Broc Romanek is Editor of CorporateAffairs.tv, TheCorporateCounsel.net, CompensationStandards.com & DealLawyers.com. He also serves as Editor for these print newsletters: Deal Lawyers; Compensation Standards & the Corporate Governance Advisor. He is Commissioner of TheCorporateCounsel.net's "Blue Justice League" & curator of its "Deal Cube Museum."

Today is the “Pay Ratio & Proxy Disclosure Conference”; tomorrow is the “Say-on-Pay Workshop: 14th Annual Executive Compensation Conference.” Note you can still register to watch online by using your credit card and getting an ID/pw kicked out automatically to you without having to interface with our staff. Both Conferences are paired together; two Conferences for the price of one.

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take about a day to post the video archives after it’s shown live). A prominent link called “Enter Pay Ratio Conference Here” – on the home pages of those sites – will take you directly to today’s Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: HTML5, Windows Media or Flash Player). Here are the “Course Materials,” filled with 182 pages of annotated model pay ratio disclosures, 156 pay ratio nuggets, talking points, etc.

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here is today’s conference agenda; times are Eastern.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if that is possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see this “List: CLE Credit By State.”

SEC Comments: What’s the New “SWAT” Process?

Recently, a member posted this question in our “Q&A Forum” (#9233): “Back on September 18th, Broc blogged about Corp Fin having a new SEC comment letter process. Is the whole “Swat” thing something that is a big difference in how Corp Fin is processing comment letters?” This was my answer:

SWAT is a workflow system that will better document the Staff’s comment letter process, make everything available to everyone on the Staff more easily, provide reports and reminders, etc. It’s all internal and won’t have any impact on what companies see. So it’s just a workflow system. No real impact on what is commented upon…

Corp Fin’s “Climate Change” Comments: The Coming GAO Report

By the way, the announcement about SWAT was buried in the SEC’s Inspector General report about Corp Fin’s comment letter process. That report was pretty innocuous and not of any great moment.

I forgot to note why the IG prepared that report. In July of last year, some members of Congress sent a letter to the IG (and to GAO) asking that they review the SEC’s efforts to implement the climate change guidance of 2010 and assess Corp Fin’s comment letter process. These members of Congress were of the view that Corp Fin should be issuing more comments and they wanted to understand why that was not the case.

This IG report says that the GAO will report separately on its observations related to the SEC’s climate change-related policies & procedures. Now that should be interesting…

Recently, I blogged how the SEC’s Edgar is critical to a transparent financial market – and how the recent hack of Edgar is serious business. This Reuters article notes that Edgar could be at risk from “denial of service” attacks. Even worse news comes from this excerpt:

The memo shows that even an unintentional error by a company, and not just hackers with malicious intentions, could bring the system down. Even the submission of a large “invalid” form could overwhelm the system’s memory.

Hopefully, Congress will do the reasonable thing and give the SEC more resources (they need it in all sorts of areas – including to investigate when it is hacked, as noted in this article). Edgar arguably is held together with duct tape and no one should act surprised that it was hacked. The NSA can’t even avoid getting hacked.

By the way, this new bill that would subject credit bureaus – like Equifax – to federal cybersecurity reviews cracks me up. As if the federal government will be using its best cyber resources to review the security of outside entities – it can’t even protect its own systems…

Your Sensitive Information Was Accessed in a Government Hack? No Remedy?

This Davis Polk blog notes that those who have their personal information stolen during a hack of a government database are unlikely to have a remedy. And this Davis Polk blog wonders whether the hack of Edgar will result in a delay of the Consolidated Audit Trail (which will consist of a central repository for SROs and broker-dealers to submit extensive information in standardized formats regarding securities trading activity)…

The SEC’s New “Cyber” Unit: Getting the Band Back Together!

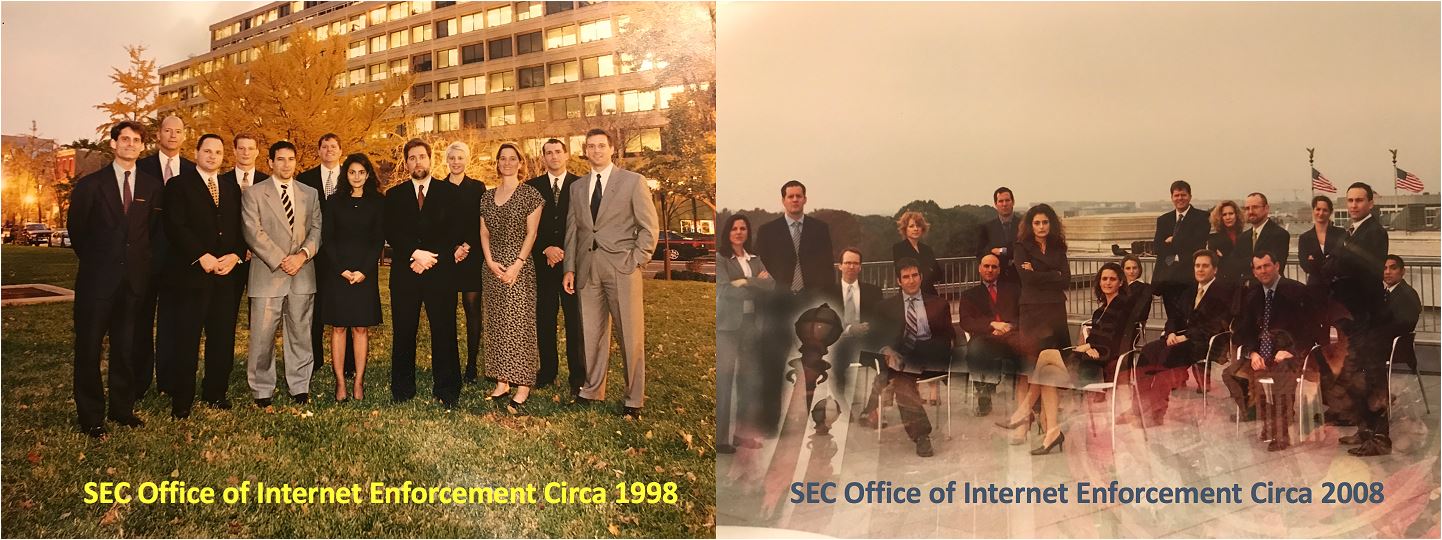

Last week, I blogged about the challenges that the SEC will face hiring cybersecurity experts given the extreme shortage of that resource. On a lighter note, it is interesting that the SEC’s Division of Enforcement disbanded its “Office of Internet Enforcement” in 2009, recognizing that the entire Division really should have expertise in that area. Now with the SEC creating a similar “Cyber” unit, John Reed Stark shared this great pic of his former office on LinkedIn:

Perhaps you thought the FAST Act was way behind us – but remember the SEC still hasn’t adopted some rules required by Dodd-Frank. Yesterday, the SEC proposed a variety of rules and form changes as required by the FAST Act. Here’s the 253-page proposing release; we’ll be posting memos in our “Disclosure Effectiveness” Practice Area. In this blog, Cydney Posner highlights some of the proposals, including:

1. Limit the period-to-period comparison required in MD&A to only the two most recent fiscal years presented in the financials, so long as the earlier period discussion is no longer material to understanding the financials and it has been included in the previous 10-K.

2. Allow companies to omit or redact confidential information from material contract exhibits that is not material and would cause competitive harm if publicly disclosed, without having to submit an unredacted copy and prior formal request to the Corp Fin Staff, as is currently required. This is intended to change process only & will not be intended to change the substantive requirements.

3. Limit the two-year “look back” requirement for exhibits to apply only to newly reporting companies.

4. Clarify that disclosure regarding properties is required only to the extent that the property is material.

5. Require inline XBRL tagging for all cover page information – and require the cover page to include the (tagged) ticker symbol for each class of securities registered under the Exchange Act.

6. Require disclosure of legal entity identifiers (“LEIs”) for the company & any significant subsidiaries identified on Exhibit 21.

7. Require links to information incorporated by reference from previously filed documents.

In this blog, Ning Chiu does a great job of listing the seven ways that periodic reporting could change…

Pay Ratio: How to Handle PR & Employee Fallout

For those coming to next week’s “Pay Ratio & Proxy Disclosure Conference,” you’ll hear tidbits about the hot “employee reaction” topic all day long – but particularly during the panel entitled “Pay Ratio: How to Handle PR & Employee Fallout.” Recently, as noted in this press release, Willis Towers Watson found that this was the topic of largest concern when it surveyed companies. Here’s an excerpt:

Indeed, roughly half of the respondents polled (49%) cited forecasting how their employees will react to the ratio disclosure as their number one challenge, but that other challenges still loom. About four in 10 (39%) said determining the consistently applied compensation measure (CACM) is their great challenge followed by getting accurate pay data (38%), deciding how to craft their required disclosure (37%) and determining where their pay ratio stands compared with that of their peers, their industry and the market (35%).

We continue to post new items regularly on our “Proxy Season Blog” for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– More on “Showing Off Your Directors Via Video”

– Shareholder Proposal Reform: Keith Higgins Wades In…

– Showing Off Your Directors Via Video

– Proxy Season: Steps to Take Now to Prepare

– Online Disclosure & Mobile IR Websites: S&P 500 Study

This is one of 4 reports coming out of Treasury dealing with various types of reform. In this Treasury Report, there’s a bunch of recommendations that impact our area of law – and most of them can be accomplished at the agency level, not needing action by Congress. We’re posting memos in our “Regulatory Reform” Practice Area.

As noted in Steve’s blog, the list includes (but is certainly not limited to):

1. Repeal of Section 1502 (conflict minerals), Section 1503 (mine safety), Section 1504 (resource extraction), and Section 953(b) (pay ratio) of Dodd-Frank. In the absence of legislative action, the SEC should consider exempting smaller reporting companies (SRCs) and emerging growth companies from these requirements.

2. The SEC should move forward to remove SEC disclosure requirements that duplicate financial disclosures required under GAAP by the FASB.

3. Companies other than EGCs be allowed to “test the waters” with potential investors who are QIBs or institutional accredited investors.

4. $2,000 holding requirement for shareholder proposals should be substantially revised.

5. Resubmission thresholds for repeat proposals be substantially revised from the current thresholds of 3%, 6%, and 10%.

6. SEC should continue its efforts, when reviewing company offering documents, to comment on whether the documents provide adequate disclosure of dual class stock and its effects on shareholder voting.

7. Modify rules that would broaden eligibility for status as an SRC and as a non-accelerated filer to include entities with up to $250 million in public float as compared to the current $75 million.

8. Extend the length of time a company may be considered an EGC to up to 10 years, subject to a revenue and/or public float threshold.

9. Expand Regulation A eligibility to include Exchange Act reporting companies.

10. Tier 2 offering limit should be increased to $75 million.

11. The SEC, FINRA and the states propose a new regulatory structure for finders and other intermediaries in capital-forming transactions.

12. Accredited investor definition should be amended with the objective of expanding the eligible pool of sophisticated investors.

13. Review of provisions under the Securities Act and the Investment Company Act that restrict unaccredited investors from investing in a private fund containing Rule 506 offerings.

Here’s a “Fact Sheet” for the Report. Also see Appendix B of the Treasury Report (pg. 203) for a tabular breakdown of the recommendations by topic…

Today’s Webcast: “Evolution of the SEC’s OMA”

Tune in today for the DealLawyers.com webcast – “Evolution of the SEC’s OMA” – to hear Michele Andersen, Associate Director of the SEC’s Division of Corporation Finance & Ted Yu, Chief of the Corp Fin’s Office of Mergers & Acquisitions, Skadden’s Brian Breheny, Weil Gotshal’s Cathy Dixon, Alston & Bird’s Dennis Garris and Morgan Lewis’ David Sirignano in a discussion of how the Corp Fin’s Office of Mergers & Acquisitions has evolved over the years…

Mandatory Arbitration: Bad for Defendants?

In July, John blogged about SEC Commissioner Piwowar’s apparent support for mandatory arbitration clauses – which historically have been considered contrary to public policy & potentially inconsistent with Securities Act anti-waiver provisions.

This blog from Lane Powell’s Doug Greene explains why a shift to mandatory arbitration wouldn’t be the panacea that companies are looking for – in fact, they might be a lot worse off. Here’s a teaser:

These arbitrations would be unmanageable. Each plaintiffs’ firm would recruit multiple plaintiffs to initiate one or more arbitrations—resulting in potentially dozens of arbitrations over a disclosure problem. Large firms would initiate arbitrations on behalf of the institutional investors with whom they’ve forged relationships, as the Reform Act envisioned. Smaller plaintiffs’ firms would initiate arbitrations on behalf of groups of retail investors, which have made a comeback in recent years.

We often object to lead-plaintiff groups because of the difficulty of dealing with a group of plaintiffs instead of just one. In a world without securities class actions, the adversary would be far, far worse—a collection of plaintiffs and plaintiffs’ firms with no set of rules for getting along. Securities-disclosure arbitrations would cost multiple times more to defend and resolve.

All this to say – if a policy shift does come to fruition – we’re not sure it’ll be quickly embraced.

Tune in today for the webcast – “E&S Disclosures: The In-House Perspective” – to hear National Vision’s Jared Brandman, Davis Polk’s Ning Chiu, Bristol-Myers Squibb’s Kate Kelly, Apple’s Jung-Kyu McCann and Clorox’s Stephanie Tang discuss environmental & social disclosure issues – in both SEC filings & other types of filings.

SASB Proposes ESG Disclosure Standards

As Ning notes in her blog, the Sustainability Accounting Standards Board (SASB) released draft standards for Environmental, Social and Governance (ESG) disclosure last week, launching a 90-day public comment period which ends on December 31st. Four years in the making, these standards set forth ESG topics covering 11 different sectors and 79 industries for public companies to disclose annually.

Ning has a link to where the exposure draft resides. I decided not to do so – because I’m dismayed that one can only receive a copy if you fill out a form. Studies show that downloads of documents dramatically go down if you force people into providing their personal information – even if the document is free. I dislike this practice – particularly for something like this that has a regulatory feel…

Heads Up! Legal Entity Identifier (LEI)/MiFID II Deadline

A member recently asked in our “Q&A Forum” (#9237): “It appears that several EU firms are reaching out to U.S. public companies to obtain a Legal Entity Identifier (LEI) in advance of the new EU financial markets regulation (MiFID II and MiFIR) becoming effective (or risk that company shares cannot be traded in Europe after January 3, 2018). Are public companies applying for LEI’s, and if so, how? It looks like Bloomberg is an accredited issuer of LEIs as a Local Operating Unit (LOU), but I’m just trying to get a handle on how other public companies are responding any why.”

I asked a few in-house friends about this – and they were unaware of this requirement. We posited some potential thoughts on this topic in response to the query in the “Q&A Forum” – and now the first law firm memo is out about it. Send more!

– How to Attend by Video Webcast: If you are registered to attend online, just go to the home page of TheCorporateCounsel.net or CompensationStandards.com to watch it live or by archive (note that it will take a few hours to post the video archives after the panels are shown live). A prominent link called “Enter the Conference Here” – which will be visible on the home pages of those sites – will take you directly to the Conference (and on the top of that Conference page, you will select a link matching the video player on your computer: HTML5, Windows Media or Flash Player).

Remember to use the ID and password that you received for the Conferences (which may not be your normal ID/password for TheCorporateCounsel.net or CompensationStandards.com). If you are experiencing technical problems, follow these webcast troubleshooting tips. Here are the conference agendas; times are Eastern.

– How to Earn CLE Online: Please read these “FAQs about Earning CLE” carefully to see if it’s possible for you to earn CLE for watching online – and if so, how to accomplish that. Remember you will first need to input your bar number(s) and that you will need to click on the periodic “prompts” all throughout each Conference to earn credit. Both Conferences will be available for CLE credit in all states except for a few – but hours for each state vary; see our “CLE Credit By State” list.

– Register Now to Watch Online: There is still time to register for our upcoming pair of executive pay conferences – which starts on Tuesday, October 17th – to hear Keith Higgins, Meredith Cross, etc. If you can’t make it to Washington DC to catch the program in person, you can still watch it by video webcast – either live or by archive. Register now to watch it online.

– Register in Washington DC to Watch In-Person: Starting next Thursday, October 12th, you will no longer be able to register to attend in Washington DC through this site – but you can always register to attend when you arrive in DC! You just need to bring payment with you to the conference and register in-person. But until next Thursday, you can still register online to attend in DC…

Transcript: “Pay Ratio Workshop – What You (Truly Really) Need to Do Now”

We have posted the transcript for our recent pre-conference webcast: “Pay Ratio Workshop – What You (Truly Really) Need to Do Now.” Now get ready for the main event taking place in less than two weeks in Washington DC and by video webcast – 20 pay ratio panels over 2 days: “Pay Ratio & Proxy Disclosure Conference.” It’s time to register now…

SEC Seeks to Enhance Cybersecurity Expertise: Good Luck With That…

Yesterday, SEC Chair Clayton gave testimony before the House Financial Services Committee about the SEC’s budget for the agency’s next fiscal year. The Chair noted that he intended to ask for a $100 million increase over the $1.6 billion budget that the SEC currently has – and also planned to ask permission to lift the hiring freeze currently in place.

The main reason for the additional funds would be to enhance the SEC’s cybersecurity efforts. This article excerpts the key paragraph from the Chair’s testimony:

“The $234 million that the SEC plans to spend on information technology in fiscal year 2018 is quite modest, by way of comparison, to the amounts that the major Wall Street firms spend on their own information technology systems,” he said. “For example, in 2016 one large financial institution alone spent more than $9.5 billion on technology firm-wide, with $3 billion of that dedicated to new initiatives. Another large financial institution spent $6.6 billion in 2016 on technology initiatives.”

That paragraph says it all. When many are predicting a very serious shortage of cybersecurity expertise in the near future, how is a government agency able to compete in recruiting cybersecurity people worth their salt? The government is quite limited in the pay packages it can offer. It’s going to be a very uphill climb – even if Congress agrees to give the SEC this additional money…

Yesterday, I blogged about the seriousness of the SEC’s Edgar being hacked (and what we know – & don’t know – about that hack). Today, let’s delve into “what does it mean for those of you that are in-house?” For purposes of this blog, I’m assuming a different type of scenario than the Edgar hack that was just disclosed by the SEC. Something more sinister – such as a hacker going in and changing the numbers in a company’s financials, etc.

John has come up with your “11-step plan of action” if one of your company’s filings on Edgar is hacked:

1. Review your prior filings and press releases on your website and the EDGAR database to determine whether they have been altered from their original versions.

2. Keep a hard copy of your SEC filings “at the ready.” If Edgar is hacked – and it’s your filing being manipulated – you may need something that you know isn’t tainted. It’s hard to taint a hard copy.

3. Have a plan in place to react to your SEC filing being hacked. This includes a list of who you’re going to call first (think senior management, the board, your stock exchange, etc.). And what you’re going to say. After verifying the accuracy of prior filings & coming up with an action plan, contact your stock exchange rep to either confirm to them that any prior filings they’ve looked at are valid – or tell them what you’re working to correct.

4. This is instantly a board matter. Contact the head of the audit committee or other appropriate committee charged with risk oversight immediately. The SEC and the FBI should also be on the short list of people you contact (the SEC’s Enforcement Division has just formed a special unit in this area). Tell your Assistant Director in Corp Fin what has happened and what you are doing to address it early on in the process.

5. Don’t assume that your filing is the only thing that’s been hacked or that it’s the SEC’s fault. Proceed under the assumption that your most sensitive internal systems have been hacked and initiate an investigative and cybersecurity response on that basis. Also, proceed under the assumption that the hack has been going on for a long time. Just blaming the SEC right away might not be appropriate – maybe it was someone at your company (or your financial printer, etc.) that screwed up.

6. Your top public communications priority needs to be correcting the record or acting to disseminate material non-public information that may have been comprised. If the hack has resulted in inaccurate disclosure (e.g., if your filing was hacked), correct it immediately and succinctly. If you have reason to believe that it has resulted in a leak of MNPI, get the information out immediately.

7. Move! Time is of the essence. Don’t get bogged down in narrow legal issues about whether you have a duty to speak. Depending on the circumstances, you may or may not have a legal obligation to do this – but one of the big problems is that you likely won’t know right away where the responsibility for the breach lies. Remember, you will be judged by investors and regulators in part based on how prompt, thorough and transparent your response to the problem is.

8. Credibility is essential. Be as transparent as possible. Don’t spin. Don’t speculate. If you don’t know something, tell people that. If you can’t discuss something, say so and be upfront as to the reasons why.

9. As part of your investigation, review trading activity surrounding prior SEC filings and communications (including any comment letters and responses) to determine whether there has been any unusual activity.

10. Immediately impose a blackout on insiders under your insider trading policy & review recent insider transactions (first thing the media will look at, even though it may be completely irrelevant).

11. If your company sends “test” filings through Edgar, reconsider that practice – or perhaps shorten the window between when you submit a test filing and a “live” filing. And of course, avoid posting earnings releases, etc. online before they are supposed to – remember that series of “URL-sniffing bots” fiascos from a few years back…

John notes: “I don’t know if you’ve seen the show “Mr. Robot,” but it’s basically what “Fight Club” would look like if it was written by smart people. Anyway, the show’s about a group of hackers who bring down the social order by hacking into and destroying personal financial information held by a large corporation (sound familiar?). One of the points the show makes is that in an information-based economy, everything is based on trust. Whether you have any responsibility for the hack or not, people’s trust in YOU has been undermined by it. That fundamental point should underscore every move you make in response.”

Non-GAAP: Does Reg G Apply to M&A Projections?

Here’s something that John blogged on our “DealLawyers.com Blog“: Most public company M&A disclosure documents include a section addressing the forecasts provided to the board and the company’s financial advisors in connection with their evaluation of the transaction. These forecasts typically include non-GAAP financial information, but Rule 100(d) of Reg G provides an exemption from its requirements that applies to disclosures summarizing “the bases for and methods of arriving at” a fairness opinion.

While these forecasts appear to be well within the scope of the exemption, plaintiffs – and in some cases the Staff – have challenged this assumption in the case of non-GAAP information disclosed under a separate heading (typically captioned “Forecasts” or “Projections”) from the discussion of the banker’s fairness opinion. Some have also called into question the applicability of this exemption to tender offer filings.

This Cleary blog sets forth a detailed argument that these distinctions are inappropriate – and that the reconciliation requirements of Reg G do not apply to this information, regardless of what type of disclosure document it appears in or where it appears. Here’s an excerpt summarizing the argument:

It is true that the projections in the “Forecasts” section of M&A disclosure documents include projections that are not GAAP. Indeed, projected unlevered free cash flows are a central input into any discounted cash flow analysis. But in our view the contention that these projections are subject to Regulation G is incorrect.

The provision of a GAAP reconciliation for these forecasts would not serve the purpose for which Regulation G was adopted – namely, to prevent a company from misleading investors by providing NGFMs that obscure its GAAP results and guidance. No such concern applies to the “Forecasts” section of M&A disclosure documents, where the data are being provided solely to enable shareholders to understand the specific, projected financial metrics that the company’s financial advisor used in its financial analyses to support a fairness opinion.

The blog notes that the Staff has sometimes issued comments to the effect that Reg G applies to these disclosures, and recommends that the Staff issue interpretive guidance confirming that the exemption applies to forecasts included in M&A disclosure documents.

I’m concerned that some folks aren’t worried enough about the SEC’s Edgar being hacked. I’ve seen a number of blogs about SEC Chair Clayton’s cybersecurity statement that didn’t bother to even mention the most important item in that statement: Edgar was hacked! Perhaps that was a byproduct of the SEC “burying the lead” when it stuck that revelation in the middle of a 5-page statement about cybersecurity generally.

But make no mistake about it, this is a huge development. Don’t be numb because hacking news has become so routine. John’s blog about the Chair’s statement keyed in on this theme with his title of “Wow! Edgar Hacked!”

If such breaches continue, or if the SEC is too underfunded or outgunned to fix them, it could undermine company and investor confidence in the agency. That might threaten the regulator’s ability to provide a bedrock principle of the U.S. financial system: market transparency.

The SEC’s Hacking Incident: What We Know (& Don’t Know)

The SEC is certainly now taking the hacking seriously. Yesterday, SEC Chair Jay Clayton issued this update on the breach since the agency has now found that personal information for at least two individuals was hacked (see this Reuters article).

And culling through the written testimony from Chair Clayton before the Senate Banking Committee last week – and the media pieces about that (WSJ’s Andrew Ackerman has penned several pieces; this is the latest), here’s a few things we know – and don’t know:

1. Management Kept in the Dark – Although the breach was reported in 2016 to the Department of Homeland Security and the security gaps were patched, SEC Commissioners and the SEC’s then-COO were unaware of the 2016 hack. It’s not known when in 2016 the hacking took place.

2. SEC Has Enforcement Action Pending – An ongoing enforcement probe prevents the SEC from revealing many details about the cyber incident – so there’s a probe into possible illegal trading (or “outside trading” as John Stark describes it). Chair Clayton did disclose that the investigation, which he learned about last month, spurred a second look at the breach.

3. Sparse Facts Known So Far – The SEC hasn’t revealed the type of information accessed by hackers in 2016 nor which companies were affected. So we don’t know which filings were hacked – nor which companies might have been affected by the breach. Chair Clayton’s statement says the SEC’s Inspector General is probing the source of the hack, the type of information obtained and how the SEC responded internally to the breach – he decided to disclose the SEC’s own breach as soon as he had enough information to accurately inform market participants and investors.

4. “Customized” Part of Edgar Enabled the Hack – The hackers exploited a vulnerability in the “customized” part of Edgar that allows companies to test the accuracy of data transmitted in new forms. The SEC has hired outside consultants to test the vulnerability of its systems.

Survey: Boards Not Sharing Cyber Incident News

It apparently isn’t only the SEC that is slow to share the fact that a cyber incident occurred. This recent BDO survey found that just one-quarter of boards (25%) are sharing information gleaned from cyber-attacks with external entities! The survey also found that boards are more involved with cybersecurity than they were 12 months ago – and a similar percentage (78%) say they have increased company investments during the past year to defend against cyber-attacks, with an average budget expansion of 19%.

For those registered for the upcoming “Pay Ratio & Proxy Disclosure Conference,” tune in tomorrow – 2 pm eastern (audio archive goes up when the program ends; transcript available in a week or so) – for the third in a series of three monthly webcasts that serve as a pre-conference: “Pay Ratio Workshop: What You (Truly Really) Need to Do Now.” There will be a heavy emphasis on “what now” given the SEC’s new guidance.

– Mark Borges, Principal, Compensia

– Ron Mueller, Partner, Gibson Dunn

– Dave Thomas, Partner, Wilson Sonsini

– Amy Wood, Partner, Cooley

Register Now: This is the only comprehensive conference devoted to pay ratio – and it’s only three weeks away! Here’s the registration information for the “Pay Ratio & Proxy Disclosure Conference” to be held October 17-18th in Washington DC and via Live Nationwide Video Webcast. Here are the agendas – 20 panels over two days. Register today.

ISS Releases ’18 Policy Survey Results

Yesterday, ISS released the survey results for its upcoming policy changes – with findings including:

– Unequal Voting Rights – ISS solicited respondents’ views on multi-class capital structures that carry unequal voting rights. Among investors, a large minority (43 percent) indicated that unequal voting rights are never appropriate for a public company in any circumstances. An equal proportion of investors (43 percent) said unequal voting rights structures may be appropriate for newly public companies if they are subject to automatic sunset requirements or at firms more broadly if the capital structure is put up for periodic re-approval by the holders of the low-vote shares.

– Board Gender Diversity – ISS asked respondents if they would consider it problematic if there are zero female directors on a public company board. More than two-thirds (69 percent) of investor respondents said “yes.” The lion’s share of these respondents (43 percent) said that the absence of women directors could indicate problems in the board recruitment process, while 26 percent of investor respondents said that although a lack of female directors would be problematic, their concerns may be mitigated if there is a disclosed policy/approach that describes the considerations taken into account by the board or the nominating committee to increase gender diversity on the board.

– Virtual Meetings – Survey respondents were asked to provide their views on the use of online mechanisms to facilitate shareholder participation at general meetings, i.e., “hybrid” or “virtual-only” shareholder meetings. About one out of every five (19 percent) of the investors said that they would generally consider the practice of holding either “virtual-only” or “hybrid” shareholder meetings to be acceptable, without reservation. At the opposite extreme, 8 percent of the investors did not support either “hybrid” or “virtual-only” meetings.

More than one-third (36 percent) of the investor respondents indicated that they generally consider the practice of holding “hybrid” shareholder meetings to be acceptable, but not “virtual-only” shareholder meetings. Another 32 percent of the investor respondents indicated that the practice of holding “hybrid” shareholder meetings is acceptable, and that they would also be comfortable with “virtual-only” shareholder meetings if they provided the same shareholder rights as a physical meeting.

– Pay Ratio Disclosures – ISS asked respondents how they intend to analyze data on pay ratios. Somewhat surprisingly, only 16 percent indicated that they are not planning to make use of this new information. Nearly three-quarters of the investor respondents indicated that they intend to either compare the ratios across companies/industry sectors, or assess year-on-year changes in the ratio at an individual company or use both of these methodologies. Of the 12 percent of investors who selected “other” as their response, some of them indicated a wait-and-see approach while other comments indicated uncertainty or concerns regarding the usefulness of the pay ratio data. Among non-investor respondents, a plurality (44 percent) expressed doubt about the usefulness of such pay ratio data.

Say-on-Pay: Despite Few “Failures,” 12-14% Run Into Problems

Here’s the intro from this interesting blog by Davis Polk’s Ning Chiu:

Although the failure rate for 2017 say-on pay results achieved an all-time low of just 1.3%, the number belies the fact that more than 2,000 say-on pay proposals have either received negative recommendations from ISS or less than 70% support, or both, since say-on-pay resolutions started in 2011.

Approximately 12% to 14% of companies run into problems every year. As companies have become more proactive with shareholder engagement, the number of companies that received “against” recommendations from ISS and still achieved more than 70% support has increased in the last three years, while the number of companies with those negative recommendations that received less than 70% favorable votes have fallen. What may be most surprising to companies, however, is that about 10 to 15 companies each year received positive endorsement from ISS and still obtained less than 70% support.

For those registered for the upcoming “Pay Ratio & Proxy Disclosure Conference,” we have just posted this invaluable set of course materials: The “Pay Ratio Employee Considerations” Guide. For many companies, the biggest issue related to the new pay ratio rule is how to message employees who might be angry about how their pay relates to the pay ratio median – not to mention the CEO’s pay package.

We decided to release these course materials early since so many are grappling now with the type of issues addressed in this “How to” manual. This topic will be addressed numerous times during the two days of the upcoming “Pay Ratio & Proxy Disclosure Conference” in mid-October – and it will also be addressed in our third pre-conference webcast coming up next week (on Wednesday, September 27th).

We decided to release these course materials early since so many are grappling now with the type of issues addressed in this “How to” manual. Just like the upcoming “Pay Ratio & Proxy Disclosure Conference” in October will comprehensively address these – and many more – issues. This comprehensive pay ratio event is one that you can’t afford to miss. Also remember that our third pre-conference webcast is September 27th.

Register Now: This is the only comprehensive conference devoted to pay ratio. Here’s the registration information for the “Pay Ratio & Proxy Disclosure Conference” to be held October 17-18th in Washington DC and via Live Nationwide Video Webcast. Here are the agendas – 20 panels over two days. Register today.

Sustainability Reporting: Internal Controls

The push for sustainability reporting continues to gain momentum – see last month’s blog about the G20 recommendations. But one largely unresolved question is how to go about verifying the data that would be included in this type of disclosure. This 55-page white paper examines how to use COSO’s internal controls framework to improve confidence in sustainability performance data. Here’s a teaser:

Sustainability performance (or related nonfinancial data) has unique characteristics. It is less tangible and more qualitative than financial performance data—although sustainability data is often quantifiable, as reported by companies in sustainability and corporate social responsibility (CSR) reports. It is also more forward-looking, covering multiple time periods, and often more manually sourced.

To improve confidence in sustainability performance data, a different “lens” on assurance and materiality may need to be taken relative to financial data, with professional judgment at the forefront. We believe the COSO principles on effectiveness—controls that are present, functioning, and integrated—could apply to all types of performance data, including sustainability, using professional judgment.

Yet “sustainability” has many—and often confusing or conflicting—definitions. Is it sustainability of the enterprise, thereby impacting reputation and “license to operate”? Is it about specific sustainability measures like climate control or deployment of human capital? Does it capture ESG measures? Is it all of the above?

Despite the confusing and sometimes conflicting lexicon, which we don’t attempt to solve in this paper, there is one important commonality: Sustainability performance data, combined with financial data, is important for the organization to manage and to (voluntarily) communicate its value-creation capacity and capability to global stakeholders.

Say-on-Frequency: Remember to File Your “Decision” 8-K/A!

Many companies held a “say-on-frequency” vote in 2017. If you fall in that category and haven’t already disclosed your frequency decision – now’s the time! Here’s an excerpt from this Davis Polk memo:

If the company does not report its decision in the initial Form 8-K, the due date for the Form 8-K/A is the earlier of 150 days after the annual meeting and 60 days before the next Rule 14a-8 shareholder proposal deadline, as disclosed by the company in its proxy statement. This deadline is rapidly approaching for many companies that held annual meetings in May 2017.

Failure to comply with these Form 8-K deadlines results in a loss of Form S-3 shelf eligibility. In 2011, many companies overlooked the requirement to disclose their decision on the frequency of say-on-pay votes, assuming that since the shareholder advisory vote matched the board’s recommendation, no further disclosure was necessary. Because the SEC staff recognized that many companies simply hadn’t understood this disclosure requirement, the staff routinely granted waivers of the shelf eligibility defect. It is not yet clear how the staff will handle similar waiver requests this year.