This “Audit Analytics” blog discusses an intriguing new study that suggests the SEC’s decision to make Corp Fin comment letters publicly available may have resulted in improved disclosure by companies on the receiving end of those letters. Here’s an excerpt:

It was found that when comment letters are made public, company filings include longer narratives, have a lower chance of restatements, and there were less discretionary accruals in earnings announcements. Those factors provide a more complete picture of the company’s position, benefitting the company, the SEC, and investors or firms who are concerned with company performance.

Well, wadda ya know? They’re from the government, and they actually did help you. . .

GDPR Enforcement: More on “How Will It Work for US Companies?”

Europe’s GDPR has had an enormous impact on companies that do business in the EU, but as we blogged earlier this year, there’s a lot of uncertainty about potential consequences for non-compliance by US companies that don’t have a major European presence. This Dorsey & Whitney memo reviews the recent experience of an enforcement proceeding involving a Canadian company, and this excerpt speculates on how US authorities might deal with a similar situation:

It remains unclear how GDPR enforcement would play out in the United States. The U.S. currently has no federal law similar to the GDPR. The Trump administration is discussing a U.S. version of the GDPR that would have provisions similar to provisions in the GDPR, but the passage of such a law is not imminent.

To the extent the U.S. enacts such a law, the U.S. might be incentivized to assist with GDPR investigations or enforcement against U.S. entities at least to the extent consistent with the terms of the U.S. law for purposes of encouraging reciprocal comity with the EU. However, given the Trump administration’s foreign policy stance, it is highly unlikely that the U.S. would assist in enforcing violations of any GDPR provisions that go beyond the U.S. law.

If the feds won’t play ball with the EU, there’s another possibility – state regulators. The memo notes that California recently enacted the California Consumer Privacy Act of 2018, which is similar in some respects to the GDPR – and says that it remains to be seen whether the state would assist EU regulators in a GDPR investigation “to encourage reciprocal comity with the EU in connection with enforcement of their respective data privacy laws.”

D&O Insurance: The Outlook

It’s renewal season for a lot of D&O policies – and this Woodruff Sawyer deck reviews market conditions, claims trends and coverage issues. Here’s an excerpt on pricing expectations for the primary layer of coverage:

As we head into 2019 it is increasingly rare that a company will see a year-over-year decrease in the premium paid for the primary layer. Instead, single-digit increases in premium on the primary layer are more and more common (with larger rate increases for companies with less favorable risk profiles). Companies with SIRs below those of their peers face the prospect of larger retentions, though sometimes in exchange for a flat-to-smaller premium increase.

While the market for the primary layer continues to tighten, the market for excess layers – including Side A – remains highly competitive. That competition has generally held premium increases in check, although even these markets are beginning to experience pricing pressure.

This “IR Magazine” article says that a recent study suggests that critics of the forward-looking statements safe harbor may have a point when they say it gives companies a “license to lie.” Here’s the intro:

When forward-looking statements are accompanied by a legal disclaimer, inexperienced investors are more likely to forgive a company missing its projections – even when management is shown to have knowingly misled investors, according to a new academic study published recently in “The Accounting Review.” The research was led by H Scott Asay of the University of Iowa and Jeffrey Hales of the Georgia Institute of Technology. They contend that legal disclaimers protect public companies from reprisal and therefore harm vulnerable investors in the process – going so far as to cite one attorney’s description that these disclaimers afford management the ‘license to lie’.

The study broke investors into four groups, all of whom were given the same company release to review. They were told that the company missed its earnings projections. The first two groups were told that management acted in good faith. One group’s press release contained a legal disclaimer, while the other group’s did not. Both of the first two groups were less inclined to seek compensation for the missed projections, and the legal disclaimer had no effect on their views.

The second two groups were provided with the same information, except that they were told management knew that it couldn’t hit its projections. Those investors in the group whose press release included a disclaimer were less inclined to seek compensation than those whose press release did not include a disclaimer. The study’s authors contend that this means disclaimers are likely to dissuade investors from pursuing claims – even if they know they’ve been lied to.

China Tech IPOs Raise the CEO “Pig-Out” Bar

A tip of the hat to China’s tech sector – this BusinessWeek article says those companies have no shame when it comes to compensating CEOs for their work in taking a company public:

It’s a good time for founders in China to take their startups public, at least by one measure.

Chief executive officers are beginning to get ten-figure bonuses with their initial public offerings. In the latest example, the CEO of Shanghai-based Pinduoduo, received at least $1 billion of stock without any performance hurdles as his e-commerce company prepares for a U.S. IPO. Lei Jun, the head of Beijing-based smartphone maker Xiaomi Corp. saw a $1.5 billion payday, with no strings attached, when his company went public in July. When JD.com went public in 2014 it incurred $591 million of costs from a stock grant to its chief.

Well, Marx never said that the “Vanguard of the Proletariat” had to serve the revolution for free. Does anybody know if there’s a Mandarin word for chutzpah?

Tomorrow’s Webcast: “GDPR’s Impact on M&A”

Tune in tomorrow for the DealLawyers.com webcast – “GDPR’s Impact on M&A” – to hear Davis Polk’s Avi Gesser and Daniel Foerster discuss the implications of the EU’s General Data Protection Regulation for M&A transactions. Please print out these “Course Materials” in advance…

According to the latest Spencer Stuart Board Index, financial types & techies top the “Most Wanted List” when it comes to skills desired in new directors on S&P 500 boards. Here some of the highlights when it comes to new director demographics:

– Only 36% of the new S&P 500 directors are active or retired CEOs,board chairs or vice chairs, presidents or COOs. That’s down from 47% a decade ago.

– Board experience is also no longer a prerequisite. One-third of the incoming class are serving on their first public company board.

– Directors with financial backgrounds are a priority, representing 25.5% of the new S&P 500 directors in 2018, up from 18% in 2008.

– 40% of the members of the incoming director class are female, 10% are minority males, and 17% are under 50.

– Of the directors under 50, one-third have tech or telecommunications backgrounds.

The index covers a lot of ground, and includes information about board size ranges, director tenure, board governance practices, director compensation and 1, 5 & 10-year trends in board composition.

Spencer Stuart says that the S&P 500 appointed appointed 428 new independent directors in the 2018 proxy year. Although that’s up 8% over the prior year, overall turnover is low, with new directors representing just 8% of all board seats.

While 50% of those new seats went to women or minority men, this WSJ article notes that the low turnover rate slows efforts to promote diversity. It also provides some insight into one reason why turnover may be so low:

“Boards are a little more static than they should be in a world that’s so dynamic,” said Julie Daum, head of Spencer Stuart’s North American board practice. That means there are few opportunities for women and people of color to join boards.

One reason for the low turnover: Directors have been voting to raise their own mandatory retirement ages. Of the S&P 500 companies that have such policies, around 44% set the age at 75 or older, compared with 11% in 2008. Of all S&P 500 companies, 71% disclose a mandatory retirement age.

The article says that the shift to later retirement ages emerged during the financial crisis, when companies were seeking to maximize stability by retaining experienced directors.

Shareholder Engagement: “Top of Mind” Issues for Investors

Interest in off-season engagement with investors is reportedly very high this year. If your company is one of those preparing for a round of shareholder engagement, you should check out D.F. King’s 20-page “Fall Engagement Guide,” which provides a brief overview of the issues that are currently “top of mind” among institutional investors. It’s the perfect type of document to slide across the boardroom table to your CEO or CFO – and to share with your directors.

The U.S. Chamber of Commerce recently published this report warning that the US securities class action system is yet again in dire need of reform. The report notes that while M&A litigation has long been the domain of state courts, 87% of M&A lawsuits last year were federal securities class actions. It also highlights another burgeoning category of claims – the “everything is a securities claim” class action. Here’s an excerpt:

A second variety of securities class actions has also emerged that seeks to capitalize on adverse events in a company’s underlying business, such as a product liability lawsuit, data breach, or similar high-profile, unexpected negative occurrence. The securities class action lawsuit does not seek damages for harm from the underlying event, which is addressed through other lawsuits. Rather, the securities claim asserts that the company defrauded investors by intentionally or recklessly failing to warn that the adverse event might occur, even though these events are—by definition—unexpected.

There’s no doubt that a lot of these claims are meritless, and the Chamber wants Congress to enact legislation to deter them. But recent events suggest that potential defendants should be careful what they wish for, because reforms may be accompanied by unintended consequences. For instance, an emerging trend among major investors to “opt out” of securities class actions – a trend the Chamber’s advocacy inadvertently helped to create – may represent an even bigger problem for defendants.

Alison Frankel highlighted this emerging problem in a recent blog about a $217 million settlement that Verit reached with some heavy-hitter institutions that opted out of an ongoing class action lawsuit. She suggests this settlement may have some ominous implications for defendants in securities litigation going forward:

Is this the future for defendants accused of securities fraud: facing a multitude of far-flung suits by well-counseled, well-capitalized investment funds?

If so, the business lobby has only itself to blame. As you know, the U.S. Supreme Court put shareholders on notice in its 2017 ruling in CalPERS v. ANZ Securities that if they want to preserve their right to bring individual securities fraud claims, they have to file their own suits within the three-year statute of repose, even if there’s already a class action under way. The U.S. Chamber of Commerce, the Washington Legal Foundation, the Securities Industry and Financial Markets Association and the Clearing House Association all urged the justices to uphold the strict time limit for individual investor suits.

Alison says that the bottom line for institutions is that in light of ANZ Securities, if there are big bucks on the line, they’re likely to go their own way and opt out of class actions. And as this recent “D&O Diary” blog points out, that’s going to make everybody’s life more complicated.

Earlier this week, the Sustainability Accounting Standards Board published the first-ever industry-specific sustainability accounting standards. The standards are designed to enable businesses to identify, manage & communicate financially-material sustainability information to investors. Here’s an excerpt from the press release announcing the standards:

Covering 77 industries, the standards were approved on October 16, 2018, by a vote of the Standards Board after six years of research and extensive market consultation, including engagement with many of the world’s most prominent investors and businesses from all sectors. By addressing the subset of sustainability factors most likely to have financially material impacts on the typical company in an industry, SASB’s industry-specific standards help investors and companies make more informed decisions.

SEC Enforcement: Crypto & Cyber Remain High Priorities

Earlier this month, the SEC’s Division of Enforcement published its annual report. The report notes that the agency brought 821 actions and obtained more than $3.9 billion in disgorgement & penalties. It also returned $794 million to investors, suspended trading in the securities of 280 companies – and obtained nearly 550 bars and suspensions.

The annual report also says that Enforcement “remains focused” on ICOs & crypto scams – topics that this Fortune article notes didn’t even merit a mention two years ago. As this excerpt from the report highlights, cyber issues are also high on the priority list:

Since the formation of the Cyber Unit at the end of FY 2017, the Division’s focus on cyber related misconduct has steadily increased. In FY 2018, the Commission brought 20 stand alone cases, including those cases involving ICOs and digital assets. At the end of the fiscal year, the Division had more than 225 cyber-related investigations ongoing.

Meanwhile, this front-page Sunday NYT article compares enforcement actions filed during the last 20 months of the Obama administration and the first 20 months of the Trump administration and claims that enforcement activity has declined significantly. It contends that the numbers reveal a 62% drop in penalties imposed and illicit profits ordered returned by the SEC under the Trump administration in comparison to the Obama administration. The Times laid out its methodology – with which the SEC disagrees – in a companion piece.

Yesterday, Corp Fin updated 4 CDIs to address the implications of the SEC’s adoption of rule amendments increasing the number of “smaller reporting companies” (SRCs) eligible to provide scaled disclosure. The updated CDIs reflect the impact of changes in the size thresholds for SRC status on prior interpretive guidance.

Corp Fin also withdrew 4 CDIs addressing transition issues for SRCs, as well 2 obsolete CDIs relating to old Reg S-B and a misstatement in the original SRC adopting release concerning when SRCs would have to provide audit committee financial expert disclosure. Here’s the tally of CDIs that were updated or withdrawn:

3. Section 110. Item 303 — Management’s Discussion and Analysis of Financial Condition and Results of Operations:

– CDI 110.01 (withdrawn)(obsolete guidance relating to inapplicability of old Reg S-B provision)

4. Section 133. Item 407 — Corporate Governance:

– CDI 133.09 (withdrawn) (correction of misstatement on financial expert disclosure in original SRC adopting release)

5. Exchange Act Forms CDIs – Section 104. Form 10-K:

– CDI 104.13 (updated)

Check out this Cydney Posner blog for a more detailed analysis of the updated CDIs. And also see Cydney’s blog about how the NYSE has proposed changes to Section 303A.00 of the Listed Company Manual related to the exemption from the compensation committee requirements applicable to SRCs due to the SEC’s recent changes to the SRC definition.

ESG: Making Sense of the Current Landscape for Boards

This Skadden memo reviews the many facets of the environmental, social & governance (ESG) issues that boards are confronted with and offers insights into how boards can make sense of the current environment. ESG issues can manifest themselves in a variety of ways – including shareholder proposals, surveys from ESG rating services, investor proxy voting policies, ESG-based activism, and legislation. This excerpt provides some thoughts on how boards should approach those issues:

To borrow a phrase from then-Justice Andrew Moore of the Delaware Supreme Court, in his 1985 Revlon decision, directors would appear to have wide latitude — and responsibility — for dealing with ESG issues to the extent they represent matters “rationally related [to] benefits accruing to the stockholders.”

That said, it is incumbent on directors to do their homework and apply appropriate processes to establish informed decision-making regarding that key determination — which also will enable them to defend challenges to spending shareholder money on “causes” that not all shareholders may support and to demonstrate to the “new” shareholder constituency, ESG investors, the attention paid to the subject at the board level.

Beyond that, of course, are a myriad of other important and potentially difficult decisions that may be required. These may include: Whether, when, to whom and how to engage in outreach regarding ESG issues. Choosing among ESG matters. Deciding how, how much and when to spend company resources to support selected ESG matters. How and when to communicate choices made and actions taken.

While the stakes are higher than ever when it comes to decisions surrounding ESG issues, the memo notes that these ultimately are board decisions that – like any other – require the exercise of business judgment in the best interests of the company and its shareholders.

ESG: More Sustainability Disclosure Means Less Analyst Coverage?

I guess this falls under the heading of “no good deed ever goes unpunished” – but in any event, a new study from a group of B-School profs suggests that the price for providing additional sustainability disclosures may be a reduction in the number of analysts following your stock & lower quality coverage. This excerpt from a recent article on the study summarizes its findings:

As the number of environmental performance ratings for firms in their portfolio increases, analysts cover fewer firms and provide fewer and less timely revisions for earnings-per-share forecasts. The average number of firms in their portfolios dropped 14.2 percent or 1.1 firms. Revisions to earnings-per-share forecasts decreased 3.2 percent, and those issued within two days of quarterly earnings reports were down 1.4 percent.

The study concludes that the effects are greater for negative environmental concerns than for environmental strengths, and suggests that part of the problem may be in the lack of a standardized approach to this type of disclosure.

Speaking of standardization, this King & Spalding memo notes that a rulemaking petition has been filed on behalf of a group of institutional investors requesting the SEC to develop a “comprehensive framework for clearer, more consistent, more complete, and more easily comparable information relevant to companies’ long-term risks and frameworks” to provide clarity on ESG reporting for US companies.

Recently, the NYSE issued this proposal to change the price requirements for its shareholder approval rules so they would be similar to what the SEC just approved for Nasdaq. As noted in this Cooley blog, the NYSE proposal would:

– Change the definition of market value for purposes of the shareholder approval rule and

– Eliminate the requirement for shareholder approval of issuances at a price less than book value but greater than market value.

More on “Insider Trading: Congressman Allegedly “Tipped” Sellers”

A while back, John blogged about a federal grand jury indicting Congressman Chris Collins (R-NY) on a variety of fraud-related charges arising out of alleged insider trading. I just wanted to circle back to the case to highlight how an insider trading case can impact an entire family. As John noted, the case resulted in the Congressman’s son and father-in-law also being charged.

But they aren’t the only ones facing challenges. The son’s fiancee was suspended from appearing or practicing before the Commission as an accountant. For five years. She lost her job at PwC too. She is only 25 years old. And as noted in this article, her mother also had to pay some money to the SEC. Don’t do it. Don’t insider trade…

Audit Committee Disclosures: The Trends

From this report on audit committee disclosures from the “EY Center for Board Matters,” here are the latest trends:

– In 2018, 71% of companies disclosed the length of auditor tenure. In 2017, the percentage was 64%, and in 2012 it was 25%.

– Sixty-two percent of companies disclosed the factors used in the audit committee’s assessment of the external auditor qualifications and work quality, while in 2017 and 2012 the percentage was 58% and 18%, respectively.

– In 2018, the percentage of companies disclosing that the audit committee considers non-audit fees and services when assessing auditor independence increased to 89% from 86% in 2017. In 2012, 12% of companies disclosed this information.

– The percentage of companies providing an explanation for a change in all fees paid to the external auditor decreased slightly from 45% in 2017 to 44% in 2018, while just 10% of companies made these disclosures in 2012. However, in 2018 only 16% provide an explanation for a change in the audit fee itself.

Over the years, I have blogged many times about Evelyn Y. Davis – one of the more well-known shareholder proponents of all-time. I am sad to say that Evelyn passed away a few days ago. Here’s the press release from her foundation. This CBS News article notes she was a concentration camp survivor. Here’s a few of the things I’ve blogged about EYD over the years:

1. Shareholder Proposals: Evelyn Y. Davis (“Dougie” Version)

From 2014: I’ve vowed to step up my style of making videos – and one of my new styles is the jump-cutting that has made the Green brothers so successful. So see if you like this new version of my educational video about Evelyn Y. Davis:

2. Evelyn Davis: Your Stories

From 2016: I’m starting to collect anecdotes about Evelyn – please send me your stories (as always, I won’t share them with attribution unless you give me permission). Here’s the first batch:

– You are aware of her prostitution arrest at the United Nations (sexpionage is what the press called it) and her “business services” at a Lexington Avenue hotel in New York. Brief accounts in editions of New York Post and New York Daily News. This one comes from Jim Patterson.

– When my father was 94 last year and found out that Evelyn was still around and kicking, he was shocked – “that woman was old when I was young!” He was CFO of a company 40 or so years ago and had to deal with her. Mostly, he had to stop her from attacking his outside lawyer, who was a very good looking guy.

– I remember her and Donald Trump going at it at the Alexander’s meeting many moons ago.

3. A Podcast with Evelyn Davis’ Former Husband

From 2016: In this podcast, Jim Patterson discusses the life of his former wife, Evelyn Y. Davis, including:

– Can you tell us about Evelyn’s childhood? For example, how did Evelyn’s childhood arrest with her mother and brother by the Nazis in Amsterdam in the final months of WWII affect her life?

– How did you meet Evelyn?

– Can you tell us a story to illustrate how Evelyn felt about her activism work?

– Can you tell us a story about how Evelyn liked to stir it up sometimes at annual shareholder meetings?

– What was her “contribution” to financial reporting/journalism?

– I know Evelyn was active with charitable efforts. Can you tell us about that?

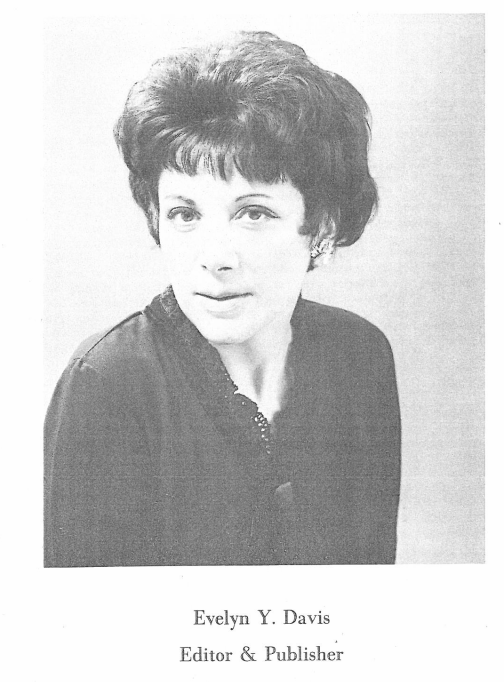

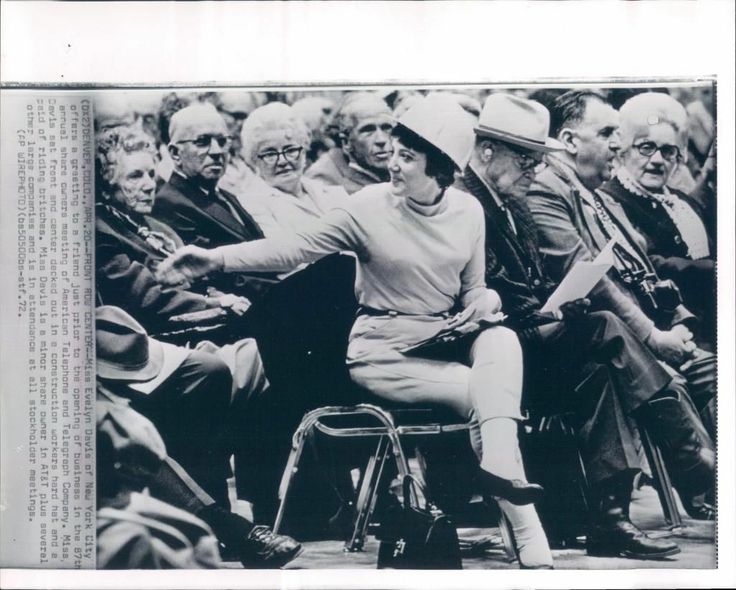

4. Evelyn Y. Davis: The Pictures

From 2016: Please send me your pictures of EYD too! From Jim Patterson, here’s a pic of Evelyn from her 1st issue of “Highlights & Lowlights”:

Here’s EYD at a 1972 AT&T annual shareholders meeting:

5. Evelyn Y. Davis: Retired?

From 2012: For many of you, the news that Evelyn Y. Davis is slowing down at age 82 will come as a mid-proxy season boost. As noted in this Reuters article, Evelyn has been skipping annual meetings this year – and even has halted production of her 47-year-old self-published newsletter “Highlights & Lowlights,” a $600-an-issue review of her governance battles that regularly features photos of her with bemused CEOs. Although Evelyn still has been submitting shareholder proposals to companies, I haven’t heard of her actually attending a meeting for the past two years.

For those of you who have never had the pleasure, go ahead and ask an old-timer for their favorite EYD story. Many of them are unsuitable for print in this family blog. I do note that she is partial to men, particularly if they are CEOs of a Fortune 50 company. Evelyn always had remarkable success with access to the powers that be – and making the CEO available to her often was a wise decision as it made it more likely that she wouldn’t turn your shareholders meeting into a complete spectacle. One day I’ll collect stories to post (including my own). I do note that Evelyn has been quite a philanthropist over the years, particularly in the effort to preserve Chicago history.

Until I post some stories, you’ll have to live with this great WaPo piece from ’03 – and this picture of Evelyn’s pre-bought tombstone in DC (I believe its two divorces behind):

A few months ago, I blogged about the dominance of white people in our industry. I heard some nice feedback. But I particularly liked this one from Carl Hagberg because he offered these concrete suggestions:

I agree that boards – and white people in general – are afraid to talk candidly about race and this needs to stop. In response to your request for ideas, here are a few things that enlightened companies can be doing about it:

– A growing number of companies have been demanding that the law firms they use must have a significant percentage of women and minority group members on the teams for every single company project they are awarded. Many law firms are struggling hard with this – which is precisely the point.

– Smart companies are bidding-out a growing percentage of their legal work – and not only demanding the same degree of diversity for the teams assigned to their projects, but awarding extra points in the evaluation of bids for pro-bono work – where it is easy to specify that diversity efforts and pro-bono work with minority groups will receive extra “extra points.”

– Companies should also be demanding – and rewarding strong diversity efforts – and actual results – at ALL of their service suppliers – like transfer agents, proxy solicitors and advisors, financial printers. And yes, in the selection of Inspectors of Election too.

I know that is extremely hard to diversify. I know from my own experience how hard it is – and why. Take a look at my article about “The Prevalence of Old White Men at Shareholder Meetings.” But if the clients don’t push harder for change, nothing WILL change!

And then Jenner & Block’s Jolene Negre sent me these common approaches:

– Mansfield Rule – Consider diverse candidates for open leadership positions (including board seats)

– Diversity training to give boards the tools they need to think and talk about race as it relates to their businesses

– Some major companies offer financial incentives to law firms staffing those companies’ matters with diverse legal teams (and penalize firms that do not)

“UTBMS”? What The…

Are “matter codes” frustrating – or practical? A new manual – “Best Practices for Using UTBMS Codes for Merger & Acquisition Transactions” – shows how codes can be used in the deal space. Having not been in a firm now for decades, I had no idea what “UTBMS” was. And my initial response was “there needs to be a manual for this!?!”

But I asked around – and here’s what I learned. “UTBMS” stands for the “Uniform Task Based Management System.” It’s how many big company clients wants you to enter your time now so that their outside consultants can flyspeck everything you bill – and it can be helpful for GCs who love all this data analytics stuff. It takes forever to enter your time now – client, matter, service code, and then an individual task code. If you talk with a client on the phone, you’ve got to enter code 9915, “Communicate (with client)”. You need to break down everything you do into these task codes e.g., “Review and Analyze,” “Research,” “Communicate (in firm),” “Communicate (opposing counsel).”

The list is endless – and god help you if you combine two service entries into a single code. The activity codes are useless for transactional work, but you still have to use them. Sounds like it’s not much fun… but that some firms have fully embraced project management now (see “SeyfarthLean” web page)…

ESG Risks Influences Foreign Sovereigns Ratings

As noted in this report, Moody’s says that changing environmental, social & governance considerations can affect sovereign ratings. Moody’s report points out that – while ESG is often spoken of as a single, homogeneous category of risk and while the three overlap in some respects – they are also quite distinct from one another. Of the three E, S and G risks, G has the strongest quantitative relationship with both sovereign ratings and Moody’s four methodology factors: economic strength, institutional strength, government fiscal strength, and susceptibility to event risk.

Here’s another “list” installment from Nina Flax of Mayer Brown (here’s the last one):

Before I begin this list, I am going full “open kimono” on some of my crazy here. My husband counted a while ago the number of books I had bought for our son – at the time I think we were still under 1000. We have two shelves in his closet that are taken up by “closet books” (i.e. books for him when he is a bit older), we have three book shelves in his room for books, we have three ledges in his room covered with books, we have two baskets around his reading chair in the hallway upstairs filled with books, we have books in various places in his playroom, we have two baskets downstairs with books by his work table, we have board books all along our fire mantle and another area in our living room storage area with more books.

I love books and I want my son to love books. And I love having so many options for books always in the house because (i) I love reading to my son and (ii) I feel personally satisfied by reading stories to him when I don’t have the bandwidth at the moment to read my own long books. I am fully aware that this is an addiction – I am okay with that.

As for what I consider Amazon “stalking” – (i) it is on a wish list, (ii) I regularly check that wish list, (iii) I monitor for price drops, (iv) I consider when checking my wish list whether to purchase the item, (v) I sometimes read updated reviews/see if another newer product should replace the stalked product on my list, etc. However, books are rarely replaced or removed from lists.

1.Gail Gibbons Books: If you have kids and haven’t read How A House Is Built, you should read it; I have read it about 100 times (not kidding – it is a popular and ongoing request). Gail Gibbons is an author I came across when looking for train books, and we now have over 15 of her titles. They are entirely digestible for children, but fun for adults too, and always well illustrated. I have a separate “Gail Gibbons Wish List.”

2. Other Children’s Books: For this category of things I stalk, I actually have three wish lists – “Most Desired Books,” “Science Books” & “Other Books”. I really am not kidding. I check “Gail Gibbons” and “Most Desired Books” frequently to see if any prices have dropped – and books only make it on my Most Desired Books if I have read them or watched a YouTube video of someone else reading them or am reasonably confident that I will definitely like them (e.g., in Spanish and written by an author that I have already purchased books from).

3. Books for Me: Paper copies are usually on the “My Most Desired Things” wish list. I am currently obsessed with the Taschen Basic Art Series. Also, every time I hear about a book I think I might want to read, it gets added to my “Kindle Books” wish list or my “Work Books” wish list.

4. Random Things I Think I Might Want But Don’t Want to Spend Money On (Yet): Which either fall on the “My Most Desired Things” wish list or my “Other Things I Might Want” wish list (the former checked more frequently because, as mentioned above, it also includes books, the latter checked less frequently because it does not include books). These include refillable dental floss made from silk, a wood rotating Scrabble board, a larger Klean Kanteen coffee mug (the one I have definitely is too small for my caffeine addiction, and they have cool new caps), a Buddha Board, puzzles that are beautiful and hard, a tagine, and an under desk elliptical (it has good reviews, and I do have a standing desk…). I promise that the way I have things grouped makes sense (to me).

5. Survival Supplies: I am not a doomsday survivalist, but moving to California and shortly thereafter experiencing two minor earthquakes during the night has made me curious about supplies. I stalk the more “normal” ones that I might actually use, like a hand crank back-up power turbine or a medical kit, as well as those that if I camped might make sense but maybe could be included in a birthday or father’s day gift for my husband, like a stormproof match kit or wound sealing powder or sponge.

6. Socks: I have supported and continue to support a local non-profit that provides assistance to homeless pregnant women. They are always in need of supplies for the babies and siblings, and in the winter (even though it is not THAT cold here), what could be better than knowing you helped someone have warmer feet? I can regularly find good quality socks for under $1.00/pair because of my “Socks” wish list.

In case this wasn’t apparent, one of the reasons I love stalking on Amazon is because I have so many lists, and regularly create new wish lists, move things around, delete old ones, etc. It is list heaven. It used to have a cherry on top, but then Amazon deleted the ability to filter by discount – I am still not pleased and hoping they bring that function back.

We continue to post new items daily on our blog – “Proxy Season Blog” – for TheCorporateCounsel.net members. Members can sign up to get that blog pushed out to them via email whenever there is a new entry by simply inputting their email address on the left side of that blog. Here are some of the latest entries:

– Proxy Advisors: Six Senators Support House Bill

– Another Year, Another No EYD

– ISS Summary: How Proxy Season Is Faring

– How Blockchain May Be Used in the Proxy Process

– Communicating Culture: Amazon’s Shareholder Letter

Yesterday, the SEC adopted rules to update how mining companies disclose their “property” – including how they disclose mineral resources & reserves – so that the SEC’s requirements are closer to what is required globally from mining companies. Here’s the SEC’s press release – and the 453-page adopting release.

The old rules – including the now-obsolete Guide 7 – permitted the disclosure of non-reserve estimates only in limited circumstances. But that will now change. There is a two-year transition period so that mining companies won’t need to comply with the new rules until its first fiscal year beginning on or after January 1, 2021. We will be posting memos in our “Mining Companies” Practice Area.

Say-on-Pay: Rite Aid With a 84% Vote “Against”!

As noted in this Bloomberg article, Rite Aid received a 84% vote ‘against’ on its say-on-pay. I was pretty sure that was a record low…but surprisingly, it’s not even the leader in the clubhouse for 2018! For example, Nuance Communications got only 10% in favor. Some bigger names also got clobbered – Wynn Resorts was at 20%, and Bed, Bath & Beyond was at 21%…

Our November Eminders is Posted!

We have posted the November issue of our complimentary monthly email newsletter. Sign up today to receive it by simply inputting your email address!