Last summer, the Supreme Court’s decision in Liu reaffirmed the SEC’s authority to seek disgorgement as a remedy in enforcement actions. Following the Court’s decision, some questioned whether Liu changed or removed the five-year statute of limitations that was settled in the Supreme Court’s Kokesh decision. Russ Ryan, former Assistant Director of Enforcement and Partner with King & Spalding offered one take on this question and discussed several reasons Liulikely doesn’t give the SEC unlimited time to sue for disgorgement claims. But now, Congress stepped in and passed the National Defense Authorization Act for Fiscal Year 2021 (NDAA), which includes amendments to the Exchange Act relating to the SEC’s ability to seek disgorgement awards.

The proposed amendments provide the SEC with express statutory authority to seek disgorgement in civil enforcement proceedings pending in federal court. And, the amendments double the statute of limitations – from 5 years to 10 years – for the SEC to seek disgorgement in claims involving fraud, although it reaffirms the 5-year limitation period to seek disgorgement for non-fraud claims.

This Paul Weiss memo provides an overview of the proposed amendments and says they are a direct Congressional response to the limitations imposed by the Supreme Court in Liu and Kokesh. One potential impact of the proposed amendments is that they may increase the SEC’s power when its involved in settlement negotiations. As noted in the memo though, the full scope and actual impact of the amendments remain to be seen and the amendments raise additional issues. Here’s an excerpt:

If enacted, the NDAA will bolster the SEC’s ability to seek disgorgement in civil actions, both by doubling the statute of limitations and by providing the SEC with express statutory authority to seek such a remedy. Nonetheless, the full scope and impact of these amendments remain to be seen, and will likely require case law development. For example, it will likely fall to the courts to determine whether the SEC’s authority to seek “disgorgement”—now untethered from the SEC’s separate authority to seek “equitable relief”—will continue to be bound by the equitable limitations identified in Liu. On the other hand, the statutory authorization to require disgorgement of any unjust enrichment “by the person who received such unjust enrichment” could limit the persons subject to disgorgement even more than the Supreme Court’s decision in Liu, which permitted the SEC to seek disgorgement against affiliates of the wrongdoer in certain circumstances.

Right before last week’s holiday, the President vetoed the NDAA. The President’s reasons for vetoing the bill are unrelated to the SEC’s authority in seeking disgorgement awards – the House voted to override the President’s veto, while it’s unclear exactly when the Senate will consider the veto override.

Paycheck Protection Program: Potential Onslaught of Investigations

Throughout the last year, we blogged quite a bit about the federal government’s Paycheck Protection Program – here’s a blog about an SEC enforcement sweep of public company borrowers. As we get ready to ring in 2021 and put 2020 behind us, last week Congress allocated more funding for the program as part of the most recent economic stimulus package – John blogged about some of the changes with this most recent funding. But, this K&L Gates memo warns companies should expect a continued wave of PPP investigations in 2021.

The memo includes several stats indicating a potential onslaught of enforcement actions, including that the SBA fraud hotline received more than 100,000 complaints in 2020 (compared to 742 complaints received in 2019) and that the SEC has brought seven COVID-19 related fraud actions and has opened more than 150 COVID-19-related investigations and inquiries. For PPP lenders and recipients, the memo says now’s the time to be proactive to be able to show more than the bare minimum has been done to ensure strong compliance with the PPP program. The memo has this advice for actions companies can take now:

Overall, lenders, recipients, and any others involved in the PPP loan approval process will want to demonstrate their specific, good faith, and documented efforts to ensure that loans not only would be disbursed and received speedily, but also carefully limited to properly covered companies and individuals. In particular, companies should revisit their control processes and document the good and compelling reasons for specifically implementing them at the time (and any changes later made), initiate and conduct routine compliance checks regarding the same, identify any red flags suggesting fraudulent or other suspicious activity, and investigate them appropriately with aid of counsel.

Farewell to Jacob Stillman

Yesterday, the SEC issued a statement mourning the passing of Jacob Stillman. Jake served the Commission for 55 years, including 17 as Solicitor and passed away December 25th. Jake’s tenure at the SEC spanned 11 administrations and he is remembered as a man of great character, a lawyer with unparalleled knowledge of the securities laws, and a beloved colleague. Over the course of his career, Jake received numerous awards, among them the Federal Bar Association’s 48th Annual Justice Tom C. Clark Award for Outstanding Government Lawyer. He also was honored by his peers with the William O. Douglas Award, granted by the Association of Securities Exchange Commission Alumni.

Don’t Forget: Renew Your Membership Today!

As all subscriptions expire on December 31st, renewal time is upon us. To our returning members, thank you for your business! If you’ve not yet renewed, visit our “Renewal Center” to ensure that your subscriptions don’t lapse and that you can continue to access all of our valuable upcoming webcasts, newsletters and other content in the new year.

Yesterday, the SEC issued a statement that President Trump designated Commissioner Elad Roisman as Acting Chair of the agency. John blogged last week about former Chairman Jay Clayton’s departure – his last day was December 23. Commissioners Hester Peirce, Allison Herren Lee and Caroline Crenshaw issued a statement congratulating Commissioner Roisman’s designation as Acting Chair. Yesterday’s SEC statement follows news last week when Commissioner Peirce tweeted an early congratulations to Chair Roisman. It’s still uncertain who President-elect Biden will nominate to serve as SEC Chair but until then, Acting Chair Roisman will preside over a four-person Commission.

Growth in ESG Investing Charges Ahead

Growth in ESG investing has been well documented – here’s a recent CNBC article. Last summer, State Street Global Advisors (SSGA) released a report about growth in ESG investing and concluded that investors who were once indifferent about ESG seem to have resolved any lingering reservations. So much so, in fact, that SSGA projects over the next ten years we’ll see an eightfold increase in global ESG ETF and index mutual fund assets. SSGA bases the prediction on how the Covid-19 pandemic has exposed inequities leading investors to place more emphasis on living according to their values, including taking a stand with investment choices. The report cites three trends that will drive the ESG investing increase:

– The great reset in a turbulent 2020: The Covid-19 pandemic and its aftershocks have put a spotlight on important ESG issues such as income inequality, diversity and inclusion, social injustice, employee welfare and climate change. Many investors have concluded that they can no longer look the other way and are ready to address these ESG issues in their portfolios. Factors such as a company’s contingency planning and work environment, as well as how they treat their customers and communities, are now top-of-mind for many investors.

– Studies suggest that portfolios with ESG integration may provide downside protection when markets are struggling, underscoring ESG’s potential as a long-term investment. Some investors have expressed concerns that ESG investments would result in subpar performance and so far, those fears have proven to be unfounded.

– Beginning of an enormous intergenerational wealth transfer: as this occurs, SSGA believes ESG investing will be in the mainstream of every investment portfolio.

SSGA recently issued another memo saying that the momentum behind ESG investing will likely carry it far beyond the pandemic. The CNBC article references research from Sustainable Research and Analysis, an independent ESG research firm, and it attributes growth in sustainable investing to similar factors, while also attributing growth to the Paris climate accord, which it says sensitized investors and asset managers to think more sustainably, and the growing number of asset managers signing on to the UN Principles for Responsible Investing.

Prioritizing Employee Health & Safety: Are Chief Medical Officers Here to Stay?

John blogged not too long ago about how many consider the “S” in ESG the most difficult for companies to analyze and integrate. One aspect of “S” that is garnering a lot of attention during the pandemic is employee health and safety along with customer safety – this NYC Comptroller press release says it has submitted an initial shareholder proposal focused on worker health and safety. One way some companies are demonstrating their commitment to employee health and safety is by bringing on a chief medical officer – or if such a role is already in place, by expanding the CMO’s role.

For companies that don’t have someone fulfilling the CMO role, this HBR article asserts that it’s time to bring one on. Companies in the hospitality sector or with employees on the front lines are places where there’s a good chance to find a CMO or where they might be considering one. But, the article says even for companies with most employees working remote, it’s still important to have an in-house medical expert:

Hiring an in-house medical expert is an important signal that your leaders cares about their people. ‘Consulting outside experts’ does not suffice. You need to show that employee physical – and mental – health is a fundamental concern. One company gave its workforce direct access to the CMO on the company intranet. The idea was to give everyone ‘peace of mind [that the organization is] seeking a medical perspective to best understand how to keep our employees and communities safe.’

With so much conflicting information that’s changing by the day, it’s important to have an expert who is capable of wading through and interpreting all the data and opinions to determine the course of action that best serves your customer base. Organizations that are not built on hospitality have to decide when and how to start seeing clients and partners, attending road shows and conferences, and much more. Ultimately, business leaders have a social responsibility to set the conditions for safe and healthy behavior.

For a look at some of what’s included in the CMO role, this blog discusses how the CMO role at Salesforce has evolved since the arrival of Covid-19. As some companies scramble to hire a CMO, the blog says it’s likely more than just a passing fad.

A couple of weeks ago, the SEC announced revisions to Volume 1 of the EDGAR Filer Manual. Volume 1 of the Filer Manual is the manual that provides general information about electronic submissions on EDGAR, including the requirements for becoming an EDGAR filer. The updates clean up outdated information and also include a couple of changes intended to simplify things. Among the updates are changes allowing those submitting EDGAR access requests to use electronic notarizations and remote online notarizations, which include electronic signatures, in addition to manually signed notarizations. The SEC also amended Rule 10 of Regulation S-T to remove the manual signature requirement for Form ID notarization.

Along with those changes, the SEC also relocated some basic instructions and technical explanations previously found in Volume 1 of the Filer Manual to the more user-friendly EDGAR – Information for Filers webpage found on the SEC’s website. Among other things, these instructions cover questions relating to preparing and submitting a Form ID application, updating company information and correcting, withdrawing or deleting a filing.

Vaccines: Possible Risk Factor for Some Companies

With distribution of vaccines underway, there’s increased hope that the other side of the pandemic will come and a recent Intelligize blog discusses whether some companies should consider the vaccines as a risk factor. As many adjusted to working from home, many took advantage of online services – the blog mentions Zoom, Netflix and DoorDash as examples. But, once the lockdown is over, consumer preferences could change – the blog notes that people may prefer to go out to eat rather than having dinner delivered. Zoom’s most recent Form 10-Q included this risk factor and for companies positively impacted by the pandemic, it may be worth considering the need to include something similar:

We may not be able to sustain our revenue growth rate in the future.

We have experienced significant revenue growth in prior periods. You should not rely on the revenue growth of any prior quarterly or annual period as an indication of our future performance. We expect our revenue growth rate to generally decline in future periods. Many factors may contribute to declines in our growth rate, including higher market penetration, increased competition, slowing demand for our platform, especially once the impact of the COVID-19 pandemic tapers, particularly as a vaccine becomes widely available, and users return to work or school or are otherwise no longer subject to shelter-in-place mandates, a failure by us to continue capitalizing on growth opportunities, and the maturation of our business, among others. If our growth rate declines, investors’ perceptions of our business and the trading price of our Class A common stock could be adversely affected.

More on “Proxy Season Blog”

We continue to post new items on our blog – “Proxy Season Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply entering their email address on the left side of that blog. Here are some of the latest entries:

– SV 150 and S&P 100 Proxy Season Recap

– Nuggets from BlackRock’s Voting Guideline Updates

– Vanguard Engagements: Focus on Board & Workplace Diversity

In addition to allocating another $35 billion in funding for new Paycheck Protection Plan borrowers, the Covid-19 stimulus legislation also contains good news for existing borrowers. My law firm colleague Brent Pietrafese tipped me off to the fact that the legislation reverses the IRS’s position on the tax deductibility of expenses paid with the proceeds of PPP loans. This excerpt from this Forbes article on the bill’s changes to the PPP program summarizes the new approach to deductibility:

Ever since the IRS published Notice 2020-32, borrowers and tax professionals alike have put their faith in Congress to overrule the Service and provide a double benefit: tax-free forgiveness of loan proceeds AND deductible expenses paid with PPP funds. Section 276 of Division N of the latest bill does just that, providing that “no deduction shall be denied or reduced, no tax attribute shall be reduced, and no basis increase shall be denied, by reason of the exclusion from gross income.” Importantly, this rule applies to ALL borrowers; even those who have already applied for forgiveness. Thus, expenses paid with PPP funds are now completely deductible.

The legislation makes a number of additional changes to the program, including expanding the categories of expenses for which PPP loan proceeds may be used, streamlines the forgiveness process for loans under $150,000, and creates the possibility of a second round of financing for certain borrowers that have fully extinguished their prior PPP loans. Like everything else about this program, the provisions in the stimulus bill are controversial. We’ll be posting memos in our “Covid-19 Issues” Practice Area.

ESG Meets AMDG: The Council for Inclusive Capitalism

The NYT DealBook had a recent story about the Vatican’s new initiative with an international group of private sector, governmental & NGO leaders. Called “The Council for Inclusive Capitalism,” the group was formed in response to Pope Francis’s challenge to “build inclusive and sustainable economies and societies.” The DealBook article notes that the group’s members represent $2.1 trillion in market cap and 200 million employees, and that, with the Pope’s blessing, they’ve made pledges toward achieving “environmental and sustainable-business goals that fit into the E.S.G. movement.”

I’m pretty cynical about this kind of thing, and I’d ordinarily conclude that an initiative like this would likely involve more spin than substance. But my money’s on the Pope here, if only because I’m not sure that these folks fully realize with whom they’re dealing. You see, Pope Francis is a member of the Society of Jesus – better known as the Jesuits – and I’m very familiar with the capabilities of that particular organization.

I spent nearly a decade as a student at a Jesuit high school and a Jesuit college. Over the ensuing years, I’ve been very impressed at how adept these guys are at extracting financial & other commitments from a wide variety of sources in support of their projects. You don’t have to take my word for it – just ask the family who owns everybody’s favorite supermarket about my own high school’s powers of persuasion.

Over the past 500 years, the Jesuits have educated everybody from Rene Descartes to Stephen Colbert. As a result, they’ve become highly skilled at cozying up to the upper crust in order to put the bite on prevail upon them for assistance in doing “the Lord’s work.” And as this anecdote from a 2013 Guardian article illustrates, they have a reputation for getting things done:

An old joke tells of a Franciscan, a Dominican and a Jesuit who are arrested during the Russian revolution for spreading the Christian, capitalist gospel, and thrown into a dark prison cell. In a bid to restore the light, each man reflects on the traditions of his own order. The Franciscan decides to wear sackcloth and ashes and pray for light. Nothing happens. The Dominican prepares and delivers an hour-long lecture on the virtue of light. Nothing happens. Then the Jesuit gets up and mends the fuse. The light comes on.

As the payoff suggests, the Society of Jesus has always been known for practicality and unflappability in the service of its motto: Ad Maiorem Dei Gloriam (for the greater glory of God) [AMDG]. Equally well known is the Jesuits’ reputation as educators – giving rise to the adage: “Give me a child of seven, and I will show you the man.”

My guess is that during his 55 years as a Jesuit, some of this probably rubbed off on the Pope. So, if any of these companies or investors signed on to this project thinking they could commit to some ESG softballs in exchange for a “green sheen” & a photo op at the Vatican, they may be in for a bit of a surprise from the Pontiff (with whom they’ll meet on an annual basis). That’s because the Jesuits’ reputation as disciplinarians is also pretty formidable. “AMDG” isn’t the only acronym associated with the Jesuits – just ask any Jesuit high school student or alum what “JUG” is all about.

By the way, the Catholic Church isn’t the only religious group that’s decided to get in the ESG game – the Church of England is playing too, and as the English might put it, they’re “throwing a bit of stick about.“

Jay Clayton Signs Off

SEC Chair Jay Clayton issued a statement announcing that yesterday would be his final day in his position. He had previously announced that he’d leave his post by the end of the year, but somehow it seems fitting that the news came on the same day that commissioners Crenshaw and Lee issued a statement dissenting from the SEC’s approval of the NYSE’s direct listings proposal.

This is my final blog for the year, and I want to close by wishing a Merry Christmas to everyone celebrating the holiday, and a healthy & prosperous 2021 to all of our readers! This has been a very tough year for everyone, and while there are likely to be more difficult days ahead, there is also reason to believe that next year will be better. So, keep your chin up & thanks for reading!

Yesterday, the SEC announced a proposal to amend the provisions of Rule 144(d) to prohibit “tacking” of certain market-adjustable convertible or exchangeable securities. The proposal would also modify and update the filing requirements for Form 144. (Here’s the 84-page proposing release.) This excerpt from the SEC’s press release summarizes the proposed changes to Rule 144’s tacking rules:

The proposal would amend Rule 144(d)(3)(ii) to eliminate “tacking” for securities acquired upon the conversion or exchange of the market-adjustable securities of an issuer that does not have a class of securities listed, or approved to be listed, on a national securities exchange. As a result, the holding period for the underlying securities, either six months for securities issued by a reporting company or one year for securities issued by a non-reporting company, would not begin until the conversion or exchange of the market-adjustable securities.

“Market-adjustable” conversion provisions are a common feature of “toxic” or “death spiral” securities. Instead of a pre-established conversion rate, the securities are issued with a conversion rate that represents a discount to the market price of the underlying securities at the time of conversion. If there’s no cap on the number of shares that may be issued or floor on the conversion price, the market adjustment feature means that the number of shares issuable upon conversion may be enormous.

Currently, holders of convertible securities are allowed to tack their holding periods for the securities held pre- and post-conversion for purposes of calculating their eligibility to resell under Rule 144 period. As this excerpt from the proposing release points out, the SEC thinks that’s a problem for market-adjustable securities:

If the securities are converted or exchanged after the Rule 144 holding period is satisfied, the underlying securities may be sold quickly into the public market at prices above the price at which they were acquired. Accordingly, initial purchasers or subsequent holders have an incentive to purchase the market-adjustable securities with a view to distribution of the underlying securities following conversion to capture the difference between the built-in discount and the market value of the underlying securities.

The SEC thinks these sellers look a lot like statutory underwriters, and proposes to remove this incentive by amending Rule 144(d)(3) to preclude tacking in the case of unlisted market-adjustable securities. Why distinguish between these securities and listed securities? According to the release, the answer is that the NYSE & Nasdaq listing rules put a cap on the amount of shares that may be issued without shareholder approval, which limits the ability of a company to issue market-adjustable securities & reduces the concerns of an unregistered distribution.

The SEC also proposes to tweak the filing requirements for Form 144. If adopted, the rules would require a Form 144 to be filed electronically, but the filing deadline would be changed so that the Form 144 could be filed concurrently with a Form 4 reporting the transaction. Rule 144 transactions involving securities of non-reporting companies would no longer require a Form 144 filing. The proposal also would amend Forms 4 and 5 to add an optional check box to indicate that a reported transaction was made under a Rule 10b5-1 plan.

Direct Listings: SEC Approves NYSE Proposal

Let’s see, where were we on the NYSE’s direct listing proposal? Oh yeah, last August, the SEC approved the proposed rule, but shortly thereafter, it stayed the rule in response to a petition for review filed by the CII. Yesterday, the SEC lifted that stay and approved the rule. In doing so, it rejected arguments that the direct listing proposal circumvented traditional due diligence processes & created a potential “end run” around Section 11 liability.

So, will this fundamentally change the IPO process as we know it? Probably not. Sure, there will always be the high-name recognition Unicorns like Palantir that may find a direct listing to be an attractive option – particularly now that primary shares may be offered. But most IPO candidates aren’t well known & need Wall Street to play its traditional role in the process.

CF Disclosure Guidance: SPACs

Looking very much like an agency that wants to get everything off its desk before the Christmas holiday, the SEC capped off a busy afternoon yesterday with Corp Fin’s issuance of new disclosure guidance. CF Disclosure Guidance Topic: No. 11 provides Corp Fin’s views regarding disclosure considerations for SPACs in connection with both their IPOs & subsequent de-SPAC transactions.

With so many of our members working remotely, we wanted to be sure to let our print newsletter subscribers know that The Corporate Counsel and The Corporate Executive are now available electronically! Renew your subscriptions today and select electronic delivery for easier access to the ongoing practical guidance you’ll receive from both of these newsletters during the challenging year ahead. You will receive email notifications each time a new issue is released.

If you wish to sign up multiple users for the electronic newsletters, please contact customer service for pricing and assistance at info@ccrcorp.com or 1-800-737-1271. We will need to make sure we have all of the correct email addresses so we can send out login credentials for each user.

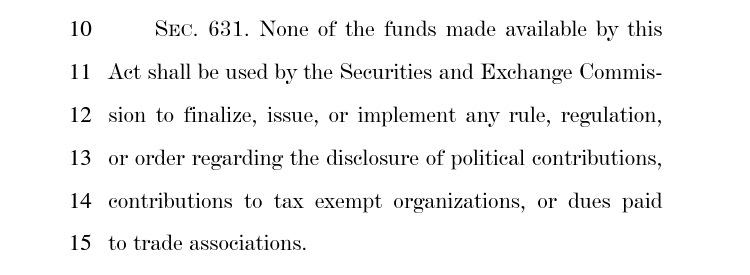

Political Contributions Disclosure: SEC Can’t Spend Funding On Rules

One of our members pointed out to us that the 2021 Consolidated Appropriations Act that Congress passed last night includes the now customary prohibition on the SEC spending any of its funds on rules requiring the disclosure of political contributions. Here it is, in all its glory:

I called this a “now customary” prohibition because Congress has been doing the exact same thing in appropriations bills for several years now. Disclosure of political contributions is a controversial issue, and the decision to ban the SEC from taking any action on it would likely be controversial too – if anybody had time to complain. Congress’s bipartisan willingness to repeatedly bury this kind of decision in one paragraph of 5,000+ page appropriations bills isn’t exactly a “profile in courage.”

November-December Issue of “The Corporate Executive”

The November-December issue of The Corporate Executive was just posted – & also sent to the printer. It’s available now to members of TheCorporateCounsel.net who also subscribe to the electronic newsletter (try a no-risk trial). This issue includes articles on:

– Tax Withholding Deposits for Stock Plan Transactions—Understanding the New Relief

– Some Deferred Compensation Plans and Employment or Stock Award Agreements May Need to be Amended by December 31, 2020

– SEC Proposes Amendments to Rule 701 and Form S-8

Last week, Liz blogged about the passage of the Holding Foreign Companies Accountable Act, which amends the Sarbanes-Oxley Act to prohibit listing on US exchanges of foreign companies for which the PCAOB has been unable to inspect audit work papers. On Friday, President Trump took time from his busy schedule – which he swears does not include declaring martial law – to sign the legislation.

Shortly thereafter, SEC Chair Jay Clayton issued his own statement on the legislation – which this excerpt suggests has thrown a bit of a monkey-wrench into the SEC’s own rulemaking initiatives regarding China-based companies:

Prior to enactment of the Act, SEC staff were finalizing recommendations for proposed rules regarding enhanced listing standards for U.S. securities exchanges and auditor qualifications for the Commission’s consideration. Because of the substantial overlap between the staff’s proposal and the Act, I have directed the staff to consider providing a single consolidated proposal for the Commission’s consideration on issues related to the PCAOB’s access to audit work papers, exchange listing standards, and trading prohibitions.

The statement says that Chair Clayton has also asked the staff to consider additional issues relating to the Act’s implementation, including how its disclosure requirements can be implemented expeditiously and how any potential uncertainties can be addressed. He also acknowledged that this “pragmatic step” means that a rulemaking proposal won’t happen during his tenure.

Innovation: In-House Departments Leave Law Firms In the Dust?

This recent Thompson Hine survey on innovation in the legal profession says that in-house legal departments are way ahead of law firms when it comes to innovative approaches to legal services. This excerpt explains:

In-house legal departments continue to face extraordinary pressures — pressures that could be eased through law firm innovation. Budgets — already taking a hit before COVID-19 — are tighter than ever in the wake of the pandemic, and companies are looking for efficiencies at every turn.

But more than two-thirds of our survey respondents said their primary outside firms had made no progress in innovation over the past year. As a result, 91% of in-house law departments have taken innovation into their own hands. The changes in-house legal departments are making on their own show their priorities.

Nearly two-thirds of our buyers cited improved project management as a key change in their legal departments. Almost half have streamlined outside counsel panels, while more than 40% have implemented self-service tools and restructured departments and/or processes. Clearly, efficiency is the order of the day, particularly when you compare the numbers with those in our first survey. Sixty-three percent of in-house law departments had improved project management in 2019 vs. 8% in 2017; 41% had restructured departments or processes vs. 8% in 2017; and 33% had outsourced to alternative legal services providers in 2019 vs. 3% in 2017.

The survey suggests that law firms’ reluctance to innovate may be causing them to miss out on new business opportunities – 53% of in-house respondents would consider hiring a new law firm because it is innovative.

Cheat Sheet: 2020 Capital Markets Rulemaking

If you’re like me, you’re probably having a little trouble keeping up with the avalanche of rulemaking from the SEC over the past several months. If you find yourself in that position, you may want to hang on to a copy of Skadden’s 2020 Capital Markets Regulatory Review. This 13-page document provides a brief overview of some of the key capital markets and corporate governance reforms that have taken effect in 2020 or are poised to take effect in 2021.

We have a new podcast available to members, in which our very own Dave Lynn interviews special guests about the latest developments in securities laws & corporate governance. Two episodes are already available for your holiday entertainment!

In this 26-minute episode, Dave talks with Karen Garnett – currently a partner at Proskauer and formerly an Associate Director of Corp Fin – about disclosure effectiveness & Reg S-K. Topics include:

– The SEC’s “Disclosure Effectiveness” initiative – why was it so successful?

– Considering changes to the description of business requirement

– Human capital disclosure – what should companies do now?

– Tackling the amended risk factor disclosure requirements

– Is the Disclosure Effectiveness initiative done?

And in this 14-minute episode, Dave talks with Jay Knight – currently a partner at Bass, Berry & Sims and previously Special Counsel in Corp Fin – about Staff comments on COVID-19 disclosures. Topics include:

– Has the SEC Staff been commenting on disclosures about COVID-19 in public filings?

– What areas of comment has the Staff raised regarding COVID-19?

– What approach has the Staff taken with respect to non-GAAP financial measures in the COVID-19 era?

– Do you think the Staff will focus on COVID-19 disclosures when it reviews 10-Ks filed in 2021?

– Are there lessons to take away from the Staff’s comments as we prepare disclosures for the upcoming reporting season?

SEC & Edgar Closed Next Thursday & Friday

This executive order announces that all federal agencies – including the SEC – will be closed this upcoming Thursday for Christmas Eve (Christmas Day was already designated as a federal holiday, so the SEC and Edgar are closed that day too).

The SEC announced that, just like the past couple of years, this means Edgar will be closed on both the 24th and 25th. No filings will be accepted on those days, Edgar filing websites won’t be operational, Edgar Filer Support will be closed, and you’ll have until Monday, December 28th to make filings that would have been due on Thursday or Friday. The announcement also says that both of those days will also be treated as federal holidays for filing purposes.

Transcript: “Pay Equity – What Compensation Committees Need to Know”

We’ve posted the transcript for our recent CompensationStandards.com webcast, “Pay Equity: What Compensation Committees Need to Know.” Mintz’s Anne Bruno, BlackRock’s Tanya Levy-Odom, Equity Methods’ Josh Schaeffer, and Impax Asset Management’s Heather Smith shared their insights on these topics:

1. Why Pay Equity Is in The Spotlight

2. Differences Between “Pay Equity,” “Pay Gap” & “Pay Ratio”

3. Shareholder Expectations

4. Disclosure Trends: Pay Gaps & Pay Equity

5. How to Collect & Interpret Data

6. Remediation Strategies

7. Mechanics of Board & Committee Oversight

8. Preparing for Shareholder Engagements & Proposals

At an open meeting yesterday, the SEC adopted final rules that will require public “resource extraction” issuers to disclose payments made to the US federal government or foreign governments, if the company engages in the commercial development of oil, natural gas, or minerals. After some drama in which Congress disapproved the SEC’s 2016 rulemaking on this topic, the current iteration is based on a 2019 proposal and implements Section 13(q) of Exchange Act, which was added by Dodd-Frank a decade ago. All of the SEC Commissioners, including Chair Jay Clayton, released their own statements about the final rules.

Although the final rules will be effective 60 days after publication in the Federal Register, there’s a two-year transition period before companies will be required to submit a Form SD with this info. And unlike the “conflict minerals” Form SD that is due by May 31st of each year for all companies, this one will be due within 270 days of each company’s fiscal year end. So for calendar-year companies, the first report will likely be due at the end of September 2024. The SEC also issued this order to recognize that a company that meets resource extraction payment disclosure requirements in the EU, UK, Norway or Canada would satisfy the Section 13(q) “alternative reporting” requirements.

– Require public disclosure of company-specific, project-level payment information;

– Define the term “project” to require disclosure at the national and major subnational political jurisdiction, as opposed to the contract, level, recognizing that more granular contract-level disclosure could be used to satisfy the rule;

– Add two new conditional exemptions for situations in which a foreign law or a pre-existing contract prohibits the required disclosure;

– Add a conditional exemption for smaller reporting companies and emerging growth companies;

– Define “control” to exclude entities or operations in which an issuer has a proportionate interest;

– Limit the liability for the required disclosure by deeming the payment information to be furnished to, but not filed with, the Commission;

– Add relief for issuers that have recently completed their US IPOs; and

– Extend the deadline for furnishing the payment disclosures.

Cyber Insurance: Claims Starting to Show “Covid-19” Impact

Over the past 5 years, companies’ average cost of cyber crime has increased 72% – to $13 million – and the average number of security breaches has increased by 67%. That’s according to this 14-page summary of cyber trends from Allianz – which, not surprisingly, explains that the work-from-home environment is heightening cyber risks. It also says hackers are selling high-end malware and tools to other attackers – so companies need to be on alert for sophisticated schemes.

That advice was underscored earlier this week when news broke about a cyberattack at SolarWinds and FireEye. This CNBC article says that SolarWinds’ stock dropped 23% after the hack was announced – not a position in which any company wishes to find itself – and a few people are also now questioning recent stock sales by some large investors of that company.

Our friend Melissa Krasnow of VLP Law Group noted that the incident highlights the need to double down on vendor management processes & agreements for privacy and data security provisions, to make sure that incident response plans and business continuity plans are in place and up-to-date, and to keep using tabletop exercises to spot weaknesses and craft responses.

Here’s more detail from the Allianz report:

Through 2020, malware and ransomware incidents have already increased by more than a third, at the same time as a 50%+ increase in phishing, scams, and fraud, according to international police body, INTERPOL. The rush to adopt new cloud systems and remote access solutions, has also driven up the number of data breaches. Over a four-month period, some 907,000 spam messages, 737 incidents related to malware and 48,000 malicious URLs – all of them in relation to coronavirus– were detected by one of INTERPOL’s private sector partners.

Business email compromise schemes (see page 7) are likely to increase further with the shift in the business landscape to remote working and the economic downturn, along with damage costs from phishing scams, ransomware attacks and insecure remote access to networks. Coronavirus-themed online scams and phishing campaigns which aim to take advantage of public concern about the pandemic are unlikely to dissipate anytime soon.

The pandemic will also have a long-term impact as companies increasingly digitalize, work remotely and rely more on online sales in response, meaning cyber risks will evolve in different shapes and forms.

Farewell to Paul Sarbanes

Paul Sarbanes, the 5-term U.S. Senator from Maryland who co-wrote the Sarbanes-Oxley statute, passed away last week at the age of 87. John, Broc and I reminisced about the landmark law a few years ago on the 15th anniversary. Here’s an excerpt from Mr. Sarbanes’ NYT obituary:

While other members of Congress pursued the Enron scandal with splashy televised hearings and spirited denunciations, Mr. Sarbanes approached it by holding 10 thorough hearings to get widespread expert advice on what corrective legislation should include.

Initially opposed by many Republicans and by the powerful lobbying of the accounting industry, the measure eventually passed 97 to 0 in the Senate after another accounting failure, at WorldCom, had sent the stock market plunging.

Mr. Sarbanes saw his career as having “bookends,” as he put it in an interview for this obituary in 2013: It began in 1974 with his role in the impeachment proceedings against President Richard M. Nixon and closed with the accounting law.

As we move closer to the finish line for 2020, our faithful correspondent Nina Flax of Mayer Brown is back with an uplifting “list” to focus on some of the positives she’s experienced (here’s our last list from Nina):

It has been a while since I have written a list. I have, as I am sure many of you have, struggled with COVID and WFH. Every day, there is something new, ridiculous, sad, frustrating, amazing to add to the items that elicit an “it’s 2020!” response. Despite having been stuck on I-80 with my son in the car exactly when the LNU Lightning Complex jumped the highway and shut down traffic (perhaps the subject of a future list), I am extremely grateful today that I have literally and figuratively found my way through the impending wall of smoke to find these things:

1. Dinner with my son. My son eats dinner at 5pm, if even that late some days. I cannot explain it other than that is when he is hungry, so that is when he eats because we prefer him to not be hangry. Before WFH, I very rarely made it home in time to actually eat dinner together. I have made it a point to try to do that almost every day – force myself to take the 30 minute break to have that time. Sometimes we talk about high/lows, sometimes we go around saying something we are grateful for, sometimes we take turns doing mad-lib style storytelling, mostly we just sit down and laugh about something. I have never been happier. (Except for one day I remember before child where I never got out of bed and slept for about 12 hours in between watching TV?)

2. More movement. Before WFH, my close colleague and I would take breaks from sitting at our desks and walk in circles around our office building to talk through legal issues – conceptual or drafting – it really helped. With WFH, air permitting, you will frequently find me walking up and down my driveway while on calls. Moving helps me focus. Moving helps me process. Moving helps me be creative – professionally and personally.

3. Appreciativeness. Not grand gratefulness in a trendy mindfulness way. Being away from people has made me appreciate people more. And miss them. Before, I would go out of my way to write a holiday time card to each colleague that I had worked with or collaborated with over the year that I valued. Very personalized, very intentional. Now, I go out of my way to say thank you for the small things. Thank you for responding so quickly. Thank you for taking my call. Thank you for the follow up. Thank you for taking the lead. Thank you for your collaboration. This of course also applies to my personal life. Thank you for always being there for me. Thank you for taking the time to answer my questions. Thank you for going to the grocery store. Thank you for getting the ridiculously howling dog to stop howling. Thank you for organizing this friends call. Thank you for passing along this interesting article. Thank you for the book suggestion. Thank you for checking in on my parents. Thank you for scheduling this outside, socially distanced playdate. Thank you for being you.

4. Knitting and Other Old Loves. This is more of a re-found. I picked up knitting in law school, but for whatever reason I stopped knitting before I met my husband. In the COVID-induced cleaning and house reorganizing, I re-discovered my needles. Then I found a great store, took my son and he picked out three colors. Side note: It was an amazing moment of pride that he picked colors that completely epitomize South Florida – citrus (bright yellow), tangerine (bright orange) and electric (a bright aqua). Second side note: I love the way that people name colors. My husband and I used to play a game where I would try to guess the name of a color (and often came pretty close). Back to the knitting point, my son now has a fantastic hat and matching cowl (if I do say so myself, but really, others have said so too). I am working on matching mittens and looking forward to giving knitted gifts to many in the coming months. For other old loves, I have picked up drawing and painting again in a way that I have not enjoyed since I first went to college intending to major in art and minor in chemistry (no, I have no idea what I was thinking back then; yes, I do know how I ended up here).

5. New Curiosities. There are many reasons that through this year I have felt more drawn to nature. I have been making fun informational cards about leaves, shells, flies and bees for my son. I have a list of nature books (of course, as an Amazon list) that I want to read. I have a nature journal. I have a stack of articles and studies from an amazingly supportive friend who has always been intensely focused on sustainability. I watched My Octopus Teacher as soon as I could and cried. I am feeling inspired.

I think I will pull that last sentence down to here – I am feeling inspired. In the face of all of the negative from 2020, my inspiration enables me to laugh that it snowed chocolate in Olten, to hug my husband, son and dogs enough to make up for all of the other hugs I am missing out on (I am a hugger), to deal with frustrations in different ways, to drive initiatives I feel strongly about, to focus on kindness and caring, to not compromise on expectations, to accept whatever may happen, to know that I can make a change, to know that I will survive. Maybe resiliency that I read so much about in the context of children is really about inspiration?

**End note: I promise that this time has not been all positive for me. There have been very hard negatives. Without those, I would not be here now. I am sure I will face negatives in the future. I am hoping this time helps me meet those challenges more adeptly, with stronger mental health. I hope the same for all of you.

Enforcement Director Stephanie Avakian to Leave SEC

Last week, the SEC announced that Enforcement Director Stephanie Avakian will depart from the Commission by the end of the year. Stephanie began her career at the SEC and began her latest tour in 2014. She’s led the Enforcement Division over the last four years as Co-Director and then Director. Deputy Director Marc P. Berger will serve as Acting Director upon her departure. The SEC’s press release includes a long list of the Enforcement Division’s accomplishments under Stephanie’s leadership – and here’s a statement from Commissioner Elad Roisman.