The latest issue of The Corporate Counsel has been sent to the printer. It is also available now online to members of The CorporateCounsel.net who subscribe to the electronic format. The issue includes the following articles:

– Supreme Court Weighs in on MD&A Disclosure: Should You Revisit Your MD&A Now?

– Navigating Item 601(b): Material (and Other) Agreements

Please email sales@ccrcorp.com to subscribe to this essential resource if you are not already receiving the important updates we provide in The Corporate Counsel newsletter.

We’re off tomorrow for the Juneteenth holiday. Our blogs will be back on Thursday.

– John Jenkins

Al disclosure is a topic that’s getting a lot of attention from investors and a lot of scrutiny from the SEC. That’s why we pleased to bring you this week a series of three guest blogs on AI disclosure practices among the S&P 500 by Orrick’s J.T. Ho, Bobby Bee and Hayden Goudy:

The growth of generative artificial intelligence (AI) is transforming business, sparking a rise in public company disclosure and considerable investor interest. A growing number of companies are disclosing AI capabilities, opportunities and risks in filings with the Securities and Exchange Commission (SEC). At the same time, the SEC has demonstrated its commitment to combat “AI washing” – the practice of overstating or falsifying AI usage – with enforcement actions against several investment advisors signaling the start of a broader effort to police AI-related disclosures.

Activist investors are also interested in AI-related risks. Several shareholder proposals requesting disclosure of AI-related oversight have received high levels of support at recent annual shareholder meetings.

Our review of SEC filings from the S&P 500 for the 12 months ending April 30, 2024, paints the portrait of an evolving landscape when it comes to AI-related disclosures. It reveals trends in:

– Emerging investor expectations

– Activist investor interests

– Corporate disclosures

(Including in proxy statements and in the “Risk Factors,” “Business” and “Management Discussion and Analysis” (MD&A) sections of annual reports on Form 10-K)

What Public Companies Should Consider Doing Now

Relevant disclosure is not only appropriate but often necessary when AI becomes a material aspect of a company’s business. Investors and market regulators expect transparency, effective governance oversight and effective risk management over the numerous ways that companies are developing and deploying AI. Misrepresenting AI capabilities and failing to properly oversee risks could severely damage investor trust and lead to lawsuits and regulatory action.

Where AI has a significant impact on the business, public companies should:

– Validate AI statements and develop effective disclosure controls and procedures to support the accuracy of public AI-related disclosures.

– Develop governance structures to identify and manage AI-related risks at both the board and management level, and disclose both significant AI-related risks and oversight of those risks in required SEC disclosures.

A Closer Look at Investor Activity and Corporate Disclosure Trends

In the sections that follow, we examine AI-related disclosure trends in SEC filings across the S&P 500. We also explore the expectations of proxy advisors and activist investors, share data on increasing references to AI in annual reports on Form 10-K and highlight a potential gap in proxy statement disclosures regarding AI oversight.

Emerging Investor Expectations

While AI is an emerging priority for many investors, institutional asset managers and proxy advisors generally have not established formal guidelines regarding oversight of AI by the board or its committees.

Several major investors have identified AI as a significant opportunity for their investment activities, but most U.S.-based investors have not articulated specific expectations for oversight and management of AI by public companies.

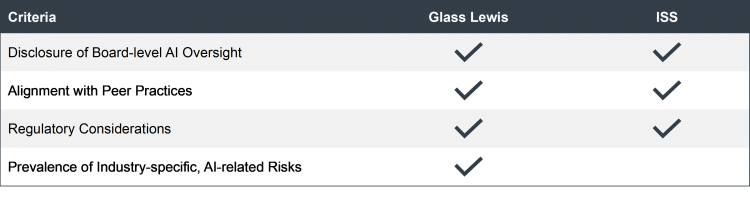

The proxy advisors Glass Lewis and ISS have identified AI as a relevant area for future policy development, but currently approach AI-related matters on a case-by-case basis. For the limited number of AI-related shareholder proposals voted on to date, Glass Lewis and ISS generally consider the following criteria when making recommendations:

Activist Investor Interests

Activist investors are also interested in AI-related issues.

We identified 13 shareholder proposals related to AI submitted in the 2024 proxy season. These proposals ask for disclosure on topics including the use of AI in company product and operations, the role of the board in overseeing AI and the prevalence of AI-related risks. Several AI-related proposals have received the support of 20 percent or more of votes cast at an annual shareholder meeting.

We expect AI-related shareholder proposals to continue to be an agenda item for activist investors, especially for companies that experience AI-related controversies or have business models at risk due to the potential impact of AI.

Be sure to check out the next installment of this three-part series, which will focus on AI-related risk factor disclosures.

– John Jenkins

Tune in at 2 pm Eastern tomorrow for the CompensationStandards.com webcast – “Proxy Season Post-Mortem: The Latest Compensation Disclosures” – to hear Mark Borges of Compensia, Dave Lynn of CompensationStandards.com and Goodwin & Ron Mueller of Gibson Dunn discuss the ins and outs of compensation disclosures during the 2024 proxy season. They’ll cover:

- The State of Say-on-Pay During the 2024 Proxy Season

- Highlights and Tips from this Year’s CD&As

- Best Practices for Disclosing Incentive Compensation Adjustments and Outcomes

- Trends in Disclosure Regarding Operational and Strategic Metrics

- Pay-versus-Performance: SEC Staff Guidance Issues and Year 2 Enhancements

- Compensation Clawback Policies – Multiple Policies/Potential Disclosure Issues

- Perquisites Disclosure and Recent Enforcement Focus

- Shareholder Proposals – Company Strategies; No-Action Trends; Activists and Universal Proxies

- Proxy Advisory Firms – Is Their Influence Starting to Wane?

- Rule 10b5-1 Plan Disclosure Developments

- Pending SEC Rulemaking

Members of CompensationStandards.com are able to attend this critical webcast at no charge. If you’re not yet a member, subscribe now. If you need assistance, send us an email at info@ccrcorp.com – or call us at 800.737.1271.

We will apply for CLE credit in all applicable states (with the exception of SC and NE, which require advance notice) for this 90-minute webcast. You must submit your state and license number prior to or during the program using this form. Attendees must participate in the live webcast and fully complete all the CLE credit survey links during the program. You will receive a CLE certificate from our CLE provider when your state issues approval, typically within 30 days of the webcast. All credits are pending state approval.

– John Jenkins

The Exchange Act celebrates its 90th birthday on June 6th. Among other things, that statute created the SEC (the FTC was the original regulator under the Securities Act). The SEC is commemorating that milestone with a webcast event featuring two panels, one comprised of former SEC chairs, and another featuring historian Michael Beschloss, legal scholar Joel Seligman, and former Maryland lieutenant governor Kathleen Kennedy Townsend. Lt. Gov. Townsend is also the granddaughter of the SEC’s first chair, Joseph Kennedy.

The SEC has a rich history that you can learn quite a bit about by visiting the SEC Historical Society’s website. For example, this excerpt from the website’s discussion of the early days of the SEC provides a reminder that strong policy disagreements among commissioners are nothing new:

The Securities Exchange Act required a bipartisan Commission. The two Republicans appointed by Roosevelt were highly experienced: George C. Mathews had directed the Wisconsin Public Utilities Commission before joining the FTC; and Robert E. Healy sat on the Vermont Supreme Court and ran an FTC investigation of public utility holding companies before joining the Commission.

Not surprisingly, some conflict arose during the sessions that the Commission held nearly every day during its first three months. Pecora continually pushed for a more adversarial approach, hoping that further revelations would lead to greater reform. Owing to his public utilities knowledge, Healy sympathized, but sided with Kennedy in the end. Landis and Mathews both agreed with the Chairman that the SEC could best establish its legitimacy and further constructive reform by easing regulations and accommodating business.

Although he respected the Chairman’s abilities, Pecora tired of being in the minority and resigned after six months. For the remainder of Kennedy’s tenure, the four Commissioners handled the heavy load alone.

The Library of Congress also has resources devoted to the Exchange Act and the SEC, including this blog on how the agency’s activities have made public company information more transparent and broadly available, and this group photo of the first commissioners.

Seated, left to right: Ferdinand Pecora, Joseph P. Kennedy, James M. Landis. Standing, left to right: George C. Matthews, Robert F. Healy.

– John Jenkins

The last time we checked in on the PPP loan program we found that the SBA had concluded that the level of fraud was apparently massive & that the loan forgiveness process was snarled in red tape. Now, bankrupt small business lender Kabbage, which was one of that program’s largest lenders, has agreed to pay up to $120 million to the federal government in order to resolve fraud allegations raised by the US Attorney for the District of Massachusetts. Here’s an excerpt from the US Attorney’s press release announcing the settlement:

The first settlement, which provides the United States with a claim for recovery of up to $63.2 million, resolves allegations that Kabbage systemically inflated tens of thousands of PPP loans, causing the SBA to guarantee and forgive loans in amounts that exceeded what borrowers were eligible to receive under program rules. As part of the settlement, KServicing Wind Down Corp. admitted and acknowledged that Kabbage double-counted state and local taxes paid by employees in the calculation of gross wages; failed to exclude annual compensation in excess of $100,000 per employee; and improperly calculated payments made by employers for leave and severance.

The United States alleged that Kabbage was aware of its errors as early as April 2020, yet Kabbage failed to remedy all incorrect loans that had already been disbursed and continued to approve additional loans with miscalculations. The resolution also provides for Kabbage to receive a $12.5 million credit for payments it previously returned to the SBA during the Department’s investigation of this alleged misconduct.

The second settlement, which provides the United States with a claim for recovery of up to $56.7 million, resolves allegations that Kabbage knowingly failed to implement appropriate fraud controls to comply with its PPP and BSA/AML obligations. In particular, the United States allege that Kabbage removed underwriting steps from its pre-PPP procedures in order to process a greater number of PPP loan applications and maximize processing fees.

The government further alleged that Kabbage knowingly set substandard fraud check thresholds despite knowledge of SBA’s concerns that fraudulent borrowers might seek to benefit from the PPP; relied on automated tools that were inadequate in identifying fraud; devoted insufficient personnel to conduct fraud reviews; discouraged its fraud reviewers from requesting information from borrowers to substantiate their loan requests; and submitted to the SBA thousands of PPP loan applications that were fraudulent or highly suspicious for fraud.

During the pandemic, we blogged about Kabbage’s problematic PPP loans to purported agricultural businesses located on Long Beach Island, NJ. In addition to being my summer vacation destination of choice, LBI has recently achieved notoriety for another summer resident’s regrettable outdoor decoration choices. Anyway, I can assure you that LBI has miles of beaches, and plenty of ice cream shops, seafood markets, restaurants and delis – but like most beach communities, it’s pretty devoid of agricultural businesses, unless the Wawa in Ship Bottom somehow counts.

– John Jenkins

We’re really looking forward to reconnecting in person with many of our old friends & meeting new ones at our “2024 Proxy Disclosure & 21st Annual Executive Compensation Conferences” in San Francisco. We have assembled a terrific group of speakers who will cover a range of timely topics over two full days of sessions on October 14th & 15th.

As many of you know, we hold our conferences in conjunction with our friends at the National Association of Stock Plan Professionals (NASPP), which is hosting its own annual conference in San Francisco that week. NASPP has set July 26th as the early bird registration deadline for its conference. We thought it would make sense to have a consistent deadline, so we’ve decided to extend our early bird deal to that date as well.

Our early bird in-person Single Attendee Price is $1,750, which is discounted from the regular $2,195 rate! If you can’t make it in person, we also offer a virtual option so you won’t miss out on the practical takeaways our speaker lineup will share, and we offer discounted rate options for groups of virtual attendees. You can register now by visiting our online store or by calling us at 800-737-1271.

– John Jenkins

Weil recently issued “The Big Three & ESG,” a report that provides guidance on BlackRock, State Street & Vanguard’s voting policies on key ESG issues. The report also addresses important policy changes announced by the Big Three in 2024, summarizes the expectations of these asset managers concerning company practices and disclosures around selected ESG topics, and highlights areas where failing to meet expectations may result in votes against directors. Here’s an excerpt with some practice pointers for public companies:

Refine Approach to Shareholder Engagement. Companies should review agendas and goals for engagement meetings with the Big Three, to ensure they reflect shareholder engagement priorities and can address as appropriate areas where the company may not be currently meeting expectations. Companies should ensure that directors and senior management participating in engagement meetings are well-briefed on material ESG-related risks and opportunities, current disclosures and practices relating to ESG topics, and do’s and don’ts of shareholder engagement.

Identify Vulnerabilities. Companies should review their disclosures and practices in light of the Big Three’s policies and guidance, to help identify where one or more of the Big Three may vote against directors and/or support shareholder proposals. Companies may work with proxy solicitors to determine the expected support of the Big Three and other major shareholders on ballot items, as well as the expected recommendations of proxy advisory firms. To reduce the risk of significant votes against directors, companies should assess director vulnerabilities and may wish to conduct additional shareholder outreach.

Refresh Materiality Analysis as to ESG-Related Risks and Board Oversight. Given significant recent ESG developments, companies should refresh their materiality analysis relating to ESG-related risks, and how ESG-related risks are integrated into the company’s enterprise risk management framework that facilitates risk identification, assessment, mitigation and monitoring. Companies should also review how the board provides oversight of material ESG-related risks and opportunities, and how this is reflected in board committee charters and related disclosure.

The report also recommends that companies confirm that their ESG narrative is cohesive across SEC filings, sustainability reports, company websites and other materials. In planning ESG disclosures for the year ahead, the report suggests that companies consider refining their ESG disclosures on certain ESG topics to better address the Big Three’s expectations.

– John Jenkins

A recent survey of 600 C-Suite executives by PwC and The Conference Board found that although they felt that boards did a pretty good job in traditional areas of responsibility, executives felt that they fell short when it came to emerging areas of oversight responsibility. This excerpt from the survey’s introduction suggests that executives also perceive overboarding as a significant concern:

Executives continue to express confidence in their boards in traditional areas such as strategy and knowledge of key business risks but are less confident about areas such as digital transformation and ESG. We’re seeing a significant increase in executives who think directors are unprepared, perhaps in large part because executives see an issue with overboarding — their top complaint. This may be one of the reasons a record-high 92% of executives advocate replacing at least one director on their board.

At least 70% of executives surveyed said that their boards were proficient in providing oversight in traditional areas such as corporate strategy, key business risks and opportunities, and executive comp. However, only a little more than 50% of those executives said that their boards were proficient in addressing the impact of digital transformation/emerging technologies and non-climate ESG risks and strategy. Finally, only 48% felt that their boards had a good grasp on US and international ESG reporting requirements.

– John Jenkins

As most of our readers know, our friend and colleague Liz Dunshee is on medical leave and has spent the last few weeks here in Cleveland recuperating from thoracic surgery at the Cleveland Clinic. Liz has asked me to thank everyone for their good wishes and to let you know that she’s doing well and is heading home to Minneapolis today. We know that you join us in continuing to wish her a speedy recovery and look forward to having her back with us soon!

– John Jenkins

Last month, Meredith blogged about the ongoing kerfuffle over whether Delaware corporations should consider reincorporating in another jurisdiction. In that blog, she cited a Wilson Sonsini memo pointing out that one of the big factors that might prompt a corporation to remain in Delaware is the ability to access the Delaware judiciary’s corporate law expertise. According to a recent blog from Keith Bishop, one newly converted Nevada corporation appears to want to keep that access:

I was doubly surprised to come across the following provision in the articles of incorporation of a corporation that had recently converted from a Delaware corporation to a Nevada corporation:

Unless the Corporation consents in writing to the selection of an alternative forum, the Court of Chancery in the State of Delaware shall, to the fullest extent permitted by law, be the sole and exclusive forum for (i) any derivative action or proceeding brought on behalf of the Corporation, (ii) any action asserting a claim of breach of fiduciary duty owed by any director, officer, other employee or stockholder of the Corporation to the Corporation or the Corporation’s stockholders . . . (iv) any action to interpret, apply, enforce or determine the validity of these Articles of Incorporation or the Bylaws . . .

The corporation’s preference to have a Delaware court interpret and apply Nevada law is one reason that Keith was “doubly surprised” by this provision. More importantly for companies that might be interested in this kind of “Nevada-ware” alternative, the other reason for his surprise was the failure of the articles to include at least one Nevada court as a forum for internal actions, which is required by Nevada’s statute.

By the way, I’m very pleased with myself for the “Nevada-ware” moniker, which I think I’ve coined. It will be interesting to see if other companies that opt to move away from Delaware try to figure out ways to take the parts of Delaware they like with them as they move to their new homes. Anyway, if Nevada-ware corporations become a thing, just remember you heard it here first.

– John Jenkins