We’ve blogged a few times about Vanguard’s updated proxy voting guidelines and the impact they might be having on recent climate change proposals. We shouldn’t overlook that Fidelity’s also joined the party. Here’s an excerpt from its updated “Proxy Voting Guidelines,” which were previously silent on environmental & social issues:

FMR generally will vote in a manner consistent with management’s recommendation on shareholder proposals concerning environmental or social issues, as it generally believes that management and the board are in the best position to determine how to address these matters. In certain cases, however, Fidelity may support shareholder proposals that request additional disclosures from companies regarding environmental or social issues, where it believes that the proposed disclosures could provide meaningful information to the investment management process without unduly burdening the company.

For example, Fidelity may support shareholder proposals calling for reports on sustainability, renewable energy, and environmental impact issues. Fidelity also may support proposals on issues such as equal employment, and board and workforce diversity

I blogged a few weeks ago about the historic climate change proposal at ExxonMobil – it passed with 62% support. BlackRock voted in favor of the proposal, and this vote bulletin explains why. Here’s a teaser:

The BlackRock Investment Stewardship team has identified climate risk disclosure, in line with the Task Force on Climate-related Financial Disclosures (TCFD), as one of our five engagement priorities for 2017-18.

In the past year, we’ve engaged more directly on Exxon’s reporting of climate-related risks. We have also engaged with the shareholder proponents to better understand their views. We believe it is in long-term shareholders’ best economic interests for Exxon to enhance its disclosures. We therefore voted in favor of the shareholder proposal focused on the 2-degree Celsius warming target (the “2-degree scenario”) as outlined in the Paris Agreement under the United Nations Framework Convention on Climate Change.

In addition, we have repeatedly requested to meet with independent board directors over the past two years to better understand the board’s oversight of the company’s long-term strategy and capital allocation priorities amidst major strategic challenges and regulatory inquiry (including but not be limited to oversight of climate risk). The company declined to make directors available, citing a non-engagement policy between independent board members and shareholders.

So a couple takeaways here are – first, to understand your shareholders’ priorities – and second, if a key shareholder asks to meet with directors…make it happen. Last week’s blog has some tips on both of these topics.

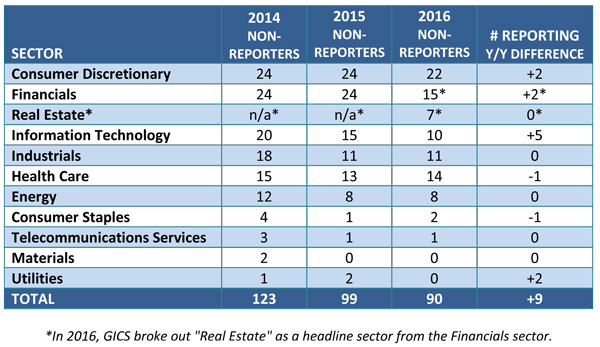

Sustainability Reports: Published by 82% of the S&P 500

This recent Governance & Accountability Institute study found that 82% of the S&P 500 are publishing a sustainability or corporate responsibility report. Up from 20% just 5 years ago! Here’s a chart that shows the declining number of non-reporters by industry:

At our “Women’s 100” Conferences, we heard from some institutional investors who look at sustainability as a risk issue – and not one that applies just to extractive industries. They want to understand what the company’s doing to stay competitive for years to come. You can share this info in your proxy statement in the absence of a full-blown sustainability report, but still check out Clorox’s “Integrated Report” – it’s a cool example & shows what types of topics to cover. We have even more resources in our “ESG” Practice Area. And tune in for our October 10 webcast – “E&S Disclosures: The In-House Perspective” – featuring experts from the Coca-Cola Company, Bristol-Myers Squibb, Apple & Clorox.

Last week, John blogged about evolving MD&A disclosures under the new revenue recognition standard. Check out this SEC Institute blog for more examples of early adopters – Alphabet, Ford, Raytheon & others. Here’s an excerpt from First Solar’s Form 10-Q:

We adopted ASU 2014-09 in the first quarter of 2017 using the full retrospective method. This adoption primarily affected our systems business sales arrangements previously accounted for under ASC 360-20, which had required us to evaluate whether such arrangements had any forms of continuing involvement that may have affected the revenue or profit recognition of the transactions, including arrangements with prohibited forms of continuing involvement. When such forms of continuing involvement were present, we reduced the potential profit on the applicable project sale by our maximum exposure to loss.

With 6 months till the new revenue recognition standard is required, only about 20 companies in the Russell 3000 have adopted it. This blog from Audit Analytics shows as-reported progress towards adoption & provides industry-specific examples of revenue streams that are likely to be materially affected. It also cautions that the SEC is commenting on transition disclosure that’s too generic. Here’s an excerpt from a recent letter:

You state that you are in the process of evaluating the impact that the amended revenue recognition guidance in Topic 606 will have on your consolidated financial statements. Please revise to provide qualitative financial statement disclosures of the potential impact that this standard will have on your financial statements when adopted. In this regard in your next filing, include a description of the effects of the accounting policies that you expect to apply, if determined, and a comparison to your current revenue recognition policies. Describe the status of your process to implement the new standard and the significant implementation matters yet to be addressed. In addition, to the extent that you determine the quantitative impact that adoption of Topic 606 is expected to have on your financial statements, please also disclose such amounts. Please refer to ASC 250-10-S99-6 and SAB Topic 11.M.

Canada Tries for Single-Regulator Framework: Now Doomed?

This Blakes memo notes that the Quebec Court of Appeal ruled against Canada’s proposed nationwide framework for securities regulation – finding part of it unconstitutional because it infringes on provincial sovereignty. This ruling might delay implementation, which was planned for next June. Here’s some thoughts on next steps:

One option is to push ahead with implementing the Cooperative System in a form modified to address the Council’s powers that the Court of Appeal identified as incompatible with parliamentary sovereignty and the division of powers between the federal and provincial governments.

Another, and more likely, option is for the federal government to seek the Supreme Court of Canada’s (SCC) opinion on the Cooperative System. If it chooses this option, the federal government could either appeal the Quebec Court of Appeal’s decision to the SCC or direct a separate reference to the SCC. The SCC’s decision would take precedence over that of the Quebec Court of Appeal.

At the risk of depressing our resident “Annual Meeting Fanboy” – this Joe Nocera article is notable just because the mainstream media doesn’t report much on the state of annual meetings. Joe attended four meetings – in a single day! – as background for his piece.

He suggests annual shareholder meetings aren’t what they used to be (and perhaps they never really did have much value). No more free coffee! No more swag! Here’s an excerpt:

Look, I get why good-governance types want to prevent companies from holding online-only meetings. As my old friend Nell Minow, a long-time corporate governance expert, put it in an email, “I think the threat of looking unhappy investors in the eye and having to answer questions in person still makes a difference.” My Bloomberg View colleagues made a similar argument, among others, in an April 12 editorial.

But from what I can see, this reasoning, though sensible in theory, doesn’t reflect reality. None of the shareholders I’ve seen are likely to strike fear in a chief executive or board member. And shareholders who do have the clout to shake up a company, like Carl Icahn, hardly wait around for the annual meeting. They own enough stock to command private meetings with management.

Virtual-Only Meetings: CII Weighs In

Recently, Broadridge reconvened its “Committee for Best Practices for Annual Shareholder Meetings” in an effort to update its guidelines for virtual annual meetings since they’re five years old. Earlier this month, CII sent this letter to the Committee to reaffirm its opposition to virtual-only meetings.

New Lease Accounting: Parsing an Example

Beginning in 2019, under the FASB’s ASU 2016-02, companies will need to recognize assets & liabilities for operating leases (see these memos in our “Lease Accounting” Practice Area). This blog by Steve Quinlivan gives the following example:

Lessee enters into a 10-year lease of an asset, with an option to extend for an additional 5 years. Lease payments are $50,000 per year during the initial term and $55,000 per year during the optional period, all payable at the beginning of each year. Lessee incurs initial direct costs of $15,000.

At the commencement date, Lessee concludes that it is not reasonably certain to exercise the option to extend the lease and, therefore, determines the lease term to be 10 years. Lessee also determines the lease is an operating lease.

The rate implicit in the lease is not readily determinable. Lessee’s incremental borrowing rate is 5.87 percent, which reflects the fixed rate at which Lessee could borrow a similar amount in the same currency, for the same term, and with similar collateral as in the lease at the commencement date.

At the commencement date, Lessee makes the lease payment for the first year, incurs initial direct costs, and measures the lease liability at the present value of the remaining 9 payments of $50,000, discounted at the rate of 5.87 percent, which is $342,017. Lessee also measures a right-of-use asset of $407,017 (the initial measurement of the lease liability plus the initial direct costs and the lease payment for the first year).

Lessee determines the cost of the lease to be $515,000 (sum of the lease payments for the lease term and initial direct costs incurred by Lessee). The annual lease expense to be recognized is therefore $51,500 ($515,000 ÷ 10 years).

At the end of the first year of the lease, the carrying amount of Lessee’s lease liability is $362,093 ($342,017 + $20,076; the $20,076 represents accrued interest on the lease liability), and the carrying amount of the right-of-use asset is $375,593 (the carrying amount of the lease liability plus the remaining initial direct costs, which equal $13,500).

As John blogged last week, Microsoft is voluntarily adopting the new lease standard on July 1st – you may be able to glean some pointers from their disclosure.

Yesterday, the SEC announced that Rob Evans will serve as a Deputy Director for Corp Fin – joining existing Deputy Director Shelley Parratt (Rob will head the “Legal & Regulatory Policy” side; Shelley will continue to lead “Disclosure Operations”). Rob comes to the SEC from Shearman & Sterling – he worked there with Corp Fin Director Bill Hinman before Bill moved to Simpson Thacher. Rob was also a colleague of former Corp Fin Director Linda Quinn.

SEC Commissioner Nominees: Hester Peirce Back in the Mix?

Broc blogged last year – and again a few months ago – about the nomination saga of Hester Peirce. Now – according to this Bloomberg article – her name’s reportedly returned to the top of the list for the open Republican seat at the SEC:

Hester Peirce, a former U.S. Securities and Exchange Commission counsel and Senate aide, is the Trump administration’s likely choice to fill the open Republican seat at the Wall Street regulator, according to people familiar with the matter.

Should President Donald Trump pick Peirce to be an SEC commissioner, her nomination will likely be paired with a candidate backed by Senate Democrats for another vacant seat at the agency, according to the people, who weren’t authorized to speak publicly about the process. Candidates that have been discussed for the Democratic spot include Robert Jackson, a Columbia University law professor, and Bharat Ramamurti, an aide to Senator Elizabeth Warren, the people said.

SEC’s Chief Accountant: Guidance for Audit Committees

A recent speech by SEC Chief Accountant Wes Bricker addressed how attention by audit committees to their core responsibilities can help promote the integrity of financial reporting & our capital markets. Here’s an excerpt from Ning Chiu’s blog:

– New Revenue Recognition Standard. Audit committees should understand management’s implementation plans and the status of the progress on the new revenue recognition standards, including any required updates to internal control over financial reporting. The audit committee should also communicate with auditors about any concerns the auditors may have regarding management’s application of the standard.

– Auditor Independence. Audit committees should “own” the selection of the audit firm, including making final decisions in the negotiation of audit fees. In its oversight of the audit relationship, audit committees must oversee auditor independence. The Office of the Chief Accountant (OCA) encourages audit committees and management to address independence questions with the SEC staff. If an auditor submits an independence matter to OCA, the SEC staff will sometimes reach out to the audit committee to understand its position.

The speech also touched on the PCAOB’s proposed changes to audit reports, which I blogged about earlier this month.

Recently, we held the 4th Annual “Women’s 100 Conferences” – in both Palo Alto & New York City. I’ve been attending these from the beginning & this year’s continued to live up to the hype! Here are 5 things I learned:

1. How To Know Your Shareholders: If you don’t have a centralized database to track notes from your shareholder engagement meetings (and your shareholders’ voting guidelines) – start one. Some companies have added this element to existing IR software – e.g. Ipreo. Others have a more basic approach. The bottom line is that institutional investors expect you to know where they stand on important issues. And they don’t want to rehash the same issues every year – you should just cover how their concerns have been considered or resolved. Your notes should also include your shareholders’ current contact procedures & preferences, which often change from year to year.

2. How To Know Your Potential Shareholders: We didn’t debate whether “the law of attraction” applies to shareholder engagement – but several people recommended thinking not only about your existing shareholders, but also the type of shareholders you’d like to get. This plays out in governance structures (e.g. single v. dual-class shares), environmental & social initiatives and your outreach efforts. Don’t overlook the communication value of your public disclosures for both existing & potential shareholders.

3. The Art of Using Directors in Off-Season Engagement: Shareholders might ask to meet with a director if there’s been a big strategic or executive pay change – or if there was low support for a company proposal at the annual meeting. They want to understand the board’s decision-making process & how it’s processing shareholder feedback. Directors can be really helpful, particularly if there are messages that are difficult to convey in a written proxy statement. But it’s extremely important to prep them on that shareholder’s policies & concerns – and how they relate to the company & its existing disclosures. Avoid cringe-worthy moments like “we just approved the pay package because the consultant recommended it.”

4. Icebreakers Work: Everyone introduced themselves at the beginning of both events – super helpful for anyone trying to connect with a particular person. On the West Coast, we all described our practice – but almost everyone’s was similar. On the East Coast, we had everyone say a “favorite” – book, movie, band, travel destination, etc. In addition to getting some good recommendations, I learned that this 10 minutes can really set the tone for the day. People were relaxed & jumped in with lots of questions during the panels.

5. We’re Building Community: I’ve always loved these conferences because the format encourages lots of interaction – you can meet heavy-hitters during speed-friending & connect over lunch with peers at the same career stage. So it was especially cool to talk with two women who are now close friends, after meeting at the conference a few years ago. We hope this becomes common!

Sights & Sounds: “Women’s 100 Conference ’17”

This 1-minute video captures the sights & sounds of the “Women’s 100” events that just wrapped up in Palo Alto & NYC:

The debate over voting rights (or lack thereof) wound up being the hottest issue of the proxy season. As Broc recently blogged, the debate over Snap’s dual-class structure continues. More recently, this Form S-1 filed by Blue Apron has created a stir. Here’s an excerpt that describes its triple-class voting rights:

We have two classes of voting common stock, Class A common stock and Class B common stock, and one class of non-voting stock, Class C capital stock. Each share of Class A common stock is entitled to one vote and each share of Class B common stock is entitled to ten votes. Shares of Class C capital stock have no voting rights, except as otherwise required by law.

Holders of Class A common stock and Class B common stock vote together as a single class on all matters (including the election of directors) submitted to a vote of stockholders, unless otherwise required by law. Upon the completion of this offering, the holders of the outstanding shares of Class B common stock will collectively have the ability to control the outcome of matters submitted to our stockholders for approval, including the election of our directors and the approval of any change in control transaction.

We are issuing shares of Class A common stock in this offering. The outstanding shares of Class B common stock are held by our executive officers, employees, directors and their affiliates, and certain other stockholders who held our capital stock immediately prior to this offering. The Class C capital stock is available for use for, among other things, strategic initiatives, including financings and acquisitions, and the issuance of equity incentives to employees and other service providers.

As described in this blog from Cooley’s Cydney Posner, Professor Charles Elson predicts that Delaware courts will be reluctant to apply the business judgment rule when there are multi-class structures like this. See this blog by Manifest for a UK perspective on multiple classes.

Pay Ratio: Odds of a Delay?

Here’s an excerpt from this blog by Steve Seelig & Puneet Arora of Willis Towers Watson:

If the SEC follows the lead of the Department of Labor (DOL), which recently decided it will not further delay its controversial fiduciary rule, we may not get a delay of CEO pay ratio. In essence, the DOL determined that as a matter of regulatory procedure, it cannot move to delay a final rule without reopening the rulemaking process for additional comments.

Regarding pay ratio, we think Acting Chairman Michael S. Piwowar’s request for additional comments earlier this year may have been anticipating this regulatory hurdle, so it is possible the SEC would view those comments as supporting a delay.

Even if this was the thinking, the question would not be considered until the SEC has a sufficient number of Commissioners in place. As of today, Jay Clayton (R) is Chairman, with Kara M. Stein (D) and Mr. Piwowar (R) holding the other seats. SEC rules require three commissioners to constitute a quorum, and the thinking is that Commissioner Stein would not agree to attend a meeting where delay of the CEO pay ratio rule would be on the agenda.

– Special Considerations in California M&A Deals

– Alternatives to Traditional Working Capital True-Ups: The Locked Box Mechanism

– Chart: Delaware Standards of Review for Board Decisions

Remember that – as a “thank you” to those that subscribe to both DealLawyers.com & our Deal Lawyers print newsletter – we are making all issues of the Deal Lawyers print newsletter available online. There is a big blue tab called “Back Issues” near the top of DealLawyers.com – 2nd from the end of the row of tabs. This tab leads to all of our issues, including the most recent one.

And a bonus is that even if only one person in your firm is a subscriber to the Deal Lawyers print newsletter, anyone who has access to DealLawyers.com will be able to gain access to the Deal Lawyers print newsletter. For example, if your firm has a firmwide license to DealLawyers.com – and only one person subscribes to the print newsletter – everybody in your firm will be able to access the online issues of the print newsletter. That is real value. Here are FAQs about the Deal Lawyers print newsletter including how to access the issues online.

As Liz recently blogged, it’s no secret that public companies have been declining nearly as fast as honeybees – & in some circles, their endangered status is just as disquieting. However, this EY report says we all need to chill out about this. Here’s an excerpt from the intro:

US public companies are fewer in number today than 20 years ago but much larger by market capitalization. They are also more stable, and delisting rates are much lower than immediately following the dot-com boom. In general, the total number of domestic US-listed companies has stabilized, especially post-2008, and the number of foreign companies listed on US exchanges has steadily increased over the same time.

A lower number of IPOs than during a boom-bust cycle should not automatically be viewed as problematic. There is ample evidence that today’s IPOs are creating stronger, healthier companies than at any time in the past. Growth companies choosing to sell shares to the public today are typically stable and have solid prospects for growth. Today’s healthy IPO market is a stark contrast to the post-dot-com bubble years, when companies with uncertain business prospects that went public, often shortly after formation, later collapse.

Is it a good thing that we have fewer public companies that are larger and more stable? As “The Economist” notes, how the market came to be dominated by those larger & more stable companies matters too:

Some firms get bought by private-equity funds but most get taken over by other corporations, usually listed ones. Decades of lax antitrust enforcement mean that most industries have grown more concentrated. Bosses and consultants often argue that takeovers are evidence that capitalism has become more competitive. In fact it is evidence of the opposite: that more of the economy is controlled by large firms.

As for the previous IPO boom & bust cycles, it’s hard to defend the dot.com bubble, but is it really a bad thing that “companies with uncertain business prospects” were able to go public during hot markets? Some win; most lose – you pay your money & you take your chances. An appetite for some risk isn’t such a bad thing.

So… Is Private the New Public?

No sooner do I finish my rant about the decline of public companies than Prof. Ann Lipton blogs that “publicness” is now increasingly an attribute of a lot of private companies. Here’s what she means:

“Publicness,” a concept first developed by Hillary Sale, refers to the general social obligations a corporation is perceived to have toward the public in terms of transparency and regularity of operations.

The growing private resale market for shares in high-profile private companies is blurring some of the lines between “public” and “private” companies. So perhaps it’s not surprising that in today’s environment, a company like Uber is perceived by the public to have certain duties in terms of ethics and responsible governance – despite not having public shareholders.

Small Cap IPOs: First Reg A+ Listing on NYSE.MKT

Here’s a little good news on the IPO front – a few months ago, I blogged about medical device company Myomo’s efforts to obtain a listing on the NYSE.MKT in conjunction with its Reg A+ IPO.

This Duane Morris blog reports that the company completed its offering and became the first Reg A+ IPO issuer to officially begin trading on an exchange. This excerpt provides an upbeat take on the results of Reg A+ & this listing milestone:

The Reg A+ rules permit non-listed companies a “light reporting” option after their IPO, further reducing costs and burdens as a public company while retaining strong investor protections. The SEC also has given extremely limited review to these filings, and has reported an average of 74 days from initial filing to SEC approval or “qualification.” As a result, companies are reporting a speedier, more cost-efficient and simpler process in completing their Reg A+ offerings than with traditional IPOs.

To date, the SEC has reported that dozens of Reg A+ deals have been consummated and hundreds of millions of dollars raised since the SEC’s final rules were implemented in 2015. Only a handful of these companies, however, have commenced trading their stock. To have completed the first Reg A+ deal to trade on a national exchange, therefore, is a very significant development for those working to redevelop a strong new IPO market for smaller companies.

This Shearman note flags the SDNY’s recent decision in Xiang v. Inovalon Holdings. To make a long story short, the plaintiff in a Section 11 case alleged that the issuer should’ve disclosed the effect of pending tax changes on its earnings in response to Item 303’s “known trends” requirement. The court refused to dismiss this claim, holding that the plaintiff adequately pled knowledge on the part of the company.

How did the plaintiff establish knowledge? That’s where the plot thickens. Here’s what the blog has to say:

The Court also found that plaintiffs had adequately pleaded that Inovalon should have disclosed its increased tax liability under Item 303, which requires disclosure of known trends reasonably expected to have a material impact on the registrant’s revenues or income.

Plaintiffs adequately pleaded that defendants knew of the tax change by pleading that Inovalon was a client of Deloitte, and as such “would have received Deloitte’s January 23, 2015 client alert” regarding the impending tax reforms. This directed communication, the Court held, adequately alleged actual knowledge even though allegations of public information alone have been held insufficient to establish such knowledge in other cases.

Aside from making a subscription to our sites even more of a necessity, this case shows both the resourcefulness of the plaintiffs’ bar and the potential need for companies to incorporate the “client alert” communications from their professional advisors into their disclosure controls & procedures.

Board Diversity: Female CEOs Have More Women on the Board

This Equilar blog says that S&P 500 companies whose CEO is a woman have more women on their boards – a lot more. Check out the stats in this excerpt:

In analyzing the boards of directors at those companies with female CEOs using BoardEdge data, Equilar found that 33.2% of board seats were occupied by women. In 2016, just 21.3% of S&P 500 boards overall were female, according to the Board Composition and Recruiting Trends report, and just 15.1% of board seats in the Russell 3000 overall were occupied by females in 2016, as noted in the recent Equilar Gender Diversity Index report.

Also on the board gender diversity beat, this Davis Polk blog says that SEC Chair Jay Clayton is getting heat from Congress to push for more gender diversity disclosure:

Citing research that found that only half of S&P 100 companies referenced gender when disclosing their board diversity, Representatives Carolyn Maloney (D-NY) and Donald Beyer (D-VA) asked Clayton to consider the SEC staff’s review of the existing rule previously ordered by former SEC Chair White. In March, Representative Maloney reintroduced a bill on board gender diversity that would require the SEC to establish a group to study and make recommendations on ways to increase gender diversity on boards. Companies must also disclose the gender composition of their boards.

Representative Gregory Meeks (D-NY), along with 28 other House Democrats, requested that Clayton go further, and to work on a rule proposal. That letter also asked the SEC to share with Congress the status of the SEC staff’s review.

10b5-1 Plans: They Really Do Work

Over on CompensationStandards.com, Mike Melbinger recently blogged about Harrington v. Tetraphase Pharma., Inc. (D. Mass.; 5/17), which held that the use of a 10b5-1 plan implemented prior to an alleged fraud will undermine allegations that trades made pursuant to that plan are indicative of scienter.

As Mike put it, the decision is important “because it illustrates how executives’ sales of stock made (or begun) prior to a period of adverse public information and declining stock price can still be protected.”

We’ve already blogged quite a bit about the new revenue recognition standard, but this blog by Steve Quinlivan provides advice on preparing the first post-adoption MD&A – and it’s definitely worth a look. Here’s the intro:

The SEC has made clear its expectations regarding MD&A disclosure for periods prior to the adoption of the new revenue recognition standard. What has received less attention is the content of MD&A after the new revenue recognition standard has been adopted. Set forth below are some guidelines to be considered. While putting pen to paper to draft the first MD&A is still months away, public companies need to begin crafting disclosures controls and procedures so they will be in place when disclosures must be made.

Steve recently followed up with this blog reviewing the MD&As filed by early adopters of the new revenue recognition standard.

FASB Lease Standard: We Have An Early Adopter!

Speaking of early adopters, although companies have until 2019 to implement the new FASB lease standard, Microsoft will adopt it on July 1, 2017 (the first day of their next fiscal year). This SEC Institute blog has an excerpt of the disclosure about the impact of the new standard from the company’s most recent 10-Q.

FCPA: Kokesh Case Will Impact DOJ Pilot Program

It seems that the fallout from the Supreme Court’s recent Kokesh decision– which held that SEC disgorgement claims are subject to a 5-year statute of limitations – is going to hit other regulators as well. As this McGuire Woods blog notes, the DOJ’s FCPA pilot program could feel a major impact:

The five year statute of limitations at issue in Kokesh is a general one that applies in FCPA civil enforcement actions as well as in the securities laws underlying Kokesh. Indeed, the parties’ briefing in the case referenced the large amounts of disgorgement in FCPA cases and that disgorgement in FCPA cases often goes directly to the U.S. Treasury and not to any victims as they may be difficult to ascertain in the FCPA context.

In holding that the statute of limitations applies to disgorgement, the Supreme Court affected a critical component of the DOJ’s FCPA Pilot Program. DOJ guidance expressly requires that to be eligible for the Program’s main benefit of mitigation credit, a company must disgorge all profits resulting from the FCPA violation. Accordingly, published declinations pursuant to the Program have indicated substantial disgorgements.

Potential responses to Kokesh include DOJ conditioning participation in the program on waivers of the statute of limitation, or requiring full disgorgement in order to award cooperation credit. The blog also notes that the decision may also increase the reluctance of parties whose conduct occurred primarily outside of the statute of limitations to participate in the program.

The article also makes clear that, if the Corp Fin Staff questions the use of a non-GAAP financial measure in the comment letter process, a public company may be able to convince the Staff that the use of a particular non-GAAP financial measure is appropriate and compliant.

The article notes, however, that the ability of public companies to prevail may be correlated with the nature of the non-GAAP financial measure being used, and that public companies have been less successful in defending their usage of non-GAAP revenue-based measures (which have been the subject of particular scrutiny by the Staff) in comparison to non-GAAP earnings-based measures.

Just like with other types of Staff comments, resolving a non-GAAP comment without being required to make a change in disclosure remains quite common. For example, the Corp Fin Staff has said at multiple conferences that they didn’t expect practice to change much for restructuring & related exclusions – and that is exactly what happened. And on the speaking circuit, Corp Fin Staffers have been talking recently about the success of the non-GAAP project and how they expect comment volume in this area to drop…

Audit Reports: Will “Critical Audit Matters” Become “Fighting Words”?

Like most of what is referred to – apparently without irony – as “accounting literature,” the definition of the term “critical audit matters” seems dull & lifeless. Under the PCAOB’s new auditing standard, critical audit matters are “matters communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements; and (2) involved especially challenging, subjective, or complex auditor judgment.”

The definition may not sound exciting – but this recent blog from Cooley’s Cydney Posner says that its application may result in some real battles between auditors & management:

I don’t think I’d be going too far out on a limb if I predicted that we might see some disputes erupt over CAM disclosure. Essentially, the concept is intended to capture the matters that kept the auditor up at night, so long as they meet the standard’s criteria.

But will auditors’ judgments about which CAMs were the real nightmares be called into question? Will the new disclosure requirement precipitate many auditor-management squabbles over the CAMs selected or the nature or extent of the disclosure? And just how enthusiastic will the CFO be about the prospect of the auditor’s sharing with the investing public the convoluted nature or opacity of the company’s policies or the struggles involved in performing the audit or reaching conclusions about the financials?

While the process of identifying CAMs is supposed to involve collaboration, auditors may be unlikely to give much weight to management & audit committee input – and may use the new requirement as a leverage point in disclosure disputes with management.

Tomorrow’s Webcast: “Proxy Season Post-Mortem – Latest Compensation Disclosures”

Tune in tomorrow for the CompensationStandards.com webcast — “Proxy Season Post-Mortem: The Latest Compensation Disclosures” – to hear Mark Borges of Compensia, Dave Lynn of CompensationStandards.com and Jenner & Block, Ron Mueller of Gibson Dunn analyze what was (and what was not) disclosed this proxy season.