This morning, it’s my pleasure to welcome Meredith Ervine as the newest member of our editorial team! Meredith has had a distinguished career in private practice, and her securities and corporate transactional expertise make her a great addition to our crew. She also has the kind of friendly and down-to-earth personality and sense of humor that makes it a cinch that you’re going to really enjoy getting to know her.

Meredith also brings an important intangible to the table. As she points out in the next blog, her presence also will help us diversify the mix of bad dad jokes & boomer pop culture references that have been the stock-in-trade of the more geriatric members of the editorial team (yeah Dave, I’m talking about you & me) by adding a more millennial twist. This will undoubtedly appeal to our younger readers and will also reduce the number of times that Liz rolls her eyes when reading our blogs.

If you’re a frequent visitor to our Q&A Forum, you may have already noticed that Meredith has hit the ground running. Meredith will be blogging later this week on the Proxy Season Blog, and you’ll also see her work on the DealLawyers.com Blog next week. Once she settles in, you can look forward to seeing her as part of the blogging rotation here as well. To give you a taste of what you have to look forward too, I’m turning the next blog over to Meredith so that she can introduce herself to everyone.

Following Liz’s announcement in early December, I’m sure a few of you have wondered whether we’d be adding to our editorial ranks. As of this month, our small but mighty team has officially grown by one, and no one is more excited about it than I am!

I’d like to take a minute to introduce myself since you’ll be hearing more from me soon. I’ve spent the last 14 years as a corporate securities attorney in private practice, having joined the law firm world in fall 2008 (not the easiest of times).

Since you all seem to share my love of lists, I thought I would introduce myself, and my passion for our sites, with my top three reasons for joining CCR Corp.

1. John, Liz, David and Alan. I appreciate that there are personalities behind our sites. If you also use our sites daily, I’m sure you share my deep appreciation for the time they spend keeping our members in the know.

2. Sharing my experience. I love that our sites go beyond substance to share practical skills for all career levels from new associates, to new in house counsel to the path to GC. I hope to make your job easier and help you look great in front of your clients and your CEO and Board!

3. Connecting with all of you. We’re more than a resource; we’re a community. I look forward to interacting with our members at our annual Proxy Disclosure & Executive Compensation Conference (a not-to-be-missed event!) and on our Q&A forums and learning from you too. Thank you for all you do!

You can also read my bio on our About Us page. I feel compelled to alert you that my presence here may increase our tally of exclamation points and millennial pop culture references. You’ve been warned!

Please feel free to drop me a line anytime at mervine@ccrcorp.

We’ve posted the transcript for our recent webcast – “The Latest: Your Upcoming Proxy Disclosures” – in which Mark Borges of Compensia and CompensationStandards.com, Alan Dye of Hogan Lovells and Section16.net, Dave Lynn of Morrison Foerster and TheCorporateCounsel.net, and Ron Mueller of Gibson Dunn covered the waterfront of issues to consider as you prepare your upcoming proxy disclosures – with lots of attention to pay vs. performance. Check out the transcript for info on:

1. Pay vs. Performance Disclosures

2. Meeting Format

3. Clawbacks

4. Say-on-Pay Trends

5. Showing “Responsiveness” to Low Say-on-Pay Votes

6. CD&A Updates

7. CEO Pay Ratio Considerations

8. Perquisites Disclosure

9. Shareholder Proposals

10. ESG Metrics & Disclosures

11. Proxy Advisor & Investor Policy Updates

12. Status of Other Pay-Related & Human Capital Management Rulemaking

Speaking of proxy disclosure, Corp Fin issued a boatload of Pay v. Performance CDIs on Friday. Be sure to check out Liz’s blog on CompensationStandards.com for the details.

The SEC Enforcement Division’s “EPS Initiative” appears to be alive & well – by the looks of an “cease & desist” order from earlier this week – which resulted in a $4 million settlement (and a $75k penalty against the person who served as Chief Accounting Officer – and later, Chief Financial Officer – of the company in question). The claims were settled on a “neither admit nor deny” basis.

In the SEC’s telling, the internal controls & supporting documents for the bonus accruals left gaping holes that allowed for manipulation. Here’s an excerpt from the SEC’s order:

15. On October 7, 2015, during the closing process for the third quarter of 2015, Nash directed the accrual of $300,000 for the PB Bonus Plan, which had not yet been approved by Gentex’s Board of Directors. This journal entry was made without any supporting documentation. Additionally, Nash did not maintain documentation of any purported analysis that was required to be performed pursuant to Accounting Standards Codification (“ASC”) Topic 450, Contingencies, concerning the loss contingency associated with the PB Bonus Plan.

16. On October 8, 2015, Nash realized that the initial accrual of $300,000 would cause Gentex to miss the consensus EPS estimate of $0.27 for the third quarter of 2015. He directed a journal entry to reduce the $300,000 accrual to $100,000. The journal entry for the revised accrual was again made without any supporting documentation and Nash did not conduct any analysis that should have been performed pursuant to ASC 450-20 concerning the PB Bonus Plan.

17. In an October 9, 2015 email exchange with the CFO, the CFO asked Nash if he had reserved some money for the PB Bonus Plan. Nash responded, “100K. had [sic] 300K, but had to reduce in order to keep .27 per share.” The CFO replied, “[g]ood call. That puts in line with consensus, right?” to which Nash replied, “[y]es.”

There were other internal controls sins here too, according to the SEC – but I was surprised that this $200k accrual adjustment appears to be so central to the case. That doesn’t seem like a lot in the grand scheme of things, but the company would have missed consensus EPS estimates by one penny if the adjustment hadn’t been made – and the SEC’s data analytics tools were sensitive enough to pick up something fishy with the situation.

One moral of this story is that if the SEC comes knocking, you want to make sure to have documentation of your internal controls & accounting analysis instead of a conversation about managing EPS to the consensus number.

Here’s something I blogged yesterday for members of CompensationStandards.com:

A few pay versus performance disclosures are starting to roll in! This is something that we’ve all been eagerly awaiting – and I send my condolences to those who have had to be brave and take the first leap. These are from smaller companies – we continue to await a large-cap example. Thanks to Aon’s Corporate Governance & ESG Advisory Group for alerting us!

– Praxis Precision Medicines Form 10-K (pg. 136) – It is unclear to me why the company included this disclosure in a Form 10-K – as this Goodwin FAQ points out, the SEC rules only require pay vs. performance disclosure in proxy & information statements; it isn’t required in Form 10-K even when other Item 402 disclosure is included. But I didn’t read this filing or the company’s filing history in-depth to understand whether there is a reason they might have wanted to go ahead with it here.

– Panbela Therapeutics Form S-1/A (pg. 72) – Seems to have missed some of the disclosure requirements, but has the distinction of being the first to report under the new rule.

If you aren’t already a member of CompensationStandards.com, now is a good time to sign up. That’s where we are sharing the latest updates & analysis on the new pay vs. performance rules, along with updates on say-on-pay, ESG metrics, and other “executive compensation” hot topics. Email sales@ccrcorp.com or visit our membership center to start a no-risk trial. Our “100-Day Promise” guarantees that during the first 100 days as an activated member, you may cancel for any reason and receive a full refund. If you have any questions, email sales@ccrcorp.com – or call us at 800.737.1271.

I blogged earlier this week on CompensationStandards.com and on this site about whether to include the two new “clawbacks”-related checkboxes on your Form 10-K cover page this year. The Dodd-Frank clawback rules are not yet effective – but the checkboxes are included on the cover page of the updated Form that the SEC has published. There was lingering confusion after Corp Fin’s CDI a couple of weeks ago.

I’ve now heard from a few folks that the Staff has confirmed in informal conversations that you should include the checkboxes (but don’t need to mark them). If you are concerned that a blank checkbox could be misleading, you could add an explanatory note to the effect that the checkboxes are blank pending adoption of the underlying rules.

When it comes to finding unconventional ways to raise cash, AMC will find a way – and selling equity to do it is a key part of the meme stock playbook, as another retailer’s offering this week showed. Two years ago, the company abandoned a proposal to increase its authorized number of common shares because its retail investors weren’t showing up to deliver the votes needed for approval of the charter amendment. That temporarily shut off the spigot of raising capital through stock sales.

Undeterred, last summer AMC used its blank check preferred provision to issue a new class of shares: APEs (that stands for “AMC Preferred Equity,” of course). Here’s the Form 8-K they filed at the time. Each APE unit has terms identical to 1/100th of a share of common stock – including voting rights – and will automatically convert to common stock if & when AMC is able to issue enough common shares to cover the conversion of all of the APEs.

Now, with the APEs unfortunately trading at a 65% discount to the equivalent common shares as of year-end, AMC is going back to its common shareholders to once again seek approval for a higher number of authorized common shares, which would trigger the preferred stock conversion, as well as to effect a 1-for-10 reverse stock split for the existing common shares. The interesting part is that with this go-round, it will include votes from the APE holders – and AMC baked in a key provision to make approval more likely. In a column last week, Bloomberg’s Matt Levine pointed out that AMC’s deposit agreement for the APEs includes this language:

In the absence of specific instructions from Holders of Receipts, the Depositary will vote the Preferred Stock represented by the AMC Preferred Equity Units evidenced by the Receipts of such Holders proportionately with votes cast pursuant to instructions received from the other Holders.

Proportionate voting! This is a bold move as at least one major brokerage firm has moved away from proportionate voting for common stock and asset managers are pushing pass-through voting despite the generally low voter turnout from retail investors. It’s too soon to know whether pass-through voting will do more harm than good to individual shareholders – the early consensus is that it will just make solicitations more complicated & costly for companies, and give proxy advisors more influence. For this specific charter amendment – and with the preferred stock in the mix – AMC has possibly found a way to bring in a vote despite these hurdles.

Last week, a jury in a securities class action lawsuit found in favor of Elon Musk for his 2018 “funding secured” tweet – in which he said he was considering taking Twitter private at $420 per share and had locked in the funding. Here’s a NYT article about the outcome. The SEC had also taken issue with those tweets, resulting in a $40 million settlement and the “Twitter sitter” – plus a lot of animosity from Elon towards the Commission.

All I can say is that I’m nearly as happy as Elon that we can finally put this saga to bed. There’s no real takeaway for other companies because the jury’s verdict appeared to rest on the determination that nobody takes Elon Musk’s tweets all that seriously – and at the same time, they trust him to get things done when he really wants to.

So, investors truly may not have cared if instead of “funding secured,” the tweet had said “I might have a handshake deal for funding” – because it’s Elon Musk and he’ll either bring in the money when he wants to, or the whole thing was a joke in the first place. Did the statement really cause people to buy Tesla stock at an inflated price? The jury apparently was not convinced of that.

The reason this doesn’t translate well to other companies is that Elon Musk has carefully (or not-so-carefully?) cultivated a free-wheeling, Teflon persona and a cult-like following. It would be difficult & risky for other public company CEOs to emulate that. We don’t give legal advice in this blog, but common sense says it’s a bad idea for others to try “going private; funding secured” announcements without a commitment letter in-hand.

Yesterday, the SEC announced an open meeting to be held next Wednesday, February 15th. The Sunshine Act Notice says that the meeting will include consideration of whether to adopt rules & rule amendments under the Securities Exchange Act of 1934 to shorten the standard settlement cycle for most securities transactions.

Presumably, this relates to the Commission’s February 2022 proposal to shorten the settlement cycle to T+1 and make other “market plumbing” changes. The proposed rules and rule amendments would be applicable to broker-dealers and certain clearing agencies.

For those who are still refining their risk factors for this year’s Form 10-K, I’m happy to share this guest post from Orrick’s JT Ho, Carolyn Frantz, Bobby Bee and Hayden Goudy:

For companies with a fiscal year end on December 31, the drafting and review process for the annual report is well underway. Companies, however, should make sure they are considering emerging practices for disclosing environmental-, social-, and governance- (“ESG”) related risk factors.

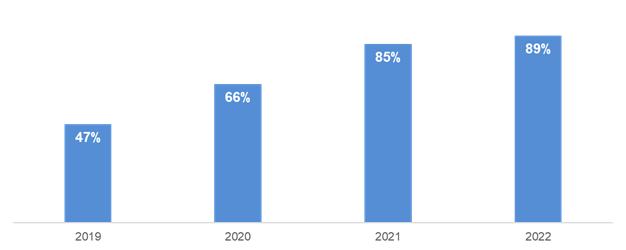

Based on our review of companies in the S&P 500, having ESG-related disclosures in the risk factors is now a common practice. For companies which have already filed their annual report for fiscal year 2022, 89% had ESG-related risk factors. These risk factors spanned a range of ESG-related topics, primarily related to climate change, but also including diversity-, other environmental-, or general ESG-related risks. This graph shows the percentage of the S&P 500 with an ESG-Related Risk Factor in the annual report (by fiscal year):

As you can see, the number of companies with an ESG-related risk factor has increased year-over-year. Less than half of the S&P 500 had an ESG-related risk factor in their annual report for fiscal year 2019. Since then, a significant number of companies have added ESG-related risk factors to their annual report, and we expect this trend to be followed by small- and mid-cap companies.