach of fiduciary duty & unjust enrichment claims. That probably means I’ll have to blog about Musk again at some point in the not-too-distant future. Lucky me.

SEC Settles Nissan Fraud Charges: Don’t Have the CEO Set Their Own Pay!

It’s been a big week for CEO compensation stories. Here’s something Liz blogged earlier this week on CompensationStandards.com: Wow. Broc & I have blogged a couple of times over the past year about the SEC’s Nissan investigation, which (among other reasons) is of interest because Nissan is a Japanese company, and also because of the bold efforts people took to conceal former CEO Carlos Ghosn’s pay.

Yesterday, the SEC announced that it settled Section 10(b)/Rule 10b-5 fraud charges with Nissan, Ghosn, and a former director/HR exec for omitting $140 worth of Ghosn’s compensation from Japanese securities filings – which were published in the US because the company’s securities trade as ADRs on the OTC – and which required information about executive pay. Allegedly, Ghosn went to all this effort to restructure & hide his pay because he was worried that people would criticize the amounts (pro tip: at least in the US, that’s a hint that you’re probably required to disclose the info).

Nissan is ponying up $15 million – while the individuals are getting off with civil fines of $1 million and $100k. Seems like a pretty good deal for those two, based on the allegations in the SEC’s complaint against them – e.g., Ghosn first brainstormed ways to conceal part of his pay by paying it through Nissan-related entities…when that didn’t work, he started entering into secret contracts with employees and executing backdated letters for LTIP awards, and decided that “postponing” pay (along with creative accounting) would get him around the disclosure obligations.

Initially, one problem here for the company might have been faulty internal controls. But according to the SEC’s complaint against the company, the fatal blow was that because Nissan had specifically delegated to Ghosn the authority to set individual pay arrangements – including his own! – he was acting within the scope of his employment when he intentionally misled investors, and the company was liable under the principles of respondeat superior. We can complain all we want about the burdensome listing rules here, but maybe they’re saving some companies from themselves…

Audit Reports: What Does Auditor Tenure Disclosure Look Like?

This Audit Analytics blog discusses the disclosures that accounting firms are including in their audit reports in response to the relatively new requirement to disclosure their tenure with a particular company. The blog says that although the PCAOB has provided guidance on determining & reporting tenure, “auditors have discretion regarding exactly what and how the information is disclosed, resulting in substantial variation in disclosures.”

Having reviewed the blog, I can assure you that auditors have used their discretion to ensure that all versions of tenure disclosure are extremely boring.

This Stinson blog highlights rule changes that could prompt a few tweaks to D&O questionnaires. Specifically, the blog notes that:

– Companies can now rely on Section 16 filings & written representations to determine whether an insider has delinquencies. As a result, companies may ask whether all required Section 16 reports have been filed on EDGAR instead of asking whether all of those reports have been provided to it.

– If Nasdaq’s proposed changes to the definition of the term “family member” are approved, Nasdaq-listed companies may want tweak the definition contained in their D&O questionnaires to reflect the changes.

The blog also urges companies to be cautious about eliminating references to Section 162(m) in D&O questionnaires for compensation committee members unless it’s clear that the committee isn’t required to administer any compensation arrangements under the transition rule.

Stinson’s blog is a reminder that although it may seem like proxy season just ended, it’s actually right around the corner. And to help you get ready, we’ve already scheduled our “Pat McGurn’s Forecast for 2020 Proxy Season” webcast for January 16th.

Today’s Open Commission Meeting: Cancelled

The SEC has cancelled the open meeting that it had previously scheduled for today to consider, among other things, adopting its “test the waters” for all proposal. No word on rescheduling yet.

I don’t know if this had anything to do with the decision to cancel the meeting, but all 5 Commissioners were grilled for several hours yesterday by the House Financial Services Committee. Committee Chair Maxine Waters (D – Cal.) opened the hearing with a statement that accused the SEC of “not fulfilling its mission as Wall Street’s cop.” No doubt a good time was had by all.

ESG: Investors Want Companies to Align with Paris Climate Goals

According to this Ceres press release, a group of 200 socially conscious institutional investors with more than $6.5 trillion in AUM sent a letter to 47 large public companies asking them to align their climate change lobbying activities with the Paris Agreement’s goal of limiting global temperature increase to less than 2° C and pursue efforts to hold it at 1.5° C.

The group’s letter doesn’t just address the lobbying activities of the individual companies – it also calls upon them to review those of any trade associations to which they belong and engage with the organization if its activities are inconsistent with the Paris Agreement’s goals. If companies are unable to persuade the association to modify its position, then the signatories ask that they “consider taking the steps necessary to disassociate your company from these policies.”