Here’s the final installment in our series of guest blogs on AI Related Disclosures by Orrick’s J.T. Ho, Bobby Bee and Hayden Goudy:

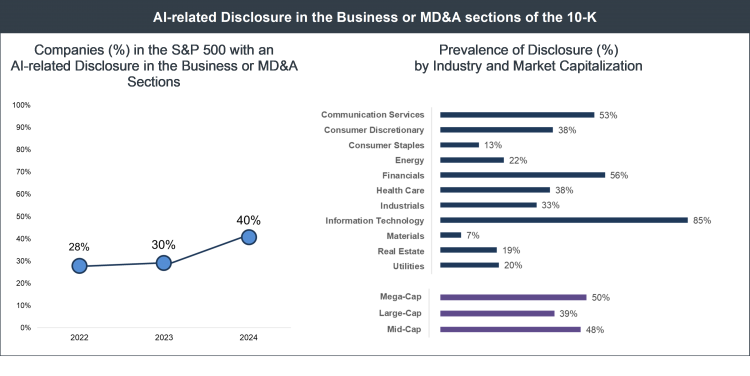

AI-related Business and MD&A Disclosure. Several companies in the S&P 500 mentioned AI in the Business or MD&A sections of their most recent 10-K, tying AI to their main products and services or to key business updates. While less common than an AI-related risk factor, 40% of the S&P 500 had an AI-related disclosure in the Business or MD&A sections of their most recent 10-K, an increase from 30% in the previous period.

AI-related disclosure in the Business or MD&A sections of the 10-K varied significantly by industry. For instance, 85% of companies in the information technology sector made an AI-disclosure in the Business or MD&A sections, compared to 56% of companies in the financial sector and 38% of companies in health care.

As more companies adopt AI in their operations, products and services, we expect more references to AI in the Business and MD&A sections of 10-Ks across the S&P 500.

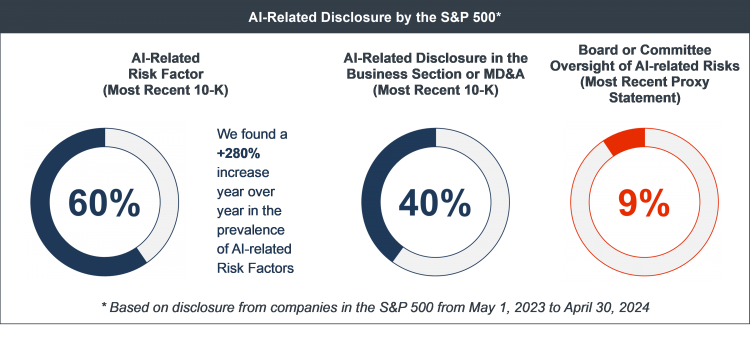

Limited Disclosure in the Proxy Statement. AI-related disclosure in the proxy statement across the S&P 500 was limited. While more than 39% of companies in the S&P 500 mentioned AI in their most recent proxy statement, a significant proportion of references were to new AI-related products or the role that AI was playing as part of a business transformation. Additionally, 24% of the S&P 500 disclosed director-level AI-related expertise or experience in their most recent proxy statement.

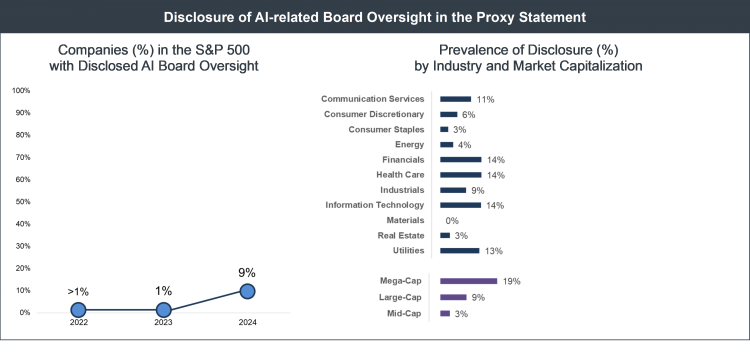

However, a much smaller percentage of companies in the S&P 500, approximately 9%, disclosed the role of the board or its committees in overseeing AI-related risks.

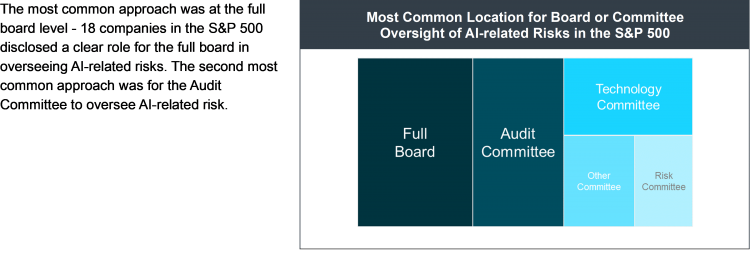

For companies that disclosed board or committee oversight, the allocation of that responsibility varied.

The most common approach was at the full board level – 18 companies in the S&P 500 disclosed a clear role for the full board in overseeing AI-related risks. The second most common approach was for the Audit Committee to oversee AI-related risk.

We’re really looking forward to returning to an in-person format for our upcoming Proxy Disclosure and Executive Compensation Conferences to be held in San Francisco on October 14th and 15th. Our agenda is always topical, and this year is no exception. Here’s a taste of what we have in store for you:

– If you’ve been following this week’s blogs on AI-related disclosure issues, you won’t want to miss our “Governing and Disclosing AI” panel

– Our “Cyber Incidents: Handling Real Time Reporting” panel will offer insights to keep you out of the Division of Enforcement’s cross-hairs when it comes to cybersecurity issues.

– Our “Living with Clawbacks – What Have We Learned?” panel will bring you up to speed on how companies are adjusting to the clawback listing standards and the emerging issues they are encountering.

Of course, we’ll also have panels addressing the latest developments in shareholder activism, climate disclosure, key 10-K and proxy disclosures, perks, navigating ISS & Glass Lewis. You’ll hear insights on proxy disclosure and executive comp hot topics from our “SEC All-Stars” and have the opportunity to listen to Dave interview Corp Fin Director Erik Gerding. As always, we’ll also have a little fun – this year, it’s in the form of a “Family Feud”-style “lightning round” ame show that we think you’ll really enjoy.

We hope many of you will join us in San Francisco! Register by July 26th to lock in our “early bird” deal for individual in-person registrations ($1,750, discounted from the regular $2,195 rate). If traveling isn’t in the cards, we also offer a virtual option so you won’t miss out on the practical takeaways our speaker lineup will share. (Also check out our discounted rate options for groups of virtual attendees!) You can register now by visiting our online store or by calling us at 800-737-1271.

Yesterday, the SCOTUS granted a cert petition filed by NVIDIA seeking review of the 9th Circuit’s decision in E. Ohman J:Or Fonder AB v. NVIDIA Corp., (9th Cir.; 8/23), concerning the PSLRA’s heightened pleading requirements for allegations of falsity and scienter. In its cert petition, NVIDIA pointed out that plaintiffs often try to meet the PSLRA’s heightened pleading requirements for falsity & scienter by alleging that internal documents contradict a company’s public statements, and that the 9th Circuit’s ruling presented two questions that have divided the circuits concerning how the PSLRA’s pleading requirements apply in this “common and recurring context”:

1. Whether plaintiffs seeking to allege scienter under the PSLRA based on allegations about internal company documents must plead with particularity the contents of those documents.

2. Whether plaintiffs can satisfy the PSLRA’s falsity requirement by relying on an expert opinion to substitute for particularized allegations of fact.

NVIDIA went on to note that, with respect to the pleading requirement for alleging scienter based on internal documents that contradict public statements, five circuits have held that the statute requires to allege the contents of those documents with particularity, while two (now including the 9th) have held that plaintiffs may allege scienter “merely by hypothesizing about what those documents ‘would have’ said.” As to the falsity requirement, NVIDIA pointed out that two circuits have held that plaintiffs can’t satisfy the PSLRA’s pleading standards by substituting an expert opinion for particularized allegations of fact, so the 9th Circuit’s decision permitting plaintiffs to do that creates a split.

By the way, the case caption isn’t a typo, “E. Ohman J:Or Fonder AB” is the correct name of the lead plaintiff. For some odd reason, today is my day for blogs involving parties with names that look like typos to American eyes. Over on DealLawyers.com, I blogged about an EC investigation of a deal under the EU’s Foreign Subsidy Rule in which for some reason the regulators decided to abbreviate the name of Emirates Telecommunications Group Company PJSC as “(e&)”.

Here’s the second installment in our series of three guest blogs on AI Related Disclosures by Orrick’s J.T. Ho, Bobby Bee and Hayden Goudy:

Corporate Disclosure Trends We identified AI as one of the fastest growing disclosure topics in SEC filings across the S&P 500, with a rapidly growing number of companies disclosing AI-related risk factors in the 10 K. However, disclosure of AI-related oversight at the board and management level in the proxy statement significantly lagged disclosure of AI-related risks in the 10-K.

Companies Disclosed AI-Related Risks More Often Than AI Oversight. We found a gap between the prevalence with which companies in the S&P 500 disclosed significant or material AI-related risks and the prevalence with which they disclosed board and committee oversight of those risks in the proxy statement. Together with growing investor and activist interest, we expect increasing pressure from a range of stakeholders on public companies to address this gap, including pressure to develop and disclose an approach to AI oversight at the board or committee level.

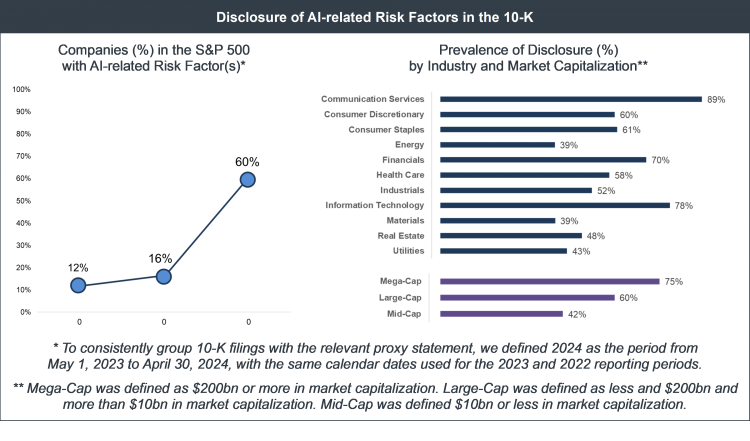

AI-related Risk Factors.The most common type of AI-related disclosure in SEC filings across the S&P 500 was an AI-related risk factor. Nearly 60% of the S&P 500 disclosed an AI-related risk factor in their most recent 10-K. This was a major increase from the previous reporting period, where only 16% of the S&P 500 disclosed an AI-related risk factor.

Most relevant risk factors in the S&P 500 were not focused solely on AI. Instead, we found that references to AI were generally integrated into existing risk factors. Companies included AI-related references into risk factors addressing:

– Cybersecurity risks, such as higher levels of exposure due to threat actors using AI, or a higher likelihood of a data breach due to the use of AI tools.

– Operational and business risks, such as higher costs from adopting AI technology or potential loss of market share from AI-driven disruption.

– Potential harm to the company brand and reputation from intellectual property disputes involving AI.

– Costs or risks associated with AI regulations.

The final installment of this series will address AI-related Business and MD&A disclosure, as well as practices regarding AI-disclosures in proxy materials.

The latest issue of The Corporate Counsel has been sent to the printer. It is also available now online to members of The CorporateCounsel.net who subscribe to the electronic format. The issue includes the following articles:

– Supreme Court Weighs in on MD&A Disclosure: Should You Revisit Your MD&A Now?

– Navigating Item 601(b): Material (and Other) Agreements

Please email sales@ccrcorp.com to subscribe to this essential resource if you are not already receiving the important updates we provide in The Corporate Counsel newsletter.

We’re off tomorrow for the Juneteenth holiday. Our blogs will be back on Thursday.

Al disclosure is a topic that’s getting a lot of attention from investors and a lot of scrutiny from the SEC. That’s why we pleased to bring you this week a series of three guest blogs on AI disclosure practices among the S&P 500 by Orrick’s J.T. Ho, Bobby Bee and Hayden Goudy:

The growth of generative artificial intelligence (AI) is transforming business, sparking a rise in public company disclosure and considerable investor interest. A growing number of companies are disclosing AI capabilities, opportunities and risks in filings with the Securities and Exchange Commission (SEC). At the same time, the SEC has demonstrated its commitment to combat “AI washing” – the practice of overstating or falsifying AI usage – with enforcement actions against several investment advisors signaling the start of a broader effort to police AI-related disclosures.

Activist investors are also interested in AI-related risks. Several shareholder proposals requesting disclosure of AI-related oversight have received high levels of support at recent annual shareholder meetings.

Our review of SEC filings from the S&P 500 for the 12 months ending April 30, 2024, paints the portrait of an evolving landscape when it comes to AI-related disclosures. It reveals trends in:

(Including in proxy statements and in the “Risk Factors,” “Business” and “Management Discussion and Analysis” (MD&A) sections of annual reports on Form 10-K)

What Public Companies Should Consider Doing Now

Relevant disclosure is not only appropriate but often necessary when AI becomes a material aspect of a company’s business. Investors and market regulators expect transparency, effective governance oversight and effective risk management over the numerous ways that companies are developing and deploying AI. Misrepresenting AI capabilities and failing to properly oversee risks could severely damage investor trust and lead to lawsuits and regulatory action.

Where AI has a significant impact on the business, public companies should:

– Validate AI statements and develop effective disclosure controls and procedures to support the accuracy of public AI-related disclosures.

– Develop governance structures to identify and manage AI-related risks at both the board and management level, and disclose both significant AI-related risks and oversight of those risks in required SEC disclosures.

A Closer Look at Investor Activity and Corporate Disclosure Trends

In the sections that follow, we examine AI-related disclosure trends in SEC filings across the S&P 500. We also explore the expectations of proxy advisors and activist investors, share data on increasing references to AI in annual reports on Form 10-K and highlight a potential gap in proxy statement disclosures regarding AI oversight.

Emerging Investor Expectations

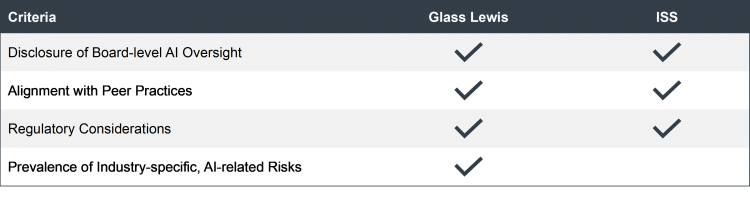

While AI is an emerging priority for many investors, institutional asset managers and proxy advisors generally have not established formal guidelines regarding oversight of AI by the board or its committees.

Several major investors have identified AI as a significant opportunity for their investment activities, but most U.S.-based investors have not articulated specific expectations for oversight and management of AI by public companies.

The proxy advisors Glass Lewis and ISS have identified AI as a relevant area for future policy development, but currently approach AI-related matters on a case-by-case basis. For the limited number of AI-related shareholder proposals voted on to date, Glass Lewis and ISS generally consider the following criteria when making recommendations:

Activist Investor Interests

Activist investors are also interested in AI-related issues.

We identified 13 shareholder proposals related to AI submitted in the 2024 proxy season. These proposals ask for disclosure on topics including the use of AI in company product and operations, the role of the board in overseeing AI and the prevalence of AI-related risks. Several AI-related proposals have received the support of 20 percent or more of votes cast at an annual shareholder meeting.

We expect AI-related shareholder proposals to continue to be an agenda item for activist investors, especially for companies that experience AI-related controversies or have business models at risk due to the potential impact of AI.

Be sure to check out the next installment of this three-part series, which will focus on AI-related risk factor disclosures.

Meredith is taking a well-deserved break for a couple of weeks & Liz is still out on leave, so the newest member of our editorial team, Meaghan Nelson, is taking a turn at blogging. Meaghan’s been working with us for the past several months updating our Handbooks, but now she’s stepping out into a more public role as a blogger – and I think you’ll really enjoy her stuff. Now, I’ll turn this blog over to Meaghan and let her tell you a little more about herself in her own words:

Hello, everyone! I’ve been working with the editorial team the last several months behind the scenes and am now ready for prime time (although truth be told, I did make a brief guest appearance back in 2021)! I’ll be cutting my teeth on The Advisors’ Blog over on CompensationStandards.com this week and will be making appearances on the other blogs in due time.

As the blog title alludes to, I’ve been a huge fan of CCR Corp for the entirety of my practice and am thrilled to join these illustrious ranks. My only hope is that I can deliver the important and timely corporate and securities news and practical tips we’ve all come to enjoy with the same level of humor and pith as my fellow editors. At the bare minimum, I’ll continue the current trend of increasing exclamation points and millennial pop culture references.

A few things about me:

I’ve been a corporate and securities lawyer for the last 14 years, the last 8 of which were spent in-house building corporate teams and leading the legal function. I’ve worked in finance, big law (both NYC and Silicon Valley), at companies both newly public and public for decades, and, most recently, at a late-stage start-up that is on the path to an IPO whenever that window opens again. More details on my background are in my bio.

I currently live in Boise, ID having relocated in the summer of 2021. As a newly minted Idahoan and a person married to an actual Midwesterner, I feel compelled to issue a PSA that we’re in the Mountain West not the Midwest. While Idaho is my home now, I’m a native Californian who has lived all over—SF Bay Area for a decade and before that (at various points of time): NYC, Illinois, Tennessee, Georgia, Maine, Florida, Republic of Ireland, Northern Ireland, West Virginia, Kansas, and California. I credit my extroversion to all that moving and enjoy being able to make a regional connection with nearly everyone I meet.

I look forward to sharing my experiences as both outside and in-house counsel and keeping you all up to date. I’d love to hear from you regarding any ideas you have on what would be interesting to read and hear about (mnelson@ccrcorp.com). Thank you for being a part of this community!

Tune in at 2 pm Eastern tomorrow for the CompensationStandards.com webcast – “Proxy Season Post-Mortem: The Latest Compensation Disclosures” – to hear Mark Borges of Compensia, Dave Lynn of CompensationStandards.com and Goodwin & Ron Mueller of Gibson Dunn discuss the ins and outs of compensation disclosures during the 2024 proxy season. They’ll cover:

The State of Say-on-Pay During the 2024 Proxy Season

Highlights and Tips from this Year’s CD&As

Best Practices for Disclosing Incentive Compensation Adjustments and Outcomes

Trends in Disclosure Regarding Operational and Strategic Metrics

Pay-versus-Performance: SEC Staff Guidance Issues and Year 2 Enhancements

Perquisites Disclosure and Recent Enforcement Focus

Shareholder Proposals – Company Strategies; No-Action Trends; Activists and Universal Proxies

Proxy Advisory Firms – Is Their Influence Starting to Wane?

Rule 10b5-1 Plan Disclosure Developments

Pending SEC Rulemaking

Members of CompensationStandards.com are able to attend this critical webcast at no charge. If you’re not yet a member, subscribe now. If you need assistance, send us an email at info@ccrcorp.com – or call us at 800.737.1271.

We will apply for CLE credit in all applicable states (with the exception of SC and NE, which require advance notice) for this 90-minute webcast. You must submit your state and license number prior to or during the program using this form. Attendees must participate in the live webcast and fully complete all the CLE credit survey links during the program. You will receive a CLE certificate from our CLE provider when your state issues approval, typically within 30 days of the webcast. All credits are pending state approval.

On Wednesday, the PCAOB announced that it approved the adoptionof an amendment to PCAOB Rule 3502 to provide that an individual accountant can be held liable for substantially and negligently contributing to their firm’s violations of PCAOB laws, rules, and standards. Here’s the explanation of the change from the PCAOB’s press release:

For decades under PCAOB and predecessor auditing standards, auditors have been required to exercise reasonable care any time they perform an audit, and the failure to do so constitutes “negligence.”

Previously, however, Rule 3502 allowed the PCAOB to hold associated persons liable for contributing to a registered firm’s violation only when they did so “recklessly” – which represents a greater departure from the standard of care than negligence. This means even when a firm commits a violation negligently, an associated person of that firm who directly and substantially contributed to the firm’s violation could be sanctioned by the PCAOB only if the PCAOB were to show that the associated person acted recklessly.

As adopted, the updated rule changes Rule 3502’s liability standard from recklessness to negligence, aligning it with the same standard of reasonable care auditors are already required to exercise anytime they are executing their professional duties. Similarly, the U.S. Securities and Exchange Commission already has the ability to bring enforcement actions against associated persons when they negligently cause firm violations.

At the same time, the updated rule maintains Rule 3502’s requirement that an associated person must have contributed to the firm’s violation both “directly and substantially” in order to be held liable.

I’m sure John wasn’t the only person who, when this amendment was proposed, had concerns that lowering the bar for actions against individuals might spur increased efforts by auditors to protect their firms & themselves — with attendant increased costs for public companies. Wednesday’s statement by PCAOB Chair Erica Williams tried to assuage those concerns with this comment:

There is no reason this amended rule should cost auditors significant time, resources, or money, because auditors are already prohibited from being negligent today as part of their requirement to exercise reasonable care and competence any time they perform an audit. Similarly, the U.S. Securities and Exchange Commission (SEC) already has the ability to seek penalties in enforcement actions against associated persons when they negligently cause firm violations.

As I’ve said before, if you are doing what you are already supposed to be doing, this amended rule would not affect you. If you are not, there may be consequences.

It seems proxy statements aren’t the only filing type commonly containing XBRL tagging errors this year. This Public Chatter Blog from Perkins Coie picks up on the recent statement from the SEC’s Office of Structured Disclosure flagging observations by SEC Staff that a number of filers have used incorrect tagging practices in 10-Ks and 10-Qs filed in 2024. The statement encourages filers to review their EPS tagging in particular, specifically identifying the following incorrect practices:

– Creating custom tags such as BasicAndDilutedEarningsPerShare to tag this amount;

– Tagging this amount only once using one of the two standard tags; and

– Tagging this amount using a standard tag that was deprecated in 2022.

The data should be tagged using GAAP Financial Reporting taxonomy elements us-gaap:EarningsPerShareBasic and us-gaap:EarningsPerShareDiluted. In filings where basic and diluted EPS have the same value and are presented only once on the face of the income statement, an entity should tag that amount twice using both tags.

The blog says “without fixing the tags, apparently the data is useless to end users” and “the upshot is that the SEC’s Division of Economic and Risk Analysis is monitoring this stuff.” It also acknowledges that this might not be very understandable to folks unfamiliar with tagging practices. If that’s you, share the SEC statement with your financial reporting folks and anyone who works on or confirms XBRL tagging.

– John Jenkins

– John Jenkins