Yesterday, the SEC issued this Section 21(a) report about companies with deficient internal controls – in particular, nine unnamed companies that became victims of a cyberfraud called “business email compromises.” This fraud entails employees receiving spoofed or otherwise compromised electronic communications – and in response, employees wired large sums of money or paid fake invoices to the tune of at least $1 million. Two of them lost more than $30 million! Losses for the nine companies totaled nearly $100 million, almost all of which has not been recovered – and some of the frauds lasted a long time & weren’t discovered until the real vendor complained they hadn’t been paid yet.

As noted in this article, there were two kinds of business email compromises — emails from fake executives and ones from fake vendors. In schemes involving emails from fake executives – also called “executive impersonation” – fraudsters not affiliated with a company use spoofed email addresses to send communications that appeared to come from a company executive, typically the CEO. Sometimes, the spoofed emails used real law firm and attorney names. The executive impersonation emails often had these common elements:

1. Referred to time-sensitive “deals” that needed to be completed within days, emphasizing the need for secrecy from other company employees and sometimes suggested some form of government oversight.

2. Claimed that the requested funds were needed for foreign transactions – and all directed the wire transfers to foreign banks. The emails provided minimal details about the transaction – and while all of the companies had some foreign operations, these types of foreign transactions would have been out of the ordinary.

3. Typically went to mid-level personnel who rarely communicated with the executives being spoofed – and who typically were not involved in the supposed transactions.

4. Often included grammatical errors. Hint, hint.

Meanwhile, see this blog about how courts are wrestling with insurance coverage for cyber-related claims…

Governance Stats: Silicon Valley v. S&P 100

This Fenwick & West study surveys the landscape of Silicon Valley’s governance practices and compares them with those found at S&P 100 companies. Not surprisingly, the study found significant differences between Silicon Valley and Corporate America. Here are some highlights:

Annual Meeting Participation:

– An average of approximately 89.1% of shares of SV 150 companies was represented in person or by proxy at company annual meetings during the 2018 proxy season, similar to 2016. However, in addition to the approximately 10.9% not represented, an additional 14.5% were represented via proxy by brokers who did not receive instructions on voting for the bulk of matters for which broker discretionary voting is not permitted. This compares to 12.8% not represented and 13.9% broker non-votes in the S&P 100 in the same period.

– The ranges of representation and voting, though, were somewhat broader in the SV 150 than the S&P 100 (e.g., 52.9% –100% voting in the SV 150, compared to 71.3% – 93.9% voting in the S&P 100).

Director Elections:

– In the vast majority of cases, the elections of directors continue to be uncontested. One of the SV 150 companies and two of the S&P 100 companies had a contested election at its annual meeting in the 2018 proxy season (compared to one in each group in 2017).

– In the SV 150, the dissident stockholder was able to elect two of the three candidates sought.

– In the S&P 100, the dissident was able to have its candidate appointed after very narrowly losing the stockholder vote at Procter & Gamble, and Broadcom was forced to withdraw its slate at the 11th hour following CFIUS review.

Say-on-Pay:

– Opposition to named executive officer compensation reached 15% or more of votes cast (ignoring abstentions and broker non-votes) at 22.8% of SV 150 companies (compared to 13.8% of S&P 100 companies). Within those SV 150 companies with relatively lower levels of support, opposition reached 30% or more at 15 companies (of which nine had opposition of 40% or more, including seven companies where opposition exceeded 50%).

Other Proposals Voted On:

– Setting aside director elections, say-on-pay (as well as say-on-frequency) and auditor approval voting, stockholders at SV 150 companies were asked to vote on one other matter on average, while stockholders at S&P 100 companies averaged 2.5 other matters voted on. The difference is primarily driven by the fact that stockholder proposals are primarily a large company phenomenon. There were only four such proposals voted on by stockholders outside of the top 50 companies in the SV 150.

Company Proposals:

– Excluding director elections, say-on-pay (as well as say-on-frequency) and auditor approval voting, stockholders at SV 150 companies voted on 86 company-sponsored proposals in the 2018 proxy season, primarily in compensation-related subjects, as well as some governance matters (compared to 56 such proposals at S&P 100 companies).

Stockholder Proposals:

– The stockholder-sponsored proposals voted on in the SV 150 generally focused on governance matters or policy issues (this was also true in the S&P 100).

– The average support for stockholder-sponsored proposals was approximately 31.9% at the SV 150 companies (compared to approximately 27.3% at S&P 100 companies).

– The most common topic for stockholder-sponsored proposals in the SV 150 were proxy access (eight proposals, two of which succeeded) and anti-discrimination/diversity (eight proposals, none of which were successful).

– The most common such topic in the S&P 100 was regarding political/lobbying activities (31 proposals, none of which succeeded).

In a speech on Friday, Assistant Attorney General Brian Benczkowski of DOJ’s Criminal Division announced a newly updated policy to guide the Division’s decision-making on whether to require a monitor as part of a corporate criminal resolution. The updated policy codifies the principle that imposing a corporate monitor should be “the exception, not the rule.” Specifically, the policy requires a cost-benefit analysis, directing that a corporate monitor be imposed only where there is “a demonstrated need for, and clear benefit to be derived from,” a monitor when compared to the costs and burdens to the corporation. A monitor “will likely not be necessary” if a corporation’s compliance program is “demonstrated to be effective and appropriately resourced at the time of resolution.”

The new policy also mandates that, where a monitorship is imposed, its scope should be “appropriately tailored to address the specific issues and concerns that created the need for the monitor.” To ensure suitable tailoring, Criminal Division agreements must now include an explanation of the monitorship’s scope, along with a description of the process for replacing a monitor, if necessary. And AAG Benczkowski emphasized that Criminal Division prosecutors have an ongoing obligation to ensure that monitors are acting properly and effectively by “operating within the appropriate scope of their mandate.”

In the same speech, AAG Benczkowski announced that the Criminal Division will eliminate the position of compliance counsel – a role created to some fanfare in the last administration – citing the institutional limitations of relying on a single person as the repository of compliance expertise. But AAG Benczkowski hastened to emphasize that assessment of the compliance function will continue to be a key consideration in every corporate enforcement matter. Rather than hiring a new compliance counsel, the Criminal Division will institute a hiring and training program to cultivate “a workforce better steeped in compliance issues across the board.” Accordingly, this change does not signal a shift in DOJ’s approach to corporate enforcement nor does it diminish the importance of maintaining an effective compliance program.

Since I’ve been blogging so much about Edgar outages (here’s the latest), I decided to get a little more educated about the state of play for Edgar. About a year ago, the “Edgar Business Office” was created. This new office will eventually house “nearly everything Edgar” – including “Edgar Filer Support.” Among other things, the new “Edgar Business Office” is responsible for two main tasks: existing Edgar functions, as well as an Edgar redesign that will take several years to complete.

As for Edgar outages, my primary beef has been a lack of transparency as to when Edgar is down – and when it is back to being operational. As I understand it, this problem is more complicated than I realized. When Edgar is down, it might be just for a few companies (meaning Edgar works for most companies; but not all) – and it might be just for a few minutes. Another challenge for the SEC is that it might take them a little while to realize the magnitude of the problem. So you’re encouraged to contact “Edgar Filer Support” to report a problem.

Given all that, I can see how it would be challenging for the SEC to keep us apprised of what is happening with Edgar – unless there was such a big shortage that it would be apparent (and clearly material to our community as a whole). But there is good news! The SEC has started posting notices when Edgar problems impact the ability of filers to access Edgar – and when they are resolved. These notices are being posted on this “Edgar Systems Announcements” page…

For what it’s worth, this recent update to the “Edgar Filer Manual” addresses warning messages for incorrect XBRL tags, preventing the system from retrieving & exposing a return copy of a test or live submission…

More on “Do You Read Footnotes?”

Recently, I blogged about whether it’s okay to use footnotes when you write. I received many responses from members – and the poll that I ran was popular: 35% said they read them only when they’re in the mood; 41% always read them; 18% only read them for court opinions & SEC releases (no one never reads them – and 7% selected the joke answer of wishing their significant other had the temperament of a footnote).

One member shared the sage advice of his civil procedure professor at Cornell Law – the late & incomparable Rudolf Schlesinger – delivered with a wagging index finger: “The children of lawyers who do not read footnotes will starve.” And Allen Matkins’ Keith Bishop wrote this blog about whether it’s legal to use footnotes…

Will Google Face a SEC “Cybersecurity Disclosure” Enforcement Action?

Over the past few years, the SEC has conducted a number of cybersecurity disclosure investigations – but not much has come out of that other than last year’s action against Yahoo. As detailed in this blog by John Stark, perhaps that will change due to the circumstances involving a data breach at Google…

Steven’s book (“The CEO Pay Machine“) is an easy-to-read & entertaining dissection of how we got to where we are – and how we can fix it. His book is laden with stories that really “tell it like it is.” Please check it out & tell others that can help make a difference…

Tune in tomorrow for the webcast – “Proxy Solicitation: Nuts & Bolts” – to hear Morrow Sodali’s Tom Ball, Strategic Governance Advisors’ Mark Harnett, Kingsdale Advisors’ Lydia Mulyk and Alliance Advisors’ Reid Pearson discuss the art of proxy solicitation in this activism-heightened world.

ISS & CII Team Up Against Proxy Advisor Reform

As noted in this Davis Polk blog by Ning Chiu, ISS & CII recently teamed up to create “Protect the Voice of Shareholders” in an effort to oppose H.R. 4015, the ‘Corporate Governance Reform and Transparency Act,’ that passed the House last October (but never got further than that).

For the last four years, the US Chamber of Commerce & Nasdaq have partnered to survey corporate views of proxy advisors. The latest results – from 165 participating companies – come just in time for the SEC’s upcoming ‘proxy process’ roundtable. Here’s a sampling:

– 92% of companies surveyed had a proxy advisor make a recommendation on an issue featured in their proxy statements, nearly identical to 2017, but an 11% increase over 2016.

– 83% of companies carefully monitor proxy advisors’ recommendations for accuracy or reliance on outdated information.

– 21% of companies surveyed formally requested previews of advisor recommendations—a 9% decrease from 2017, but little changed from 2016. For companies that requested a preview, proxy advisory firms provided them only 44% of the time, a 4% drop from 2017.

– 38% of companies asked proxy advisors for opportunities to provide input both before & after the firms’ recommendations were finalized. However, as in previous years, the amount of time companies were given to respond to the recommendations varied. Companies again reported being given anywhere from 30 to 60 minutes to two weeks. In 2018, 1 to 2 days was a common response among companies.

– 39% of companies believed that the proxy advisors carefully researched and took into account all relevant aspects of the particular issue on which it provided advice, up from 35% in 2017.

– 29% of the companies pursued opportunities to meet with proxy advisors on issues subject to shareholder votes, a significant decrease from 52% in 2017. Of those companies that sought a meeting, their request was denied 57% of the time, significantly more often than in 2017. Companies reported mixed results from meetings they had.

– One perceived problem with the proxy advisory system has been a trend toward “robo-voting” where a company’s outstanding shares are voted in line with an ISS or Glass Lewis recommendation in the 24-hour period after the recommendation is issued. With ISS, several companies reported that 10%-15% of their shares would vote automatically in line, while others estimated that between 25%-30% fell into that category. The problem seemed to be less apparent with Glass Lewis, with many companies reporting that less than 10% of their shares would be voted in line within 24-hours.

Quarterly Reporting: SEC Chair Says Here To Stay (For Now)

Back in August, John predicted that the latest push for semi-annual reporting wouldn’t go too far. Yesterday, SEC Chair Jay Clayton seemed to confirm that view for the near-term – except, perhaps, for a remote chance for smaller companies. That’s based on these remarks – reported in this WSJ article and this blog from Cooley’s Cydney Posner:

“I don’t think quarterly reporting is going to change for our top names anytime soon,” Clayton said. “It was good of the president to raise it,” he said, adding that it could make sense to ease the requirements for smaller companies….

“The President did touch on a nerve—which is ‘Are people running their companies too much for the short term in response to pressures?'” Clayton said in a brief interview after the event. “We’ve been hearing that for a while.” …While Clayton lauded Trump and others for raising the issue, he said that other factors like activist investing are also behind companies becoming more focused on the short term.”‘I would not say the driving factor is quarterly reporting.”

Across the Pond: New Governance & Reporting Requirements

From the land of the “original” say-on-pay, the UK is now revamping its “Corporate Governance Code” to encourage the long-term success of its businesses – and improve public confidence following some high-profile scandals. This WSJ blog summarizes a few of the enhanced “comply or explain” requirements:

– Vesting & holding period of 5 years or more for shares awarded to executives under long-term incentive plans

– Disclose when board chair’s tenure exceeds 9 years

– Disclose how the company’s approach to corporate governance contributes to long-term success

– Address cases in which more than 20% of shareholders vote against a management proposal

– Enhance workforce engagement – e.g. by creating an advisory panel

– Describe the nominating committee’s process, the board’s diversity policy and the gender balance of senior management

The code applies to companies listed in the premium segment of the London Stock Exchange – they’ll need to start complying in January. And although the revisions don’t add specific diversity targets or require companies to disclose broader diversity stats, that’s under consideration. This article notes that the UK’s Financial Reporting Council isn’t happy with the status quo and has been contacting companies to encourage more disclosure – though some people worry that will lead to useless boilerplate.

This Stinson Leonard Street blog highlights rule changes that could affect the upcoming proxy season. It says that most companies won’t need to make any changes to their D&O questionnaires for 2019 – though some might add questions on board diversity if the company wants to voluntarily explore that hot topic. In addition, the steady trickle of this year’s SEC guidance & rule changes means that there are plenty of things to watch out for outside of the questionnaires. Among other items, the blog delves into these topics:

– 162(m) disclosures

– Impact of changes to smaller reporting company rules

– Inline XBRL

– Changes to Form 10-K cover page

– Impact of SEC’s disclosure simplification

– Perks disclosures

– Cybersecurity disclosures

As you’re preparing for proxy season, don’t forget to tune in Tuesday, October 16th for the webcast – “Proxy Solicitation: Nuts & Bolts” – to hear a panel of experts discuss the role of proxy solicitors and whether they can help predict activist campaigns. And we’ve already scheduled two January webcasts to help you conquer this crazy time of year:

Investor Meetings: They Aren’t Going As Well As You Think?

Here’s your chance to be a hero and offer practical client advice that doesn’t just reduce risk, but gets money in the door. This blog from Adam Epstein offers a buy-side perspective on why investor meetings chronically falter – even if companies think they’re going well. For example, everyone’s favorite PowerPoint deck might be doing more harm than good. Here are a few tips for improving it:

– Length: Smart investors know that the length of a PowerPoint presentation is often inversely proportional to the quality of the company. Aim for less than 20 slides. Precedent matters, and the number of great small-cap companies with ~ 25+ page decks is not high.

– Information Weighting: Executive bios, market data, service/product description, intellectual property, strategy, risks, competitors, financials, and use of proceeds slides should all be evenly distributed. When key information isn’t equally weighted (e.g., 35%+ of the slides are about the market opportunity), investors know there is a reason why…and it’s never good.

– Accessibility: Investors marvel at why so many companies make their investor presentations so challenging to find on their websites. Always follow the two-click rule for information investors most want: the information should never be more than two-clicks away from the company’s home page. When investors have to try hard to find basic information, it sends a bad message.

More on “The Mentor Blog”

We continue to post new items daily on our blog – “The Mentor Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Chart: Rule 144

– Insider Trading Policies: Addressing “Cyber” Info

– Sustainability Progress: “The Devil’s In The Details”

– What Does an “Interested Directors Statute” Do for You?

– Insider Trading: “Big Data” – Big Problem?

As I blogged today in this “Proxy Season Blog,” shareholder support of corporate political spending proposals increased to 28% this year – which is an 8% increase since 2014. With that in mind, here are results from our recent survey on political spending oversight:

1. Oversight of our company’s political spending is conducted by:

– Full board – 13%

– Board committee – 58%

– Committee consisting only of management – 8%

– Individual officer – 17%

– Other – 4%

2. For those overseeing political spending, the type of information they get regarding actual contributions is organized by:

– Individual contributions – 38%

– Particular contributions (e.g. sensitive races or large amounts) – 0%

– Aggregate breakdown (e.g. total annual amount, amount by type of election, political party breakdowns, etc.) – 46%

– No information is provided about actual contributions – 17%

3. If the board or a board committee is involved, their role is primarily:

– Ensure the process is sound from a governance perspective – 55%

– Ensure there is a process & that it’s followed – 36%

– Provide input on the amount or type of contributions – 0%

– Maximize the likelihood that contributions will be consistent with the company’s mission – 9%

Please take a moment to participate anonymously in these surveys:

We haven’t heard as much about proxy access this year. But it’s covered on page 38 of this 110-page report from Shearman & Sterling – which has lots of interesting info about governance provisions & disclosure, executive pay and proxy season trends.

As many have discovered first-hand, it’s an uphill battle to resist shareholder requests to implement proxy access: 90% of companies that received “adopt” proposals in 2015-2018 ended up doing so. And although there’s been a big drop in the number of these proposals, that’s partly because 67% of the S&P 500 and 89 of the largest 100 companies now have a proxy access bylaw in place. Here are some other stats:

– 53 companies adopted proxy access during the 2018 proxy season – compared to 87 during 2017

– Only 22 “adopt” proposals were received this season compared to 100 last year – due to a greater number of companies choosing to voluntarily adopt proxy access and shareholders switching their focus from “adopt” to “fix-it” proposals

– Only 28 “fix-it” proposals were received this season compared to 64 last year – but shareholders continue to advocate for changes to details in proxy access bylaws, as well as restrictions on the shareholder aggregation cap, renominations and the percentage of directors electable via proxy access

– From 2016-2018, only 2 of 103 “fix-it” proposals passed – and those were at companies that used a 5% minimum percentage ownership threshold. However, 37 companies have amended their proxy access bylaws during that time period – which might suggest behind-the-scenes pressure.

– More than 900 meetings have been held by companies with a proxy access bylaw since 2011. Only 1 nomination has been attempted using proxy access – and zero proxy access candidates have ultimately appeared in a company proxy statement

Transcript: “Nasdaq Speaks”

We have posted the transcript for our recent webcast: “Nasdaq Speaks – Latest Developments & Interpretations.”

As a look-back on their first full year as Co-Directors of the SEC’s Division of Enforcement, Stephanie Avakian gave this speech – and Steve Peikin gave this speech – to recap their accomplishments. Stephanie’s speech expands on Enforcement’s “Guiding Principles” for investor protection – and emphasizes that statistics showing a decline in the number of enforcement actions don’t adequately reflect the quality of their efforts. Instead, the goal is to use limited resources to bring “meaningful cases that send clear & important messages.” Here’s the intro:

Last year Steve and I articulated five principles that would guide our decision-making. They are: (1) focus on the Main Street investor; (2) focus on individual accountability; (3) keep pace with technological change; (4) impose sanctions that most effectively further enforcement goals; and (5) constantly assess the allocation of our resources.

I’m going to talk about the Division’s approach to dealing with initial coin offerings (ICO) and digital assets, and second, I will address the Division’s Share Class Selection Disclosure Initiative. These two examples illustrate our approach of identifying challenges and risks facing investors and markets, and developing a response that addresses those challenges in a thoughtful and effective way, and that maximizes our use of resources.

In the context of ICOs, she goes on to discuss non-fraud enforcement actions for ICO registration cases – and says Enforcement isn’t going to shy away from recommending substantial remedies for Section 5 violations. And as I’ve previously blogged, it’s not just issuers who can be the target of an ICO enforcement action. Recent settlements included a hedge fund that violated investment company registration requirements and an unregistered broker dealer.

SEC Enforcement: “Money Isn’t Everything”

John’s blogged that the magnitude of monetary penalties might not be the right way to measure enforcement activity – and Steve Peikin seems to agree. In his recent speech, he elaborated on the full range of relief that the Division of Enforcement recommends to the SEC – and says Theranos is a good example of how customized non-monetary remedies are deployed:

Aspects of the Theranos matter have been covered extensively in other forums. But for today’s purposes, one of the most important elements of the Commission’s settlement with Holmes were undertakings that (1) required her to relinquish her voting control over Theranos by converting her supermajority shares to common shares, and (2) guaranteed that in a liquidation event, Holmes would not profit from her ownership stake in the company until $750 million had been returned to other Theranos investors.

In Theranos, the Commission confronted a situation where, because of the capital structure of the company, Holmes had nearly complete control of the company. And given what we alleged had occurred, it was appropriate to seek relief that protected investors from potential misuse of that controlling position going forward. The undertakings were designed to do exactly that.

Tomorrow’s Webcast: “This Is It! M&A Nuggets”

Tune in tomorrow for the DealLawyers.com webcast – “This Is It! M&A Nuggets” – to hear Weil Gotshal’s Rick Climan, Arnold & Porter’s Joel Greenberg, McDermott Will’s Wilson Chu and Sullivan & Cromwell’s Rita O’Neill impart a whole lot of practical guidance!

Our last “list” blog featured Nina Flax’s morning routine. Now we get to see how Karla Bos starts her day:

OK, here’s the “Bos” edition of the pre-8:30 am accomplishment list. Very different from Nina’s, aside from the requisite coffee and email consumption, but that’s no surprise—she’s a Commuting Supermom and I’m a Work-from-Home Empty Nester. My list looked more like hers when I had a commute and kids at home.

Even so, reflecting on my current list, I realized that 10 years ago I would have read it and totally rolled my eyes, wondering what working person could find the time for all this in the morning and get up so many hours before they really had to. All I can say is that I started to get up earlier and earlier over the years as it dawned on me that doing so allowed me to take control of my day and take care of myself in a meaningful way. So for me, where I am now, this program works:

1. Decide Whether Sleep Will Come Again After 4 a.m. I’ve learned that, as soon as one of my three dogs whimpers or my monkey mind starts jumping, going vertical bears more fruit than chasing a few extra and unlikely minutes of sleep. But if the dogs are quiet, I hold off so the husband can sleep.

2. Get Up by 4:45 a.m. I don’t say “wake up” because I am almost always awake by then. Sometime during the last 10 years I turned into a morning person.

3. Take Dogs Outside. Scan the yard and stand guard for predators (hence, no doggie door) while my little dogs sniff everything as if for the first time. “Oh tree, how I’ve missed you!” I take a moment to enjoy the early morning desert quiet—until the senior dog barks to announce we can go in NOW …

4. Feed the Dogs. For age and health reasons, everyone gets their own custom menu with varying levels of meds and supplements. Start my coffee. Encourage the puppy to eat instead of play.

5. Take Dogs Outside Again. And generally repeat a slightly faster version of step #3. If it’s light enough by now I putter in the yard and make a mental list of what needs attention.

6. Set Out Coffee for My Husband. He’s in the shower about now. He is much less of a morning person (and less of a talker) than I and has a healthy commute. We used to carpool when we worked at the same company, which I thought was great because I could talk and talk and check my email while he drove—but I think he enjoys the quiet time now.

7. Coffee/Digital Content Intake. This means distracting the dogs with dental chews while I drink coffee, check email, and read to get a little smarter about corporate governance and the world. Being in Arizona, I share Nina’s challenge of waking up to east coast days that are already in full swing. Fortunately, our geographically distributed and highly responsive team helps make the time zone balancing act manageable.

8. Throw on Workout Clothes. This is one of the times I listen to a favorite podcast. Once I’d worked from home for a while, I realized I’d stopped doing this, so now I catch up here and there in the morning and whenever I step out of my office for a break.

9. Exercise and Stretch. Some days this means a full-on workout (Empty Nester = spare room for a home gym), some days mostly stretching (which I don’t love because I am not flexible, so podcasts are a great distraction), but it’s a must. It’s key to managing stress, aging, and too much time sitting. Drink water.

10. Check Email.

11. Walk the Dogs. The desert gear required is a separate list but includes big floppy hat, tweezers to remove cactus spines, and a whistle and pepper spray to fend off any aggressive wildlife (which usually keep their distance, but we had a dicey encounter with a group of javelinas and we see coyotes most mornings). Also a headlamp when it’s still dark. Enjoy the stillness and quiet but watch for predators. (You get used to it, rather like walking the streets of NY.)

12. Check Email.

13. Brush Dogs’ Teeth. Owners of small dogs know they require dental vigilance or things get ugly and pricey. Another chance to listen to podcasts.

14. Shower—and Sing! Singing in the shower is another must. Really gets me energized, and I cannot think (worry) about anything when I am belting out a showtune.

15. Meditate for 10-15 Minutes. Mindfulness meditation, which I’m new at, but feels really valuable. One time in the day I don’t make mental lists (well, try not to; like I said, I am new at this).

16. Get Dressed. While I love that this takes far less time and effort now that I work from home, it’s still important to set and adhere to standards, e.g., anything you slept or worked out in is not suitable work attire, and you’re not trying hard enough if your husband comes home and looks startled when he sees you.

17. Eat a Healthy Breakfast. Admittedly this happens at my desk if the preceding 16 activities expanded.

18. Commute to Work. There are things I miss about working onsite with a team, but I adore that my commute simply means walking down the hallway to my home office, where the dogs settle in for a snooze. Power up and get to work!

Nasdaq Proposes Changes to Initial Listing Liquidity Requirements

On Friday, Nasdaq announced that it’s seeking public comment on potential changes to its liquidity requirements for new listings. While all input is welcome, the proposal identifies four topics of particular interest:

– Restricted Shares

– Minimum Investment Value for Holders

– Trading Volume

– Reg A+ Listings & SPACs

Any changes to the rules will apply only to initial listings – not continued listings. Comments are due by November 16th.

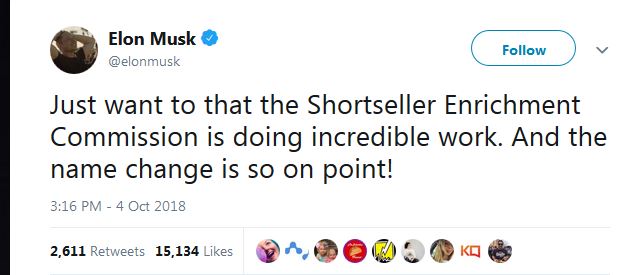

Less than a week into his settlement with the SEC over alleged securities law violations relating to his tweets, Tesla CEO Elon Musk took to Twitter to voice his displeasure with the SEC with this tweet:

Interestingly, in a speech that Liz will blog about next week, Steve Peikin – Co-Director of the SEC’s Enforcement – noted a few days ago that one of the remedies that the SEC obtained is a requirement that Tesla add an experienced securities lawyer to its legal department (see the 4th undertaking associated with fn 8; note that requirement wasn’t noted in the SEC’s press release). I can tell you that Tesla has had one of those already for years. And it doesn’t strike me that Musk is the kind of guy that will listen to his lawyers…

According to news reports, Mark Cuban urged Musk to settle. You may recall that Cuban battled the SEC for years over alleged insider trading – and then Cuban even showed up at the annual “SEC Speaks” conference afterwards. And I even had my own touch of fame after I blogged about Cuban’s settlement and he tweeted at me…

New “Disclosure Simplification” Rules: Effective November 5th

Yesterday, the SEC’s “Disclosure Simplification” rules were published in the Federal Register. They’ll be effective November 5th. I blogged last week about transition issues. We continue to post memos in our “Fast Act” Practice Area…

Group of Investors Files “ESG Disclosure” Rulemaking Petition

Recently, as noted in this press release, a group of investors, state treasurers, public pension funds & unions – representing more than $5 trillion in assets under management – and securities law experts and foundations filed this rulemaking petition with the SEC seeking a standard set of rules requiring companies to disclose environmental, social and governance (ESG) risks.

There were many signatories to this petition. Does that matter? Personally, I don’t think so. Unless they happen to align with the SEC Chair’s rulemaking agenda anyway, rulemaking petitions rarely are acted upon. Remember the rulemaking petition about political contribution disclosures that received over 1 million signatures in support that has gone nowhere…

Certain ISS policies, procedures, and products rely on GICS classifications, including executive compensation peer group formation, equity compensation plan evaluation, and Environmental & Social QualityScore. ISS has issued FAQs designed to answer the most frequently asked questions regarding how the adjustment to GICS structure will impact ISS analyses, and when those changes will be effective.

The FAQs address the following questions:

– How will the new GICS code affect the evaluation of equity compensation plans under ISS’ U.S. Equity Plan Scorecard?

– How will the new GICS code affect the evaluation of equity plans under ISS’ burn rate policy for France?

– How will the new GICS code affect the evaluation of executive compensation?

– How will the new GICS code affect the evaluation of director compensation?

– How will the new GICS code affect Environmental & Social QualityScore?

– How will the new GICS code affect ISS policies, such as the director performance evaluation policy, that examine a company’s TSR performance relative to its industry?

– When will Question 130 in Governance QualityScore, which examines each covered company’s burn rate relative to its industry, be updated to reflect the new GICS structure?