Yesterday, as noted in this press release, the SEC adopted two interim final rules as mandated by the FAST Act that revise Forms S-1 and F-1 for emerging growth companies to provide that as long as their registration statements include all required financial information at the time of the offering, the ECGs can omit certain historical period financial information prior to the offering.

The interim final rules also revise Form S-1 to allow smaller reporting companies to use incorporation by reference for future filings – along with a request for comment on whether the rules should be expanded to include other registrants or forms.

These interim final rules will become effective as soon as they are published in the Federal Register – so within the next week – and folks can comment for 30 days if they want to push the SEC to change these interim final rules before they become “final final”…

ESG: Coming Up on Earnings Calls

This blog by Pam Styles illustrates how sustainability has become a more frequent topic on quarterly earnings calls…

Spanking brand new. By popular demand, this comprehensive “Audit Response Letters Handbook” covers all you need to know about dealing with audit response letters (it’s now posted on our “Audit Response Letters” Practice Area). This one is a real gem – 48 pages of practical guidance.

Webcast: “Audit Committees in Action – The Latest Developments”

Tune in tomorrow for the webcast – “Audit Committees in Action: The Latest Developments” – to hear Morgan Lewis’ Rani Doyle, Deloitte’s Consuelo Hitchcock and Gibson Dunn’s Mike Scanlon catch us up on a host of new SEC, FASB & PCAOB developments that impact how audit committees operate – and more…

Cap’n Cashbags: The Call from the IRS

In this 40-second video, Cap’n Cashbags gets a surprising call from the IRS:

For those that can remember, as noted in this Davis Polk blog, it was the NYC Comptroller’s office who really took the proxy access movement to the next level last year. Now, the Comptroller has issued a new list of 72 companies that have received proxy access shareholder proposals – 36 of them repeats from last year’s list of the 75 that received shareholder proposals…

Webcast: “The Latest Developments – Your Upcoming Proxy Disclosures”

Tune in tomorrow for the CompensationStandards.com webcast – “The Latest Developments: Your Upcoming Proxy Disclosures” – to hear Mark Borges of Compensia, Alan Dye of Hogan Lovells and Section16.net, Dave Lynn of CompensationStandards.com and Morrison & Foerster and Ron Mueller of Gibson Dunn discuss all the latest guidance about how to overhaul your upcoming disclosures in response to say-on-pay-including the latest SEC positions-and the other compensation components of Dodd-Frank, as well as how to handle the most difficult ongoing issues that many of us face.

Sqoop: How Journalists Might Be Viewing Your SEC Filings

I have no idea if this new service aimed at journalists is taking off – most new services don’t – but I found it interesting. It’s called “Sqoop” (but I have no idea how that is pronounced) – and here’s their description of how it works:

Simply execute a search for a company, executive or interest, and Sqoop will deliver search results that click through to detail pages that are far more useful that those from Edgar. For the Form 4, Sqoop translates the codes and does the math so you don’t need to. On all other forms, we provide filing along with any exhibits in expandable view, all within one page. Not only does this help you more quickly assess the news value, but it’s also a better reader experience than linking to dumb Edgar pages where exhibits are inaccessible.

I have no idea why Sqoop is targeting journalists specifically with this service. It seems like it could be useful to others who consume SEC filings. And of course, for those that draft SEC filings, it’s good to keep track of how your end-product may be consumed…

In this podcast, Jim Patterson discusses the life of his former wife, Evelyn Y. Davis, including:

– Can you tell us about Evelyn’s childhood? For example, how did Evelyn’s childhood arrest with her mother and brother by the Nazis in Amsterdam in the final months of WWII affect her life?

– How did you meet Evelyn?

– Can you tell us a story to illustrate how Evelyn felt about her activism work?

– Can you tell us a story about how Evelyn liked to stir it up sometimes at annual shareholder meetings?

– What was her “contribution” to financial reporting/journalism?

– I know Evelyn was active with charitable efforts. Can you tell us about that?

Evelyn Davis: Your Stories

I’m starting to collect anecdotes about Evelyn – please send me your stories (as always, I won’t share them with attribution unless you give me permission). Here’s the first batch:

– You are aware of her prostitution arrest at the United Nations (sexpionage is what the press called it) and her “business services” at a Lexington Avenue hotel in New York. Brief accounts in editions of New York Post and New York Daily News. This one comes from Jim Patterson.

– Bob Lamm of Gunster notes: When my father was 94 last year and found out that Evelyn was still around and kicking, he was shocked – “that woman was old when I was young!” He was CFO of a company 40 or so years ago and had to deal with her. Mostly, he had to stop her from attacking his outside lawyer, who was a very good looking guy.

– I remember her and Donald Trump going at it at the Alexander’s meeting many moons ago.

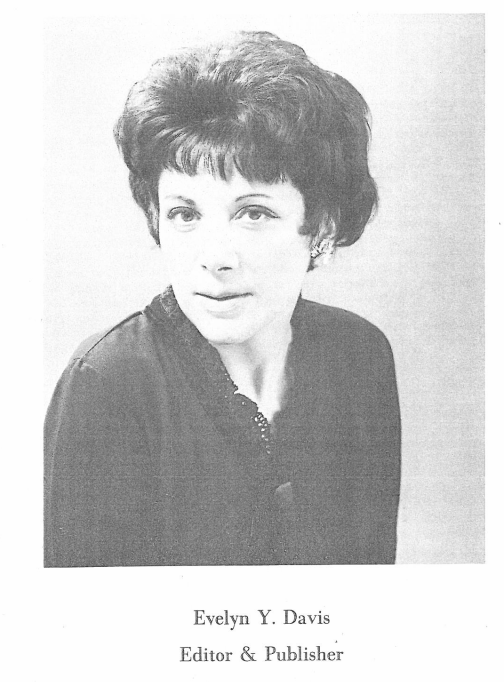

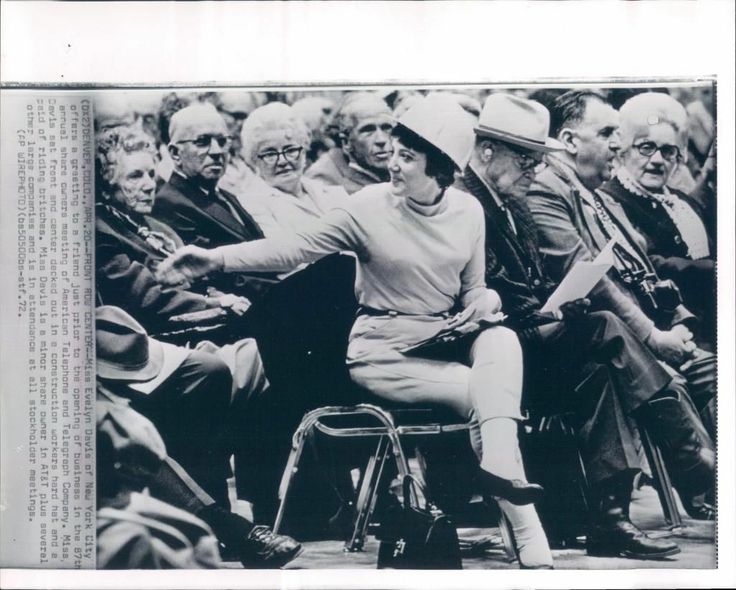

Evelyn Y. Davis: The Pictures

Please send me your pictures of EYD too! From Jim Patterson, here’s a pic of Evelyn from her 1st issue of “Highlights & Lowlights”:

Here’s EYD at a 1972 AT&T annual shareholders meeting:

As noted in our “Annual Report & 10-K Wrap Handbook,” glossy annual reports are one of the few documents that companies furnish to the SEC in paper rather than being filed electronically in Edgar. Companies are permitted to furnish them electronically – but most choose to mail them in because it’s hard to format them so that Edgar accepts them.

For some time now, Corp Fin has been scanning in the paper copies of glossy annual reports and posting them on Edgar. However, as noted in Edgar Filer Support newsletter, Corp Fin recently decided to forego this practice “in an effort to reduce costs and simplify administrative processes, and in light of the availability of these annual reports on other web sites.”

The Edgar Filer Support newsletter notes that a Registration Fee Estimator – a tool designed to assist filers in estimating required fees for EDGAR filing submissions – should be available within the next 6 months…

Director Removal: Delaware Rules on ‘Without Cause’

Here’s a memo by Wachtell Lipton’s William Savitt:

The Delaware Court of Chancery recently held that a corporation without a classified board or cumulative voting may not restrict stockholders’ ability to remove directors without cause. In re Vaalco Energy S’holder Litig., C.A. No. 11775-VCL (Dec. 21, 2015). The ruling gives rise to questions for the many companies with similar charter or bylaw provisions.

In 2009, Vaalco’s stockholders approved an amendment to the company’s certificate of incorporation to declassify the board, but the amendment left intact clauses in the bylaws and charter providing that directors could be removed only for cause. When an activist investor launched a consent solicitation to remove four members of the board in late 2015, Vaalco responded that any such written consent would be “null and void” because its directors could “only be removed from office for cause.” Stockholder plaintiffs sued, arguing that under § 141(k) of the Delaware General Corporation Law, stockholders have the right to remove directors without cause unless the company has a staggered board or cumulative voting.

In a transcript ruling, the Court of Chancery agreed and invalidated the terms of Vaalco’s charter and bylaws providing that directors may be removed only for cause. Shortly thereafter, Vaalco reached a resolution with the activist investor.

The practical significance of the ruling for the scores of other companies with unclassified boards whose charters allow director removal only “for cause” remains to be determined. Even if the Delaware Supreme Court confirms the Vaalco rule — and the Supreme Court has not had the opportunity to pass on the issue — a without-cause removal right may be of limited importance, especially for companies whose charter and bylaws do not provide low thresholds for stockholder-called special meetings. More fundamentally, a board vulnerable to a without-cause removal campaign is likely equally vulnerable to a proxy fight at an ensuing annual meeting. In many cases, therefore, the Vaalco rule is unlikely to have real-world impact in a contested election scenario.

But stockholder plaintiffs may seek to capitalize on the ruling nonetheless, by bringing suit or demanding that boards comply with the Vaalco rule and then claiming a fee if a conforming change is made. Confronted with such a claim, companies will have the option to settle or litigate the matter in the Court of Chancery and the Supreme Court. Given the tactical complexity of these governance and litigation choices, companies affected by the Vaalco ruling should consider carefully whether a response is in order.

Director Exposure: Personal Liability for Whistleblower Actions?

It will not come as news to anyone that corporate directors face the possibility of direct personal liability for their actions or omissions in the capacities as directors. However, the scope of these individuals’ potential liability exposures can and does change. As a result of recent legal developments, at least two new areas of potential liability exposure for corporate directors have emerged. As discussed below, a recent federal district court decision suggests that directors can be held personally liable under both the Sarbanes-Oxley Act and the Dodd-Frank Act for whistleblower retaliation, and a recent California legislative enactment provides that corporate directors can be held personally liable for violations of the state’s wage and hour laws.

A lot of responses to my blog yesterday about the newly posted model annotated D&O questionnaire. Goodwin Procter’s John Newell gave me a nice add for the “D&O Questionnaire Handbook” and my section on page 24 about “Whether to Obtain Competition-Related Information.” In that section, I noted that it’s possible that some companies include a question about the Clayton Act depending on their questionnaire philosophy – but that we hadn’t seen one. John sent me one:

Do you, or have you at any time on or after the beginning of the company’s most recent completed fiscal year, served as either a director or an officer of any business other than the Company, including non-public businesses, that had (a) total liabilities and stockholders equity (i.e., net worth as shown on its balance sheet) in excess of $29,945,000 as of the end of that business’s most recently completed fiscal year and (b) revenues of $2,994,500 or more attributable to business operations that could be viewed as competing with the Company because of the nature of the other business’s business operations and the geographical markets in which the other business operates? If so, please provide the name of the business in the space below.

And John notes that the trick is that the FTC updates the dollar thresholds annually – but not until the second or third week of January, so anyone who uses this question before that date gets the prior year’s dollar amount.

And then another member sent me this example that doesn’t need to be updated every year:

Do any of the companies for which you serve as an officer or director (whether publicly-traded or privately-held) compete, directly or indirectly, with any of the company’s businesses?

YES NO

If YES, please identify below the company and provide an estimate of its total annual sales for its last completed fiscal year and an estimate of its annual sales which are competitive with the company.

As noted in this blog by Duane Morris’ David Feldman, the OTCQX has increased their listing and governance requirements effective January 1st. The QX is the highest tier of trading among the OTC options. There will now be a higher initial bid price of $0.25 to trade on the OTCQX U.S. tier. US companies on the QX will have to keep a price above $0.10. International companies will be required to meet new initial and ongoing minimum bid prices of $0.25 and $0.10 to trade on the OTCQX International tier. Both US and international companies will have higher initial and ongoing market capitalizations of $10 million and $5 million, respectively. All companies now will be required to have at least two market makers.

In addition, there are new minimum corporate governance requirements for American companies on the QX. These are: a minimum of two independent directors on the board of directors; an audit committee composed of a majority of independent directors; and they must conduct annual shareholders’ meetings and submit annual financial reports to shareholders at least 15 calendar days prior to such meetings. They also added even more stringent new requirements for the higher level “premier” tier on the QX.

Political Contributions: “Forcing the SEC to Adopt Rules” Case Dismissed

Here’s an excerpt from this blog by Steve Quinlivan:

The United States District Court for the District of Columbia has dismissed a two-count complaint asking the Court to mandate the SEC be required to adopt rules regarding disclosure of political contributions. The plaintiff had submitted a request for rulemaking to the SEC, and the SEC never took action on the request.

FASB Issues “Financial Instruments Recognition & Measurement” Standard

Here’s an excerpt from this blog by “Accounting Today”:

The Financial Accounting Standards Board issued Tuesday a long-awaited accounting standards update (2016-01) for the recognition and measurement of financial instruments that it has been developing for over a decade with the International Accounting Standards Board.

The standard affects public and private companies, not-for-profit organizations, and employee benefit plans that hold financial assets or owe financial liabilities. FASB also plans to issue this year a separate standard on the impairment of financial instruments that will differ markedly from the IASB’s. The IASB issued its own financial instruments standard, IFRS 9, in 2014. The “recognition and measurement” standard was formerly referred to as “classification and measurement” but was changed to better reflect what FASB was trying to address.

Here’s something from the “DealLawyers.com Blog” that I recently posted: Occasionally, you hear that people have received advice to be especially careful about emails so “don’t put it in an email, give him/her a call.” Often the advice is couched in terms of “avoid putting anything in an email that you would be embarrassed to read about on the front page of the Wall Street Journal. Make a call instead.” That advice is insufficient given what often happens in litigation. According to a recent WSJ article regarding pending M&A litigation, it’s alleged that: “[employee of buyer] later testified that [employee of target’s financial advisor] called him and said “we should not email on this.”

And then consider this quote from a recent Delaware Chancery Court opinion:

“On the evening of March 24, [employee of buyer] summarized the situation in an email [to other employees of the buyer]: I have spoken to a number of bankers on our side (for advice) and theirs (for back-channel feedback). There are definitely two other offers as we suspected, both say they need another week of work but the company’s bankers think it is more like 2-3 weeks. Sounds like both are higher but again not a knock-out, I haven’t been able to get more specific info than that.”

Things to bear in mind include:

1. Any advice, if given by one transaction participant to another participant or their representatives, is discoverable. Even if you don’t disclose it, the other person may – and you should assume likely will.

2. While not necessarily wrongful, there can be lots of innocent and/or perfectly valid reasons for making the suggestion to talk rather than exchange email (e.g., to avoid ambiguity or misinterpretation or because time is of the essence) – plaintiffs will likely allege that the person making the suggestion was trying to hide something damaging.

3. Just because you speak with someone and don’t put it in an email doesn’t ensure that the substance of the conversation will not be memorialized in writing – and be discoverable. Even if you don’t put it in an email, the person you talk to may.

The bottom line is: while it is not always possible to avoid saying, doing or writing things that are potentially vague, ambiguous or subject to misinterpretation, and sometimes back-channel communications are authorized for purposes of seeking a bump in price from the buyer, you should not assume that it’s okay to say something so long as you don’t put it in an email. The better advice is to try to “avoid saying, doing or putting anything in an email that you would be embarrassed to read about on the front page of the Wall Street Journal.”

Related-Party Transactions: SEC Approves NYSE’s Exemptions from Shareholder Approval

Cooley’s Cydney Posner’s blog provides the long history behind the SEC’s approval of the NYSE proposal to exempt certain related-party transactions from shareholder approval requirements – despite concerns of the SEC’s Investor Advocate…

SEC Commissioner Aguilar Bids Farewell

On the heels of SEC Commissioner Gallagher issuing a brief farewell statement, Commissioner Aguilar has now issued a lengthy one too. I don’t recall Commissioners doing this in the past. In his statement, Aguilar summarizes the changes in the SEC & in the law during his tenure, lists his accomplishments and notes some “unfinished business.” And this is on top of his recent list of tips for incoming Commissioners.

Can you think back and wonder what you would write for every job you left…

I’m sad to note that former Rep. Mike Oxley passed away on New Year’s Day. As noted in this article, Congressman Oxley served 25 years in the House, representing Ohio, serving as Chair of the Financial Services Committee for the max term of six years and was co-author of the Sarbanes-Oxley of 2002. I had the fortune of interviewing Mike at our conference in 2012, the 10th anniversary of Sarbanes-Oxley. He was insightful, engaging and witty. And Mike was quite the athlete – particularly golf where he could boast that he had six “hole-in-ones” during his lifetime. Six! Condolences to his family & friends, including his colleagues at BakerHostetler.

Our January Eminders is Posted!

We have posted the January issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!