Last week’s attack on the Capitol – I still can’t believe I’m writing those words – has prompted many companies to hit pause on their political contributions. Initially, corporate donors targeted Republican lawmakers who objected to the certification of President-Elect Biden’s victory, but many have at least temporarily halted all political contributions.

Critics have suggested that these actions are merely symbolic, and that companies will jump back into the political game once the news cycle moves on to something else. I have no doubt that they’ll be back, but it’s just possible that last week’s attack may represent a turning point when it comes to how companies approach political spending. Why? Well, this pause isn’t occurring in a vacuum, and it may help accelerate some existing and emerging trends:

– Institutional investors and companies are under increasing pressure to align their political spending with their stated priorities & to disclose more information about that spending. Ironically, on the day of the attack, Liz’s lead blog was all about BlackRock’s efforts to urge greater transparency among the companies in which it invests when it comes to corporate political activities.

– The results of the latest CPA-Zicklin survey indicate that companies themselves are continuing to become more transparent about & accountable for their political spending.

– Activist investors increasingly look for ESG hooks to expand their base of investor support for their campaigns. In an increasingly divided and volatile environment, a company’s political spending may prove to be low hanging fruit for activists.

It also looks like political spending disclosure will be a priority issue for the SEC under the Biden Administration. The SEC will need a little help from Congress if the agency intends to act on disclosure rules. As I blogged last month, Congress recently continued the bipartisan tradition of stealthily prohibiting the SEC from using any of its funding to adopt political spending disclosure rules.

Why Don’t Ex-SEC Enforcement Lawyers Join the Plaintiffs’ Bar?

This week’s announcements of the departure of the SEC’s Chief Accountant & its Acting Director of Enforcement are a reminder that a change in presidential administrations always results in an exodus of senior SEC Staff to positions in the private sector. The SEC’s senior accountants usually find their way to the Big 4 in some capacity, while many former SEC enforcement lawyers end up with positions in private law firms. However, few former SEC lawyers opt to work for firms on the plaintiffs’ side, despite the potentially lucrative nature of that work.

Michele Leder (aka footnoted.com) recently tweeted about a study that explores why that’s the case. This ProMarket blog from the study’s author suggests that the reasons are likely more complex than the simplistic “quid pro quo” explanation that usually has been put forth by academics:

While traditional academic analysis of the “revolving door” focuses on evidence of a material quid pro quo — for instance, an enforcement attorney who receives an offer of lucrative private sector employment in exchange for going “easy” on that target while she’s in government — more recent work has acknowledged that government officials may come to internalize industry preferences as a result of softer mechanisms and influences.

The rapidly revolving door between the SEC and the defense bar, and the close contact SEC attorneys have with defense-side attorneys throughout investigations and enforcement actions, give SEC attorneys ample exposure to the defense bar’s characteristic skepticism and hostility towards securities class actions and the lawyers who pursue those cases. By contrast, SEC attorneys are unlikely to have any direct contact with plaintiffs’ attorneys, even when there is a parallel private lawsuit against a company they are pursuing.

Interestingly, there is one area on the plaintiffs’ side that former SEC enforcement lawyers have apparently embraced – representing whistleblowers. The blog notes that whistleblower cases differ from traditional plaintiffs’ work in that they are oriented around the SEC itself, and permit former Staff members to leverage their unique government expertise and connections for a competitive advantage.

Yesterday, I blogged about the effective date & mandatory compliance date for the SEC’s new MD&A and financial disclosure rules. Unfortunately, there appears to be a bit of confusion within the U.S. government about when companies will be required to comply with the new rules. The version of the adopting release for the rules published in the Federal Register (p. 2109) says that the mandatory compliance date is August 9, 2021, while the updated version at the SEC’s website (p. 104) says the compliance date is September 8, 2021.

The version originally published by the SEC said that the mandatory compliance date would be 210 days after publication of the rules in the Federal Register, which gets you to August 9th. The September 8th date is 210 days after the effective date of the rules. Well, at least we have some time to sort this out – although I think the Federal Register version controls.

Update: August 9th it is! The SEC has revised the version of the adopting release on its website to conform to the Federal Register.

SEC Solicits Comment on NYSE Shareholder Approval Proposal

Last month, the NYSE submitted proposed amendments to its shareholder approval rules. On December 28th, the SEC issued a notice soliciting public comment on the proposed rule change. Here’s the intro from this Mayer Brown blog:

On December 16, 2020, the New York Stock Exchange (“NYSE”) filed a proposed rule change to certain of its shareholder approval requirements, which would bring the NYSE’s shareholder approval rules into closer alignment with those of Nasdaq. Last year, the NYSE temporarily waived certain requirements under Section 312 in order to provide listed companies with greater flexibility to raise capital during the COVID-19 crisis (the NYSE has proposed to extend these temporary waivers through March 31, 2021). The NYSE’s proposed rule change includes amendments that are identical to such waivers.

The blog also provides details on other aspects of the rule proposal. The NYSE’s temporary waiver of certain requirements under Section 312 was initially issued back in April 2020. It was originally scheduled to expire in June 2020, but was subsequently extended to the end of the year & recently extended again until March 31, 2021. The comment period on the rule proposal expires 21 days after publication of the notice in the Federal Register – or maybe September 8th, I don’t know. . .

Tomorrow’s Webcast: Glass Lewis Dialogue – Forecast for the 2021 Proxy Season

Tune in tomorrow for the webcast – “Glass Lewis Dialogue: Forecast for the 2021 Proxy Season” – to hear Courteney Keatinge of Glass Lewis, Ning Chiu of Davis Polk and Bob Lamm of Gunster discuss what to expect with the new proxy adviser rules, investors’ focus on diversity and other ESG issues, virtual meetings and other pandemic-related developments.

Earlier this week over on “The Proxy Season Blog”, Liz blogged about State Street’s efforts to ratchet up the pressure on boards to address diversity issues, which makes this webcast even more timely!

The calendar says it’s 2021, but the distressing events in Washington last week suggest that the 2020 dumpster fire continues to rage on unabated. This Bryan Cave blog says that as much as we’d all like to put 2020 in the rear-view mirror, boards should factor the year’s lessons into the topics they discuss during upcoming board evaluations. Here are some suggested supplemental discussion topics prepared with the annus horribilis in mind:

– All board members have sufficient technology capabilities, IT infrastructure and cybersecurity protections to effectively access board materials, prepare for and participate in board meetings in the virtual environment.

– Board members pay sufficient attention to environmental and social consequences and potential risks resulting from the company’s activities.

– Board members are able to clearly and effectively communicate with each other and with management in the virtual environment, enabling them to fulfill their responsibilities and make rapid and significant decisions during the COVID-19 pandemic.

– All board members, regardless of their gender, race or ethnicity, feel that their voices are heard and their contributions are respected and valued.

The blog suggests several additional topics for consideration in the self-evaluation process. It says that expanding the process to cover these topics will assist boards in learning from the events of 2020 & in taking appropriate actions to adapt to the pandemic and address the other areas of heightened investor concern that arose last year.

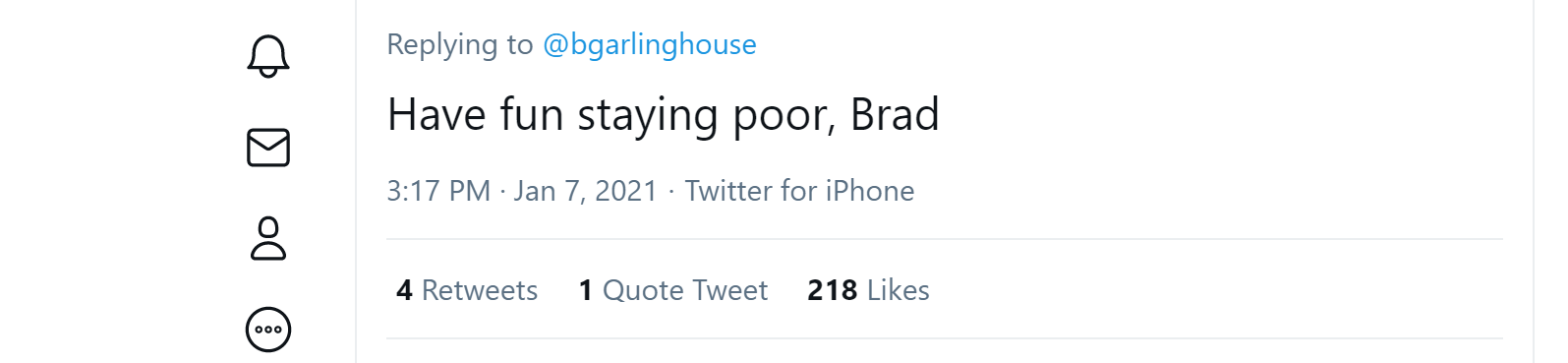

SEC Enforcement: Ripple’s “Takin’ It To The Tweets. . .”

I think the last time I blogged about the fraught relationship between the crypto folks & SEC Enforcement, I reviewed how Kik Interactive got clobbered by a federal judge after it actively courted an enforcement proceeding. Daring the SEC to bring an enforcement action is something that I have a hard time understanding, but then again, I have a hard time understanding quite a few things about the digital asset evangelists.

The latest situation to befuddle me involves Ripple Labs, which recently found itself the target of the customary SEC enforcement action alleging that its $1.3 billion unregistered offering of digital assets violated Section 5 of the Securities Act. Being crypto folks, Ripple’s management went out and did a very crypto thing in response to the SEC’s allegations. Instead of just issuing the standard press release indicating that the company intended to vigorously contest the SEC’s claims, Ripple opted to take to social media, where its CEO Brad Garlinghouse posted a 10 tweet thread addressing “5 key questions” raised by the proceeding. Not to be outdone, Ripple’s GC weighed-in with a brief thread of his own addressing the lawsuit.

Admittedly, this isn’t functionally all that much different from addressing a major piece of litigation or an SEC enforcement action in an investor call. But one of the benefits of the more traditional approach is that you avoid the baggage that comes along with the “rage as a service” platform known as Twitter – such as being on the receiving end of a grenade like this in your mentions:

Ouch! That’ll leave a mark.

MD&A & Financial Disclosures: Effective Date of the New Rules

One of our members pointed out in our Q&A Forum that the SEC’s amendments to the MD&A and financial disclosure rules were published in the Federal Register on Monday. The rules will be effective February 10, 2021 – and early compliance is permitted for filings made after that date, so long as the company provides disclosure responsive to an amended item in its entirety. However, companies are not required to comply with the new rules until the first fiscal year ending on or after August 9, 2021 (210 days after the Federal Register publication date).

Since the clock is now ticking, be sure to check out today’s webcast on the new rules!

Remember when I blogged that the Playboy Enterprises deal was “peak SPAC”? Upon further review, I think I made a bad call. On Friday, Bloomberg’s Eric Balchunas tweeted about a Form S-1 filing by a SPAC called “LMF Acquisition Opportunities, Inc,” which I think beats Playboy pretty handily. What makes this deal stand out? Well, the cover page of the prospectus discloses that the Nasdaq trading symbol for the company’s Class A Common Stock is “LMAO.” A quick perusal of the filing indicates that the company is looking to raise $75 million. I guess if it does, then it will be in a position to LMAO all the way to the bank. If that isn’t peak SPAC, I don’t know what is.

While we’re on the topic of “peak SPAC,” a recent WSJ opinion piece suggests that the “SPAC bubble” may soon burst – and that this would be a good thing for investors. This excerpt explains why:

We studied SPACs that completed mergers between January 2019 and June 2020 and found that, on average, they lost 12% of their value within six months following the merger, while the Nasdaq rose roughly 30%. Even with these drops in share price, the 20% that the sponsor gets essentially for free provides a nice return on its investment. The sponsors of these SPACs enjoyed a return on investment of more than 500% as of the end of 2020.

LMAO indeed!

IPOs: The Outlook for 2021

Baker McKenzie recently issued its 2020 IPO Report, which discusses the current year’s activity & the trends to watch for in 2021. Peak SPAC or not, it looks like SPAC deals will continue to feature prominently in the mix – at until things return to a more normal environment:

In looking at what 2021 holds for the IPO markets, the economic outlook will largely hinge on the distribution of a vaccine to COVID-19, heralding the official beginning of a return to “normalcy” and the full return of consumer confidence. As businesses successfully re-engineer their financial statements to an economic environment of recovery, we can expect to see capital raises for businesses to start expanding and investing in their growth and development, leading to a ripple effect of economic activity.

Until then, we will likely continue to see a proliferation of Special Purpose Acquisition Companies (SPACs) as well as businesses continuing to access the capital markets in conventional ways with going public, given that there remains a huge amount of dry powder in the private equity markets.

SPACs have historically been met with skepticism by the market and investors alike, but improved regulatory requirements and a number of recent high profile and successful acquisitions have helped to build the interest and momentum behind one of this year’s biggest trends. While these regulatory requirements vary across geographies, the more risk-averse framework in the US is one of the primary reasons that almost all SPAC activity takes place in New York.

The report notes that SPAC deals drove a huge increase in US domestic IPO activity during 2020, and points out that continuing tensions between the U.S. and China and the recent enactment of the Holding Foreign Companies Accountable Act has led to a number of jurisdictions, Hong Kong and London in particular, planning and introducing regulatory changes on stock exchanges in an effort to lure China-based listings away from the U.S. markets.

Tomorrow’s Webcast: “Streamlined MD&A and Financial Disclosures – Early Considerations”

Tune in tomorrow for the webcast – “Streamlined MD&A and Financial Disclosures: Early Considerations” – to hear our own Dave Lynn of Morrison & Foerster, Bryan Brown of Jones Day, Lyuba Goltser of Weil, Gotshal & Manges and John Newell of Goodwin Procter discuss the newly amended MD&A and financial disclosure rules and the benefits and drawbacks of voluntary early compliance.

In addition to allocating another $35 billion in funding for new Paycheck Protection Plan borrowers, the Covid-19 stimulus legislation also contains good news for existing borrowers. My law firm colleague Brent Pietrafese tipped me off to the fact that the legislation reverses the IRS’s position on the tax deductibility of expenses paid with the proceeds of PPP loans. This excerpt from this Forbes article on the bill’s changes to the PPP program summarizes the new approach to deductibility:

Ever since the IRS published Notice 2020-32, borrowers and tax professionals alike have put their faith in Congress to overrule the Service and provide a double benefit: tax-free forgiveness of loan proceeds AND deductible expenses paid with PPP funds. Section 276 of Division N of the latest bill does just that, providing that “no deduction shall be denied or reduced, no tax attribute shall be reduced, and no basis increase shall be denied, by reason of the exclusion from gross income.” Importantly, this rule applies to ALL borrowers; even those who have already applied for forgiveness. Thus, expenses paid with PPP funds are now completely deductible.

The legislation makes a number of additional changes to the program, including expanding the categories of expenses for which PPP loan proceeds may be used, streamlines the forgiveness process for loans under $150,000, and creates the possibility of a second round of financing for certain borrowers that have fully extinguished their prior PPP loans. Like everything else about this program, the provisions in the stimulus bill are controversial. We’ll be posting memos in our “Covid-19 Issues” Practice Area.

ESG Meets AMDG: The Council for Inclusive Capitalism

The NYT DealBook had a recent story about the Vatican’s new initiative with an international group of private sector, governmental & NGO leaders. Called “The Council for Inclusive Capitalism,” the group was formed in response to Pope Francis’s challenge to “build inclusive and sustainable economies and societies.” The DealBook article notes that the group’s members represent $2.1 trillion in market cap and 200 million employees, and that, with the Pope’s blessing, they’ve made pledges toward achieving “environmental and sustainable-business goals that fit into the E.S.G. movement.”

I’m pretty cynical about this kind of thing, and I’d ordinarily conclude that an initiative like this would likely involve more spin than substance. But my money’s on the Pope here, if only because I’m not sure that these folks fully realize with whom they’re dealing. You see, Pope Francis is a member of the Society of Jesus – better known as the Jesuits – and I’m very familiar with the capabilities of that particular organization.

I spent nearly a decade as a student at a Jesuit high school and a Jesuit college. Over the ensuing years, I’ve been very impressed at how adept these guys are at extracting financial & other commitments from a wide variety of sources in support of their projects. You don’t have to take my word for it – just ask the family who owns everybody’s favorite supermarket about my own high school’s powers of persuasion.

Over the past 500 years, the Jesuits have educated everybody from Rene Descartes to Stephen Colbert. As a result, they’ve become highly skilled at cozying up to the upper crust in order to put the bite on prevail upon them for assistance in doing “the Lord’s work.” And as this anecdote from a 2013 Guardian article illustrates, they have a reputation for getting things done:

An old joke tells of a Franciscan, a Dominican and a Jesuit who are arrested during the Russian revolution for spreading the Christian, capitalist gospel, and thrown into a dark prison cell. In a bid to restore the light, each man reflects on the traditions of his own order. The Franciscan decides to wear sackcloth and ashes and pray for light. Nothing happens. The Dominican prepares and delivers an hour-long lecture on the virtue of light. Nothing happens. Then the Jesuit gets up and mends the fuse. The light comes on.

As the payoff suggests, the Society of Jesus has always been known for practicality and unflappability in the service of its motto: Ad Maiorem Dei Gloriam (for the greater glory of God) [AMDG]. Equally well known is the Jesuits’ reputation as educators – giving rise to the adage: “Give me a child of seven, and I will show you the man.”

My guess is that during his 55 years as a Jesuit, some of this probably rubbed off on the Pope. So, if any of these companies or investors signed on to this project thinking they could commit to some ESG softballs in exchange for a “green sheen” & a photo op at the Vatican, they may be in for a bit of a surprise from the Pontiff (with whom they’ll meet on an annual basis). That’s because the Jesuits’ reputation as disciplinarians is also pretty formidable. “AMDG” isn’t the only acronym associated with the Jesuits – just ask any Jesuit high school student or alum what “JUG” is all about.

By the way, the Catholic Church isn’t the only religious group that’s decided to get in the ESG game – the Church of England is playing too, and as the English might put it, they’re “throwing a bit of stick about.“

Jay Clayton Signs Off

SEC Chair Jay Clayton issued a statement announcing that yesterday would be his final day in his position. He had previously announced that he’d leave his post by the end of the year, but somehow it seems fitting that the news came on the same day that commissioners Crenshaw and Lee issued a statement dissenting from the SEC’s approval of the NYSE’s direct listings proposal.

This is my final blog for the year, and I want to close by wishing a Merry Christmas to everyone celebrating the holiday, and a healthy & prosperous 2021 to all of our readers! This has been a very tough year for everyone, and while there are likely to be more difficult days ahead, there is also reason to believe that next year will be better. So, keep your chin up & thanks for reading!

Yesterday, the SEC announced a proposal to amend the provisions of Rule 144(d) to prohibit “tacking” of certain market-adjustable convertible or exchangeable securities. The proposal would also modify and update the filing requirements for Form 144. (Here’s the 84-page proposing release.) This excerpt from the SEC’s press release summarizes the proposed changes to Rule 144’s tacking rules:

The proposal would amend Rule 144(d)(3)(ii) to eliminate “tacking” for securities acquired upon the conversion or exchange of the market-adjustable securities of an issuer that does not have a class of securities listed, or approved to be listed, on a national securities exchange. As a result, the holding period for the underlying securities, either six months for securities issued by a reporting company or one year for securities issued by a non-reporting company, would not begin until the conversion or exchange of the market-adjustable securities.

“Market-adjustable” conversion provisions are a common feature of “toxic” or “death spiral” securities. Instead of a pre-established conversion rate, the securities are issued with a conversion rate that represents a discount to the market price of the underlying securities at the time of conversion. If there’s no cap on the number of shares that may be issued or floor on the conversion price, the market adjustment feature means that the number of shares issuable upon conversion may be enormous.

Currently, holders of convertible securities are allowed to tack their holding periods for the securities held pre- and post-conversion for purposes of calculating their eligibility to resell under Rule 144 period. As this excerpt from the proposing release points out, the SEC thinks that’s a problem for market-adjustable securities:

If the securities are converted or exchanged after the Rule 144 holding period is satisfied, the underlying securities may be sold quickly into the public market at prices above the price at which they were acquired. Accordingly, initial purchasers or subsequent holders have an incentive to purchase the market-adjustable securities with a view to distribution of the underlying securities following conversion to capture the difference between the built-in discount and the market value of the underlying securities.

The SEC thinks these sellers look a lot like statutory underwriters, and proposes to remove this incentive by amending Rule 144(d)(3) to preclude tacking in the case of unlisted market-adjustable securities. Why distinguish between these securities and listed securities? According to the release, the answer is that the NYSE & Nasdaq listing rules put a cap on the amount of shares that may be issued without shareholder approval, which limits the ability of a company to issue market-adjustable securities & reduces the concerns of an unregistered distribution.

The SEC also proposes to tweak the filing requirements for Form 144. If adopted, the rules would require a Form 144 to be filed electronically, but the filing deadline would be changed so that the Form 144 could be filed concurrently with a Form 4 reporting the transaction. Rule 144 transactions involving securities of non-reporting companies would no longer require a Form 144 filing. The proposal also would amend Forms 4 and 5 to add an optional check box to indicate that a reported transaction was made under a Rule 10b5-1 plan.

Direct Listings: SEC Approves NYSE Proposal

Let’s see, where were we on the NYSE’s direct listing proposal? Oh yeah, last August, the SEC approved the proposed rule, but shortly thereafter, it stayed the rule in response to a petition for review filed by the CII. Yesterday, the SEC lifted that stay and approved the rule. In doing so, it rejected arguments that the direct listing proposal circumvented traditional due diligence processes & created a potential “end run” around Section 11 liability.

So, will this fundamentally change the IPO process as we know it? Probably not. Sure, there will always be the high-name recognition Unicorns like Palantir that may find a direct listing to be an attractive option – particularly now that primary shares may be offered. But most IPO candidates aren’t well known & need Wall Street to play its traditional role in the process.

CF Disclosure Guidance: SPACs

Looking very much like an agency that wants to get everything off its desk before the Christmas holiday, the SEC capped off a busy afternoon yesterday with Corp Fin’s issuance of new disclosure guidance. CF Disclosure Guidance Topic: No. 11 provides Corp Fin’s views regarding disclosure considerations for SPACs in connection with both their IPOs & subsequent de-SPAC transactions.

With so many of our members working remotely, we wanted to be sure to let our print newsletter subscribers know that The Corporate Counsel and The Corporate Executive are now available electronically! Renew your subscriptions today and select electronic delivery for easier access to the ongoing practical guidance you’ll receive from both of these newsletters during the challenging year ahead. You will receive email notifications each time a new issue is released.

If you wish to sign up multiple users for the electronic newsletters, please contact customer service for pricing and assistance at info@ccrcorp.com or 1-800-737-1271. We will need to make sure we have all of the correct email addresses so we can send out login credentials for each user.

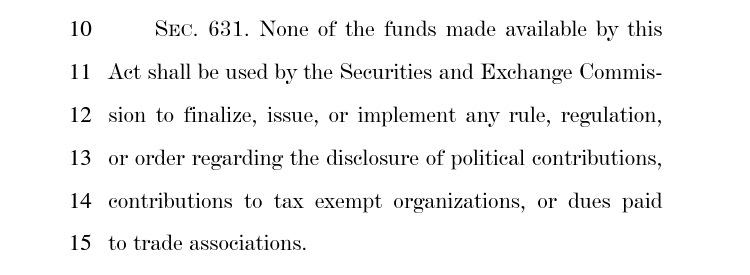

Political Contributions Disclosure: SEC Can’t Spend Funding On Rules

One of our members pointed out to us that the 2021 Consolidated Appropriations Act that Congress passed last night includes the now customary prohibition on the SEC spending any of its funds on rules requiring the disclosure of political contributions. Here it is, in all its glory:

I called this a “now customary” prohibition because Congress has been doing the exact same thing in appropriations bills for several years now. Disclosure of political contributions is a controversial issue, and the decision to ban the SEC from taking any action on it would likely be controversial too – if anybody had time to complain. Congress’s bipartisan willingness to repeatedly bury this kind of decision in one paragraph of 5,000+ page appropriations bills isn’t exactly a “profile in courage.”

November-December Issue of “The Corporate Executive”

The November-December issue of The Corporate Executive was just posted – & also sent to the printer. It’s available now to members of TheCorporateCounsel.net who also subscribe to the electronic newsletter (try a no-risk trial). This issue includes articles on:

– Tax Withholding Deposits for Stock Plan Transactions—Understanding the New Relief

– Some Deferred Compensation Plans and Employment or Stock Award Agreements May Need to be Amended by December 31, 2020

– SEC Proposes Amendments to Rule 701 and Form S-8

Last week, Liz blogged about the passage of the Holding Foreign Companies Accountable Act, which amends the Sarbanes-Oxley Act to prohibit listing on US exchanges of foreign companies for which the PCAOB has been unable to inspect audit work papers. On Friday, President Trump took time from his busy schedule – which he swears does not include declaring martial law – to sign the legislation.

Shortly thereafter, SEC Chair Jay Clayton issued his own statement on the legislation – which this excerpt suggests has thrown a bit of a monkey-wrench into the SEC’s own rulemaking initiatives regarding China-based companies:

Prior to enactment of the Act, SEC staff were finalizing recommendations for proposed rules regarding enhanced listing standards for U.S. securities exchanges and auditor qualifications for the Commission’s consideration. Because of the substantial overlap between the staff’s proposal and the Act, I have directed the staff to consider providing a single consolidated proposal for the Commission’s consideration on issues related to the PCAOB’s access to audit work papers, exchange listing standards, and trading prohibitions.

The statement says that Chair Clayton has also asked the staff to consider additional issues relating to the Act’s implementation, including how its disclosure requirements can be implemented expeditiously and how any potential uncertainties can be addressed. He also acknowledged that this “pragmatic step” means that a rulemaking proposal won’t happen during his tenure.

Innovation: In-House Departments Leave Law Firms In the Dust?

This recent Thompson Hine survey on innovation in the legal profession says that in-house legal departments are way ahead of law firms when it comes to innovative approaches to legal services. This excerpt explains:

In-house legal departments continue to face extraordinary pressures — pressures that could be eased through law firm innovation. Budgets — already taking a hit before COVID-19 — are tighter than ever in the wake of the pandemic, and companies are looking for efficiencies at every turn.

But more than two-thirds of our survey respondents said their primary outside firms had made no progress in innovation over the past year. As a result, 91% of in-house law departments have taken innovation into their own hands. The changes in-house legal departments are making on their own show their priorities.

Nearly two-thirds of our buyers cited improved project management as a key change in their legal departments. Almost half have streamlined outside counsel panels, while more than 40% have implemented self-service tools and restructured departments and/or processes. Clearly, efficiency is the order of the day, particularly when you compare the numbers with those in our first survey. Sixty-three percent of in-house law departments had improved project management in 2019 vs. 8% in 2017; 41% had restructured departments or processes vs. 8% in 2017; and 33% had outsourced to alternative legal services providers in 2019 vs. 3% in 2017.

The survey suggests that law firms’ reluctance to innovate may be causing them to miss out on new business opportunities – 53% of in-house respondents would consider hiring a new law firm because it is innovative.

Cheat Sheet: 2020 Capital Markets Rulemaking

If you’re like me, you’re probably having a little trouble keeping up with the avalanche of rulemaking from the SEC over the past several months. If you find yourself in that position, you may want to hang on to a copy of Skadden’s 2020 Capital Markets Regulatory Review. This 13-page document provides a brief overview of some of the key capital markets and corporate governance reforms that have taken effect in 2020 or are poised to take effect in 2021.

Prof. Sarah Haan of Washington & Lee Law School recently posted a draft article online that’s eye opening, to say the least. In short, her thesis is that a trend that scholars have overlooked – the explosive growth in the percentage of stock owned by women during the early decades of the 20th century – played a major role in the development of the modern paradigm for public company corporate governance. Here’s an excerpt from the article’s abstract:

Corporate law scholarship has never before acknowledged that the early decades of the twentieth century, a transformational era in corporate law and theory, coincided with a major change in the gender of the stockholder class. Scholars have not considered the possibility that the sex of common stockholders, which was being tracked internally at companies, disclosed in annual reports, and publicly reported in the financial press, might have influenced business leaders’ views about corporate organization and governance.

This Article considers the implications of this history for some of the most important ideas in corporate law theory, including the “separation of ownership and control,” shareholder “passivity,” stakeholderism, and board representation. It argues that early twentieth-century gender politics helped shape foundational ideas of corporate governance theory, especially ideas concerning the role of shareholders. Outlining a research agenda where history intersects with corporate law’s most vital present-day problems, the Article lays out the evidence and invites the corporate law discipline to begin a conversation about gender, power, and the evolution of corporate law.

Some of the language in the abstract may make the article sound a little wonky, but in reality, it’s accessible and engaging. It sounds cliché to call a work “groundbreaking,” but I can’t come up with a better word to describe this one. I’m sure they’ll be plenty of back & forth among governance scholars on the merits of Prof. Haan’s arguments, but my take is that she may have put her finger on something that’s been hiding in plain sight for a long time.

Revenue Recognition: E-Commerce Disclosures a Sleeper Issue?

Many companies have seen their e-commerce sales explode as a result of the pandemic and, not surprisingly, many have also called this growth out in earnings releases & other disclosures. This Bass Berry blog says that the new requirement to disclose “disaggregated revenues” under ASC 606 may be a “sleeper issue” for some of these companies. Here’s an excerpt:

Under ASC 606-10-50-5, a public company must “disaggregate revenue recognized from contracts with customers into categories that depict how the nature, amount, timing, and uncertainty of revenue and cash flows are affected by economic factors.” Additionally, per the implementation guidance in ASC 606-10-55-90, when selecting the type of category (or categories) to use to disaggregate revenue, an entity should consider how the information about the entity’s revenue has been presented for other purposes, including the following:

– Disclosures presented outside of the financial statements such as MD&A, earnings releases and investor presentations.

– Information regularly reviewed by our Chief Operating Decision Maker (CODM).

– Any other information similar to the information identified in (1) and (2) that is used by the company or users of the financial statements to evaluate the company’s financial performance or make resource allocation decisions. (emphasis added)

In determining the categories to include, ASC 606-10-55-91 says that an entity should consider the following examples:

– The type of good or service (e.g., major product lines).

– Geographical region (e.g., country or region).

– Market or type of customer (e.g., government or non-government customers).

– Type of contract (e.g., fixed-price or time-and-materials).

– Contract duration (e.g., short- or long-term).

– Timing of transfer of goods or services (e.g., point-in-time or over time).

– Sales channels (e.g., direct to customers or through intermediaries).

The blog acknowledges that the company’s accounting staff and its outside auditor will make the final analysis on this issue, but suggests that the continued focus on e-commerce in public company disclosures might prompt more companies to conclude that they should disaggregate revenues by sales channels, including e-commerce sales. It also cautions that disaggregate revenue disclosure continues to be an area of interest for the Staff, and cites a recent comment letter exchange as an example of some of the issues that might be raised.

Blockchain & Beyond: FinHub Gets an Upgrade

In 2018, the SEC announced the establishment of “FinHub” within Corp Fin. Since then, FinHub has served as a resource for public engagement on blockchain & other FinTech-related issues and initiatives. Yesterday, the SEC announced that FinHub was being upgraded to an independent office. This excerpt from the SEC’s press release explains the decision:

Designating FinHub as a stand-alone office strengthens the SEC’s ability to continue fostering innovation in emerging technologies in our markets consistent with investor protection. The office will continue to lead the agency’s work to identify and analyze emerging financial technologies affecting the future of the securities industry, and engage with market participants, as technologies develop.

FinHub’s existing Director, Valerie Szczepanik will continue to serve in that capacity, and will “coordinate the analysis of emerging financial innovations and technologies across the SEC’s divisions and offices and with global regulators and will advise the Commission and SEC staff as they develop and implement policies this area.”

The SEC’s pre-Thanksgiving rulemaking frenzy gave my colleagues Liz & Lynn plenty to blog about over the last couple of weeks. In contrast, the well has been a little dry this week in terms of breaking news. That’s left me scrambling a bit for blog topics. I knew I had a couple of SPAC-related blogs in the hopper, but SPACs aren’t a topic with broad appeal outside of the folks in the IPO and M&A crowd. So, I wanted to hold off on them until I found a lead blog that would make the topic more relatable & interesting.

Fortunately, I recently stumbled across just what I was looking for – a SPAC story featuring a bona fide A-List celebrity! That’s because no less than Jay-Z himself has decided to participate in the SPAC boom. According to this Bloomberg article, he has signed on to serve as an officer for a cannabis SPAC:

Subversive Capital Acquisition Corp., a special-purpose company that’s growing in the cannabis business, said it acquired two California companies and named Shawn “Jay-Z” Carter as its chief visionary officer. Subversive is buying Caliva, a cannabis brand with direct-to-consumer sales, and Left Coast Ventures Inc., a producer of cannabis and hemp products. The deals will create a new holding company and include $36.5 million of equity commitments from new and existing shareholders.

The holding company, which will be called TPCO Holding Corp., expects revenue from the combined entities to be $185 million in 2020 and $334 million next year. The deals’ aim is to “both consolidate the California cannabis market and create an impactful global company.” The new company aims to reach 75% of California consumers and Jay-Z will run its brand strategy and work on a related project to reform criminal justice.

Jay-Z may be the only A-lister to become an exec at a cannabis-related business, but he’s far from the only celeb backing one. We’ve already blogged about Snoop Dogg’s venture capital activities targeting “The Chronic”, and the cannabis beverage brand Cann recently announced a number of its own celebrity investors, including the likes of Gwyneth Paltrow & Rebel Wilson.

If you think I get unduly excited when I find an excuse to blog about celebs – well, you’re probably right. The truth is that I’m a frustrated gossip columnist who would dearly love a gig on TMZ or Page Six.

To SPAC or Not to SPAC? That is the Question. . .

This Cooley blog has a lot of information about how the SPAC market continues to grow & evolve, but there’s one aspect of it in particular that I thought readers of this blog might find interesting – a discussion of the differences and similarities between a SPAC transaction and a traditional IPO. This excerpt addresses timing considerations:

Despite common misconceptions, the timeline for completing a de-SPAC transaction and an IPO are comparable—often between four to six months, although that timeframe can vary depending on SEC review and comment. In a SPAC transaction, parties can expect to take approximately four to six weeks to negotiate a business combination agreement and line up a PIPE, and then another two to four months to prepare and file a joint Form S-4/proxy and deal with any SEC comments. Just as it would in a traditional IPO, the target must be prepared to provide the required financial information and other documentation necessary to operate as a public company, including PCAOB financials.

Other topics addressed include lockups, SEC review, Rule 144 limitations applicable to SPACs, & governance matters. The blog also addresses key trends in de-SPAC transactions, which represent the biggest difference between the SPAC & traditional IPO route to the public market.

SPACs: Auditor Market Share

One of the interesting things about SPAC deals is the relative absence of the involvement of Big 4 audit firms. In fact, as this Audit Analytics blog reviewing auditor market share for SPACs makes clear, the market is dominated by two non-Big 4 firms:

When it comes to blank check initial public offerings (IPOs), two firms dominate the market: Withum and Marcum. Together, these two firms account for 90.2% of all blank check IPOs from January 1, 2019 to September 30, 2020, with 156 companies raising over $47.7 billion. Only two Big Four firms audited a blank check company at the time of IPO during this period; KPMG, with three clients, and PwC, with one.

What accounts for the relative absence of Big 4 firms from the blank check/SPAC market? An earlier blog suggests some reasons:

While blank check IPOs and SPACs have raised billions and can offer a quick public offering, the type of transaction can pose unique challenges, especially for auditors tasked with preparing the necessary filings. There are special considerations and nuances for these transactions and based on these complexities; it is not surprising that some audit firms have specialized teams for SPACs, while others prefer to focus business elsewhere.

Non-Big 4 firms’ dominance of this part of the IPO market isn’t a new development. The blog says that while the Big 4 had over 70% of the market share for all IPOs from 2004-2019, they had only 6.5% of the market share for blank check IPOs.