The SEC Enforcement Division’s “EPS Initiative” appears to be alive & well – by the looks of an “cease & desist” order from earlier this week – which resulted in a $4 million settlement (and a $75k penalty against the person who served as Chief Accounting Officer – and later, Chief Financial Officer – of the company in question). The claims were settled on a “neither admit nor deny” basis.

In the SEC’s telling, the internal controls & supporting documents for the bonus accruals left gaping holes that allowed for manipulation. Here’s an excerpt from the SEC’s order:

15. On October 7, 2015, during the closing process for the third quarter of 2015, Nash directed the accrual of $300,000 for the PB Bonus Plan, which had not yet been approved by Gentex’s Board of Directors. This journal entry was made without any supporting documentation. Additionally, Nash did not maintain documentation of any purported analysis that was required to be performed pursuant to Accounting Standards Codification (“ASC”) Topic 450, Contingencies, concerning the loss contingency associated with the PB Bonus Plan.

16. On October 8, 2015, Nash realized that the initial accrual of $300,000 would cause Gentex to miss the consensus EPS estimate of $0.27 for the third quarter of 2015. He directed a journal entry to reduce the $300,000 accrual to $100,000. The journal entry for the revised accrual was again made without any supporting documentation and Nash did not conduct any analysis that should have been performed pursuant to ASC 450-20 concerning the PB Bonus Plan.

17. In an October 9, 2015 email exchange with the CFO, the CFO asked Nash if he had reserved some money for the PB Bonus Plan. Nash responded, “100K. had [sic] 300K, but had to reduce in order to keep .27 per share.” The CFO replied, “[g]ood call. That puts in line with consensus, right?” to which Nash replied, “[y]es.”

There were other internal controls sins here too, according to the SEC – but I was surprised that this $200k accrual adjustment appears to be so central to the case. That doesn’t seem like a lot in the grand scheme of things, but the company would have missed consensus EPS estimates by one penny if the adjustment hadn’t been made – and the SEC’s data analytics tools were sensitive enough to pick up something fishy with the situation.

One moral of this story is that if the SEC comes knocking, you want to make sure to have documentation of your internal controls & accounting analysis instead of a conversation about managing EPS to the consensus number.

Here’s something I blogged yesterday for members of CompensationStandards.com:

A few pay versus performance disclosures are starting to roll in! This is something that we’ve all been eagerly awaiting – and I send my condolences to those who have had to be brave and take the first leap. These are from smaller companies – we continue to await a large-cap example. Thanks to Aon’s Corporate Governance & ESG Advisory Group for alerting us!

– Praxis Precision Medicines Form 10-K (pg. 136) – It is unclear to me why the company included this disclosure in a Form 10-K – as this Goodwin FAQ points out, the SEC rules only require pay vs. performance disclosure in proxy & information statements; it isn’t required in Form 10-K even when other Item 402 disclosure is included. But I didn’t read this filing or the company’s filing history in-depth to understand whether there is a reason they might have wanted to go ahead with it here.

– Panbela Therapeutics Form S-1/A (pg. 72) – Seems to have missed some of the disclosure requirements, but has the distinction of being the first to report under the new rule.

If you aren’t already a member of CompensationStandards.com, now is a good time to sign up. That’s where we are sharing the latest updates & analysis on the new pay vs. performance rules, along with updates on say-on-pay, ESG metrics, and other “executive compensation” hot topics. Email sales@ccrcorp.com or visit our membership center to start a no-risk trial. Our “100-Day Promise” guarantees that during the first 100 days as an activated member, you may cancel for any reason and receive a full refund. If you have any questions, email sales@ccrcorp.com – or call us at 800.737.1271.

I blogged earlier this week on CompensationStandards.com and on this site about whether to include the two new “clawbacks”-related checkboxes on your Form 10-K cover page this year. The Dodd-Frank clawback rules are not yet effective – but the checkboxes are included on the cover page of the updated Form that the SEC has published. There was lingering confusion after Corp Fin’s CDI a couple of weeks ago.

I’ve now heard from a few folks that the Staff has confirmed in informal conversations that you should include the checkboxes (but don’t need to mark them). If you are concerned that a blank checkbox could be misleading, you could add an explanatory note to the effect that the checkboxes are blank pending adoption of the underlying rules.

When it comes to finding unconventional ways to raise cash, AMC will find a way – and selling equity to do it is a key part of the meme stock playbook, as another retailer’s offering this week showed. Two years ago, the company abandoned a proposal to increase its authorized number of common shares because its retail investors weren’t showing up to deliver the votes needed for approval of the charter amendment. That temporarily shut off the spigot of raising capital through stock sales.

Undeterred, last summer AMC used its blank check preferred provision to issue a new class of shares: APEs (that stands for “AMC Preferred Equity,” of course). Here’s the Form 8-K they filed at the time. Each APE unit has terms identical to 1/100th of a share of common stock – including voting rights – and will automatically convert to common stock if & when AMC is able to issue enough common shares to cover the conversion of all of the APEs.

Now, with the APEs unfortunately trading at a 65% discount to the equivalent common shares as of year-end, AMC is going back to its common shareholders to once again seek approval for a higher number of authorized common shares, which would trigger the preferred stock conversion, as well as to effect a 1-for-10 reverse stock split for the existing common shares. The interesting part is that with this go-round, it will include votes from the APE holders – and AMC baked in a key provision to make approval more likely. In a column last week, Bloomberg’s Matt Levine pointed out that AMC’s deposit agreement for the APEs includes this language:

In the absence of specific instructions from Holders of Receipts, the Depositary will vote the Preferred Stock represented by the AMC Preferred Equity Units evidenced by the Receipts of such Holders proportionately with votes cast pursuant to instructions received from the other Holders.

Proportionate voting! This is a bold move as at least one major brokerage firm has moved away from proportionate voting for common stock and asset managers are pushing pass-through voting despite the generally low voter turnout from retail investors. It’s too soon to know whether pass-through voting will do more harm than good to individual shareholders – the early consensus is that it will just make solicitations more complicated & costly for companies, and give proxy advisors more influence. For this specific charter amendment – and with the preferred stock in the mix – AMC has possibly found a way to bring in a vote despite these hurdles.

Last week, a jury in a securities class action lawsuit found in favor of Elon Musk for his 2018 “funding secured” tweet – in which he said he was considering taking Twitter private at $420 per share and had locked in the funding. Here’s a NYT article about the outcome. The SEC had also taken issue with those tweets, resulting in a $40 million settlement and the “Twitter sitter” – plus a lot of animosity from Elon towards the Commission.

All I can say is that I’m nearly as happy as Elon that we can finally put this saga to bed. There’s no real takeaway for other companies because the jury’s verdict appeared to rest on the determination that nobody takes Elon Musk’s tweets all that seriously – and at the same time, they trust him to get things done when he really wants to.

So, investors truly may not have cared if instead of “funding secured,” the tweet had said “I might have a handshake deal for funding” – because it’s Elon Musk and he’ll either bring in the money when he wants to, or the whole thing was a joke in the first place. Did the statement really cause people to buy Tesla stock at an inflated price? The jury apparently was not convinced of that.

The reason this doesn’t translate well to other companies is that Elon Musk has carefully (or not-so-carefully?) cultivated a free-wheeling, Teflon persona and a cult-like following. It would be difficult & risky for other public company CEOs to emulate that. We don’t give legal advice in this blog, but common sense says it’s a bad idea for others to try “going private; funding secured” announcements without a commitment letter in-hand.

Yesterday, the SEC announced an open meeting to be held next Wednesday, February 15th. The Sunshine Act Notice says that the meeting will include consideration of whether to adopt rules & rule amendments under the Securities Exchange Act of 1934 to shorten the standard settlement cycle for most securities transactions.

Presumably, this relates to the Commission’s February 2022 proposal to shorten the settlement cycle to T+1 and make other “market plumbing” changes. The proposed rules and rule amendments would be applicable to broker-dealers and certain clearing agencies.

For those who are still refining their risk factors for this year’s Form 10-K, I’m happy to share this guest post from Orrick’s JT Ho, Carolyn Frantz, Bobby Bee and Hayden Goudy:

For companies with a fiscal year end on December 31, the drafting and review process for the annual report is well underway. Companies, however, should make sure they are considering emerging practices for disclosing environmental-, social-, and governance- (“ESG”) related risk factors.

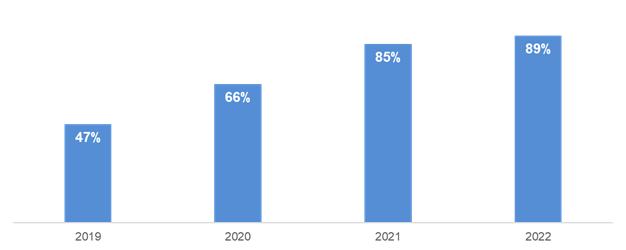

Based on our review of companies in the S&P 500, having ESG-related disclosures in the risk factors is now a common practice. For companies which have already filed their annual report for fiscal year 2022, 89% had ESG-related risk factors. These risk factors spanned a range of ESG-related topics, primarily related to climate change, but also including diversity-, other environmental-, or general ESG-related risks. This graph shows the percentage of the S&P 500 with an ESG-Related Risk Factor in the annual report (by fiscal year):

As you can see, the number of companies with an ESG-related risk factor has increased year-over-year. Less than half of the S&P 500 had an ESG-related risk factor in their annual report for fiscal year 2019. Since then, a significant number of companies have added ESG-related risk factors to their annual report, and we expect this trend to be followed by small- and mid-cap companies.

When it comes to “general” versus “specific” risk factors, the Orrick team of JT Ho, Carolyn Frantz, Bobby Bee and Hayden Goudy share a reminder that “specific” is better.

In addition to the growing number of ESG-related risk factors, we’ve seen an increase in the number of ESG-related risks specific to the reporting company’s business, rather than “general” or “other” risks. The increase in specific ESG-related risk factors is consistent with guidance from 2019 in which the Securities and Exchange Commission (“SEC”) “eschewed ‘boiler plate’ risk factors that are not tailored to the unique circumstances of each registrant.” See below for an example ESG-related risk factor specific to the reporting company’s business compared with an example ‘general’ ESG-related risk.

Example Specific Risk Factor

Costs of Compliance with Environmental Laws are Significant, and the Cost of Compliance with New Environmental Laws, Including Limitations on GHG Emissions Related to Climate Change, Could Adversely Affect Cash Flows and Financial Condition

Our operations are subject to extensive federal, state and local environmental statutes, rules and regulations. Compliance with these legal requirements requires us to incur costs for, among other things, installation and operation of pollution control equipment, emissions monitoring and fees, remediation and permitting at our facilities. These expenditures have been significant in the past and may increase in the future. We may be forced to shut down other facilities or change their operating status, either temporarily or permanently, if we are unable to comply with these or other existing or new environmental requirements, or if the expenditures required to comply with such requirements are unreasonable.

Compare that to a “general” ESG risk factor:

Example General Risk Factor

Catastrophic events may disrupt our business which could have a material adverse effect on our business, financial condition, and results of operations.

Our business, financial condition, results of operations, access to capital markets and borrowing costs may be adversely affected by a major natural disaster or catastrophic event, including civil unrest, geopolitical instability, war, terrorist attack, the effects of climate change, or pandemics or other public health emergencies such as the recent COVID-19 outbreak, and measures taken in response thereto. In the event of a major disaster or event impacting any of our locations, we may be unable to continue our operations and may endure system interruptions, reputational harm, delays in our application development, lengthy interruptions in our services, breaches of data security and loss of critical data, all of which could have a material adverse effect on our business, financial condition, and results of operations.

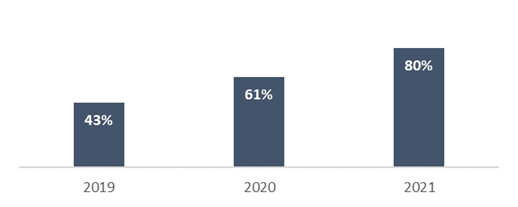

To estimate the increase in the specificity of ESG-related risk factors, we reviewed the headings used to categorize each risk factor in the annual report and assumed that risk factors in the “General” or “Other” category were non-specific, while risk factors that were in other categories (such as “Legal and Regulatory Risks” or “Market and Industry Risks”) were specific to the reporting company’s business. This assumption is not true in every case, but we believe it is a good proxy. Following this methodology, for fiscal year 2019, 43% of the S&P 500 had a specific ESG-related risk factor, which increased to 80% for fiscal year 2021. This chart shows the percentage of the S&P 500 with a specific ESG-Related Risk Factor in the annual report (by fiscal year):

Rounding out the intel on ESG-related risk factors, the Orrick team of JT Ho, Carolyn Frantz, Bobby Bee and Hayden Goudy break down the variety of climate-related risk factors that are appearing in S&P 500 disclosures:

Climate-related risks accounted for most ESG-related risk factors in the S&P 500, with a significant increase in the number of companies reporting climate related risks since 2019. 82% of companies in the S&P 500 reported climate-related risks in fiscal year 2021, compared to just 45% for fiscal year 2019. For the 20% of companies in the S&P 500 which have already filed an annual report for fiscal year 2022, 85% had climate-related risk factors.

Most climate-related risk factors were specific to the reporting company’s business. The most common type of climate-related risks reported for fiscal year 2021 were physical risks related to business operations, with 45% of companies identifying operational risks including potential disruptions in the supply chain due to climate related events and the direct exposure of company assets and operations to more severe hurricanes and wildfires. 15% of the S&P 500 disclosed climate-related legal and regulatory risks for fiscal year 2021. We expect this percentage to increase for fiscal year 2022 given the SEC’s proposed climate-related disclosure rules (the “Proposed Rules”) which are expected to be finalized this year, and the European Union’s Corporate Sustainability Reporting Directive (the “CSRD”), which went into effect this year. Companies should engage with counsel to understand how the Proposed Rules and CSRD may affect their reporting practices and risk-related disclosures.

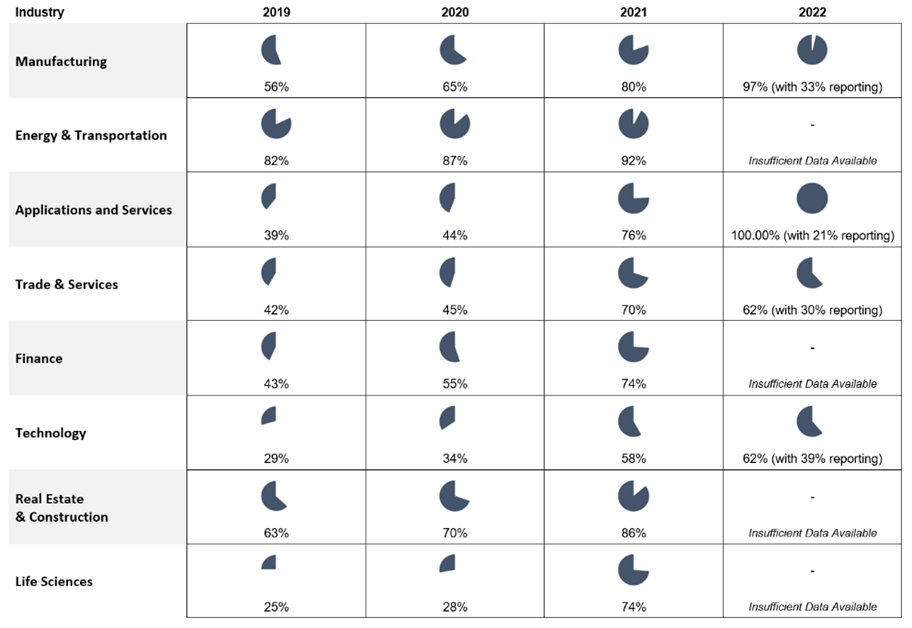

Climate-related risk factors are also becoming more prevalent across industries. For fiscal year 2019, only three industries had more than 50% of their companies report a climate-related risk; energy and transportation (82%), real estate and construction (63%), and manufacturing (56%). By fiscal year 2021, a large majority in every industry across the S&P 500 reported a climate-related risk. Here’s the percentage of the S&P 500 (by industry) with a specific Climate-Related Risk Factor in the annual report (by fiscal year):

Not every company will have ESG- or climate-related risk factors. But regardless of your industry, if you do not have a process in place to identify material company-specific ESG-related risks, especially climate-related risks, there is a potential that your risk management processes and disclosures will fall behind market practices.

On Friday, the SEC announced a $35 million settlement with Activision Blizzard for findings that it failed to maintain disclosure controls related to complaints of workplace misconduct – and separately, that it violated the whistleblower protection rule. The SEC’s 7-page order rests on two main allegations by the SEC. The press release summarizes:

According to the SEC’s order, between 2018 and 2021, Activision Blizzard was aware that its ability to attract, retain, and motivate employees was a particularly important risk in its business, but it lacked controls and procedures among its separate business units to collect and analyze employee complaints of workplace misconduct. As a result, the company’s management lacked sufficient information to understand the volume and substance of employee complaints about workplace misconduct and did not assess whether any material issues existed that would have required public disclosure.

Separately, the SEC’s order finds that, between 2016 and 2021, Activision Blizzard executed separation agreements in the ordinary course of its business that violated a Commission whistleblower protection rule by requiring former employees to provide notice to the company if they received a request for information from the Commission’s staff.

For the disclosure controls aspect of this settlement, the SEC focused on the company’s risk factors and cautionary language in Forms 10-K & 10-Q. The SEC didn’t allege that any particular statement was materially inaccurate or misleading – the problem in the SEC’s view was that shortcomings in how workplace-related information was collected and communicated to the company’s disclosure committee prevented the disclosure decision-makers from evaluating whether disclosure on this topic was needed. SEC Commissioner Hester Peirce dissented from both aspects of the order. Here’s her objection to the alleged “disclosure controls” violation:

In other words, the required disclosure controls and procedures must capture not only information that a company is required to disclose, but also an additional, vaguely defined category—information “relevant” to a company’s determination about whether a risk or other issue reaches the threshold where it is “required to be disclosed.”

She continues:

The requirement cannot be that a company’s disclosure controls and procedures must capture potentially relevant, but ultimately—for purposes of disclosure—unimportant information. As I read it, in this Order, the SEC once again has sat down at the gaming console to play its new favorite game “Corporate Manager.” Using disclosure controls and procedures as its tool, it seeks to nudge companies to manage themselves according to the metrics the SEC finds interesting at the moment. For Activision Blizzard, today, that metric is workplace misconduct statistics, but other issues will follow. In this level of the enforcement game, the SEC has added $35,000,000 to its point total despite the Order not identifying any investor harm.

The settlement comes at a time when the SEC has signaled that it may propose more prescriptive human capital disclosure rules in response to investors wanting more comparable info on that topic. Those rules are not yet in place, but the Enforcement Division already appears to be interested in the principles-based aspects of that topic.

Regardless of whether you find yourself nodding along with Commissioner Peirce, this settlement is another reminder that “workplace misconduct” continues to be a topic that requires board attention, appropriate oversight & information collection, and careful disclosures. The whistleblower component of the action also suggests you should take a fresh look at your separation terms. As this Cooley blog notes, this stuff is no longer just “employment lawyer” territory – you should have a cross-functional team.

Recall that last month, the SEC brought an enforcement action against McDonald’s to allege that the company mischaracterized the nature of the former CEO’s separation from service by not acknowledging that purported workplace misconduct was “cause.” (Commissioners Peirce & Uyeda dissented and said they believed the SEC was rewriting Item 402 disclosure requirements through an enforcement proceeding.) Two weeks later, the Delaware Court of Chancery allowed a fiduciary duty claim to proceed against McDonald’s HR head, finding at the motion to dismiss stage that if all the facts alleged by the plaintiff were true, the officer consciously ignored red flags and didn’t put in place reasonable information systems to report to the CEO & board. And while Activision settled an EEOC claim last year for a lower amount than this SEC matter, that company continues to face litigation in state court.