In light of the SEC’s recent trend of tacking on “disclosure controls” violations to charges about non-financial disclosures, I was somewhat heartened to see that the recent “director independence” enforcement action reflected a settlement with the former director, but no action against the company.

It appears the company took standard steps to collect info about director relationships that might affect the “independence” determination:

– Providing a questionnaire with a non-exclusive list of relationships that could affect independence and asking both broad & specific questions to gather information,

– Instructing D&Os to “exercise great care” in providing answers (worth a shot!), and

– Giving the director the opportunity to review and comment on the proxy statement before it was published.

Alas! Although it’s still nice the company wasn’t charged with wrongdoing here, it’s a stretch to rely on this settlement for comfort that these steps will always be adequate. That’s because, in this particular case, it appears the SEC just brought charges relating to proxy disclosures under Exchange Act Section 14(a) and Rule 14a-9 (even though this disclosure had been incorporated into the company’s Form 10-K). If there were no Section 13(a) charges, a disclosure controls charge would be off the table.

The gist of the rule, as amended, is that if you use a reverse stock split to regain compliance with the minimum bid price requirement, and that causes you to fall below the minimum number of publicly held shares and holders that Nasdaq standards require, you don’t get extra time to cure the new violation. The SEC notice gives more detail – here’s an excerpt (also see this Cooley blog):

Under the proposed rule, such company will not be considered to have regained compliance with the Bid Price Requirement if the company takes an action to achieve compliance and that action results in the company’s security falling below the numeric threshold for another Exchange listing requirement without regard to any compliance periods otherwise available for that other listing requirement. In such event, the company will continue to be considered non-compliant until both: (i) the other deficiency is cured and (ii) thereafter the company meets the bid price standard for a minimum of ten consecutive business days, unless Nasdaq staff exercises its discretion to extend this ten-day period as discussed in Rule 5810(c)(3)(H).

If the company does not demonstrate compliance with (i) and (ii) during the compliance period(s) applicable to the initial bid price deficiency, Nasdaq will issue a Staff Delisting Determination Letter.

This rule is separate from the one I blogged about earlier this week on “accelerated delistings” for penny stocks – although both involve Rule 5810. In fact, this blog has been corrected a couple hours after publication to reflect the distinction. Nasdaq probably had good reasons for making these two separate proposals, but those reasons aren’t clear to me, and I apologize for adding to any confusion in the original blog post!

Spencer Stuart recently published its 2024 Board Index – which always includes valuable data points about board composition and governance practices in the S&P 500. The Index also spotlights trends over the 1-, 5-, and 10-year periods.

One thing that jumped out, which Meredith also discussed in a recent podcast with ESGAUGE’s Paul Hodgson, is the small but noticeable shift away from mandatory director retirement policies. According to Spencer Stuart’s data, 67% of S&P 500 boards still have a retirement policy – but that’s a decrease from 69% last year and 73% in 2014. Moreover, at companies that do have policies in place, the mandatory retirement age has been creeping up (from approximately 72 to approximately 75, with the average being 74). This A&O Shearman memo from late last year articulates why some companies are reconsidering mandatory retirement policies:

Given the challenges described above and the focus on individual directors, it seems certain that boards will feel a sense that the pace of the need for refreshment is accelerating. Traditional models for ensuring reasonable turnover on the board, such as mandatory retirement age and term limits are blunt tools that may not result in the optimum outcomes in terms of board configuration and deliberation, especially at crucial moments in a company’s evolution. Also, these approaches may lead to a loss of experience, leadership or critical skills at an inopportune time.

Boards need to consider whether these methods operate as crutches to avoid difficult interactions about continued service or hobble their plans for refreshment. A flexible approach, where length of service and other factors are considered in the renomination process, may prove more effective, especially if coupled with a board culture that is more accepting of director departures when tenure, skills or other factors call for it, fostered by strong leadership and constant communication about the board’s needs.

Spencer Stuart’s 2024 Board Index shows that the move away from mandatory retirement policies isn’t happening in a vacuum. 28% of boards work with a third party to facilitate the evaluation process (up from 25% last year), and 47% conduct individual director evaluations as part of their process. Additionally, in just 4 years, the percentage of boards that include a director skills matrix in their proxies has almost doubled (from 38% in 2020 to 73% in 2024).

The result of all this work on refreshment? In 2024, boards across the S&P 500 added a total of 406 new independent directors, which is up from last year but down from the 432 directors added in 2019. Average tenure is unchanged from last year – but it’s dropped by 3% over the past 5 years and 7% over the past 10 years. I’m cautious about drawing too many conclusions from high-level stats, when boardroom dynamics are so company specific. But it appears that *maybe* third-party evaluations, investor voting policies, and a shareholder activism environment where “nobody is safe” may be spurring the types of hard conversations that actually affect the refreshment rate.

“You get out of it what you put into it,” is how my high school track coach always responded when we begged for an “easy” practice. As much as I disliked that response back then, over the years I’ve found that it’s a workable mantra for just about any scenario: including board evaluations.

We all know that there’s a wide divergence across the 99% of companies who conduct some form of evaluation. The Spencer Stuart 2024 Board Index offers a couple of pointers that can help turn board assessments into a meaningful tool for continuous improvement. Here’s an excerpt:

– Run frequent & robust board assessments: Boards should conduct meaningful evaluations via an independent third party every two or three years. In addition, the annual evaluation should include getting feedback from the management team to ensure a 360-degree review process for assessing the board’s contributions, effectiveness and areas for improvement.

– Implement individual director evaluations: Peer evaluations, carried out by an independent third party, should be conducted every two or three years.

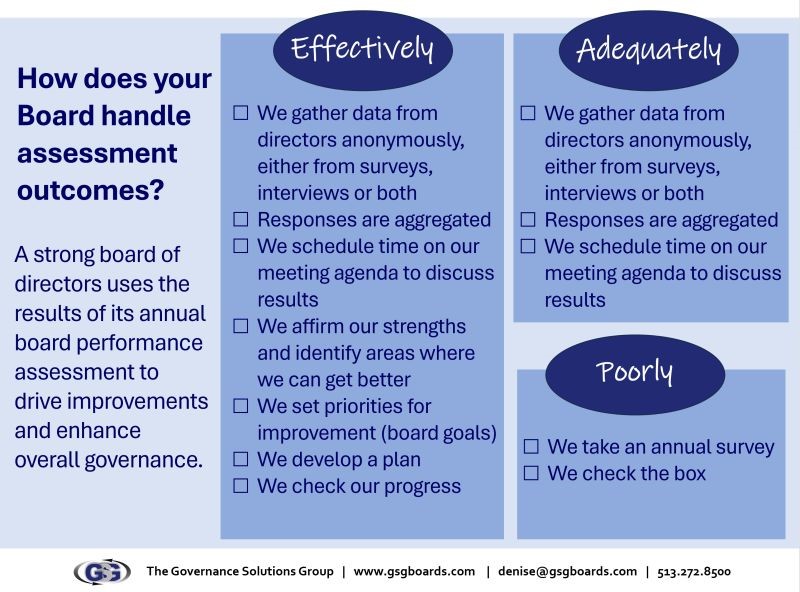

I also love this infographic from Denise Kuprionis at The Governance Solutions Group, which shows that a few basic steps can help boards get more out of the evaluation process:

Yesterday, the NACD announced a new “Blue Ribbon Commission” report to assist directors with overseeing the strategic opportunities & risks of rapidly evolving technologies. If you’re advising boards, be on alert that this may prompt questions and/or projects. The Executive Summary articulates the factors driving “technology governance” – and provides 10 recommendations for boards:

Strengthen Oversight

1. Upgrade board structures for technology governance.

2. Clearly define the board’s role in data oversight.

3. Define decision-making authorities for technology at board and management levels.

4. Ensure trustworthy technology use by aligning it with the organization’s purpose and values.

Deepen Insight

5. Establish and maintain necessary technology proficiency among the board.

6. Evaluate director and board technology proficiency.

7. Ensure appropriate and clear metrics for technology oversight.

Develop Foresight

8. Recognize technology as a core element of long-term strategy.

9. Design board calendars and agendas to ensure appropriate focus on forward-looking discussions.

10. Enable exploratory board and management technology discussions.

It’s worth noting that at many companies, the strategic importance of technology is one of the factors influencing board refreshment. The Spencer Stuart 2024 Board Index reports that technology/telecommunications was the most common industry background of new directors who joined S&P 500 boards this past year. That said, while it’s helpful to have a “tech director,” they typically aren’t “one-trick ponies” – and the full board (or a committee) still has oversight responsibility. NACD’s toolkit (for members) includes resources on evaluating director technology proficiency and assessing technology governance.

It’s hard to believe we are just one week away from our “Proxy Disclosure & 21st Annual Executive Compensation Conferences” – bundled together as one great event that you can attend with us in person in San Francisco or virtually!

On October 14th, we’ll take a deep dive into the upcoming proxy season with the “2024 Proxy Disclosure Conference” – with panels on shareholder activism, governance & disclosure of AI, cyber-related disclosure trends, shareholder proposal trends, climate disclosure updates, and more. Plus, you don’t want to miss our first-ever “All-Star Feud,” during which our intrepid “SEC All-Stars” will face off gameshow-style over burning questions on proxy disclosure and executive compensation.

On October 15th, we turn our attention to critical executive compensation matters at the “21st Annual Executive Compensation Conference” – including key updates on proxy advisors, clawback practices, compensation trends, and perks.

In addition to live and on-demand access to these fast-paced sessions, Conference attendees get exclusive access to our Course Materials – which include unique & practical bullet points and examples from our experienced speakers on each topic we’ll be covering. Our speakers go the extra mile to provide usable takeaways. The Course Materials are an invaluable resource to refer back to as proxy season approaches!

For those seeking CLE credit, here’s a list of states in which credit is available – and CLE FAQs about live and on-demand credit.

Act Now: The Conferences begin next Monday, October 14th. With 17 sessions over 2 days, you’ll walk away with action items to help support director elections and say-on-pay, leverage your executive compensation, and avoid costly mistakes. You can still register. Sign up online or by calling 1-800-737-1271.

Lastly, if you have registered, remember that your unique access link and attendance instructions will be emailed to you from no-reply@events.ringcentral.com. Here’s more detail on what to watch for.

Late last week, the SEC posted notice that it was extending the time period for action on Nasdaq’s proposal to accelerate the delisting process for non-compliance with minimum bid price requirements. I blogged about the proposed amendment when it was published in August – and Meredith shared follow-up commentary that AI and biotech startups are most at risk of delisting if the rule is approved.

The Commission has now designated November 21st as the date by which it will either approve or disapprove, or institute proceedings to determine whether to disapprove, the proposed rule change.

I’m delighted to return, with Vontier’s Courtney Kamlet, for the 6th season of our “Women Governance Trailblazers” podcast. In our latest 20-minute episode, we interviewed Karen Boykin-Towns, who is an independent director at iFit, Vice Chair of the NAACP National Board of Directors, President/CEO of Encore Strategies, and a Senior Advisor of FGS Global. Karen is also a former Pfizer executive (her leadership roles include its first-ever Chief Diversity Officer in 2008). We discussed:

1. Karen’s career path, current endeavors and what she’s been most proud of over the course of her career.

2. Karen’s thoughts on the current state of corporate diversity, equity and inclusion programs and commitments.

3. How companies can balance the call to numerically measure progress in DEI initiatives with the arguments that inclusion can’t be measured and that quotas create legal risk.

4. Karen’s experience on the iFit board, including the decision to withdraw the company’s IPO.

5. Advice to boards and management for adapting to rapidly shifting information, and for monitoring their corporate reputation and emerging issues before they become a crisis.

6. What Karen thinks women in the corporate governance field can add to the current conversation on the societal role of companies.

To listen to any of our prior episodes of Women Governance Trailblazers, visit the podcast page on TheCorporateCounsel.net or use your favorite podcast app. If there are “women governance trailblazers” whose career paths and perspectives you’d like to hear more about, Courtney and I always appreciate recommendations! Shoot me an email at liz@thecorporatecounsel.net.

As John noted here and Alan noted over on the Section16.net blog, last week the SEC announced yet another enforcement sweep in the area of beneficial ownership and Section 16 reporting. As part of the sweep, the SEC announced settled charges against 23 entities and individuals for failure to timely report about their securities holdings and transactions in public company securities. The SEC brought similar “sweep” cases in this area in the past, including in 2014, 2015 and 2023. As in the past, the SEC has made clear that it uses the agency’s data analytics capabilities to identify the reporting violations that Enforcement then pursues.

Notable among these numerous cases is that, in two of the cases, the company had undertaken to make Section 16 filings for its insiders, but the filings were repeatedly late, and the company also failed to make required disclosures regarding delinquent Section 16 filings. As we all know, the individual insiders (e.g., officers, directors and greater than 10% shareholders) have the obligation to file their required Section 16 reports; however, in most situations that I have seen over the years, companies voluntarily take on the obligation to file the Section 16 reports for officers and directors (and sometimes significant shareholders). This voluntary undertaking happens out of “market” practice and a genuine desire on the part of the company to make things more convenient for the insiders, but as these recent SEC sweep cases demonstrate, a company can face some legal consequences for late filings and missed disclosures when things go awry.

In two of the cases involving a large number of late Section 16 filings, the SEC charged the companies who voluntarily accepted the responsibility to file the insider’s Section 16 reports with causing the Section 16(a) violations. As one Order Instituting Cease-and-Desist Proceedings notes:

14. Although the Commission encourages the practice of many issuers to assist insiders in complying with Section 16(a) filing requirements, issuers who voluntarily accept certain responsibilities and then act negligently in the performance of those tasks may be liable as a cause of Section 16(a) violations by insiders.

15. Since at least 2018, Respondent has voluntarily agreed with its officers and directors, as well as two other greater than 10% beneficial owners, to perform certain tasks in connection with the filing of Section 16(a) reports on their behalf, including the preparation and filing of all such reports for which Respondent had timely notification of the required information concerning the transactions. However, on multiple occasions, Respondent acted negligently in its performance of such tasks and was a cause of Legacy insiders failing to file Section 16(a) reports on a timely basis. The procedures and practices employed by Respondent were insufficient to the extent that those practices resulted in the recurrent failure to meet the two-business day filing deadline.

16. For example, between July 2019 and July 2022, Respondent’s insiders filed more than 200 untimely Forms 4 to report transactions related to, among other things, open-market stock sales and award grants of stock and options to officers and directors. Although Respondent had agreed to perform all tasks in connection with preparing and filing such reports, the reports were not timely filed due to Respondent’s negligent procedures and practices.

17. As a result of the conduct described above, Respondent was a cause of certain violations of Section 16(a) of the Exchange Act and Rule 16a-3 thereunder by Respondent’s insiders.

The company was also charged in this case with failing to disclose the late filings pursuant to Item 405 of Regulation S-K, noting:

11. Respondent failed to make the required Item 405 disclosure for its 2019, 2020, and 2021 fiscal years by improperly omitting it from its Forms 10-K filed with respect to such fiscal years. Respondent’s Forms 10-K filed with respect to such fiscal years purported to provide all Part III information required, such as information regarding its executive officers, directors, corporate governance and other required matters, but failed to include any Item 405 disclosure and did not state that it was incorporating by reference any information from other filings. An issuer may only omit the disclosure if there are no Section 16(a) delinquencies to report, and numerous Legacy insiders had multiple delinquent filings during each of its 2019, 2020, and 2021 fiscal years. Respondent also did not file an amendment to such Forms 10-K not later than 120 days after the end of the fiscal year covered by the Form 10-K to provide such information or file a definitive proxy statement no later than the end of the 120-day period that included such information.

These latest sweep cases emphasize the need to implement robust procedures and controls whenever a company voluntarily takes on the obligation to file SEC reports on behalf of insiders. While there is no one-size-fits-all approach that can apply to every situation, companies should consider:

1. Dedicating sufficient resources to the company’s Section 16 filing responsibilities, including providing sufficient staffing, training and resources such as Section16.net;

2. Establishing clear lines of responsibility for the preparation, review, approval and filing of the Section 16 reports in a timely manner;

3. Establishing a robust tracking system for monitoring transactions by and holdings of insiders that facilitates the prompt reporting of transactions;

4. Educating insiders and company personnel on the consequences of late or missed Section 16 filings and emphasizing the importance of timely communication with the company whenever transactions in company securities are contemplated;

5. Emphasizing to insiders the importance of promptly responding to requests to approve Section 16 reports that the company has prepared so those filings can be made within a two business day timeframe;

6. Leveraging the preclearance process applicable to insiders in the company’s insider trading policy as an “early warning system” for upcoming Section 16 filings;

7. Implementing appropriate follow-up procedures so that someone outside of the process of preparing the report is checking to see if the Section 16 report is on track to be timely submitted to the SEC;

8. Utilizing appropriate questions in D&O Questionnaires to solicit information about potential filing delinquencies so those delinquencies can be addressed and reported in accordance with the company’s disclosure obligation under Item 405 of Regulation S-K;

9. Establishing procedures for amending reports or filing late reports in a timely manner when it is determined that an error has occurred; and

10. Periodically reviewing the Section 16 filing process to determine if improvements can be made to the process and procedures.

Are there other procedures that you have put in place to facilitate the timely filing of Section 16 reports? Send them my way, I would love to hear from you!

I don’t know about you, but in the current high-risk environment that we live in, I seem to have risk factors running through my brain on a loop and it is very difficult to quiet them down. I suspect that is a message to me that it is a good time to revisit public company risk factor disclosure as we enter yet another reporting cycle to see if any material updates are warranted in this particularly risky time. Here are my top five risk areas that seem to haunt me the most:

1. Political risks – As we have seen in the past two Presidential elections, some companies are including risk factors that address the political uncertainties that we face in this country and the potential consequences for public companies.

2. Conflict risks – With the continued war in Ukraine and rising tensions in the Middle East, companies should continue to review their risk factors concerning geopolitical risks and conflict around the world.

3. Cybersecurity risks – The cybersecurity threat environment only seems to get scarier every day, so it is always a good idea to stay current in your disclosure concerning the nature of that threat environment and the incidents that the company has been experiencing.

4. Artificial intelligence risks – As companies increasingly integrate generative AI into their business, risk factor disclosure should continue to evolve as risks with AI continue to reveal themselves.

5. Climate risks – While the SEC’s climate disclosure rules remain on pause, the SEC’s 2010 climate guidance is still applicable to your public disclosures, including the guidance about risk factor disclosure. Weather-related events over the course of the past year have certainly emphasized areas where companies may encounter climate risk in their daily operations, so it is important to keep any risk factor disclosure on this topic up-to-date.

Keep in mind that risk factors should be tailored to provide investors with an accurate and complete view of the risks that the company faces. Further, it is not sufficient to highlight a risk in the abstract or as a hypothetical risk when company has experienced that risk.